cofotoisme

Investment Thesis

Upstart Holdings, Inc. (NASDAQ:UPST) reported yet another set of unimpressive results. Yet I’m actually upwards revising my sell rating on this stock. Why?

Because despite going into earnings with a sell rating on this stock, I believe that a lot of negativity is now priced into the stock.

By my estimates, Upstart is priced at 3x forward sales. This is a relatively low entry price for further investors considering this loan facilitator.

Upstart still has problems, most notably its growing loan book. Hence, Upstart is not out of the woods. But, with the stock down 10% pre-market, I believe that this is a new base for the stock.

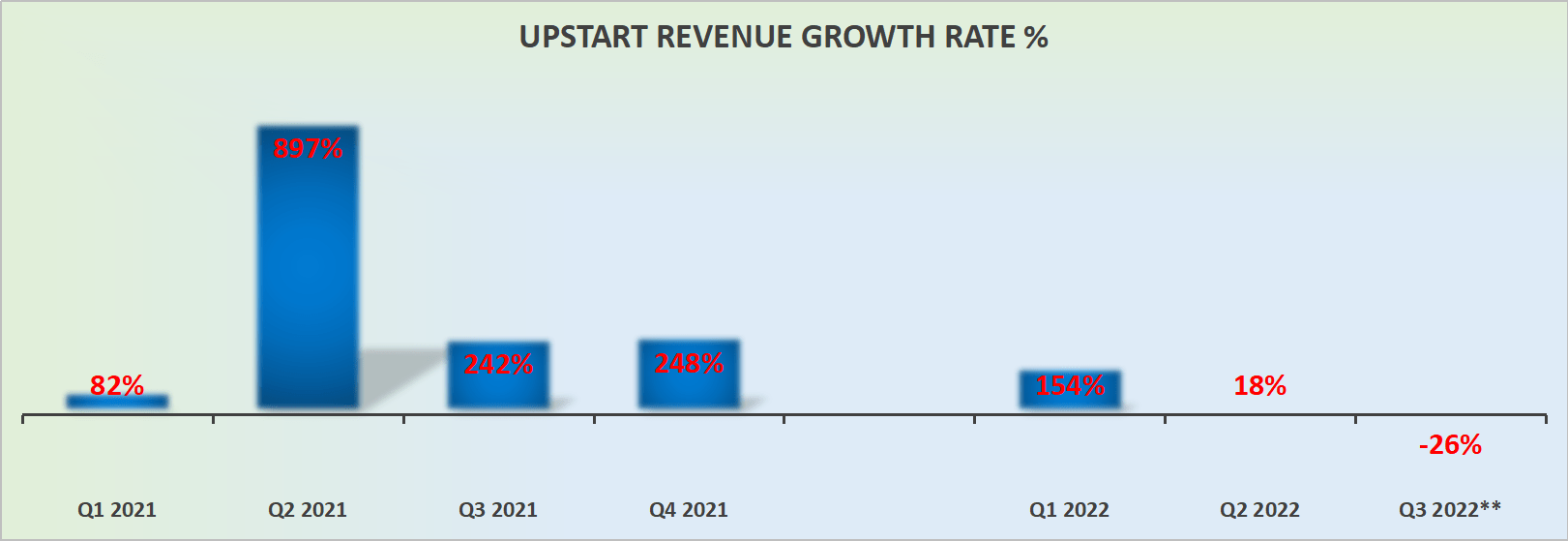

Revenue Growth Rates Turn Negative

UPST revenue growth rates

As a reminder, prior to the earnings, Upstart had already notified investors that it was set up for a dismal quarter. That was already priced into the market and investors had come to terms with that event.

What investors were truly interested to see was what its look-ahead expectations were like. And here again, Upstart disappointed.

Now, let’s get some perspective. With the benefit of hindsight, Upstart was a momentum play that culminated in November 2021. That being said, I and countless other investors, were seduced by Upstart’s rapid revenue growth rates, driven by its alluring loan approval facilitating business model.

That had been the premise that saw Upstart’s results sizzle against what was a notably strong macro environment last year.

Again, all these are now ”known knowns.” What matters at present is why did Upstart yet again bring down investors’ expectations for 2022?

What Happened to Upstart?

In a noticeably open and transparent earnings call, co-founder and CEO Dave Girouard described the two cycles that Upstart has been through in the past couple of years.

From the onset of the pandemic where stimulus checks lead to a very strong consumer with minimal loan defaults, to the more recent environment.

As stimulus checks got reduced, the percentage of customer defaults increased, which lead to institutions pushing back against holding Upstart’s loans.

By extension, this has seen Upstart’s loans held at fair value on its balance sheet increase sequentially from under $600 million to $624 million as of Q2 2022.

On this front, Upstart noted on its call that approximately 78% of the loans held on Upstart’s balance sheet are tied to its nascent auto business.

Upstart’s management went on to say during the earnings call,

[…] The performance of the credit we must confront the fact that the largely uncommitted nature of our third-party funding has proven inadequate to the task of navigating the market turbulence.

And we have turned our efforts towards building a more resilient funding model over time. Despite not having suffered any adverse loan performance, some banks are moving to limit their overall exposure to unsecured lending.

And herein lies the crux of the argument for the bears. Upstart is struggling to shed these loans. And that’s exactly what the market feared, that if there was going to be a tightening economic cycle, that Upstart could end up holding onto these loans. And that’s precisely what’s happened!

The big question now is what will Upstart do going forward? Can Upstart truly figure out some way to get banking partners to take up some of Upstarts’ loans?

Because if Upstart can’t shed these loans, its ability to rapidly grow its revenues will be severely impacted.

Profitability Profile: Once a Crown Jewel

This time last year, Upstart was a solid GAAP net income generating business, reporting a 19% of net income margin. Today, its net GAAP margin is negative 13%.

Consequently, investors today investing in Upstart have the worst of both worlds, less topline growth plus substantial losses to contend with.

Furthermore, Q3 2022 is being guided for even worse GAAP net margins, at negative 25%.

Hence, even though Upstart has brought down earnings expectations enough so that it can ultimately beat these lowered earnings estimates, the fact remains: Upstart of 2021 is not the same as Upstart of 2022.

Needless to say that none of this really matters. What matters is what will Upstart of 2023 look like. And whether or not investors are being sufficiently compensated by its lower valuation.

UPST Stock Valuation — 3x Sales

If we were to generously assume that Upstart’s Q4 revenues sequentially improve from Q3, so that Q4 2022 reports $190 million of revenues, that would mean that for 2022 as a whole Upstart’s revenues would reach approximately $675 million.

Then, if were to assume that in 2023, Upstart is somehow able to reignite its revenue growth rates, so that it could ultimately grow its revenues by 30% compared with 2022, that would see Upstart’s revenue reporting approximately $880 million in revenues.

That means that investors now considering the stock are willing to pay less than 3x sales.

I believe that this is a very fair multiple.

The Bottom Line

Upstart’s Q2 results have been a disappointment. That being said, the stock is already down 90% from its highs. Thus, I believe that at a $3 billion market cap, Upstart is really pricing in a lot of doom and gloom.

A lot of big money has already sold out of the stock. What’s left isn’t likely to sell in mass. This second group of investors is already down significantly on their holding and at this point will probably not sell in any conditions, irrespective of how bad Upstart’s prospects get.

Consequently, what’s left now is one final group of investors looking at the stock with a fresh pair of eyes, attempting to catch the bottom of the stock for a quick bounce.

On balance, I’m neutral on the stock.

Be the first to comment