Dragan Mihajlovic

Introduction

The Russo-Ukrainian war has caused Uniper SE (OTCPK:UNPRF) many financial problems. Uniper is one of the largest European importers of natural gas (2021 turnover: €164 billion) and has been ravaged by the Russian Gazprom (OTCPK:OGZPY) since June 14. Gazprom is one of Uniper’s main natural gas supplier and has reduced gas supply to Europe below contracted volume, leaving Uniper facing enormous financial challenges.

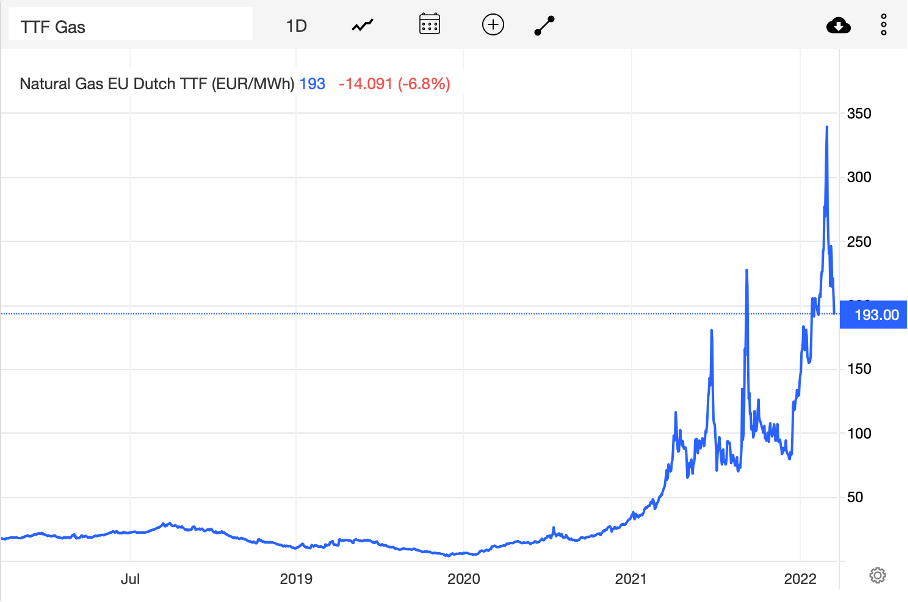

Currently, Russia has completely shut down the Nord Stream 1 natural gas pipeline and no natural gas will flow to Europe until Europe lifts sanctions. The wholesale price of natural gas is up 20x from mid-2020. The government has now intervened by offering a €15 billion rescue package to Uniper.

Biggest Loss In German Corporate History

Natural Gas EU (tradingeconomics.com)

Uniper SE generated the largest loss in German company history of a staggering €12.3 billion in the first half of 2022. As of June 30, natural gas prices have continued to rise, making Uniper’s loss in the second half expected to be even more dramatic.

Europe will have to get through this winter without Russian gas, and US companies like Sempra see this as an opportunity to help Europe. Sempra has signed 3 contracts with European LNG customers to supply Europe with American gas. Sempra has started the initial phase, the plan is being finalized, they still have to finalize the contract with Bechtel before the infrastructure can be built.

Losses Are Expected Until 2024

This status quo is expected to continue for a while, Uniper SE says it does not provide a profit forecast and expects to make a loss until 2024. This is very detrimental to Uniper SE shareholders.

