PhonlamaiPhoto

The Global X Copper Miners ETF (NYSEARCA:COPX) provides exposure to a basket of copper producers and related companies. In my opinion, commodity producers like copper miners may stand to benefit the most if China uses a replay of its 2009 playbook to stimulate its moribund economy in 2023. I expect COPX to outperform on the back of pending Chinese stimulus, as long as the rest of the world does not suffer a severe recession.

Fund Overview

The Global X Copper Miners ETF provides targeted exposure to a basket of copper miners. The COPX ETF tracks the Solactive Global Copper Miners Total Return Index (“Index”), an index designed to measure the performance of a broad-based portfolio of companies involved in the copper mining industry. These involve copper miners, refiners, and exploration companies.

To be eligible for the index, companies must be listed on a regulated stock exchange with shares tradeable by foreign investors without restriction and have a free float market capitalization of at least US$200 million and average daily traded value of US$500,000. The companies must derive or expect to derive significant revenues from copper mining or closely related activities (exploration and refining). The index has a minimum of 20 securities and a maximum of 40 securities. Index weight is determined by free float market capitalization and individual weights are capped at 4.75%. Excess weight is redistributed to index participants whose weight is not capped.

The COPX ETF has been fairly popular, with $1.7 billion in assets and charges a modest 0.65% expense ratio.

Portfolio Holdings

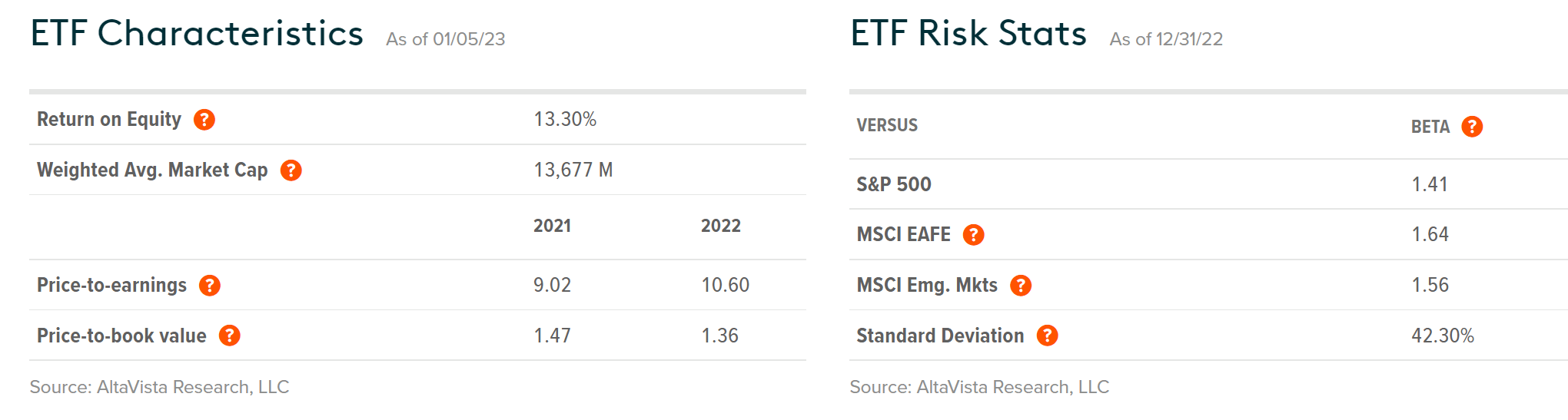

Figure 1 shows the portfolio characteristics of the COPX ETF. The fund’s holdings average market capitalization of $13.7 billion and trades at average Price-to-Earnings ratio of 10.6x.

Figure 1 – COPX portfolio characteristic (globalxetfs.com)

