metamorworks/iStock via Getty Images

We believe Veeva Systems (NYSE:VEEV) is a stock to consider for long-term investors willing to hold shares beyond five years. The sentiment toward the stock could change materially depending on the time horizon of the investment. For instance, an investor buying the stock now with a time horizon of fewer than five years might consider it to be expensive. On the other hand, an investor buying shares now with a buy and hold strategy beyond five years might consider it relatively attractive, if they are willing to increase their position gradually as the stock price keeps going down in the short term. Let’s dive into this interesting company.

Business Model

Veeva serves 1,205 clients as of January 2022 mainly from the life science sector, ranging from the largest global pharmaceutical and biotech companies to emerging growth pharmaceutical and biotechnology companies. Veeva supports them in bringing products online faster with more efficiency, as well as marketing and selling effectively considering the compliance required by government regulators.

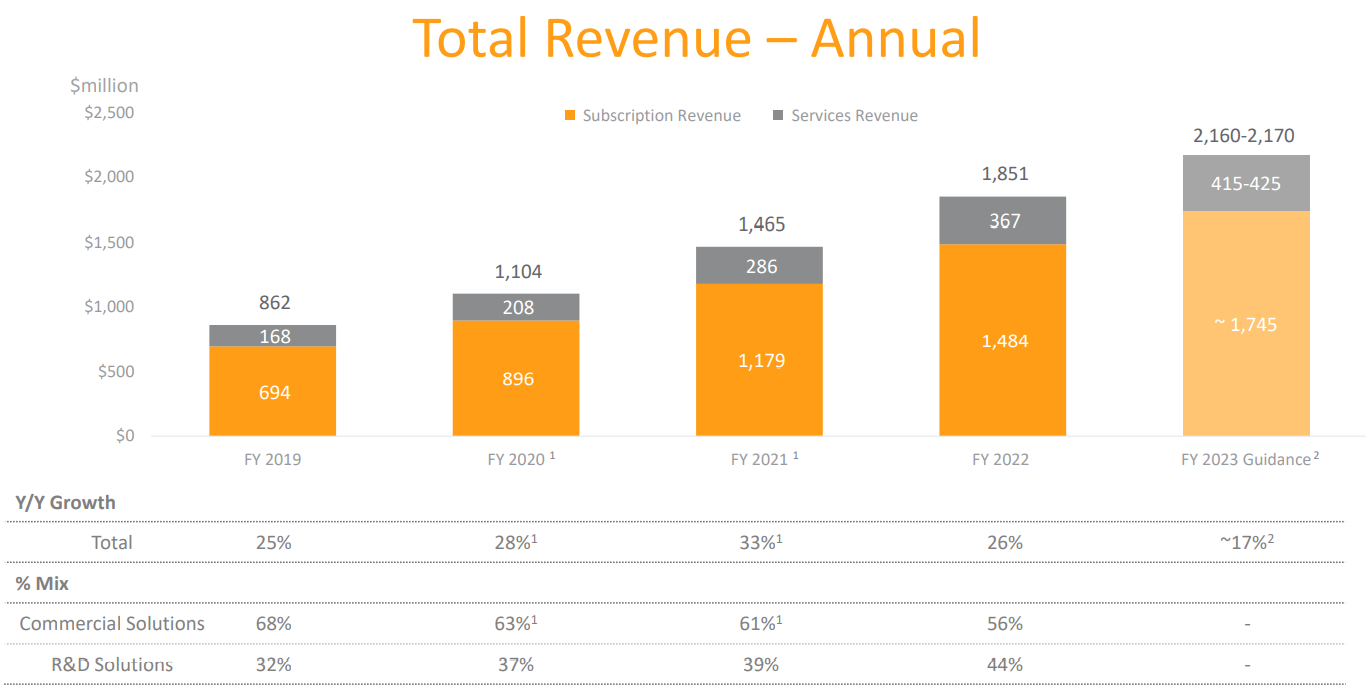

We can see that in the revenue breakdown for subscriptions and professional services for FY 2022, subscriptions have represented around 80% of the total revenues consistently over the years. That gives the company significant stability and predictability for its projections, and a better planning process for its resources.

Veeva Investor Day

Subscriptions have a collection of software oriented toward Commercial and R&D solutions. R&D solutions is a smaller business line, but it grows faster than Commercial solutions, which is more mature.

