Matt Hunt

Always laugh when you can, it is cheap medicine. ― Lord Byron

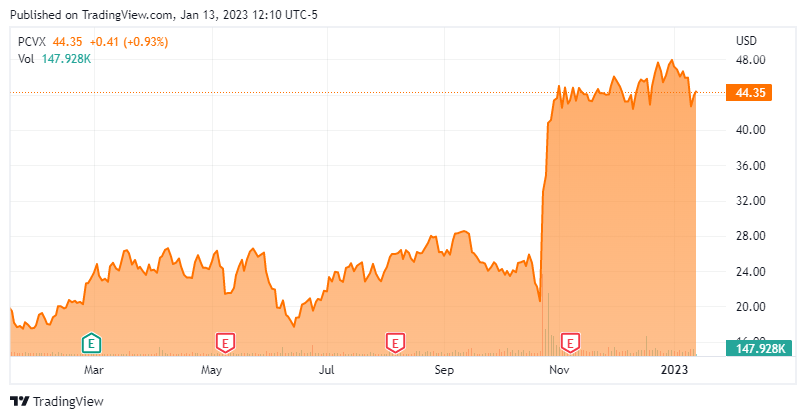

Today, we put Vaxcyte, Inc. (NASDAQ:PCVX) in the spotlight for the first time. The company has had a massive rally in its shares since late October thanks to positive news. Are further gains ahead or is the stock likely to see some profit taking in the months ahead? An analysis follows below.

Seeking Alpha

Company Overview:

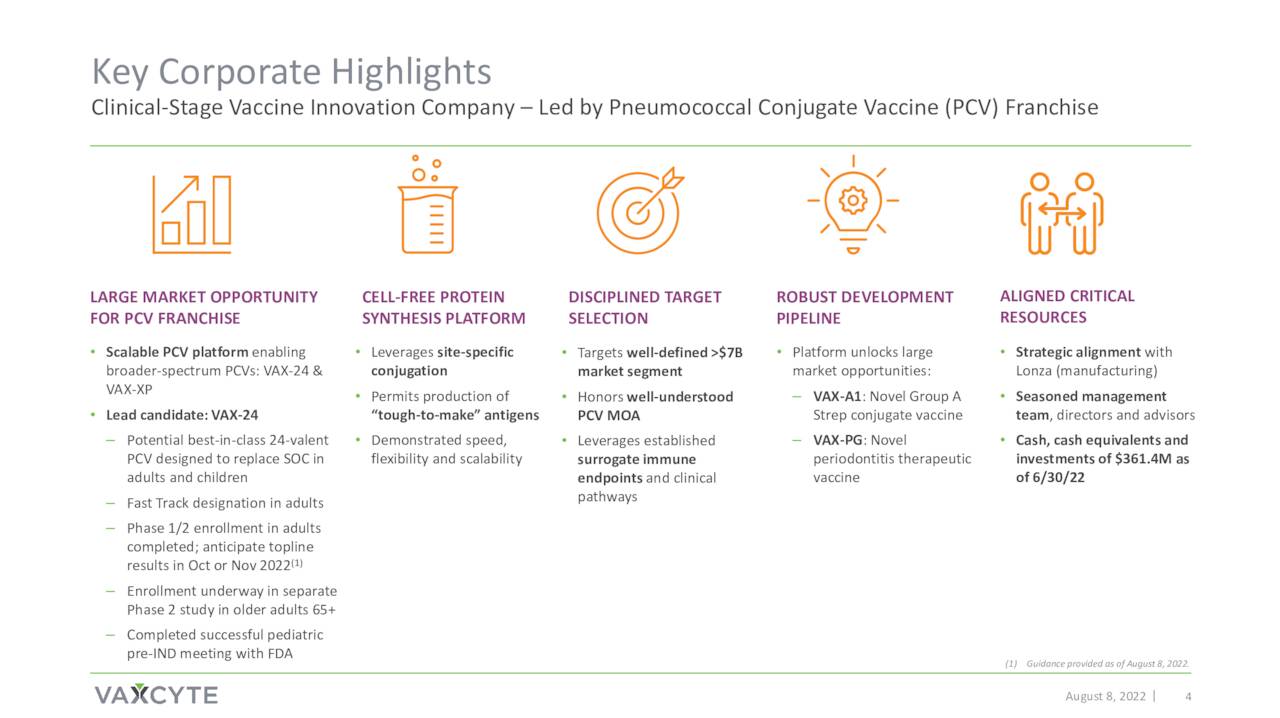

Vaxcyte, Inc. is headquartered just outside of Santa Clara, California. This firm is a clinical-stage biotechnology vaccine company focused on developing novel protein vaccines to prevent or treat bacterial infectious diseases. With the recent rally in the stock, the shares trade near the $44 level and sport an approximate market capitalization of nearly $3.5 billion.

