FXQuadro/iStock via Getty Images

Introduction

While the USA lags behind many developed nations in passenger train travel it has one of the most well-equipped freight networks in the world. Chief among those US freight operators is Union Pacific (NYSE:UNP).

Based in Omaha, Union Pacific is one of the largest transportation companies in the United States, they generate revenue through the transportation of goods, including agricultural products, chemicals, coal, industrial products, and intermodal containers.

And, as it turns out, transportation can be a lucrative business!

Within this article I’ll:

- Provide an overview of the industry and Union Pacific’s place in it

- Provide an update on recent business activity

- Review the financials of Union Pacific versus its peers

- Submit a price target for shares

Railroads in America

Railroads play a pivotal role in the American economy, its estimated that one-third of all U.S. exports and roughly 40% of long-distance freight volume pass through them each year.

In North America, seven major freight railroads connect the continent. Union Pacific and BNSF (BRK.B) hold a strong presence in the western region, while CSX (CSX) and Norfolk Southern (NSC) are the leading operators on the east coast. Canadian Pacific (CP), and Canadian National (CNI), on the other hand, operate routes that run north and south.

Shipping by rail offers many advantages as compared to shipping by truck:

Cost-effectiveness

First of all, shipping by rail can be much more cost-effective than shipping by truck, especially for moving large quantities of goods over long distances. Rail transport usually requires less fuel per mile, and railcars can carry more cargo than a single truck can. Additionally, rail transport often has lower labor costs than trucking, all of which can helps contribute to its reduced costs.

High-Volume Efficiency

Rail transport can be more efficient than trucking, particularly for bulk shipments. A single train can carry the equivalent of several dozen trucks, which helps to reduce the number of trips needed to transport goods. This can be especially useful for long-distance shipments, where it may be impractical to execute a large number of trips back and forth.

Also, rail transport is less affected by traffic congestion and weather-related road closures, which can help to improve delivery times and reliability.

If you’ve ever driven on the 405 in Los Angeles, you might understand how traffic can negatively impact travel speed.

Trains, due to the rail system, are able to avoid most car traffic-related issues.

Environmental impact

Moving goods by rail also yields a lower ecological impact than shipping by truck because rail transport emits fewer greenhouse gases per mile than trucking and it is less disruptive to local communities.

Rail transport can reduce the number of trucks on the road, which can help to reduce air pollution and traffic congestion. To learn more about this topic I would suggest reading this report by ‘Third Way’.

Operations Update

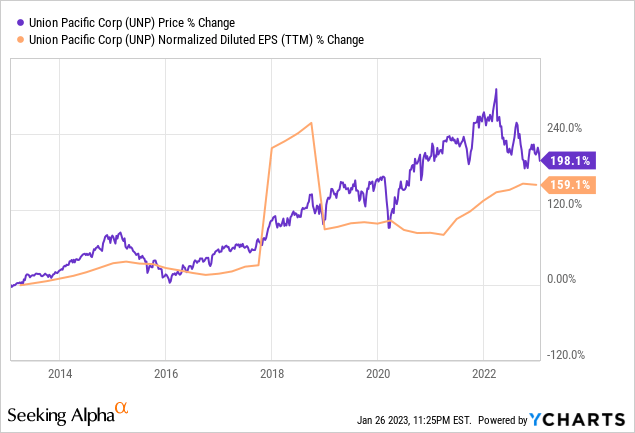

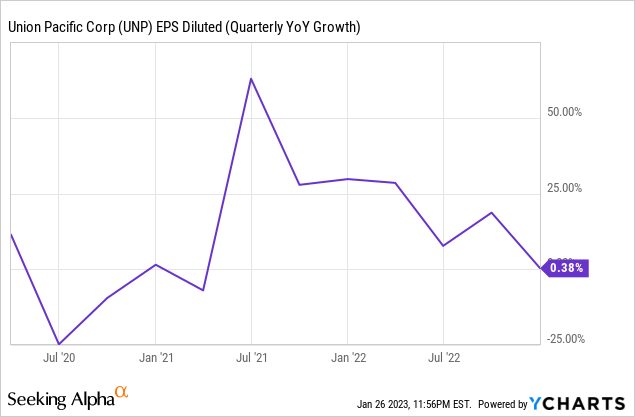

As they reported in their latest earnings report, Q4 EPS was basically flat YoY at $2.67 per share. Flat EPS growth marks a rapid slowdown in earnings growth as compared to prior earnings reports.

It’s my view that this slowdown is driven, at least in part by, the expected weakening of the global economy and a plausible recession hitting us in 2023.

As companies brace for a recession they often cut capital investment which has a direct impact on the volume of goods transported via rail. The implication of this is that Union Pacific has an inherently cyclical business that may be strongly correlated to the US economy as a whole. The premise is simple, less economic activity in the US and fewer goods that need to be transported by rail.

So, can growth pick up from here?

I would argue it can, and here’s why: Inflation, and especially wage inflation can be quite sticky, and Union Pacific is less exposed there. Rail as compared to trucking relies much less heavily on labor as a part of its cost structure and much more on capital like steel and lumber. Sure, unionized labor remains an issue in rail, but the model simply requires less labor overall. It’s my view that even if the unionized workers achieve their goals and labor becomes more expensive for rail transport, it might still be cheaper than trucking.

