MarsBars

Having read many books on investing, I’ve retained a number of maxims from the greats in the industry. One of those that stick out is a saying by Peter Lynch that money can be made investing in companies that fresh out of school MBAs don’t want to work at.

One of the reasons for that is because these companies tend to me mature and don’t require a ton of highly paid strategists to run, as Harvard MBAs are expensive! This brings me to Union Pacific (NYSE:UNP), which likely ranks low on the list of companies that fresh highly paid grads want to work at. This article highlights why UNP appears to be a wonderful company that’s fairly priced at the moment.

Why UNP?

Union Pacific is a leading railroad company in the U.S., providing rail, intermodal, and rail-to-truck transload services across 23 states in the western two-thirds of the country. It has a long history, dating back to the early 1800s, when it was chartered by the U.S. Congress to build a transcontinental railroad. Today, the company is a key player in the transportation industry, serving a diverse range of customers in the agricultural, automotive, chemical, coal, manufacturing industries

One of the key factors driving Union Pacific’s success is its extensive network of rail lines, which stretches more than 32K miles across 23 states. This network gives the company a strong competitive advantage, allowing it to reach a large number of customers and destinations. Union Pacific’s network is also well-connected to other railroads, ports, and intermodal facilities, providing the company with access to a broad range of transportation options.

In addition to its strong network, Union Pacific has a modern and efficient fleet of locomotives and railcars, and there’s no denying that rail transport remains one of the most cost effective ways to transport goods over long distances on land, especially when it comes to low value to weight ratio bulk commodities.

Plus, it helps to be in an industry that’s been largely consolidated into just a handful of players, with CSX (CSX) and BNSF (BRK.A)(BRK.B) being the other larger players. This serves as a massive barrier to entry, considering that the big players enjoy network effects, with little to no incentive to forking out a boatload of capital to build another mainline.

This translates into pricing power and robust shareholder returns. As shown below, UNP stock has largely outperformed the S&P 500 (SPY) over the past decade, producing a 321% total return.

UNP Total Return (Seeking Alpha)

UNP continues to demonstrate strong results, with operating revenue growing by 18% YoY to $6.6 billion during the third quarter, driven by higher fuel surcharges, volume growth, and price growth. Nonetheless, UNP is seeing headwinds from higher inflation and ongoing network inefficiencies, raising its OR (operating ratio) to 58.2%.

For reference, OR is calculated by taking operating expense divided by revenue, so lower is better for this ratio. Management reiterated a long-term target of achieving 55% operating ratio during the recent Credit Suisse Global Industrial Conference.

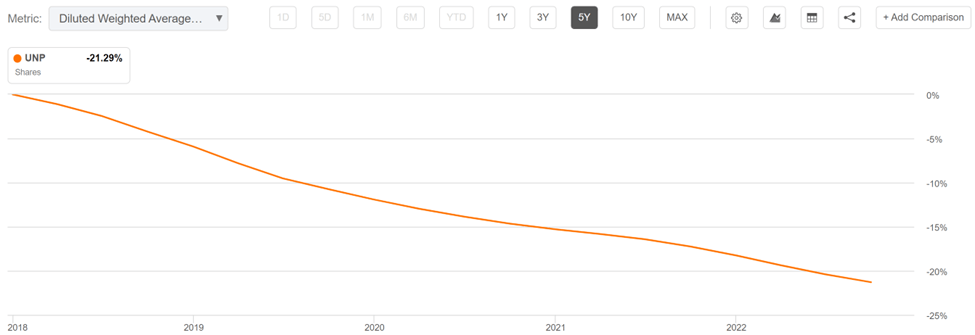

Importantly, UNP exhibits the hallmarks of a mature business that returns a ton of cash back to shareholders, as reflected by the 4 to 6% annual share buyback rate in recent years. As shown below, UNP has retired an impressive 21% of its outstanding float over the past 5 years alone.

UNP Outstanding Shares (Seeking Alpha)

Looking forward, I would expect buybacks to slow somewhat, given the potential for higher fuel costs, but the divided should remain very safe, with the support of an A- rated balance sheet. Management reiterated its commitment to the dividend and suggested that it will no longer be levering up the balance sheet to buy back shares, as noted during the industry analyst conference call:

I think it’s important to level set in terms of how we prioritize the use of our cash. So first dollar goes back into the business in terms of our capital investment. You know, the railroad is our lifeblood. It’s our engine. And so that’s where we put our first dollar of cash.

Our next priority is our dividend. And so we have a dividend target of 45% that we think is appropriate for our business. We want to be able to give our shareholders that you know, more certain return on cash. And then the excess cash is where we use it for share repurchases. And what that has historically meant is not only use of excess cash from operations but also using our balance sheet.

And so we have since 2018, you know, we put forth a new target that we were going to increase the leverage on our balance sheet, and that has been a big sustainer of some of those share repurchases. So we’re at a point today where I would say the balance sheet is largely optimized.

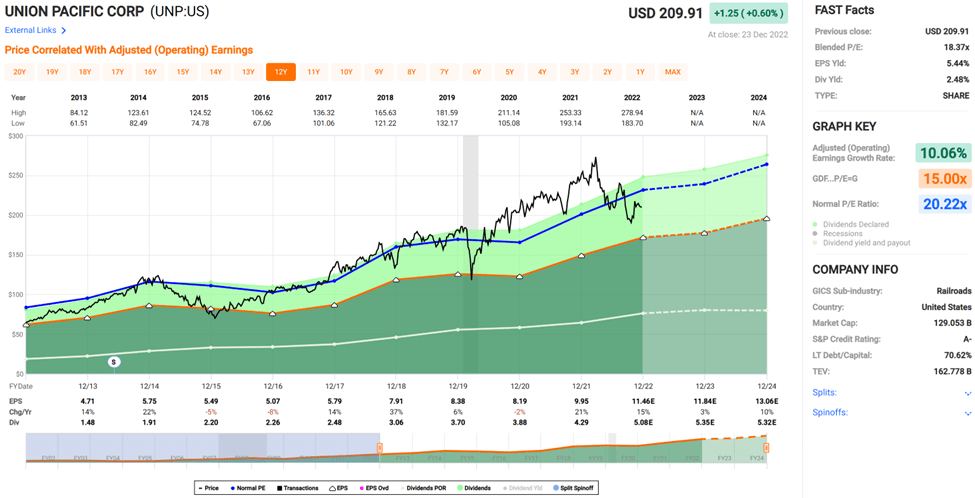

Considering the high interest rate environment and the muted potential for share buybacks, I find UNP to be fairly priced at the current price of $210 with a forward PE of 18.3. As such, value seekers may want to wait for an entry point at or below $200. This translates to a PE of 17.4, which gives a better margin of safety, and sits well below UNP’s normal PE of 20.2.

UNP Valuation (FAST Graphs)

Investor Takeaway

Union Pacific is a well-run railroad operator that has been able to generate market beating returns for shareholders over the past decade. The company has an impressive track record of returning capital back to shareholders via share repurchases and dividends, although I expect buybacks to slow down due to UNP’s already fully optimized balance sheet and the higher interest rate environment. Nonetheless, UNP carries an enduring moat that isn’t likely to go away anytime soon, if ever. For the reasons above, I view UNP as being a solid Hold at the moment.

Be the first to comment