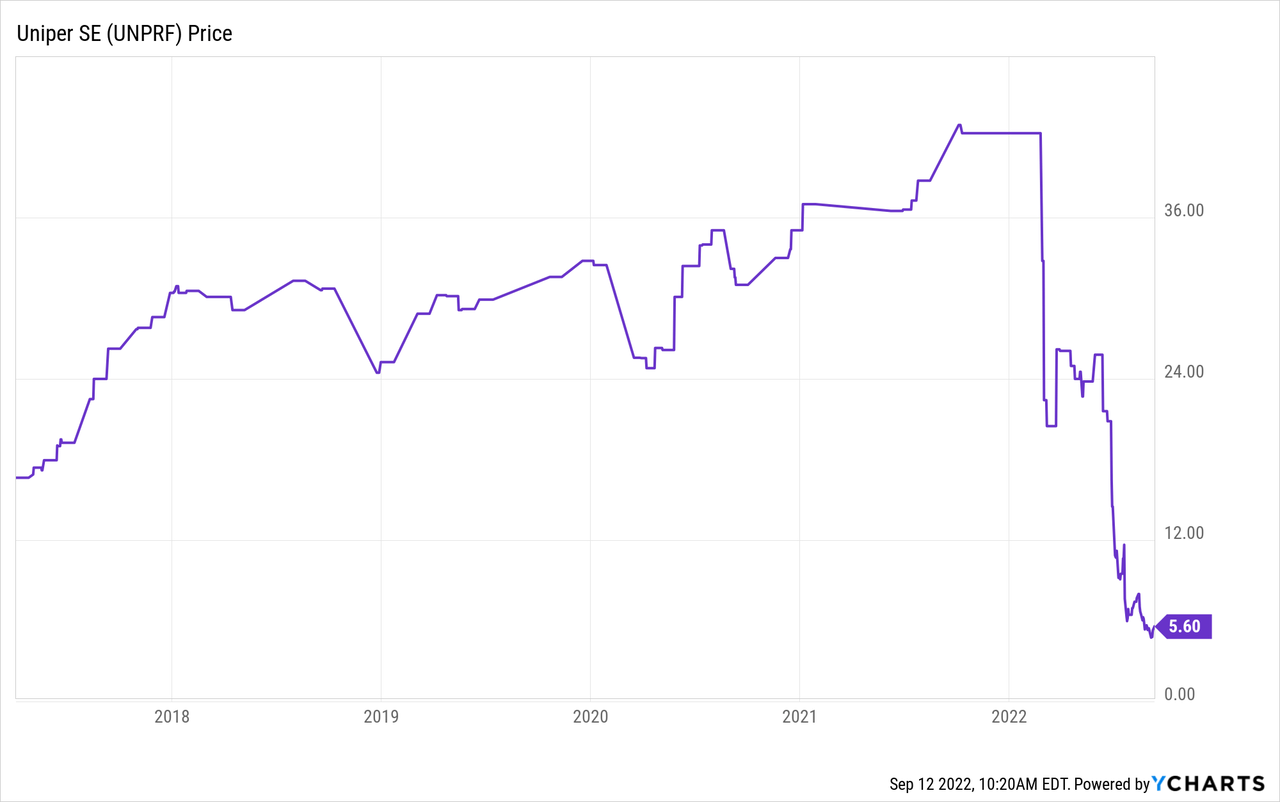

Uniper SE stock has been heavily penalized, the stock peaked early this year and has since fallen by 87%.

Does that mean it’s a good buying opportunity? I expect not. The company is entering a volatile time and will have to wait a little longer until sufficient natural gas reserves are available to continue its activities. CFO Tiina Tuomela talks in their recent earnings transcript:

What is clear is that Russian gas containments will lead to record losses in the third quarter as well as for the full year. As of October 1, the German government will enable gas importers, including Uniper, to pass 90% of the procurement cost for the missing Russian volumes in the final gas customer. This cost as true will be implemented via a general surcharge of around €0.0204 per kilowatt hour, set on Monday by the Market Area Manager Trading Hub Europe. This will dramatically reduce Uniper’s losses from Q4 onwards.

Overall, we must now classify fiscal years 2022 and 2023 as transition years. For 2024, we see light at the end of the tunnel. The funding from the stabilization package, a structural reshaping of Uniper’s gas portfolio and expected strongly reviving operating cash flows other decisive building blocks for giving Uniper a long-term business perspective again. When it comes to the stabilization bucket, the signing of the term sheet was an important milestone but we have still quite some work ahead of us.

Uniper may pass on the costs of missed gas deliveries from Russia to the customer. This is positive for Uniper but will be financially heavy for German citizens and businesses. I believe it is obvious that Germany will end up in a recession. The German government advised Uniper to restart coal-fired power stations. However, this will provide partial relief.

Russia must stop the war in Ukraine and supply natural gas, the cessation of natural gas supplies will also affect Russia’s financial strength.

The shares are a strong sell because Uniper appears to depend completely on government support. I am pretty sure that the German government will not let one of the largest energy companies collapse. But this does not mean that the stock is worth buying.

In my opinion, analyzing a stock valuation is useless because the near future is very unpredictable.

Risks

The Russo-Ukrainian war is quite unpredictable. The oil and gas industry makes up about 25% of Russia’s GDP. It is therefore important for Russia to maintain their financial strength.

If Russia keeps the natural gas taps closed for too long, this will have negative consequences for Russia’s financial strength. Russia could then just decide to supply natural gas again.

Will Europe boycott Russia? I don’t know, but I do expect that Europe will introduce a price cap on Russian gas.

Uniper will improve its financial position when Russia resumes supply of natural gas. This will push the stock up sharply. Uniper expects the loss to continue until 2024, but I think that’s an extreme scenario. I expect 2022 to be a difficult year for Uniper, so I give it a strong sell rating. Perhaps my rating will change in 2023.

Key Takeaway

- Uniper is one of the largest European importers of natural gas (2021 turnover: €164 billion) and has been ravaged by the Russian Gazprom since June 14.

- Uniper SE generated the largest loss in German company history of a staggering €12.3 billion in the first half of 2022.

- The government has now intervened by offering a €15 billion rescue package to Uniper.

- Sempra has signed 3 contracts with European LNG customers to supply Europe with American gas. Sempra has started the initial phase, they still have to finalize the contract with Bechtel before the infrastructure can be built.

- The shares are a strong sell because Uniper appears to depend completely on government support.

Be the first to comment