Alina Lyssenko

UroGen (NASDAQ:URGN) is a nanocap commercial stage developer of treatments for urothelial cancers. They have one product called Jelmyto (mitomycin) for pyelocalyceal solution, one in phase 3 targeting NMIBC or low grade intermediate risk non-muscle invasive bladder cancer, and a platform called RTGel which produces “a novel proprietary polymeric biocompatible, reverse thermal gelation hydrogel, which, unlike the general characteristics of most forms of matter, is liquid at lower temperatures and converts into gel form when warmed to body temperature.” The advantage of such a formulation is that it can be taken in liquid form by the patient but is retained for longer periods in the body cavities, the gel formulation preventing rapid excretion and increasing dwell time.

Mitomycin is a well-known chemotherapy agent whose activity against urothelial cancers is well-recognized, and although not FDA approved – being generic – it is standardly used as an adjuvant chemotherapy for the treatment of low‐grade NMIBC after trans‐urethral resection of bladder tumor (“TURBT”). Mitomycin’s problem is that it causes a lot of urination, which does not allow the drug to be in the body for more than 5 minutes. Studies have shown that higher retention of mitomycin increased time to recurrence of urothelial cancer. Indeed, the company presents data that shows:

In one such study, it was shown that mitomycin activity increased with exposure time. Specifically, the MIC90, or mean inhibitory concentration that causes 90% inhibition in cell growth, was 11‐fold lower when exposure time was increased from 30 minutes to eight hours.

Based on this research, the company has developed Jelmyto and is developing UGN-102, both of which are RTGel formulations designed to be retained in the body of patients for longer periods of time.

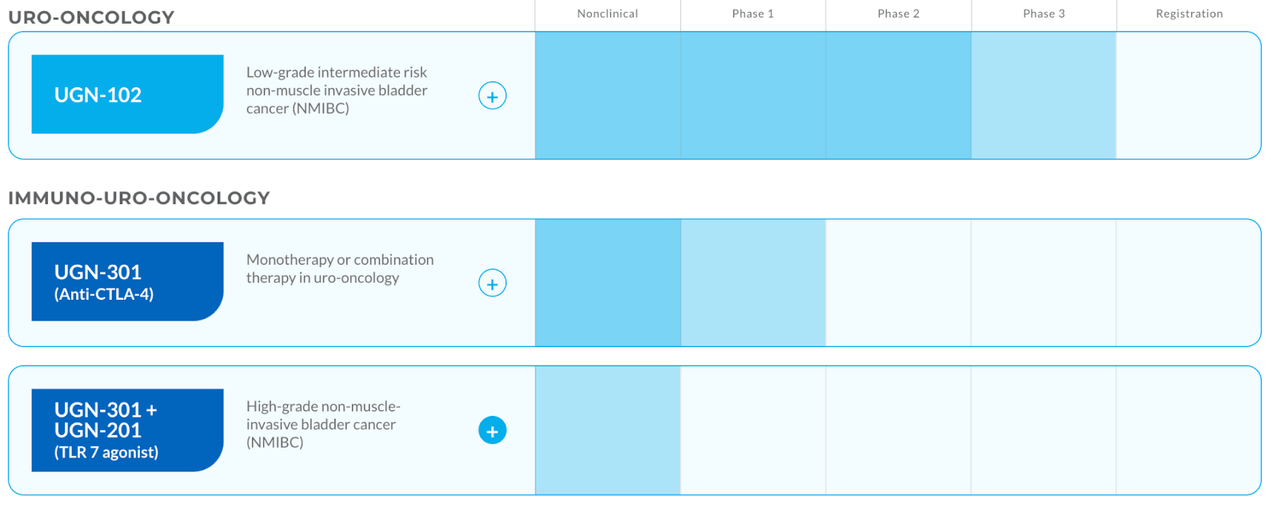

The company pipeline:

URGN pipeline (URGN website)

Jelmyto has around 6-7k US patient population and the market potential is about $700mn, or roughly $100,000 per treatment. UGN-102, the current lead pipeline asset, has a target patient population that’s 12x larger, and a market potential of $3bn. This asset is in phase 3. A third asset, UGN-301, in phase 1, has a target patient population of 18700 and a market potential of $2bn. Jelmyto is targeting Low-grade Upper Tract Urothelial Carcinoma (UTUC), UGN-102 is targeting Low-Grade Intermediate Risk Non-Muscle Invasive Bladder Cancer (LG-IR-NMIBC), and UGN-301 is targeting High-Grade Non-Muscle Invasive Bladder Cancer (HG NMIBC).

Jelmyto is the only FDA-approved nonsurgical therapy for LG UTUC. It was approved in April 2020, and has been able to generate $106mn in revenue since launch, and $46mn last year. The drug has received a permanent J code, which makes approval and reimbursement easier, with an over 99% positive reimbursement rate. The company says there’s high awareness and repeat use, with 177 accounts prescribing it to more than one patient.

