Russia, Ukraine, Ruble, Bank of Russia, USDRUB, Sanctions – Talking Points

- Russian FX exchange reserves rise for week ending April 1

- USDRUB has traded back to pre-invasion levels

- Sanctions continue to hamper Russian economy, default odds remain high

Russian foreign exchange reserves rose for the week ending April 1, but reserves remain below established levels prior to the country’s invasion of Ukraine. The Bank of Russia valued FX reserves and gold at 606.5 billion, an increase on the previous week’s reading of $604.4 billion. In the week prior to Russia’s invasion of Ukraine, foreign exchange reserves totaled roughly $643 billion.

The figures show a stark decline in reserves as the West has hit Russia with tough sanctions over the last few weeks. Russia lost access to nearly half of its reserves, but the country’s central bank (CBR) has been able to halt the slide in the ruble. The CBR elected to double it’s key interest rate to 20% in late February, while also imposing strict capital controls on domestic companies and citizens. These controls have stabilized the ruble, which has returned to pre-invasion levels.

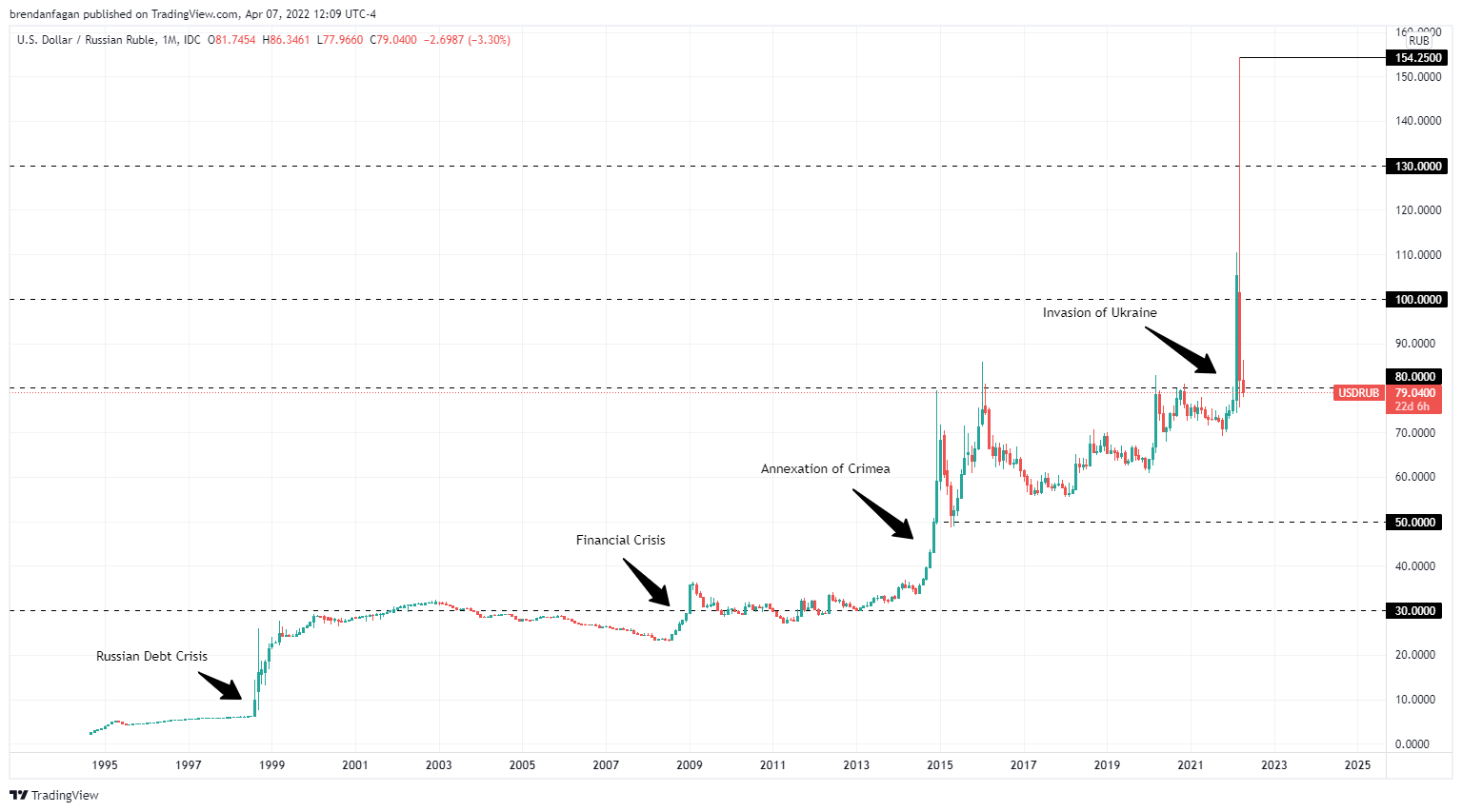

USDRUB Monthly Chart

{kind=link}

Chart created with TradingView

Despite being cut off from the West, Russia is still expected to rake in roughly $320 billion from energy exports this year. The recovery has come amid the lightest trading volumes in nearly 10 years, which has prompted some to hint that the exchange rate is “no longer floating.” Strict controls on capital flows and currency conversions may be masking the true damage to the ruble. Some experts believe that current levels of USDRUB reflect the highly manipulated domestic market, which has operated for weeks now with little to no foreign investors. However, a prolonged current-account surplus fueled by robust energy exports could continue to bolster the ruble.

