hapabapa/iStock Editorial via Getty Images

UPS (NYSE:UPS) is set to report its earnings before the market opens on Tuesday. The company is facing headwinds from the weakening global economy as well as the company’s strategic initiatives to reduce shipments from Amazon (AMZN). The current consensus sell-side estimates are expecting the company to post ~1% Y/Y sales growth and flattish EPS versus the same quarter the prior year. While the volume is expected to decline Y/Y, sell-side analysts are expecting pricing to offset some of its impacts. FedEx (FDX), whose Q2 ends in November, reported a ~2.8% Y/Y decline for the quarterly revenues when it released its earnings in December. I believe there is a chance of UPS posting slightly lower-than-expected revenues when it reports its Q4 results. Further, in addition to weakening macros, there is an added uncertainty for UPS stock in 2023 as the company’s agreement with the Teamsters Union is ending on July 31 and the company is entering a period of re-negotiation with the union. While the stock is trading at lower than historical valuations, I prefer to remain on the sidelines until the volume decline bottoms and more clarity on the company’s contract negotiations with the Teamsters emerges.

Revenue Outlook

After seeing healthy revenue growth in 2020 and 2021 due to an increase in e-commerce volumes, strong consumer demand in the U.S. (thanks to stimulus checks and a healthy consumer balance sheet), and solid pricing growth, the company witnessed a volume decline in the first nine months of 2022. Tough comps, the Russia-Ukraine war, weakening demand due to rising interest rates, and the company’s strategic initiative to reduce volume and revenue from Amazon in the U.S., all played a role in this volume decline. However, the strong pricing growth helped the company more than offset this decline, and it posted mid-single-digit revenue growth in the first three quarters of 2022.

