Bill Varie/The Image Bank via Getty Images

The fundamentals for oil are breaking down with the global economy increasingly set to be beset by poor economic growth, technical recessions, and emerging market sovereign defaults. The International Energy Agency’s January Oil Market Report predicts a substantial oil surplus in 2024 with surging oil production from US shale and new capacity from non-OPEC producers helping offset Saudi Arabia-led production cuts. Record output from the US, Guyana, Brazil, and Canada should boost global supply this year by 1.5 million barrels per day to a record 103.5 million b/d. Further, the additional voluntary OPEC+ production cuts of 2.2 million b/d brought in towards the end of 2023 look set to lapse from March and it’s not quite clear there will be an extension. United States Oil Fund (NYSEARCA:USO) invests primarily in listed crude oil futures contracts and is an accessible way for retail to play the commodity.

Trading Economics

Whilst the recent move by Saudi Arabia to reduce the official selling price of its flagship Arab Light crude to Asia was due to waning supply and demand dynamics rather than a policy shift by OPEC, the current Red Sea disruptions and Angola’s dramatic exit from the cartel, in my opinion, reduce the probability of additional voluntary oil cuts being extended beyond March. This opens up a pathway for WTI to trade down to around $60 per barrel from the latter part of spring. OPEC’s efforts to support oil prices above $80 per barrel since October 2022 have failed but also kept oil prices elevated versus underlying fundamental dynamics. The result is stickier inflation and elevated interest rates that have left economic demand muted and led to bleak forecasts for the state of the global economy in 2024.

Will There Be A Soft Landing For The Global Economy?

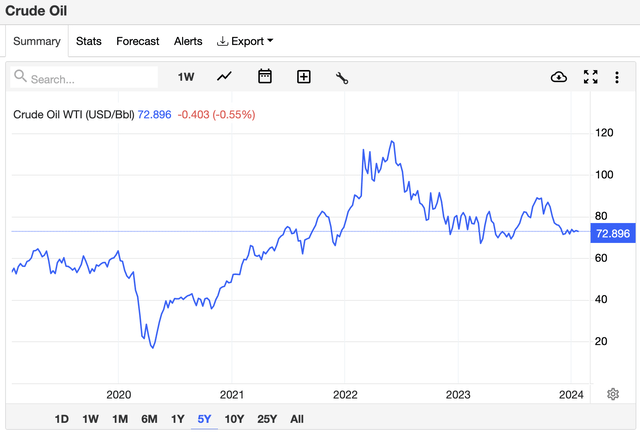

WTI oil, currently at $73 per barrel, would likely be lower without current geopolitical tension in the Middle East. Iran’s seizure of an oil tanker close to the Strait of Hormuz on the 12th of January set the backdrop of an extremely turbulent week of continued attacks against tankers and cargo ships in the Bab El-Mandeb Strait. To be clear, current geopolitical conditions are the most heightened they’ve been in decades. The current situation runs the risk of regional escalation, an outcome that would catalyze further oil upside. However, a reduction of tension aggregated with an end of voluntary production cuts forms the possible backdrop for a deterioration of oil prices. Critically, the base bull case for oil is now based on the continuation of extremes. Saudi’s push for voluntary production cuts was extreme enough to force Angola out of OPEC and perhaps runs the risk of further fracturing the cartel if pushed again beyond March.

Capital Group

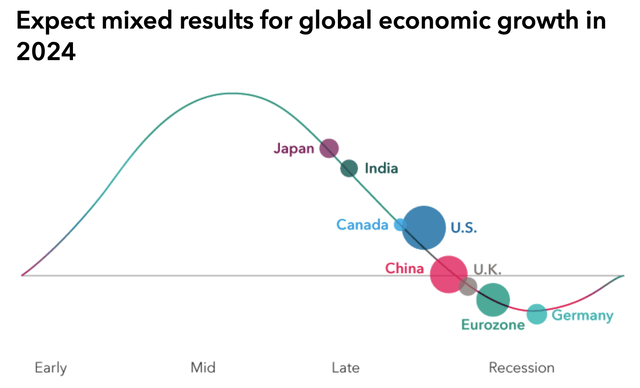

India, Japan, and the US economies are all set to be relatively bright spots in 2024 but China, the UK, and the Eurozone are all set to be laggards. The UK is forecast to enter a technical recession when their 2023 fourth quarter numbers are reported in mid-February with Moody’s predicting Chinese GDP growth slowing to 4% this year, down from an expected growth of 5.2% in 2023. The IEA report predicts that oil demand will grow this year by 1.2 million b/d, down by 1.1 million b/d from growth realized in 2023. Whilst oil bulls would be right to flag that OPEC’s estimates for oil demand growth in 2024 at 2.3 million b/d diverges significantly from the IEA’s, their forecast for growth to be equivalent to 2023 in a year when numerous economies are already flashing red and on track for a recession seems misplaced. Indeed, the World Bank is forecasting that both advanced and developing economies will experience slower growth this year than they did in 2023.

China’s Shanghai Composite recently plummeted to a four-year trading low with its housing market still in crisis as the liquidation hearing for Evergrande is set to commence on the 29th of January after two delays following the failure of the world’s most indebted developer to agree a restructuring deal with its creditors. A liquidation order event would constitute a black swan for the Chinese economy and threaten to lower growth estimates for 2024 on possible contagion. However, one of the most important factors for oil this year continues to be the explosive growth of US shale production. This formed a salvo for oil bears in 2023 by defying expectations of a slowdown as it helped the US extend its position as the largest global producer of oil at roughly 13 million b/d. This helped push OPEC+ market share to about 48%, its lowest level since 2016. OPEC+ will likely maintain their October 2022 production cuts but a future where the 2023 voluntary cuts are kept beyond March will almost certainly mean further market share loss against lower prices if geopolitical tensions have lightened.

Be the first to comment