Poulssen

Thesis

In a turbulent stock market environment, many investors look for exposure in the consumer staples sector, exploring more defensive investment opportunities. Unilever PLC (NYSE:UL) is a multinational consumer goods company focusing, mainly on personal care, beauty and food & beverage. In this analysis, I examine the company’s business attributes and financial performance. The stock’s valuation is also considered.

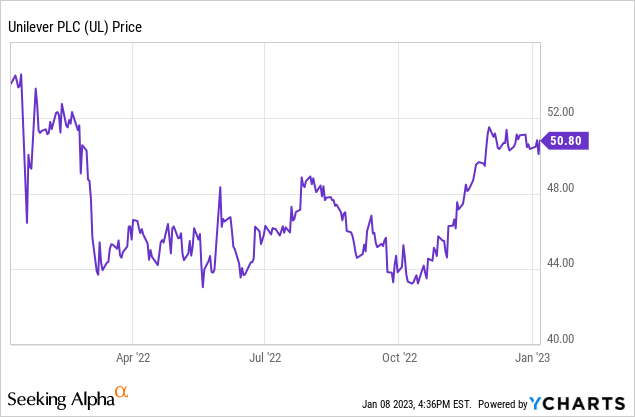

After a sharp decline in the beginning of 2022 and a noticeable consolidation pattern through the third quarter, UL has recovered significantly in the fourth quarter. Currently, the stock trades at $50.80 per share ($128.5B market cap) and pays a 3.32% dividend.

Diversification as the Priority

Unilever chooses to employ a strong diversification strategy on many fronts. Firstly, its global portfolio of around 400 brands revolves around many consumer staples product categories, including beauty, personal care, food & beverage and home care. Some of the company’s most notable brands include household names like Dove, Hellman’s, Ben & Jerry’s, Axe, Rexona, Vaseline and others. In fact, 12 brand families in Unilever’s portfolio account for over $1B in revenue with many more reaching for this mark.

Investor Presentation 2022

Diversifying across product categories achieves a few things, in my view. On one side, the company solidifies its position against competitors. A single-area focused company could be easily hurt when competitors target this part of the market and offer either less expensive products or more innovative ones. The scale that Unilever has, however, across different product categories makes it especially hard from smaller-scale companies to adversely affect its sales status.

Moreover, all of the company’s products are deemed essential for consumers and therefore maintain somewhat inelastic demand curves. This makes the company’s revenue mix resilient against downturns in the market cycle. Finally, in the case that supply chain disruptions or shortages occur for some product groups, the company’s operations are not largely affected. Unilever also maintains a commitment towards delivering premium quality products to consumers, differentiating the company further from low-cost competition. Unilever is also very well geographically diversified with large portions of total revenue originating outside the United States.

A Reinforced Distribution Channel

Unilever maintains an omni-channel distribution approach. From online-retailers like Amazon (AMZN) to Walmart (WMT), Target (TGT) and smaller grocery stores, the company’s products are widely available to almost every consumer across the U.S. and the world. As Unilever turns toward increasing digitalization, it is also expanding its direct-to-consumer distribution channel. DTC (eCommerce) sales are known to allow for larger profit margins and increased efficiency.

Financials

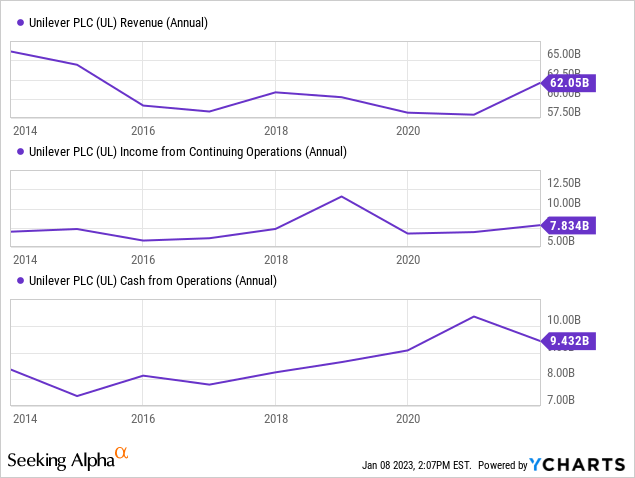

Over the past 10 years, revenue has recorded a very moderate 1.40% annualized growth, somewhat accelerating over the last 3 years to 3.50%. For the 2022 fiscal year, the company is expected to generate around $63.5B in sales. Net income has also seen little growth over the 10-year period, while Cash flow productivity has somewhat recovered, reaching $9.4B. Overall, the company records moderate financial performance, more or less comparable with the slow-growth attributes of the consumer staples sector.