Veeva Investor Day

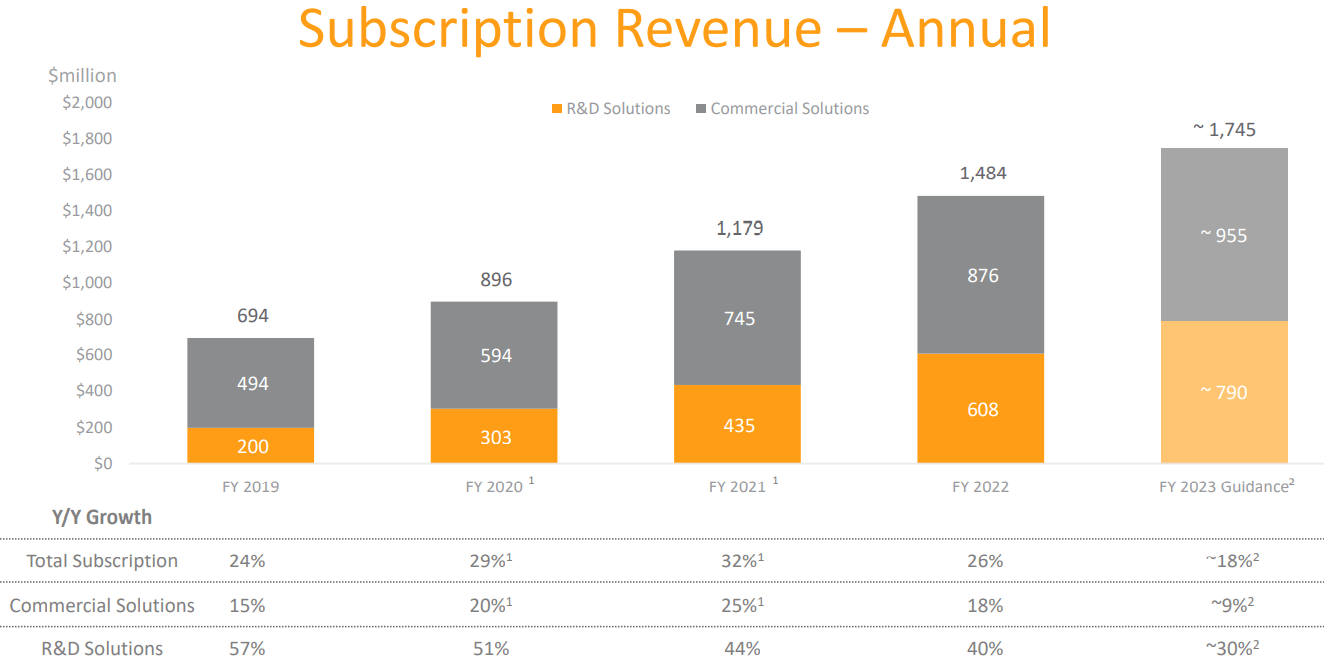

Commercial solutions include a collection of software grouped into Veeva Customer Relationship Management (CRM) and Veeva Medical CRM that help sales representatives track, manage, and optimize engagement with healthcare professionals with one integrated solution.

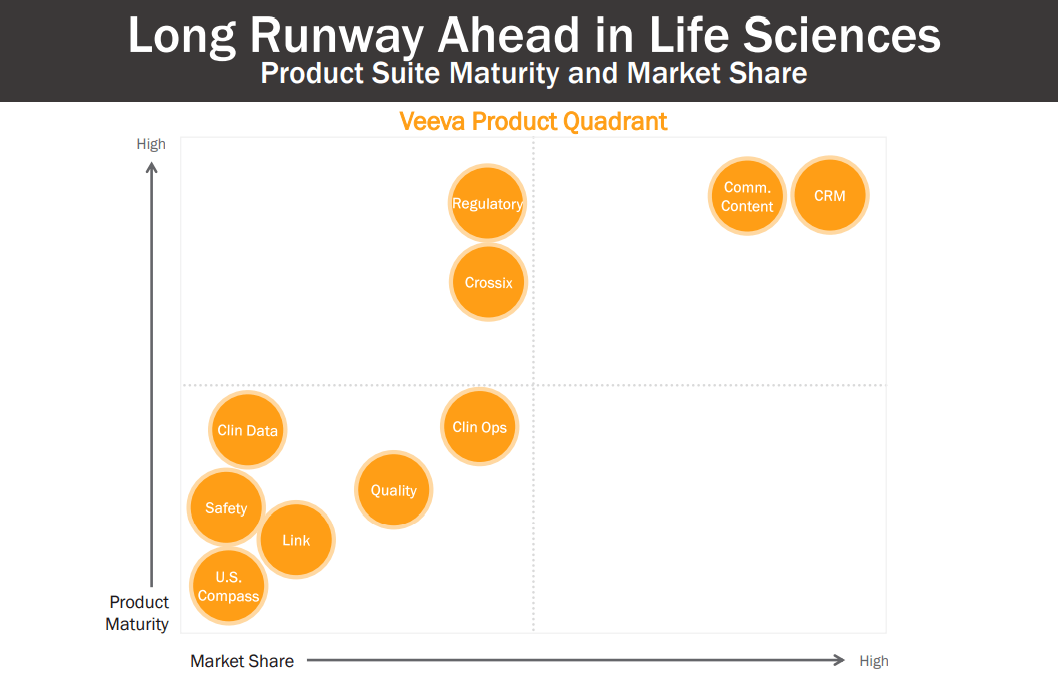

The R&D solution bases its faster growth on a collection of software grouped into Veeva Vault Clinical Suits and Vault Clinical operational Suits, which include solutions such as Clinical Data Management Suite (CDMS), Electronic Data Applications (EDC), Clinical Data Base (CDB), Randomization and Trial Supply Management (RTSM), Electronic Master Trial Master File (ETMF), etc. This software is becoming a game changer in terms of the traditional process in the clinical trial field, which is part of the long-term drivers for growth that we’ll mention later.