Financials

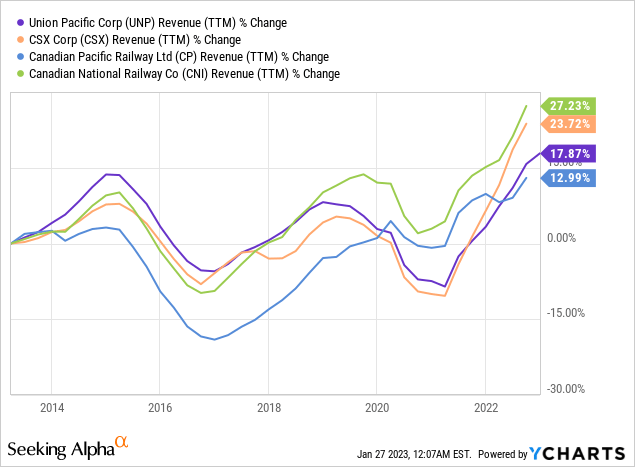

Revenue

Looking at the chart above we can see that revenue growth has been quite choppy for the rails over the past decade going through many bouts of booms and busts. The end result is that revenues have moved up between 13% and 27%. Union Pacific is close to the middle of the pack according to this metric boasting 17.87% growth over the past 10-year period.

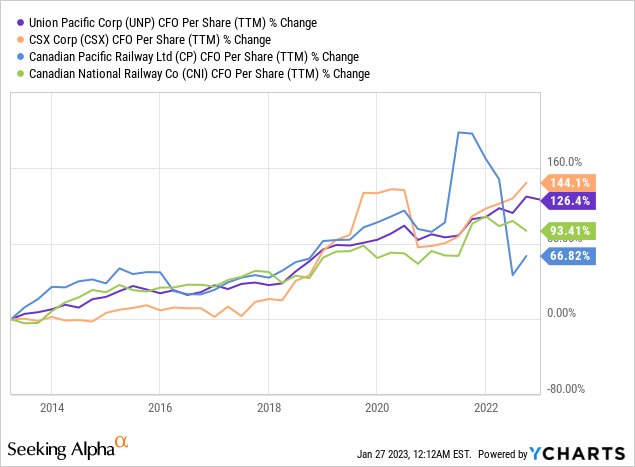

Operating Cash Flow

But where these companies lack in revenue growth they at least partially make up for it in operating cash flow per share growth. Most of these companies have doubled their CFO per share since 2013 and UNP has more than doubled their CFO, increasing by 126% over the last decade.

This is what I like to see!

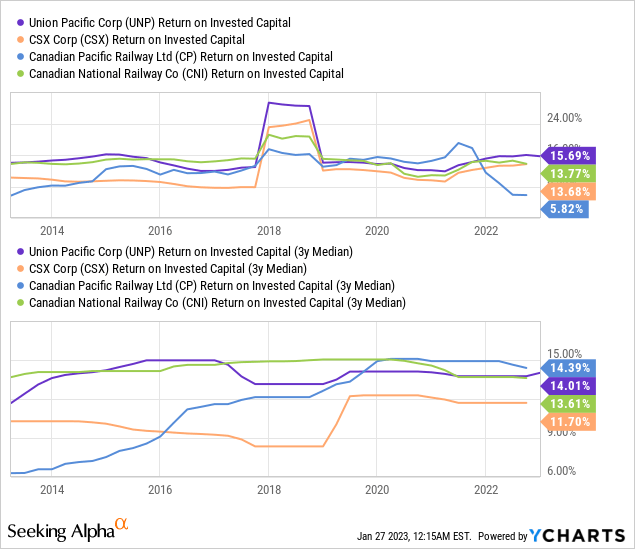

Return On Invested Capital

This is where the story gets even brighter. Union Pacific has maintained a mid-teens ROIC consistently over the past decade, 14% is quite solid. Such consistency tells me that the management is disciplined, choosing to invest in projects that make sense at the right price. I believe shareholders are greatly rewarded by this.

Risks

As I mentioned earlier, there are some risks that apply to the rail industry, notably its cyclical nature. Within this section, I would like to expand on two other risks: competition and capital intensity.

Competition

Freight is not immune to competition. Trucking companies, for example, may offer lower prices or more flexible delivery options to attract customers away from rail transport. The implementation of autonomous truck drivers could ramp up competition from trucking and threatens to nullify rails’ labor advantage. These threats can make it more difficult for rail companies to maintain pricing power and profitability.

Capital Intensity

The rail industry is inherently capital-intensive, which means that companies need to constantly invest in new locomotives, rail cars, and infrastructure to keep the service running.

For example, rail companies may need to invest in new tracks, signals, and other infrastructure to improve capacity and maintain efficiency. Rail companies may need to invest in new locomotives and rail cars to keep up with changing customer demand or to comply with new regulations. It’s plausible we could see left-leaning states mandate the use of modern locomotives which may be more fuel efficient.

To finance investments like these, companies may need to raise capital (likely through debt offerings), which may increase the riskiness of the business and/or threaten profitability.

Conclusion

Union Pacific has the markings of a great company, strong cash flow growth, strong ROIC, and a consistent business model with a decent moat. Compared to the valuations of its peers, Union Pacific seems slightly underpriced.

| Company | Current Stock Price | EPS 2024 Est. | 2023 P/E |

| UNP | $201 | $12.69 | 15.9 |

| CSX | $30 | $2.03 | 14.9 |

| CP | $77 | $3.75 | 20.5 |

| CNI | $119 | $6.43 | 18.4 |

| Average PE (excl. UNP) | 17.9 |

(Source: Yahoo Finance & Author’s Calculations)

Applying its peers’ PE ratio to Union Pacific’s estimated forward earnings yields the following prices:

Yahoo Finance & Author’s Calculations

In conclusion, I rate Union Pacific a “Buy” with a 1-Yr price target of $228.

Union Pacific has stronger returns on capital while revenue growth and cash flow growth are relatively in line with peers, therefore I do not believe a discount is warranted.

Thank You, Reader!

I hope you enjoyed today’s article, if you’d like to talk about anything discussed in the article above, please feel free to chime off below. Thank you!

Be the first to comment