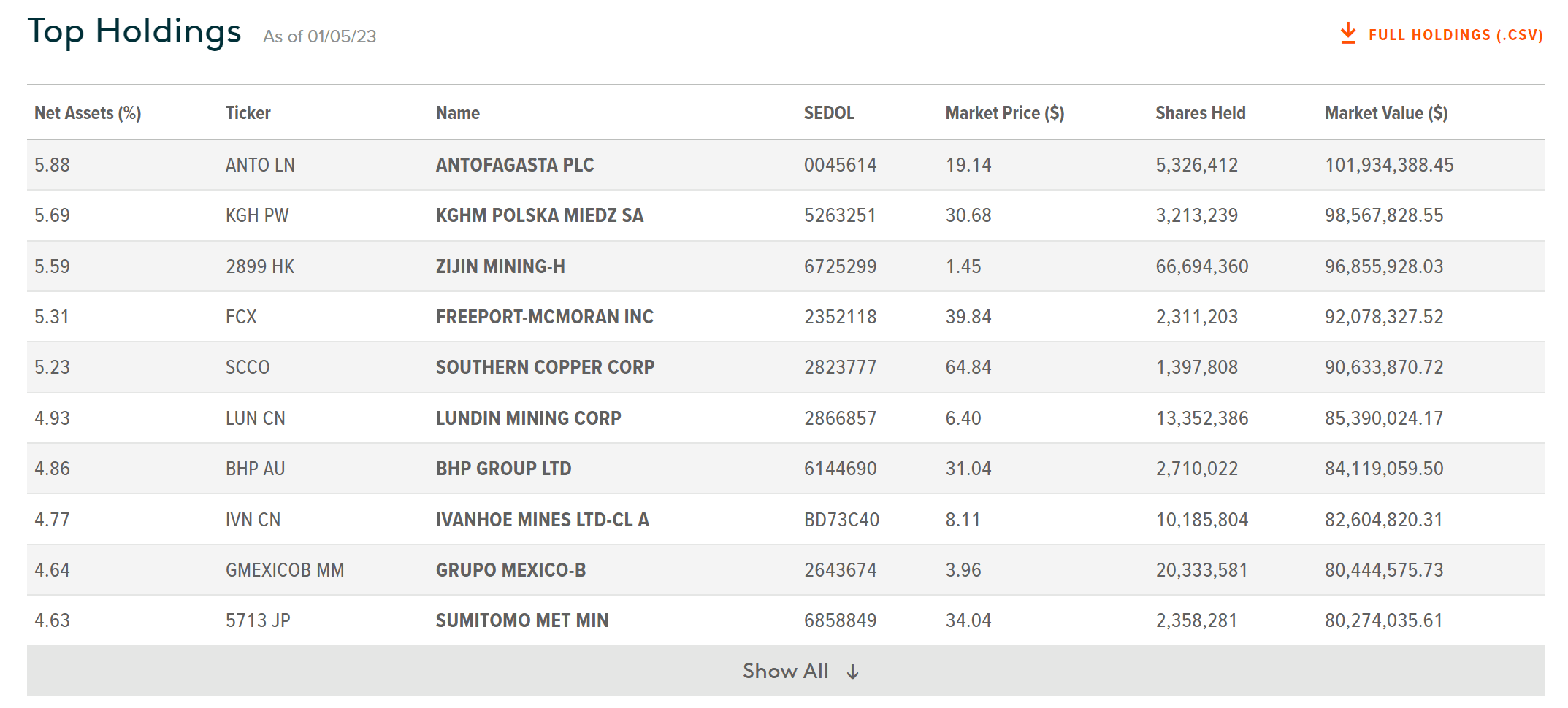

Figure 2 shows the top 10 holdings of the COPX ETF, which account for 51.5% of the fund’s assets. Investors not familiar with the mining industry may not recognize some of the top holdings, many of which are international companies.

Figure 2 – COPX ETF top 10 holdings (globalxetfs.com)

One of the features of the COPX ETF is that individual positions are capped at 4.75% weight at each rebalancing date, so the fund is not overly dominated by one or two megacap conglomerates. For example, BHP Group Ltd. (BHP), the mining behemoth with US$165 billion market cap, has the same weighting as Lundin Mining Corp. (LUN:CA) with C$7 billion market cap.

During commodity bull markets, small- to mid-cap companies tend to outperform, which benefits COPX’s weighting style (conversely, during commodity bear markets, they underperform).