August Company Presentation

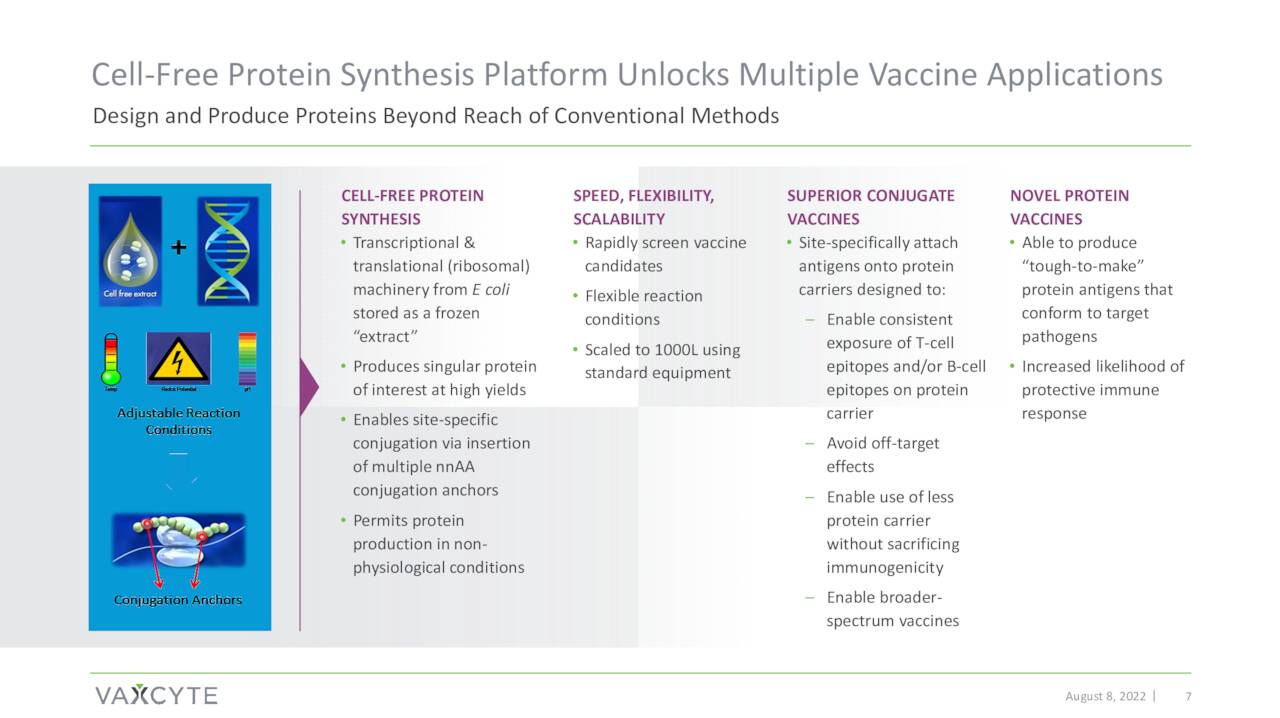

The company is using its proprietary XpressCF™ cell-free protein synthesis platform to create multiple vaccine candidates targeting various diseases including pneumococcal disease, Group A Strep and periodontitis.

August Company Presentation

The XpressCF process creates high-fidelity vaccines featuring distinct protein carriers and antigens which are the critical building blocks for vaccines.