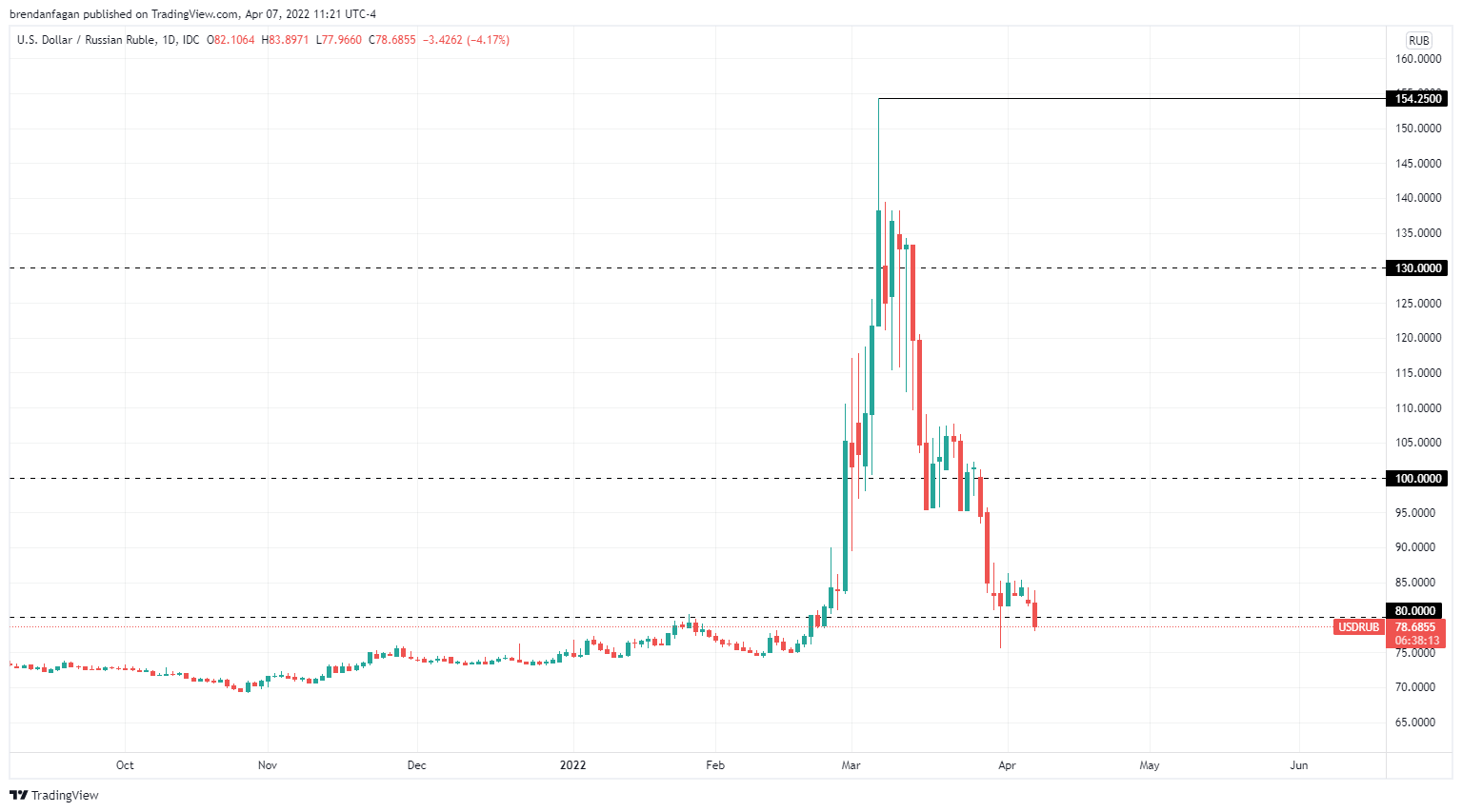

USDRUB Daily Chart

Chart created with TradingView

Perhaps a better indicator of the stress being felt across Russia can be found in the credit markets, where 1-year credit default swaps currently price a 99% chance of default. Credit default swaps on Russian corporate and government debt have skyrocketed after the US blocked Russia from using dollars held at American banks to make interest payments. At the beginning of the year, the chance of a Russian default within 5 years stood at just 8%.

With assets frozen around the world, Russia continues to struggle to meet foreign debt obligations. Following Monday’s actions by the US Treasury, the Russian Finance Ministry indicated that Russia would make payments in rubles, something that many believe would constitute a “technical” default. Prominent credit rating agencies Fitch and S&P Global have stated that Russia would be seen as “in default” if payments were indeed made in rubles. A potential default would be the first by Russia since 1917, when the Bolshevik Revolution was in full swing.

Kremlin spokesperson Dmitry Peskov said that Russia “has all necessary resources to service its debts” and that “there are no grounds for a real default.” Russia continues to argue that the West is pushing it towards an “artificial default,” with some investment banks preparing for Russia to potentially refuse to recognize an official default. With the country set to break terms and make payments using rubles, bondholders will enter a 30-day grace period before an official default is declared.

Resources for Forex Traders

Whether you are a new or experienced trader, we have several resources available to help you; indicator for tracking trader sentiment, quarterly trading forecasts, analytical and educational webinars held daily, trading guides to help you improve trading performance, and one specifically for those who are new to forex.

— Written by Brendan Fagan, Intern

To contact Brendan, use the comments section below or @BrendanFaganFX on Twitter

Be the first to comment