Guidance for 2023 and Beyond

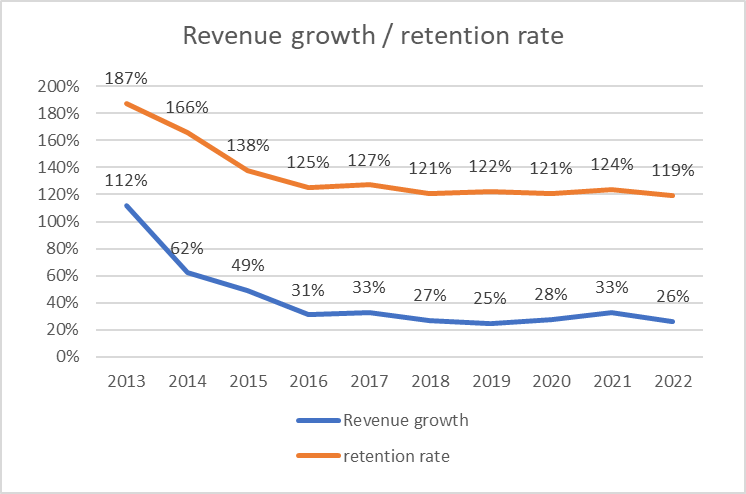

Looking the latest revenue growth of the company, Veeva is experiencing a deceleration in its revenue growth, which could have influenced the current stock price. However, Veeva’s guidance for 2023 still expects 17% revenue growth. Even though management has not mentioned a path forward for future years, we might see that the company could still offer double-digit revenue growth as its retention rates have been high and stable over the last few years:

Author

A retention rate above 100% indicates that Veeva’s clients are demanding more products from the company over time. A retention rate of 120% indicates that Veeva’s software is very successful among clients, which reinforces the stickiness of these applications. This very good level of retention rate indicates that there are a strong competitive advantages for Veeva, and that there is still room for growth for the company.

Now, let’s look at the other long-term drivers that might be good catalyzers for future growth.

Main Long-Term Drivers for Growth

Clinical Data Management

In regard to Clinical Data Management, the traditional process is very expensive with long lead times. Clinical trials are a critical stage in the process of launching new medical drugs. Using Veeva CTMS, which is part of the Veeva Vault Clinical Suit, clients will run studies end to end on a single platform that’s able to execute clinical processes independently of the role in the trial. Veeva has already signed up 40 Contract Research Organizations (CRO) to use its tools for clinical trial management.

Furthermore, two of the top 20 largest companies in the sector have already selected Veeva’s EDC, which is one of Veeva’s larger applications and a core application for clinical data management. This application enables Veeva to sell more complementary applications and software like RTSM, patient reported outcomes, etc. Therefore, it is expected that more new clients will be using this application for the first time, as well as a gradual increase in demand for more software associated with this application in the near future.

This is a clear sign that the digitalization in clinical trials is becoming the norm rather than the exception.

Crossix

Management is focused on increasing the value of one of Veeva’s latest acquisitions, Crossix, the leader in privacy-safe patient data and analytics. It should provide an increase in functionalities, increased integration with Veeva’s other CRM products, and a move toward more multiyear agreements and enterprise license agreements with customers. This will provide a guideline for revenues and stability.

A Focus on Business Outside Life Sciences

During the Q3 earnings call, Veeva CEO Peter Gassner stated that the company is now more focused on large customers in consumer products and chemicals such as food, healthcare, cosmetics, and specialty chemicals. However, there are some restrictions in constructing those new avenues for growth with more freedom given the contractual relationship with Salesforce (CRM). This might explain why Veeva is migrating from Salesforce’s platform to its own platform – Veeva CRM Vault.

Moving From Salesforce to Veeva’s CRM Vault

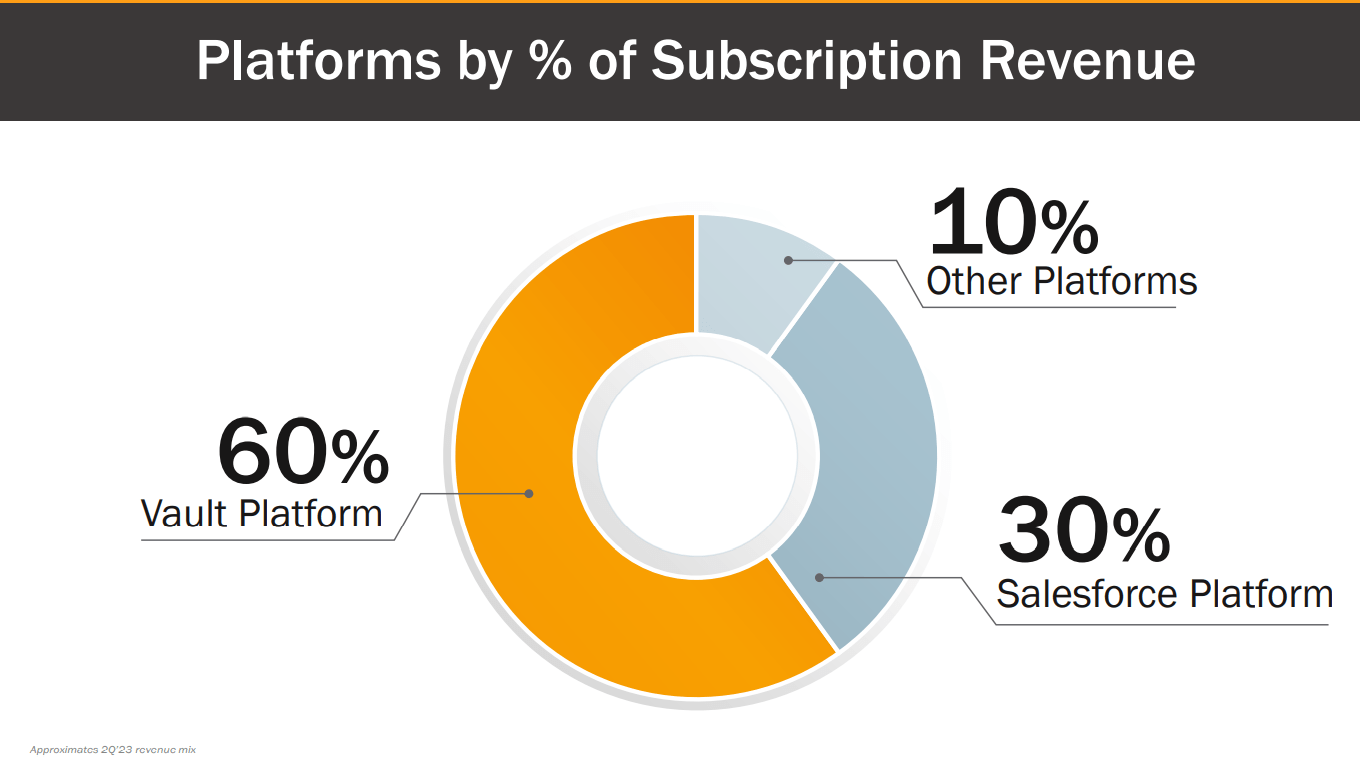

Most of Veeva’s subscription revenues are located in the Veeva CRM Vault, but there is still 30% of subscription revenue that comes from Salesforce’s platform:

Veeva Investor Day

Veeva has a significant portion of its CRM applications in Salesforce’s platform. The implication of this contractual relationship is that Veeva is restricted in the sectors where it can sell its software and applications, as mentioned in the risk factors of Veeva’s 10-K:

Our agreement with Salesforce provides that we can use the Salesforce Platform as combined with our proprietary Veeva CRM application to sell sales automation solutions only to drug makers in the pharmaceutical and biotechnology industries for human and animal treatments, which does not include the medical device industry or products for non-drug departments of pharmaceutical and biotechnology companies.

Veeva has a contract to use Salesforce’s platform that ends in September 2025, and a five-year winding down period during which Veeva might continue using the Salesforce platform combined with some of Veeva’s solutions to its customers. Nevertheless, during this five-year period there would be limitations on additional subscriptions Veeva can sell to its existing clients.

This might explain why Veeva is migrating toward its own platform before the end of the contract. This will create new opportunities for Veeva to get into those sectors that were not allowed under its contract with Salesforce, such as the medical device industry or products for non-drug departments of pharmaceutical and biotechnology companies. Furthermore, with this migration there will be better connectivity between applications, between R&D and commercial, between clinical, medical and commercial – all of which would enable Veeva to see better growth opportunities.

In regard to the migration to the Veeva Vault CRM from Salesforce’s platform, Gassner said (linked above):

We expect to have early adopters on the Vault CRM in 2024, some early adopters, and then the majority moving on 2025 or so, that’s when we’ll be selling mainly well CRM and customers will migrate over time. They have plenty of time.

This migration does not involve significant costs and the user experience will not change materially. According to Gassner, this move does not imply a rewriting of the code, but only a replatforming of the backend.

During the Q3 earnings call, Veeva management did not mention directly and explicitly that the company is preparing to get into those new sectors that were not allowed under the contractual relationship with Salesforce. We believe that’s because Veeva currently remains in this contractual relationship and there’s a good relationship between the two companies. But it’s clear that the actions taken by Veeva toward the goal of being independent from Salesforce’s platform indicate that Gassner is working to uncover new opportunities for future growth.

Long-Term Tailwinds for Vault Safety

Vault Safety is a collection of very complex applications created for the purpose of managing adverse events. During the same call mentioned above, Gassner said that Veeva is the first company to have all of this process as a cloud-native application.