August Company Presentation

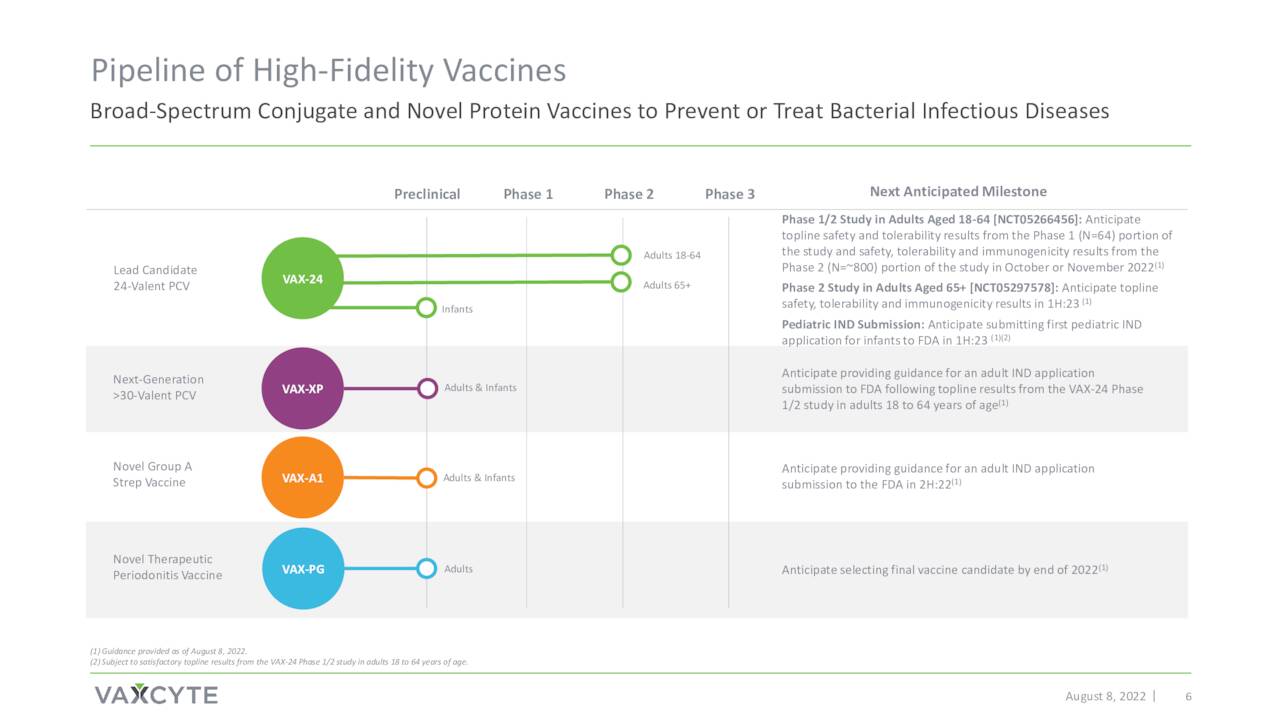

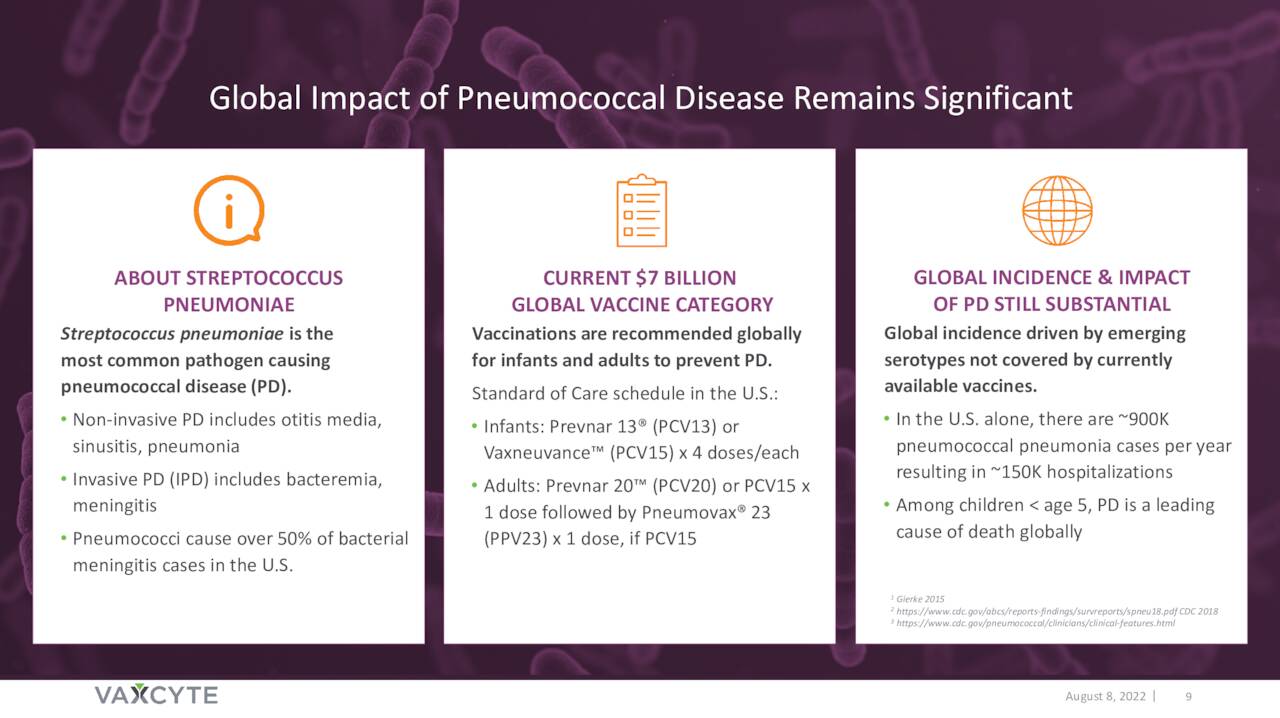

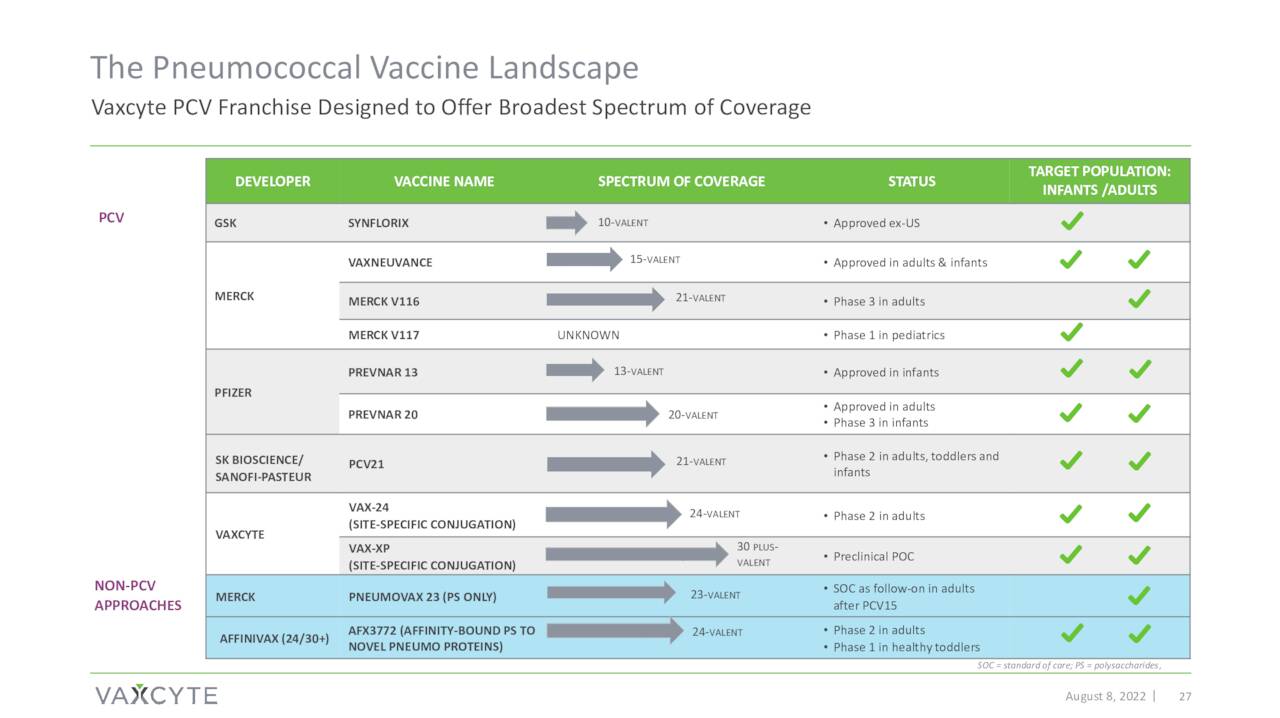

The company’s most advance effort is around Pneumococcal disease. This affliction triggers more than 4 million illnesses worldwide annually and BAML estimates the market at $7 billion. Pneumococcal disease is one of the leading causes of death globally for children under five. Approximately 900,000 people get pneumococcal pneumonia annually in the United States, resulting in 150,000 hospitalizations.

August Company Presentation

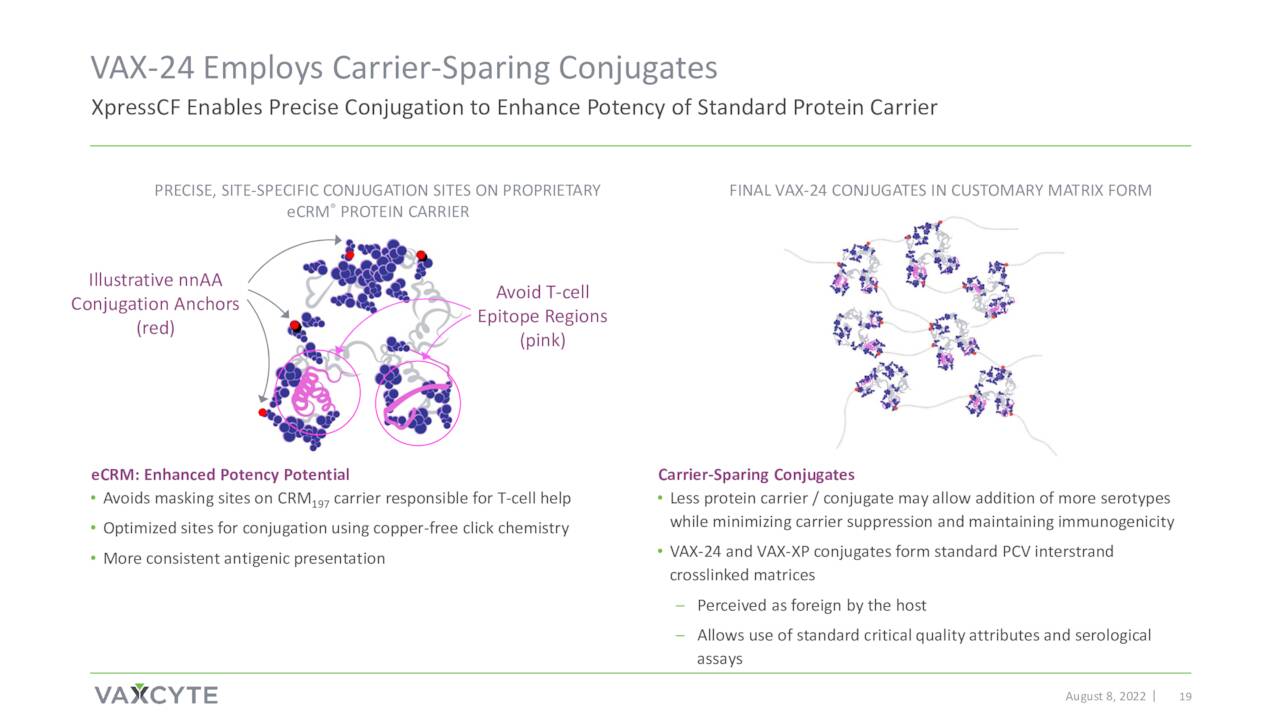

Vaxcyte’s pneumococcal conjugate vaccine or PCV candidate is named VAX-24.

August Company Presentation

The company’s other efforts are much earlier staged at this point. They are in the IND application stage of development and will not be germane to this analysis.

Recent Developments:

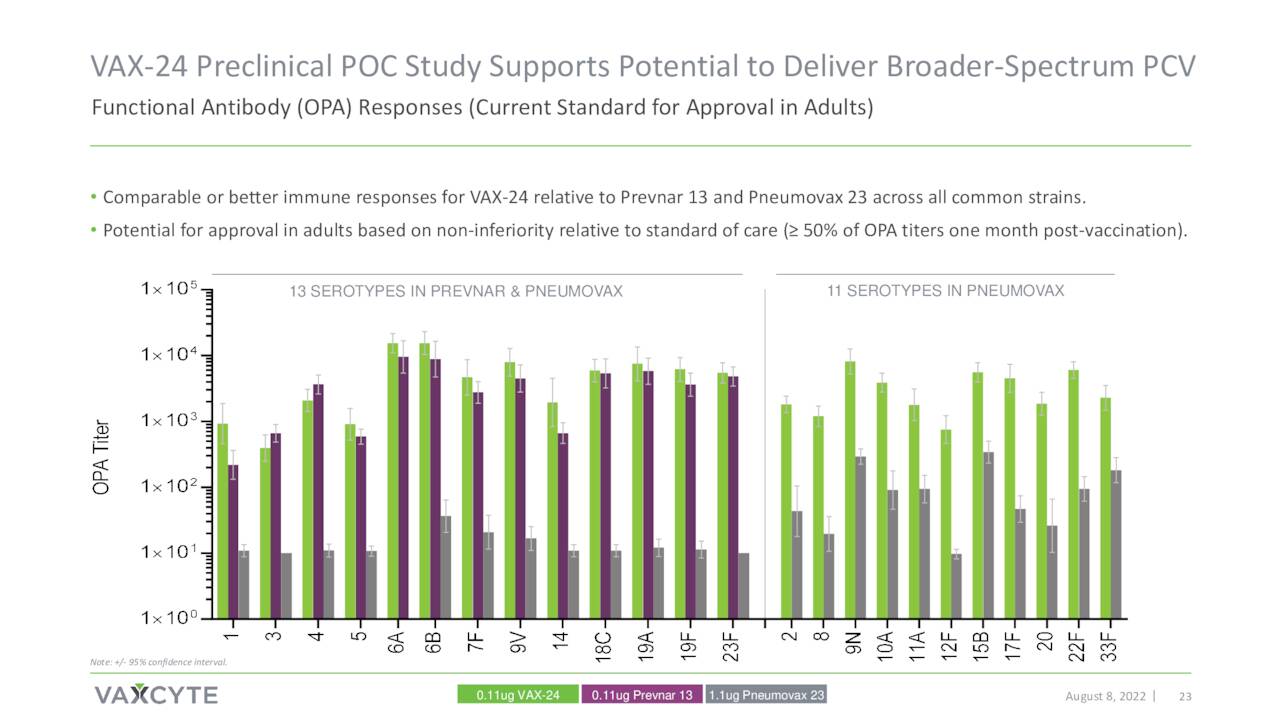

Phase 1/2 clinical proof-of-concept study around VAX-24 disclosed top-line data on October 24th. Data showed VAX-24 produced encouraging and in some cases superior results against some serotypes versus FDA-approved Prevnar 20 (PCV20) vaccine that was developed and now distributed by drug giant Pfizer (PFE). PCV20 was approved in the summer of 2021 as the latest version of the Prevnar franchise. This initial data has been the primary trigger of the roughly 100% rise in the shares since this news hit the wires.

Based on the results of this study, the FDA granted Breakthrough Therapy Status to VAX-24 on January 5th of this year. VAX-24 had already garnered Fast Track Designation for this indication.

Analyst Commentary & Balance Sheet:

Since early November, six analyst firms including Jefferies and BTIG have initiated or reissued Buy/Outperform ratings on the stock. Price targets proffered have ranged from $58 to $70 a share. Earlier this month, Needham bumped its price target on PCVX to $58 from $52 and added the equity to its ‘Conviction List’. Needham’s analyst cited ‘the company’s positive initial VAX-24 Phase 1/2 results released in October 2022, which he believes have significantly de-risked its VAX-24 Pneumococcal Conjugate Vaccine lead program‘ for the impetus for this action. Right after trial results came out on October 24th, Bank of America bumped its price target an impressive thirty bucks a share to $67 ‘citing an increase in the probability of success and peak market share for VAX-24‘ as the main impetus for its increased enthusiasm around the company’s prospects.

Approximately seven percent of the stock’s outstanding float is currently held short. Several insiders sold just over $1 million worth of shares in aggregate in the fourth quarter, but less than $15,000 so far in 2023. The company ended third quarter with just over $365 million of cash and marketable securities on its balance sheet after posting a net loss for the quarter of $57.9 million. In October, the company executed an approximate $660 million capital raise via a secondary offering. Vaxcyte has no long term debt.

Verdict:

August Company Presentation

There are some things to like about the investment case around Vaxcyte. It is developing a potential ‘best of breed’ PCV candidate aimed at a large and growing market. Pfizer’s Prevnar franchise does approximately $6 billion in annual sales. Vaxcyte also addressed its near/medium term funding needs as well.

August Company Presentation

That all said, the company’s near and medium term future will be determined by VAX-24 given the very early stage development of the other candidates in its pipeline. In addition, any potential commercialization is years away into a crowded, albeit large market. With the stock approximately doubling since those key trial results were posted, I don’t know if I want to chase that sort of rally.

August Company Presentation

Tolerability and immunogenicity data from a mid-stage study of VAX-24 in adults 65 and older should post sometime in the second quarter of this years. If the stock falls back due to profit taking to the mid $30s before then, I will probably act upon that opportunity to pick up some shares of PCVX. Until then, I think I will remain on the sidelines while watching this intriguing story continue to develop.

The art of medicine consists of amusing the patient while nature cures the disease. ― Voltaire

Be the first to comment