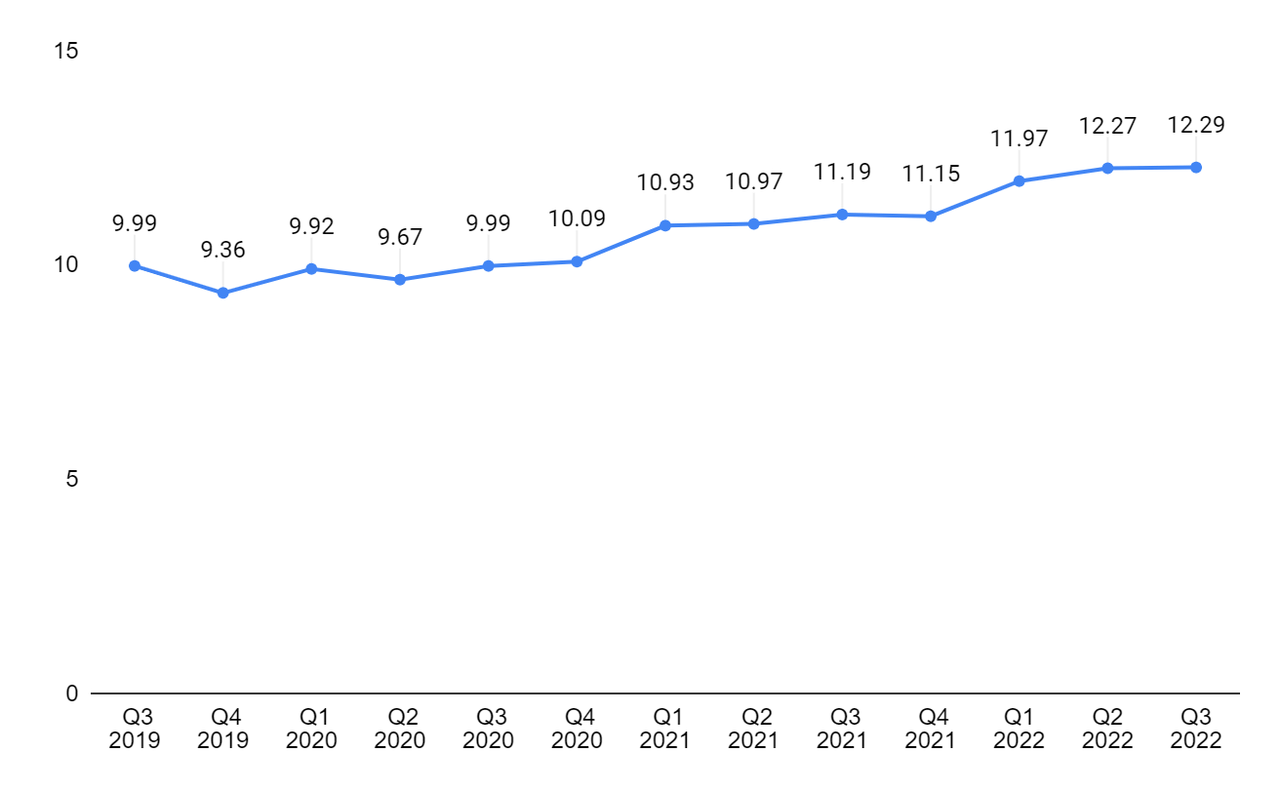

UPS historical sales and volume data (Company data, GS Analytics Research) UPS’ Revenue Per Piece in the U.S. (Company data, GS Analytics Research)

Moving forward, for Q4, the company faces two major headwinds. First, the comparisons are slightly tough. In Q3 2021, the company posted 9.2% Y/Y revenue growth, while in Q4 2021, the revenue growth was 11.5% Y/Y. So, in Q4 2022, there is a 230 bps headwind from tougher comparisons. The company posted 4.2% Y/Y revenue growth in Q3 2022, so based on this tough comparison alone, the growth should slow to 1.9% Y/Y in Q4 2022.

The second major headwind is a meaningful slowdown in the economy from Q3 to Q4. As the Federal Reserve continued to hike interest rates, consumer sentiment and economic growth moderated in Q4. Many companies that have already reported their December quarter earnings have talked about meaningful destocking in inventory at retailers/distributors. This should impact volume growth for UPS as these distributors/retailers are not ordering the new inventory at the prior pace. So, the seasonal improvement in the holiday season will likely be much more muted this year. If we look at the company’s peer FedEx, its revenue went from growth at 5.6% Y/Y in Q1 (ending August) to a 2.8% decline in Q2 (ending November). Now, the quarter end for FDX and UPS doesn’t exactly overlap, but the weakening trend as the year progressed holds true for both of them. So, I wouldn’t be surprised if UPS posts a slight decline in revenues Y/Y in Q4 2022, instead of the ~1% Y/Y growth that the consensus is building in.

In the long term, UPS is working to reduce its volume from Amazon and focusing on growing its SMB business, which has a better yield. In Q3 FY22, the SMB Average Daily Volume (ADV) increased by 1.9% Y/Y and contributed 28.3% to the total U.S. Domestic volume, up 90 bps Y/Y. The company’s Digital Access Platform (DAP), which embeds UPS’ shipping solutions directly into lending e-commerce platforms, creates a seamless experience for its customers and is helping it gain traction in the SMB space. This Platform has more than three million merchants and generated ~$1.6 bn in revenue in the first nine months of 2022. Management has set a $2 bn revenue target from this platform in 2022, which the company should be able to surpass.

While I like the company’s initial execution towards reducing its volumes from Amazon and increasing its exposure toward SMBs, Amazon is still expected to account for ~11% of UPS’ U.S. revenues by the end of FY2022. So, it is not going to be that easy a task to replace the entire Amazon exposure with SMBs. Also, FedEx has a meaningful presence in SMB markets, and it should give tough competition. Further, in the near term, with the economy weakening, SMBs are expected to be hit harder compared to bigger players, adding to further woes.

I expect 2023 to be a tough year for UPS, and the company should post a Y/Y decline in revenue. So, I am not optimistic about the upcoming FY2023 guidance either. FedEx recently cut back on Sunday deliveries in cost-saving efforts as it was not getting enough volumes. I don’t expect trends at UPS to be any better.

Margin Outlook

UPS is continuing to work on its productivity improvement initiatives to expand its margins. The company’s total service plan (TSP), which is about running a predictable on-time network, helped UPS improve its on-time departures and arrivals by 6.5% Y/Y and reduce idle time in the network in Q3 2022. The TSP also benefited the company to reduce its overtime hours and reduce fluctuations in driver paydays. The total service plan is expected to drive more than $150 mn in productivity in the fourth quarter of 2022.