There are two important things to know about this product: the first is the speed at which this product has been implemented, given the breakthrough it really means for the industry, and the second is the intrinsic complexity behind this product, which reinforces Veeva’s market position in the sector. As Veeva keeps developing improvements in these new and complex applications, it achieves a significant differentiation that generates higher stickiness over the long term.

After exploring these drivers and looking at the entire picture of Veeva’s products, we see a total addressable market of more than 13 billion for a company with revenues of $1.8 billion in 2022:

Veeva Investor Day

Now, to take advantage of these long-term drivers, Veeva will need a resilient business model, which is what we’re going to discuss next.

Resilient Business Model

The resiliency of Veeva’s business model is associated with the successful track record of its products and how critical these products are for clients. These factors are particularly important in very difficult scenarios with interest rates hikes, lower consumption, lower budgets, etc.

Furthermore, there is another factor that strengthens Veeva’s business model in those hard scenarios, which is the nature of the industry the company actually serves. Given the fact that Veeva supports life science companies in the launching of medicine to the market, Veeva is isolated, at least partially, from economic cycles. That’s because the demand for medicine and healthcare do not change materially during recession scenarios.

A big part of a company’s competitive advantages is outstanding management; let’s discuss this important factor next.

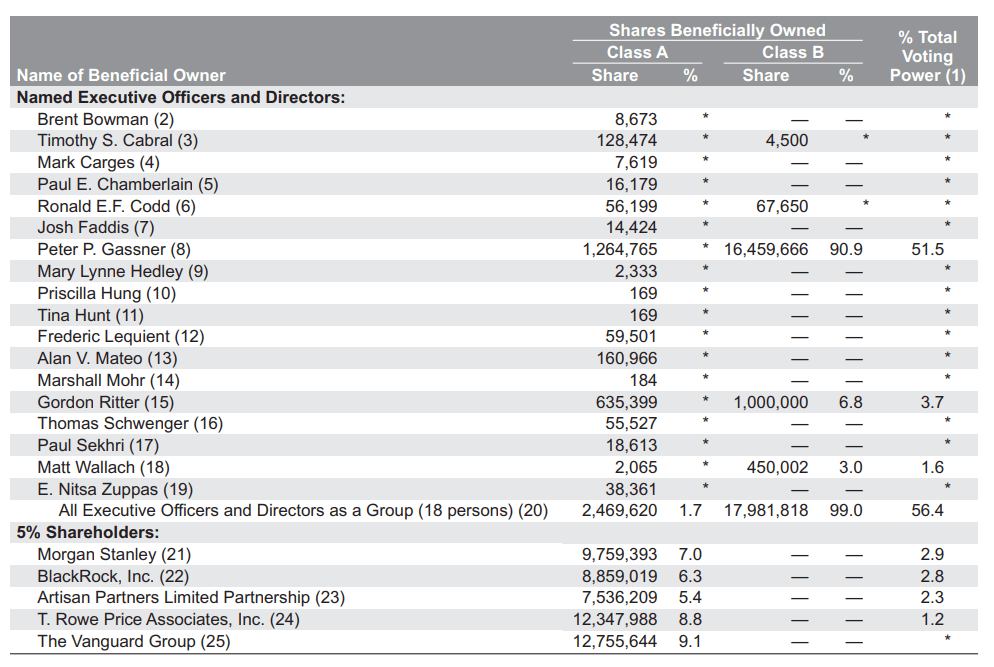

Investing in Veeva Is Investing in Peter Gassner

Gassner founded Veeva in 2007 and has 51.5% of the total voting power; as such, Veeva’s future will depend on Gassner’s ability to make shareholder-oriented decisions.

Veeva Annual Report 2022

Let’s focus on some of the acquisitions made by Veeva in the last few years to see if Gassner has overpaid for them. In 2019, Veeva acquired Crossix for $430 million, whose sales in that year were $62 million, meaning the multiple price/sales ratio was 6.94x. In the same year, Veeva bought Physician World for $41 million, whose annual sales were $20 million, meaning the multiple price/sales ratio was 2.05x.

Those multiples are conservative ones, which means that Gassner does not like to overpay for acquisitions. A benchmark could be another software-as-a-service (SaaS) company, Adobe (ADBE). It recently paid $20 billion for Figma, a company that generates roughly $400 million annually; that is a multiple of 50x sales, a very clear overpayment.

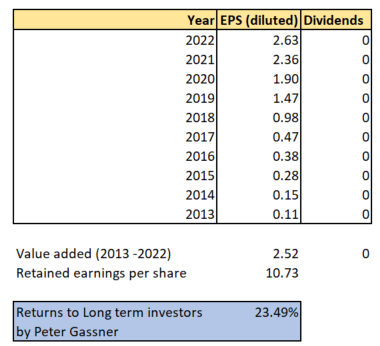

Another way to measure Gassner’s performance since the IPO of the company in 2013 is taking the difference of the diluted earnings per share (EPS) between 2013 and 2022 and dividing it by the total retained earnings in that period. This is a simple method that you can find in the book Buffettology, by Mary Buffett.