Profitability-wise, margins appear strong across the board. A 46% gross margins beats the sector average of 32%, while the same is true for both EBIT and Net margins, standing at 17.5% and 10.4%, respectively. Return on equity has also been rather impressive at 31%. The company’s operational model is very efficient, with growth seemingly being the missing part.

Over the past couple of years, both R&D spending and Capex have increased as a percent of revenue. Expected to boost innovation and digitalization, it remains to be seen how the increased spending will affect the financial performance.

When it comes to the financial health of the company, Unilever’s balance sheet gives some moderately concerning signals. A 0.8 current ratio indicates somewhat weak liquidity for the company, despite a significant cash stockpile of $6.9B. Unilever carries significant amounts of debt, although not at alarming levels, with a debt/capital ratio of 0.43x and $35.6B in total debt obligations. Debt/Free Cash Flow (“FCF”) stands at 13x, which is significantly higher than its peers. Desirable debt/FCF levels for more conservative investors often stand around 5 or 6x for slow growth companies.

The Dividend Perspective

Like many large companies in the consumer staples sector, Unilever pays an above-market average dividend. In fact, the company offers a pretty large 3.32% yield, higher than many of its competitors. Despite that, dividend growth over the past decade hasn’t been strong at all. Unilever has recorded a weak 10-year 3.90% annualized dividend growth and a 5-year 2.85% growth. The company has struggled to increase distributions as Free Cash Flow generation performance has failed to increase over time. The company gets a C- dividend safety score from Seeking Alpha.

Market Dominance is Threatened

When considering an investment in any company, the most important risk factors concerning its performance should be carefully considered. The main one for Unilever, despite its strong position in the market, achieved through diversification, as discussed earlier is, still, competition. Dozens of direct-to-consumers, online-only companies try to market products, especially in the personal care and beauty segments of the market. Large store chains like Walmart, Costco and others also keep introducing house-brands that offer low cost alternatives to Unilever’s products.

A large international sales footprint also comes with significant possible currency translation losses when volatility spreads in FX markets. The current macroeconomic and supply chain situation is also rather unfavorable, although it is likely to improve in 2023.

Valuation

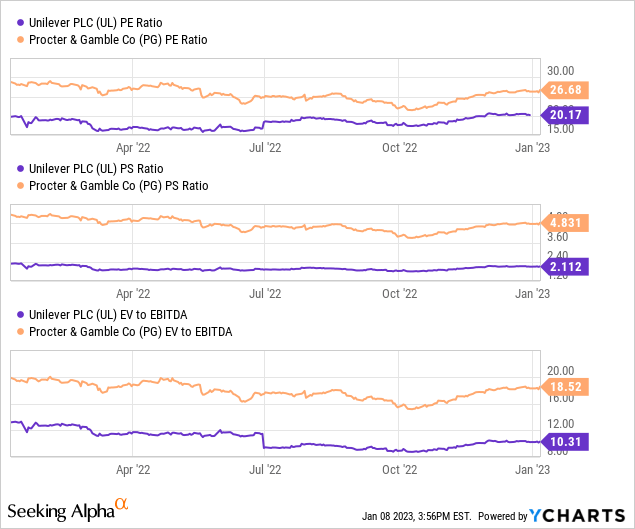

While attempting to gauge Unilever’s valuation attractiveness, Unilever is compared to Procter & Gamble (PG), arguably its largest competitor and a rather comparable business in terms of product offerings. It becomes quickly evident that Unilever is much more cheaply priced compared to P&G. The company trades at a 20x P/E multiple, a 2.1x P/S ratio and a 10.3x EV/EBITDA. While the P/E multiple still stands above market average, both the P/S and the EV/EBITDA metrics indicate a reasonably priced stock.

Putting it all Together

After all things are considered, despite a reputable, well-diversified brand portfolio, Unilever PLC lacks the strength in financial performance that most investors seek when selecting even a more defensive stock in the consumer staples sector. For these reasons, and after examining a more-or-less reasonable valuation for Unilever PLC stock, I would assign a hold rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment