ConceptCafe/iStock via Getty Images

Investment Thesis

Unity Software (NYSE:U) is already a leader in the game engine duopoly, but this company’s ability to branch into non-gaming industries provides an opportunity for even more growth. Yet its Q1’22 results waved some warning flags for investors and sent shares tumbling, so is this the end of Unity?

Of course, it isn’t.

Business Overview

Unity is the world’s leading platform for creating and operating interactive, real-time 3D content. It is mostly known for its Unity gaming engine, and boasted 94 of the top 100 game development studios as customers in 2020. Unity’s platform can be used to build and operate games by developers of any size, from individual creators to large publishers across the globe.

Yet the demand for RT3D (real-time 3D) content is growing outside the realms of gaming, and Unity’s customers range from game developers to artists, architects, automotive designers, filmmakers, and many more. There are Fortune 500 companies across these industries that utilise Unity’s platform for an ever-expanding list of use cases, including architectural design, augmented reality product configurators, autonomous driving simulations, and augmented reality workplace safety training.

Unity’s business model consists of two revenue streams: Create Solutions and Operate Solutions.

Unity Q3’20 Investor Presentation

Create Solutions offer a broad set of tools for the development of real-time 2D and 3D content. They can be used by artists, designers, and developers across a range of industries to easily create, edit, and run RT3D and 2D experiences; in short, the Create Solutions are used for digital creations – most commonly, games. This side of the business is subscription-based, and provides a recurring source of revenue.

Once someone’s created their game using Unity’s Create Solutions, they can then move onto the Operate Solutions to distribute, market, and monetise their content. Unity Gaming Services is a platform that enables developers to manage the release of their game, with offerings including Cloud Content Delivery, Multiplay Server Hosting & Matchmaking Platform, Player Engagement Monitoring, and many more. The other side of Operate Solutions is monetisation, with tools such as Personalised Advertising powered by Unity’s machine learning and deep player and game data. The Operate Solutions business for Unity generates usage-based revenues through revenue-share and consumption-based models.

The company released Q1 results back in May which stunned the market, and not in a good way. Whilst there is reason to be somewhat nervous as a shareholder, it wasn’t all bad news.

Acceleration of Create Solutions

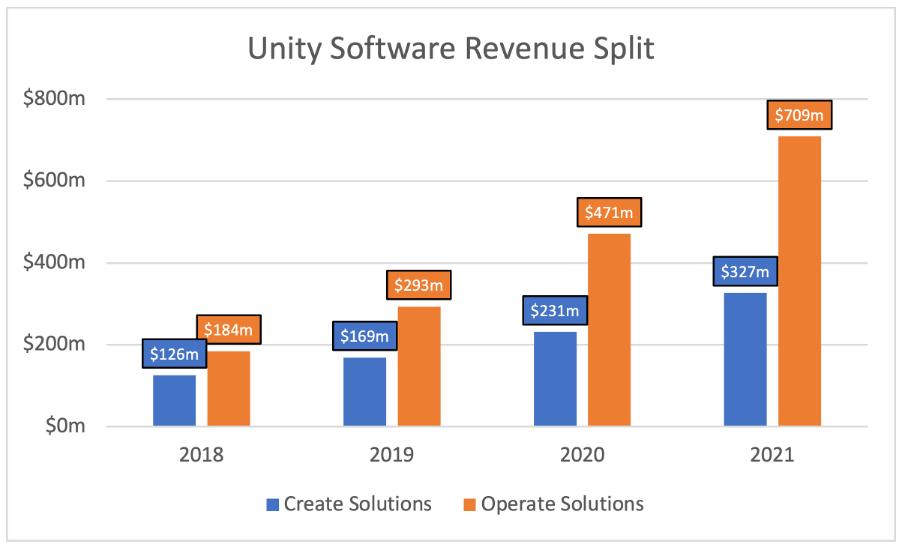

Unity’s business model operates a land-and-expand strategy. The aim is to add customers to their Create Solutions, thereby obtaining some recurring subscription revenue, and then once the customers have created their games, get them using the Operate Solutions for marketing and monetisation purposes. Since the Operate Solutions revenues are based on both revenue-share and consumption, there is the opportunity to accelerate sales in this part of the business as developers successfully market and monetise their games. This trend has generally played out, with Create Solutions growing at a 38% CAGR and Operate Solutions growing at a 57% CAGR from 2018 through to 2021.