Author

So, the difference between 2022 EPS and 2013 EPS is $2.52 per share; the retained earnings are calculated by subtracting the dividends in each year from the EPS. Then, we sum up all the retained earnings for the period between 2013 and 2022:

annual returns for long-term investors = (EPS 2022 – EPS 2013) / sum of retained earnings

Thus, by $1 of retained earnings invested, Gassner has generated $0.234 or 23.4% of annual profitability for this period on average. At this level of profitability, it is understandable that the company does not pay dividends. On the other hand, Gassner has a long-term vision for the company setting long-term goals that push Veeva to be more innovative and creative to reach or surpass those ambitious goals.

Veeva has a manager who is the company’s founder with the majority of shares; as such, his interests are aligned with those of the rest of the shareholders. This is critical since we, as retail investors, expect that Gassner has clear incentives to deliver more value over the years.

Gassner’s performance and the alignment of his interests might help us to understand, at least partially, why the market is willing to pay higher multiples for the stock. Let’s now take a look at the valuation of the company.

Valuation

We’ll divide this calculation into two different investing strategies: 1) investing to hold the stock until 2026, and 2) investing to hold the stock beyond 2026.

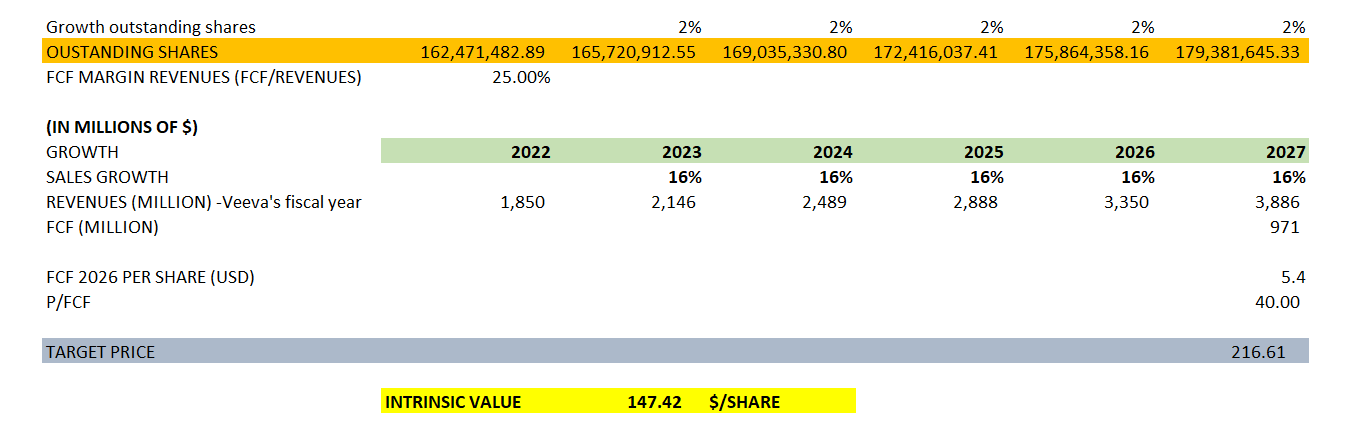

Strategy 1: Intrinsic Value for Holding Until 2026

We’ve made the following assumptions:

- Outstanding shares 2022: 162,471,482

- Annual growth of outstanding shares: 2%, based on the past 10 years

- Free cash flow (FCF) margins: 25%, based on the average from the past 10 years

- Revenue growth projections: 16%

- P/FCF: 40x; this metric ranged from 41x to 103x in the past eight years

- Veeva’s fiscal years: the fiscal year 2027 is 2026 for us

- Discounted rate: 8% is used to calculate the present value in 2023 of the target price in 2026; we use this to assume the discounted rate for high-quality companies

Under this strategy, we would buy the stock now and sell it in 2026.

Author

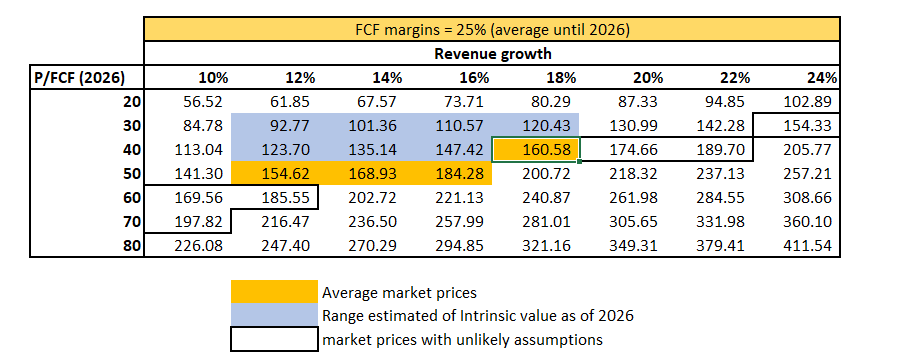

Although the intrinsic value appears to be below the current stock price, we’re assuming a revenue growth of 16% and P/FCF 2026 of nothing less than 40x. We need to perform a sensibility analysis to know what the market is assuming, with the current market price ranging between $151 and $190 in the last few months. This is particularly critical with respect to stocks trading at higher multiples, since they could experience significant volatility in their prices:

Author

All the numbers shaded in blue are the range of intrinsic values given different feasible growth rates and multiples P/FCF for 2026. These are my estimations of the intrinsic values considering feasible ranges of revenue growth for the next years.

