courtneyk

Investors who follow the tech sector may be familiar with Upstart Holdings, Inc. (NASDAQ:UPST), the cloud-based AI lending platform that uses non-traditional variables to assess consumer loan applicants’ creditworthiness and connect them to lenders who can finance them.

The U.S.-focused fintech company has been growing robustly in recent years owing to its value proposition for the risky but lucrative subprime lending market. Analysts expect it to report revenues of $830.65 million in 2022, down slightly from $851.86 million in 2021, but up significantly compared to 2020 and 2019 when it grossed $228.6 million and $159.8 million, respectively. The business has grown roughly fourfold in four years from a topline perspective, underlining the demand for its AI-powered unsecured lending solution.

Traditional lending systems employ FICO scorecards, which is a simple rules-based system that considers only a limited number of variables (12 to 20 variables) to arrive at a lending decision. In contrast, UPST’s model leverages the power of AI to assess approximately 1,600 variables spanning from credit experience to educational history, occupation, and cost of living.

The result is that consumers on UPST benefit from higher approval rates than they would if they sought the financing directly from a bank. The digital experience is also faster. Banks and institutional funding partners that work with UPST benefit from access to new customers, lower default rates relative to other players in the subprime segment, and increased automation throughout the lending process.

Banks and lenders looking to extend their reach in the unsecured lending segment have turned to UPST for its services. This article that I read provides an informative and detailed breakdown of how the company makes money through its relationships with banks and other lenders, including how it earns revenue from referral fees, platform fees and other services.

Back to square one

Following its December 2020 IPO, where it debuted at a market cap of $1.45 billion, UPST quickly became a darling of growth investors and, aided by the risk-on sentiment at the time, sky rocketed to a lofty market cap of $30 billion in October 2021 when the broader market, represented by major indices, was peaking.

It, however, crashed in 2022 and its market cap today is just $1.39 billion. The stock is essentially back to square one as far as its market cap is concerned. The important question for investors following UPST’s sharp decline over the past year is: are there fundamental issues with the business, or is UPST merely a victim of temporary negative circumstances that will shift back to neutral or positive in time?

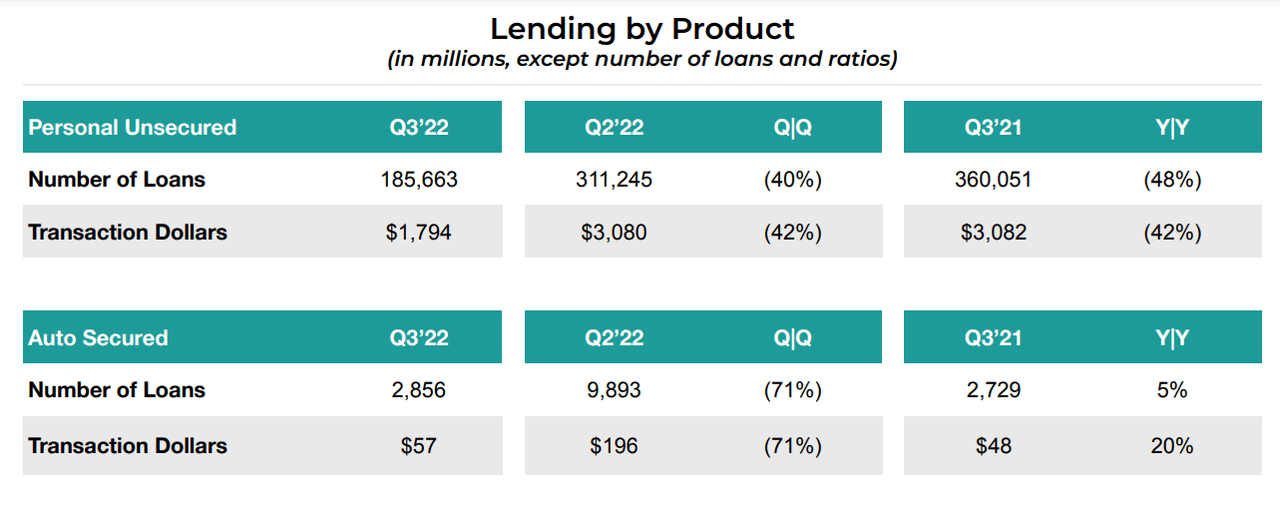

I’m convinced that the latter scenario is closer to reality. Higher interest rates usually come with greater scrutiny of borrowers and lower approval rates. The volume of unsecured lending tends to decline during times of high interest rates. UPST has been affected by this, with the value of unsecured loans declining 42% to $1.79 billion in Q3 ’22 vs $3.08 billion in Q2’22 when the current rate hike cycle began.