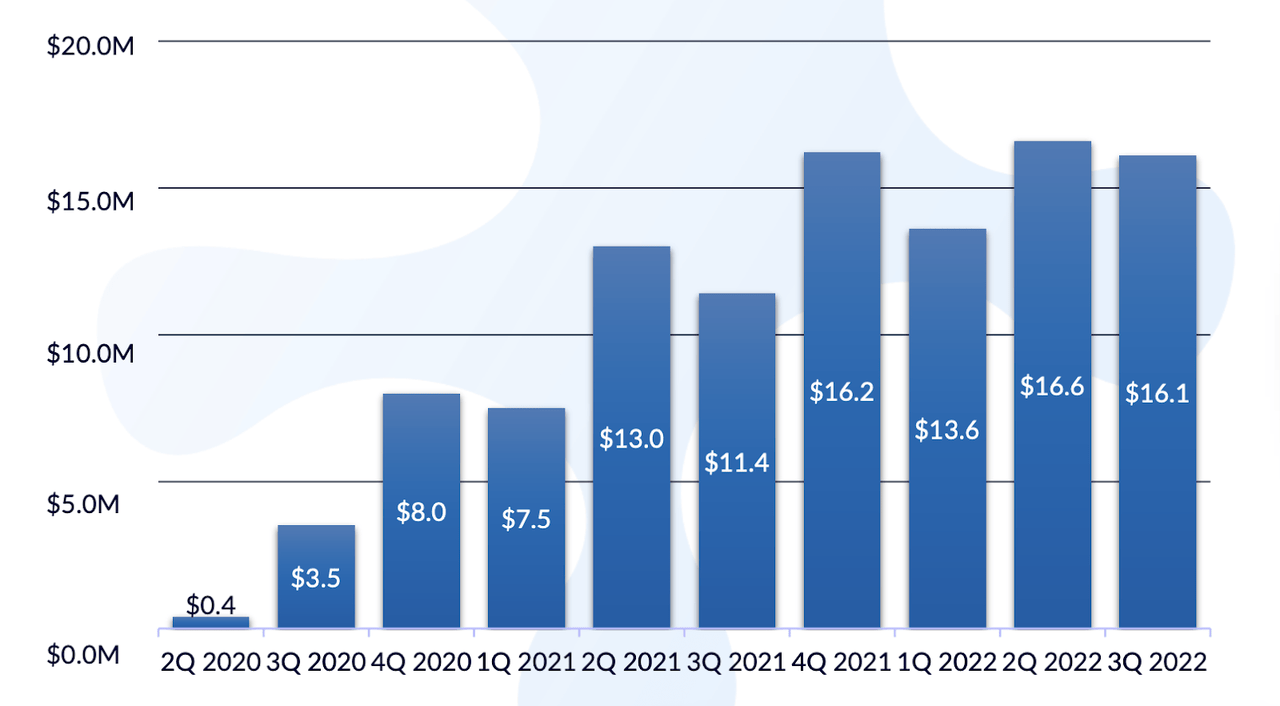

While all that is good, Jelmyto has suffered through what many other approved drugs from small companies see – very little growth post launch, an inability to reach even a small fraction of the market potential. Currently, after over two years of approval, Jelmyto has some 7% of the market. This in itself wouldn’t be bad if that was a growing number. But see the graph below:

Jelmyto revenue (UroGen website)

The asset attained $16mn in 4Q2021, over a year ago. That was the year of the Covid disaster. However, in 2022, when most of the world is out of the pandemic, Jelmyto is still not out of those pandemic numbers. It is still stuck at $16mn revenue every quarter. If you are an optimist, you will say that the trend is holding; if you are not an optimist, you will feel that the trend is stagnant. I am not an optimist when it comes to small emerging biopharma and their sales efforts. The company provides a number of Covid-related reasons for the poor show, but does not explain why, after the easing of the pandemic, there’s not a stronger growth trend over the quarters.

As for UGN-102, in the phase 2b Optima study, there was a 65% CR and a 72.5% 12-month duration of response seen in patients, which is similar to the phase 3 Jelmyto Olympus trial. At a molecular level, the two diseases are quite similar, so solid data from one indication is indicative of positive results from the other one. The phase 3 trial for UGN-102, running currently, is similar in design to the phase 2b trial. One would thus expect positive data from this trial. The company plans to submit an NDA in 2024. Note that this is an open label, single arm trial.

Financials

URGN has a market cap of $213mn and a cash balance of $95mn. This includes the first $75 million tranche of the up to $100 million term loan facility from Pharmakon Advisors. Jelmyto revenue was $16.1mn in the previous quarter. Research and development expenses for the third quarter 2022 were $13.1 million, while selling, general and administrative expenses were $19.1 million. At that rate, they have cash for only about 1-2 more quarters from now.

I should note that Liz Barrett, who is UroGen’s CEO, used to be Novartis Oncology’s CEO.

Bottom line

I found the science here not unconvincing, but the finances are dire. Jelmyto has not lived up to its promise in the market, and there’s no reason UGN-102 will do any different. Considering all that, I will continue watching URGN stock from the sidelines, because I believe the only way for this company to do well is if somebody buys it out.

Be the first to comment