The numbers closed in by a colorless square indicate market prices with unfeasible assumptions. For example, assuming a combination of revenue growth of 10% with a multiple P/FCF 2026 of 70x is unreal, or revenue growth of 24% with multiples P/FCF 2026 of 30x would not be feasible for Veeva either. The numbers shaded in orange are the range of market prices in the last months of 2022, so we may infer that the market is assuming future revenue growth between 14% and 18% for the next few years and multiples P/FCF 2026 ranging between 40x and 50x.

My range of intrinsic values in blue assumes more conservative multiples P/FCF for 2026 between 30x and 40x, considering that in the last eight years that multiple ranged between 41x and 103x. So, it’s clear that using a strategy of holding the stock until Veeva’s fiscal year 2027, or 2026 for us, shows the stock is most likely overvalued.

Why is the market assuming a P/FCF of 50x for 2026? Probably because, as we’ve seen previously, there is a strong alignment of interests between Gassner and the rest of the investors. The company operates in the healthcare sector, which is a very resilient sector in recession scenarios. The company has the ability to deliver more innovative solutions that reinforce its retention rates, and, perhaps, the majority of Veeva’s investors are in it for the very long term.

Strategy 2: Intrinsic Value for Holding Beyond 2026

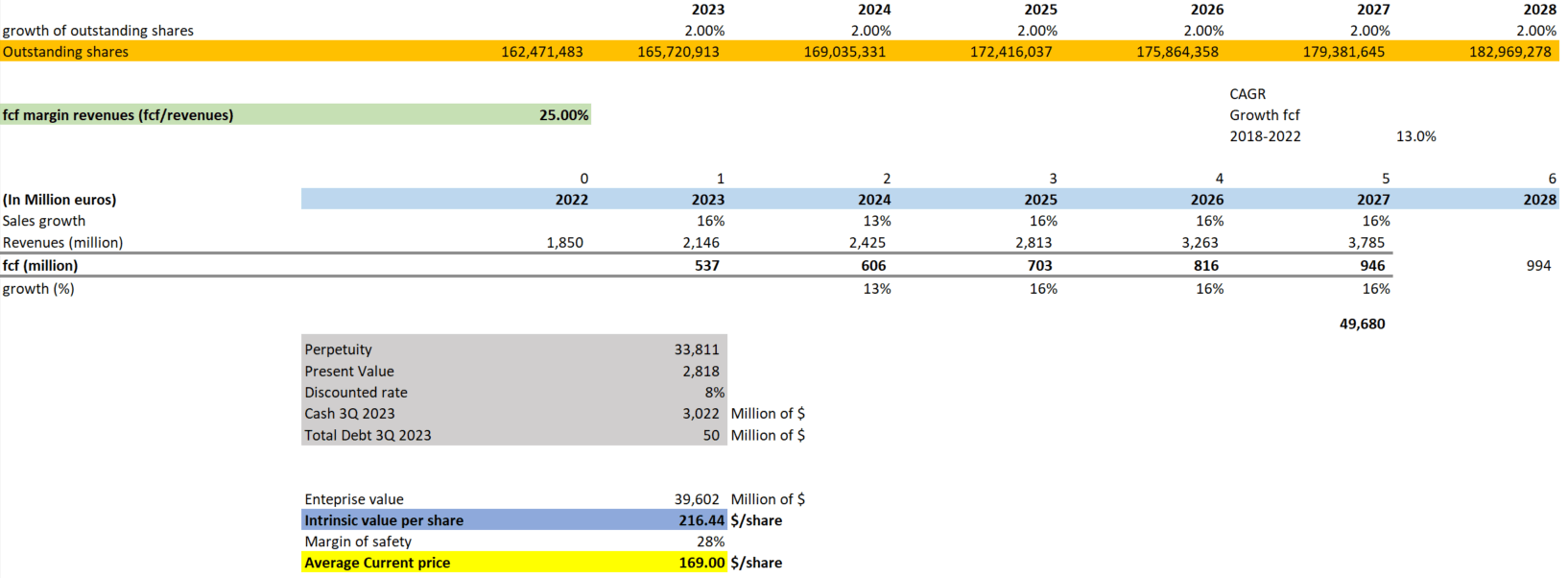

Let’s assume that we’ll hold the stock for the very long term, five to 10 years or more. These are the following assumptions for our discounted cash flow method:

- Outstanding shares: 162,471,482

- Annual growth of outstanding shares: 2%, based on the past 10 years

- FCF margins: 25%, based on the average from the past 10 years

- Revenue growth projections: 16%; 13% for 2024

- Growth of FCF in perpetuity: 6%, based on the compound annual growth rate (CAGR) of its FCF of 13% from 2018 to 2022

- Cash on hand from Q3 fiscal year 2023: $3,022 million

- Debt from Q3 fiscal year 2023: $50 million

Author

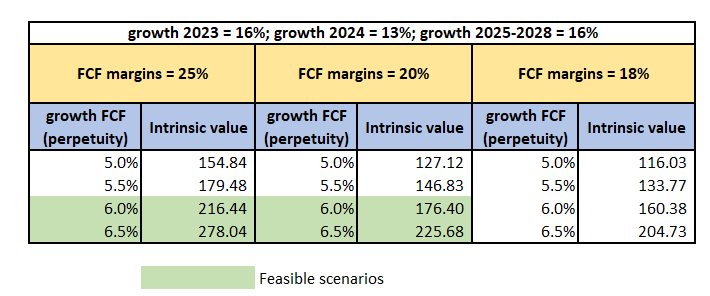

Now, if we create different scenarios changing our assumptions, we’ll get the following:

Author

Looking into these numbers in the area shaded green, Gassner would need to keep an annual growth of FCF for the long term of at least 6%, keeping the FCF margins at more than 20%. Those are totally achievable targets in the long term, even if we get into a recession scenario in 2023. Gassner already delivered a growth in FCF of 13% CAGR and FCF margins of 31% in average in the last five years, and 25% in average in the last 10 years. Increasing FCF margins and growth in FCF in perpetuity, Gassner might be able to push up the intrinsic value to $216, $225, or even $278 per share in the long term.

Under these conditions, with a very long-term strategy, we might say that the stock is undervalued. But it would be better to increase our margin of safety, taking advantage of any further drop in the stock below $165 to have a margin of safety of more than 30%. We should remember the long-term strategy for more than five years that we are assuming under this strategy.

Risks and Challenges

There are some risks and challenges that could affect the future valuation of Veeva.

The stock-based compensation of the company is growing faster than its cash flow from operations; this has the effect of increasing the outstanding number of shares by 2% on average year over year. We’ve incorporated this factor of dilution in both methodologies of the intrinsic value calculation. If that rate grows faster than 2% in the next few years, our calculation of the intrinsic value would be overestimated. Fortunately, this rate has been decelerating in the last five years: 0.93% in 2022, 1.58% in 2021, 1.37% in 2020, 1.39% in 2019, and 5.33% in 2018.

Saturation in the sector might be another factor that could slow down Veeva’s growth since most of its revenues are concentrated in global pharmaceutical and biotech companies. However, the number of clients are increasing year by year: 625 in 2018, 719 in 2019, 861 in 2020, 993 in 2021, and 1,205 in 2022. A bigger portion of this increase in the number of clients is the small and middle-size businesses (SMBs), a sector in which, apparently, Veeva does not have a strong competitive advantage as it does in the largest pharmaceutical sector.

The SMB is a sector that might suffer more by recession scenarios, combined with the fact that Veeva does not have a strong moat in this sector. SMB represents around 40% of Veeva’s overall revenues; in general, Veeva faces more competition in this sector, so its pricing power is more limited here. Nevertheless, Veeva has a very good internal culture organization that is frequently overlooked by investors and that has contributed to Veeva’s successful performance in recent years. Executing the “Veeva Way” encourages the company to increase complexity, deliver excellent and innovative products, focus on customer success – which is critical in shaping its competitive advantages in the SMB sector – and strengthen its reference selling, which means that early adopters are the best advocates for Veeva’s products and software. All of these sub-goals contribute to fortifying its main goal of generating strong growth and profitability over the long term.

Finally, Veeva has been in the process of litigation with IQVIA (IQV) since 2017 due to assertions of infringing intellectual property rights by Veeva. There are counterclaims and countersuits from Veeva that might significantly reduce any claim and suit from IQVIA. We’ll need to follow up on this litigation since it’s unclear when the final results will be, but we expect that whatever the result it will not materially affect Veeva’s growth prospects.

Final Thoughts

Veeva Systems is a very interesting company that deserves to be under consideration; the company serves a very specialized sector with high barriers to entry. In my opinion, if your strategy is to hold the stock for the long term, beyond five years, the long-term drivers will end up boosting Veeva’s market capitalization. As such, holding the stock for two or three years is not an adequate strategy, since we’re not giving the market much time to incorporate all of its drivers into the stock price.

We mentioned some intangibles here that are not frequently mentioned, such as the quality of management with a long-term vision, and the strong culture of the organization. We also didn’t overlook the high revenue growth in the last few years, the good growth prospects, and the barriers to entry of this very specialized sector. All of these factors might contribute to push up Veeva’s valuation in the long term, which strengthens our premise that a sound strategy for this stock is to buy and hold with a long-term view to take advantage of its compounding effect.

Be the first to comment