viper-zero/iStock Editorial via Getty Images

Intro To United Airlines

We wrote about United Airlines Holdings, Inc. (NASDAQ:UAL) in October, before the company’s third-quarter earnings numbers, when we stated that demand needed to push earnings higher, leading to a higher share price. Well, the bulls got the numbers they were looking for, with a significant beat in both earnings ($2.81 per share) and revenues ($12.88 billion) with shares pushing higher as a result. Although we did not get filled on our iron condor before the announcement, it would have been difficult for the delta-neutral strategy (especially if the position would have needed to be rolled out in time) to make money considering the post-earnings move. Shares are incidentally up almost 40% since our commentary pre the airline’s Q3 earnings back in October of last year.

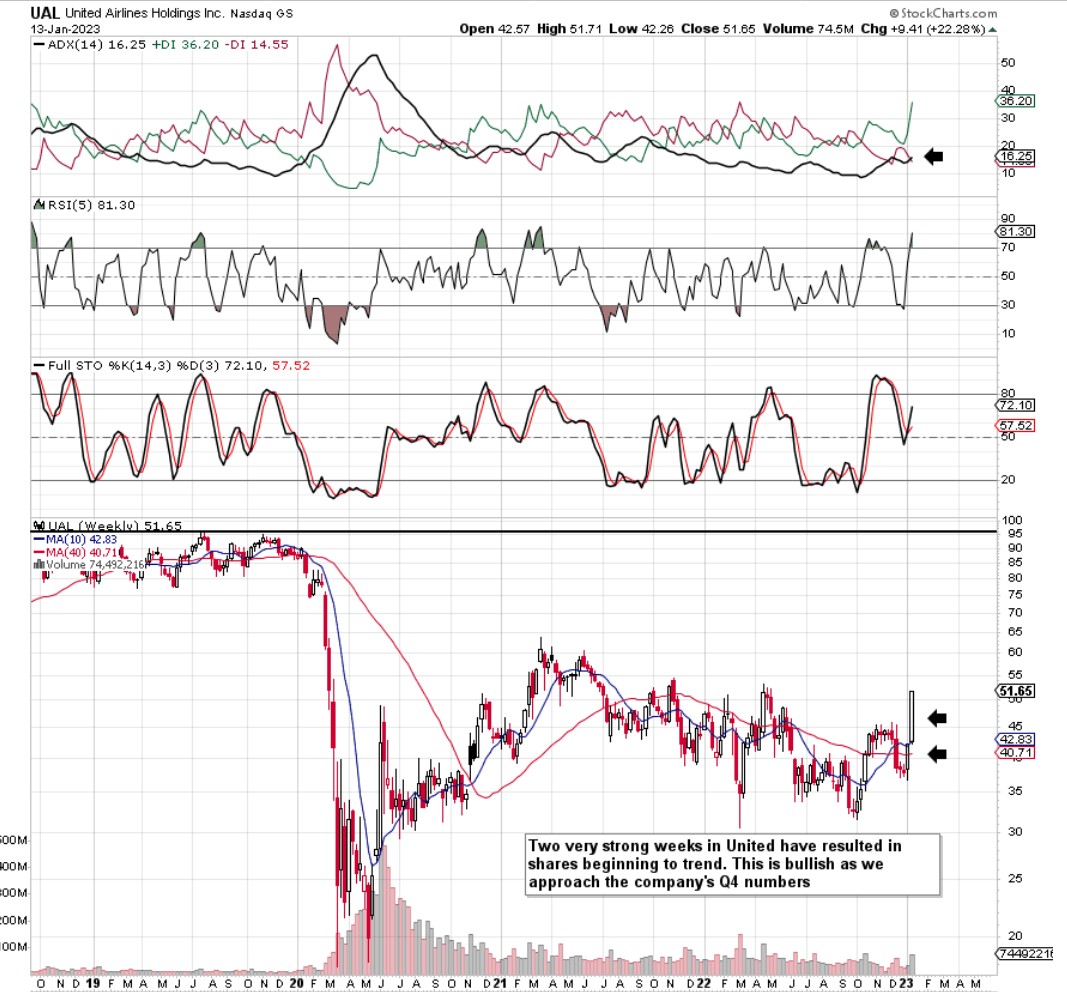

In fact, the present trend as we head into the announcement of United’s fourth quarter numbers (to be announced this week, expected January 17 post-market) is the strongest we have seen in quite some time. As we see below, last week’s stellar up-move followed a significant weekly reversal (selling climax) where buying volume meaningfully increased to the upside. Suffice it to say, United has very strong momentum going into Q4, and barring a poor earnings number (which is definitely not expected, as we have seen 18 upward EPS revisions over the past 90 days), we should see shares of United trading higher than present levels over the next month or so.

United Airlines Technical Chart (Stockcharts.com)

Demand Tailwind

Consensus is expecting $2.11 in earnings per share on revenues of $12.24 billion for the fourth quarter. The bottom-line estimate, in particular, has risen significantly in recent months as the market has begun to price in demand tailwinds which can clearly be seen in the market. These tailwinds include but are not limited to more visibility regarding aircraft delivery and no serious Covid outbreaks which would have seriously dampened demand over the Christmas period for example.

In fact, what investors need to take into account here is that shares, despite United’s recent move, remain significantly below their 2019 (Pre-Covid) highs as we see in the chart above. Yes, the airline industry may never return to pre-covid levels in terms of growth, but elevated customer demand and a general lack of supply in the industry with respect to aircraft, pilots, etc. continues to act as a strong tailwind for United’s revenues.

Spending Spree

Revenues of $38.13 billion over the past four quarters are up almost 70% over fiscal 2021 revenues and earnings are catching up fast. In fact, United’s third quarter from an operational standpoint (adjusted operating margin of 11.5%) was one of the best in the airline’s history and momentum is set to continue into the fourth quarter. With Japan having recently opened up and United’s international partnerships to the fore, United has been on the rampage of late with respect to securing aircraft to fulfill demand. 12 Boeing aircraft were secured in the third quarter with a further 24 aircraft earmarked for the fourth quarter. This significant boost in spending is expected to lift Capex spending to more than $4.5 billion this year which is on a par with numbers we witnessed pre the Covid outbreak in fiscal 2019

Q4 Ramifications

What does this mean for investors going forward and specifically United’s fourth quarter numbers? Well considering how low the share price is to yesteryear and how much Capex has been increasing (More assets on the balance sheet), we believe we remain very early in this current cycle where supply still has a lot of catching up to do concerning customer demand. Furthermore, management has been reeling in those costs in solid order with fewer peaks and troughs regarding sales definitely leading to better efficiency regarding aircraft utilization. Therefore, if the $2.11 EPS number can be met for the fourth quarter, it would really be encouraging for next year’s bottom-line target which comes in at $6.42 per share. Incidentally, this forward 2023 estimate equates to a forward earnings multiple of 8.05. This multiple is cheap in any regard as the sector at present trades with an earnings multiple of approximately 17.

Conclusion

Therefore to conclude, although airline stocks such as United Airlines Holdings, Inc. can make poor long-term investments due to their lack of a dividend and their insatiable demand for capital, United is very much in bullish mode at present, as a significant number of aircraft and personnel are expected to come on board shortly. Although binary events always throw up surprises, we expect shares of United Airlines Holdings, Inc. to be higher a month from now. We look forward to continued coverage.

Be the first to comment