Volumes of loans declined amid higher interest rates (UPST earnings presentation)

Cheaper today

Despite the operational headwinds linked to higher interest rates in the second half of 2022, UPST continued to invest in its underlying business. R&D expenses are $219 million for the trailing twelve months, a significant increase from $134 million in 2021, $38 million in 2020 and $18.8 million in 2019. Likewise, selling, general and admin expenses are $590.1 million for the trailing twelve months, up from $454.9 million in 2021, $145.3 million in 2020 and $125 million in 2019 . The increased investment in operations and R&D is a good sign given the fast pace of innovation in AI and the need to continually invest in order to remain competitive.

Importantly, UPST is cheaper today. Since it’s an unprofitable growth company with a limited operational history, price to sales is my preferred valuation metric. On this basis, UPST is trading at a price/sales ratio (fwd) of 1.67x, which is 60% lower than its P/S of 4.3x when it went public as per data from YCharts.

UPST is cheaper today despite having grown its topline fourfold, having invested in the underlying business through increased R&D spend, and having survived the downturn in unsecured lending that comes with higher interest rates.

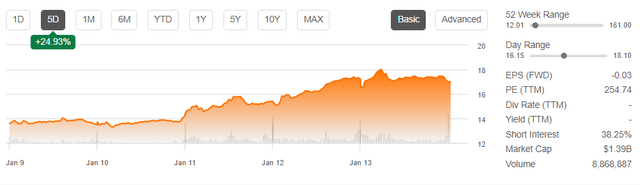

This combination of factors makes it a buy in my book. The stock is up 24% in the last week, as lower inflation in December fueled expectations of an imminent pause in interest rate increases. This is good news for UPST’s subprime lending industry and for growth stocks generally.

UPST rallied 24% last week (Seeking Alpha)

I consider UPST a strong buy below $20 per share, as the valuation from a P/S standpoint is low. The upside potential at current levels is significantly higher than the downside. It’s also my view that most of the weakness has already been priced into current valuations, further increasing the likelihood of the stock going up in 2023.

Risks

That said, the highest risk to my thesis is interest rates staying higher longer than expected, thus affecting volumes of unsecured loans processed over UPST’s platform in the first and possibly second half of 2023. This could impact growth expectations and weigh on the stock further.

Another risk is that, with profitability still far off, the company’s continued losses could lead it having to raise capital through debt or equity, a development that will likely pull down the share price. I also feel that there are additional risks worth discussing that come with investing in a stock like UPST at this point in time.

Additional risks – changing market environment, FOMO and volatility

The Fed’s current tightening cycle is its most aggressive in more than three decades. In a high interest rate environment and recessionary economy, investors favor companies that can deliver resilient profits and cash flow during over those with growth potential but no cash. UPST is in the latter category.

However, with inflation falling, investors are anticipating a pivot by the Fed later this year, with the past week’s strong rally across risk assets following news that inflation cooled in December being indicative of this expectation.

The exact timing of the Fed’s pivot will depend on when we start seeing a mix of economic weakness (or recession depending on the semantics), debt distress among households and businesses, and increased levels of unemployment. Some of these signs have already started emerging, going by the wave of recent layoffs in many leading companies and the rising credit card debt held by households.

This sequence of events could lead to increased market volatility, meaning investors who choose to buy UPST now would need to be comfortable with the risks that come with this.

Moreover, the fact that UPST has a significantly high short interest of 38.25% could make it a target for speculative investors looking to capitalize on a potential short squeeze. Meme stocks have made big moves in the past week, and this could be a sign that speculative fervor is starting to come back to the markets, bringing further risks of volatility that come with the Fear of Missing Out (FOMO) bias that is prevalent among members of the meme stock community.

Conclusion

These risks are not to be taken lightly, as they can tempt investors to disregard one of the cardinal rules of risk management – buying a good company without overpaying, then sitting down and doing nothing.

It’s difficult not to take action when your long position’s liquidation value is wildly gyrating up and down intraday and intra-week, but this is the price you have to pay for the upside potential that comes with Upstart Holdings, Inc. The stock’s 24% run in the past week could be a sign of the train leaving the station. The earlier you get onto Upstart Holdings, Inc., the better your potential returns, but the higher your risks.

Be the first to comment