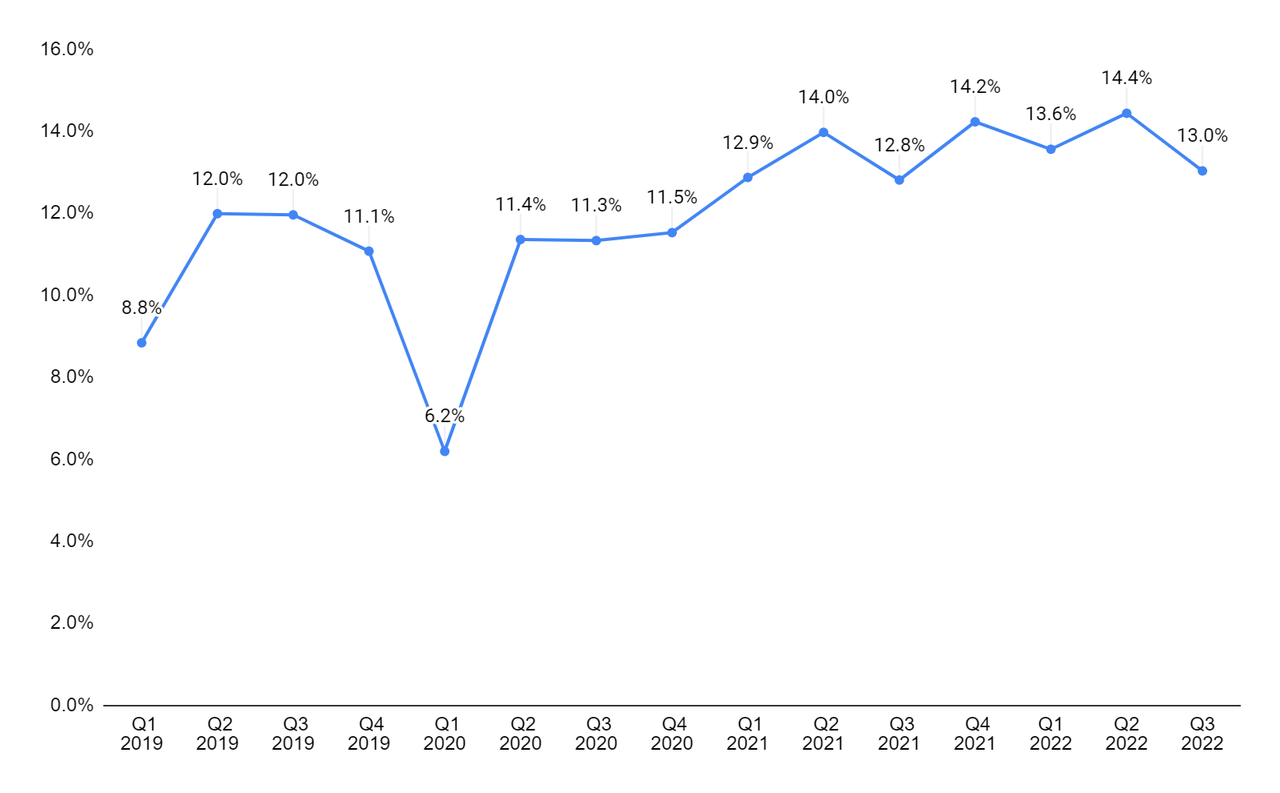

UPS adjusted operating margin (Company data, GS Analytics Research)

In addition to TSP, the company is also driving productivity by introducing smart packages, smart facilities, and RFID labeling to its packages. The company introduced these services to its 101 buildings in the first nine months of 2022. The Radio-Frequency Identification (RFID) labeling is helping UPS reduce the misloading of packages in the package car, and has helped the company achieve one in 800 package misloads (which was previously one out of every 400 packages.) Apart from misload, the RFID labeling is also helping the company eliminate manual scans by its pre-loaders every day.

While I like the company’s cost-saving efforts, deleverage from volume is a big concern in the near term. Air freight carriers usually have a high fixed cost structure, and their margins get hit during times of economic slowdown. Another concern for the company’s margin is the upcoming contract negotiation with the Teamsters Union. The company has approximately 327,000 employees employed under a national master agreement and various supplemental agreements with local unions affiliated with the Teamsters. These agreements run through July 31, 2023, and will come up for renegotiations in the current year. Since labor costs form a big portion of the company’s cost structure (Compensation and Benefits are ~48% of revenues), how these negotiations proceed will provide additional uncertainty to the stock.

Overall, I am expecting margins to decline in the near term, with volume deleveraging and rising cost inflation to offset productivity initiatives.

Valuation & Conclusion

UPS is currently trading at 15.05x FY2023 consensus EPS estimate of $12.10 which is at a discount to its historical five-year average forward P/E of 16.44x. The company also has a dividend yield of 3.34%. While I like the company’s lower-than-historical valuation and good dividend yield, near-term revenue and margin concerns keep me on the sidelines. Hence, I have a neutral rating on the stock.

Be the first to comment