Unity SEC Filings / Excel

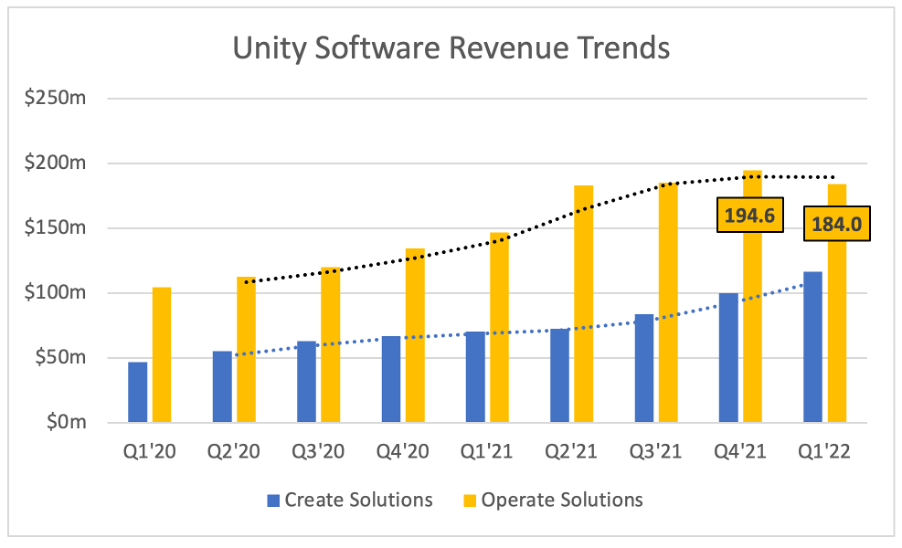

However, in Q1, we saw the complete opposite – Operate Solutions slowed substantially, but Create Solutions grew a surprising 65% YoY. I’ll get to what happened in Operate Solutions shortly, but let’s start with the positives.

Unity SEC Filings / Excel

As we can see above, Create Solutions posted its best-ever YoY growth in Q1’22, following on from a strong Q4’21. Given that Unity’s business model follows a land-and-expand approach, the growth in Create Solutions revenue is a sign that Operate Solutions revenues could grow even more rapidly in the future, as developers create first & then look to deploy on Operate Solutions. The momentum in gaming continued here, with the likes of Angry Birds being brought back to our phones through Unity’s Create Solutions, but there is one key line from CEO John Riccitiello that should have long-term shareholders excited.

Unity Create is now hitting an inflection point that we have long anticipated, where we are not only growing our gaming footprint and take-rate, we are seeing strong adoption from industries beyond gaming.

Strong Momentum Outside of Gaming

One of the aspects that appealed to me when I first researched Unity Software as a potential investment was the opportunity outside of gaming. Don’t get me wrong, it was Unity’s position in the gaming industry that attracted me to the business (and still does), but this additional optionality is the icing on the cake – and, it’s starting to pay off.

An example of this is Unity’s Digital Twins business, although we’ll start with a quick definition of a digital twin from Unity themselves:

A digital twin is a virtual representation of a physical site, asset, system, or process, capable of mimicking its real-world counterpart’s condition and behaviour. Enriched with data, it informs decision-making by helping understand the past, observe the present, and predict the future.

So, a Digital Twin is essentially a 3D digital copy of an existing real-world ‘thing’, whether that’s a building, a car, or a city. Remember that Unity is the leader in real-time 3D content, so it’s no surprise to see it succeeding in this space.

Unity.com

Unity entered 2022 with almost 3,000 customers in their Digital Twins business, and as usual, Unity is taking a land-and-expand approach. In Q1’22, Unity closed 34 deals above $100k in the Digital Twins space, up 126% YoY and 13% QoQ. The Digital Twins solution is being used in construction, commerce, manufacturing, advanced simulation, and more.

Some recent examples of how businesses are using Digital Twins include:

- One of the world’s largest energy companies deploying the Digital Twins product across their entire enterprise to run their downstream operations more effectively

- An iconic luxury brand leveraging Digital Twins to bring a differentiated digital experience

- The Orlando Partnership has hired Unity to create a digital twin of the entire region in an effort to solve regional challenges for the 800-square mile area, including transportation, climate change, and utility mapping.

And, in terms of the land-and-expand strategy, a perfect example here is Unity’s relationship with Lockheed Martin (LMT). The first project in 2017 started when Lockheed bought a few seats for design visualisation, and within 12 months, they had deployed 132 licenses to create more interactive experiences across product development. Fast forward to today, and Lockheed has nearly 500 licenses across 9 business units for use cases, including simulation, training and guidance, and collaboration.

The Digital Twins business is just one of Unity’s many non-gaming solutions; they have also been diving into the film & special effects industry with their recent acquisitions of Weta Digital and Ziva. In fact, Ziva Dynamics was used in movies such as Dune, which went on to win an Oscar for Best Visual Effects, and Weta Digital is best known for the special effects behind the perfect trilogy of films that is Lord of the Rings.

2 Big Blows to Operate Solutions

We saw how the momentum in Create Solutions is driving Unity forward, and in truth, the Q1’22 results would have been fantastic if it wasn’t for two pretty major issues in Operate Solutions.

Unity SEC Filings / Excel

Whereas the trend is clearly upwards for revenues in Create Solutions, Operate Solutions actually reversed their previous trend and showed a sequential decline of 5% in revenues – given that Unity is a company with long-term revenue growth guidance of 30% annually, it’s a worrying sign for shareholders.

The first reason for this decline is due to a fault in Unity’s platform that resulted in reduced accuracy for its Audience Pinpoint tool – exacerbated even more by the fact that this Pinpointer tool had seen strong growth after Apple’s privacy changes (this is a good thing for the long-term prospects of Unity!).

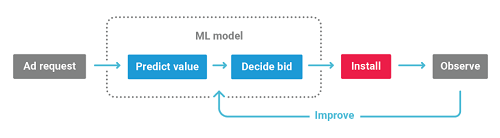

The Audience Pinpointer tool is a user acquisition tool that utilises machine learning to help customers using the Operate Solutions find players that are most likely to provide long-term value beyond an initial app install – that is, users who are most likely to continue playing their game, rather than installing it, maybe playing once or twice, and then forgetting about it. The use of dynamic pricing allows Unity’s customers to bid more for predicted high-value users, and bid less for users who are less likely to continue playing the game after installation.

I like that Unity’s Operate Solutions revenues are performance-based – it aligns incentives between Unity and its customers, and it means that when the customer succeeds, Unity succeeds. Unfortunately, the opposite is also true, and because of the drop in accuracy of Unity’s Audience Pinpointer tool, customers saw a much lower return on their ad spend & therefore the revenue that Unity generated fell substantially.

The second reason for the falling revenues is explained below by CEO Riccitiello:

We lost the value of a portion of our data training due, in part, to us ingesting bad data from a large customer.

So, let’s take a step back and untangle this. As a reminder, Unity has 3.9 billion monthly active users who play games or use apps built on Unity’s platform, and that is A LOT of data that they can utilise for their machine learning tools. And, as we saw earlier, Unity’s advertising solutions relies on ‘machine learning combined with our deep player and game data to drive end-user installs at scale’ – the problem is that Unity ingested bad data from a large customer, and that has completely thrown their machine learning algorithms.

Unity.com

My first thought – why not just go to an older backup version of the algorithm?

It would appear, quite shockingly, that they can’t – or at least, not very quickly.

CEO John Riccitiello was pretty open and frank about the issues on their Q1’22 conference call, which I appreciate, and offered the following to investors:

We estimate the impact to our business at approximately $110 million in 2022, with no carry-over impact to 2023. Luis will provide a more granular update to our guidance in a few minutes. Here I will provide a deeper explanation of the specific revenue impacts. First, we have the direct near-term impact resulting from the two issues I just mentioned, affecting the first and second quarters. Second, we expect recovery to go through steps in sequence, data rebuilding, model training and improvement and then revenue recovery as our customers scale up further on Unity Monetization. And third – as a consequence of reprioritizing work in our teams to thoroughly address the resiliency and data training issues – we delayed the launch of certain revenue-driving features such as mediation, header bidding, and new releases for Audience Pinpointer versus our original plan.

We understand the problems and we are well advanced in addressing them. We are deploying monitoring, alerting and recovery systems and processes to promptly mitigate future complex data issues. We are strengthening and innovating on our Audience Pinpointer product. And we are already scaling Unity Mediation. Once done, we should be ahead of where we were at our best.

Unity ingested bad data, the market ingested bad results, and the outcome was the same – numbers going down, resulting in investors feeling as if they’d ingested some bad seafood. Yet I am comforted by Riccitiello’s frankness, and only time will tell whether or not they are able to address and fix these issues. If they do, and the algorithm is rebuilt (even stronger, I hope), then everything should be fine and dandy by 2023.

Bottom Line

As an investor in Unity Software, this was a quarter that tore me in two. The results from Create Solutions were extremely impressive, and the non-core gaming growth has reaffirmed my belief in Unity’s future. Yet the issues with Operate Solutions are bad, and far below the expectations I have for this company.

The only question now for investors is whether you trust management to resolve these issues as they say they will. I, for one, am willing to give them time to work it out. Unity looks like a business that is firing on all cylinders, apart from the one that just snapped off – if they can fix that cylinder, then I think the sky’s the limit.

Be the first to comment