Returns

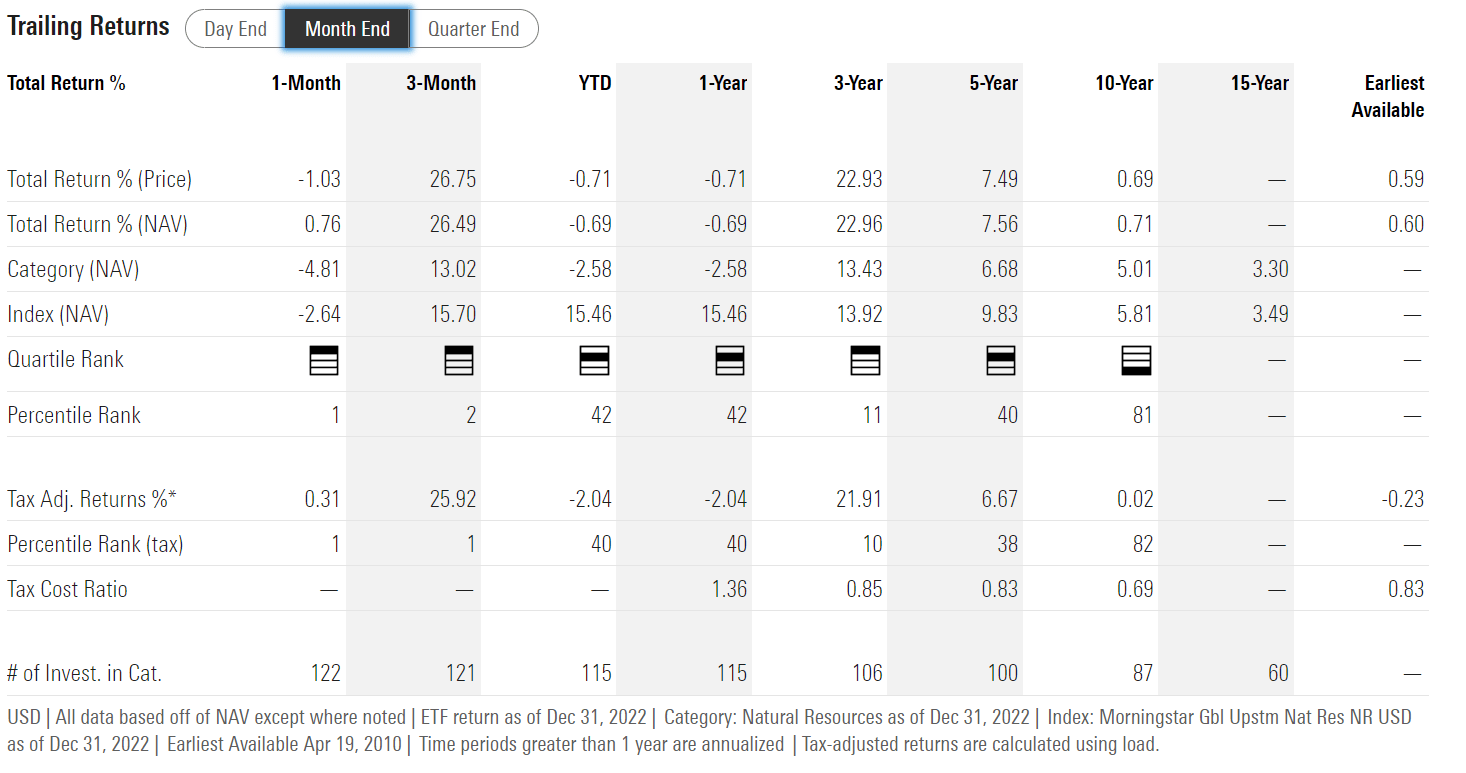

Figure 3 shows the COPX ETF’s historical returns. The fund has performed well in the medium term, with 3Yr and 5Yr average annual returns of 23.0% and 7.6% to December 31, 2022. However, its 10Yr average annual return of 0.7% has been poor.

Figure 3 – COPX historical returns (morningstar.com)

Visually, we can see that the COPX ETF was launched in 2010, essentially near the peak of the commodity supercycle driven by China’s voracious appetite for raw commodities (Figure 4).

Figure 4 – COPX price chart (stockcharts.com)

As the commodity supercycle peaked and declined in the early 2010s, COPX suffered a large drawdown from almost $50 / share to a low of sub $8 / share in early 2016.

In recent years, COPX has benefited from copper’s ‘ESG’ credentials, especially in the aftermath of the COVID-pandemic. According to COPX’s marketing materials, “copper is an essential input in electric vehicles, renewable energy storage, and other forms of next-generation infrastructure that we expect to gain popularity”.

Distribution & Yield

COPX paid a trailing $1.11 / share in distribution or 2.9% distribution yield. COPX’s distribution is paid semi-annually.

Mining Stocks Strong Out Of The Gates In 2023

In a recent article on the Materials Select Sector SPDR Fund (XLB), I noted that many metals and mining companies such as BHP and Freeport-McMoRan Inc. (FCX) had very strong returns out of the gates in 2023, returning 7.6% and 11.5% respectively in the first week of the year. With many economists expecting a global recession in 2023, it is odd that mining companies are outperforming, since mining companies tend to be very cyclical. What was behind these strong moves and is the trend sustainable?

China Set To Stimulate Its Economy in 2023

I believe the strong move in metals and mining stocks have been driven by recent news out of China where multiple sources such as Bloomberg and Reuters are reporting that the Chinese government is set to loosen its ‘three red lines’ policy in the coming months.

Chinese Economy Suffered From Real Estate Restrictions…

Recall, the Chinese government began implementing its ‘three red lines’ policy in 2020 in order to deflate a rampant housing bubble. Government officials were concerned that real estate had become a ‘one-way bet’ and was worsening a wealth inequality gap. The government targeted the debt levels of its property developers, limiting how much new debt they could raise.

By 2021, the government policies designed to slow real estate speculation morphed into a full blown housing crisis, as many property developers were pushed to the brink of bankruptcy, including Evergrande Group, once considered the most valuable real estate company in the world. Interested readers can check out Capital.com, which has good coverage of the Chinese housing crisis.

As the housing crisis progressed into 2022, Chinese policymakers tried multiple times to restart lending in its property sector. However, Chinese homebuyers were reluctant to buy, as the official party line was still against real estate speculation. This helped cause China’s GDP figures to miss the official 5.5% target in 2022.

… And Zero-COVID In 2022

Another factor that had worked against China’s economy in 2022 was the government’s draconian response to the COVID-19 virus. While the rest of the world had vaccinated (to varying levels of success) their vulnerable populations and mostly reopened their economies, China stuck to its Zero-COVID policies, often locking down whole regions and cities at the first sign of COVID-19 cases.

While this approach protected its citizens (the official death toll from COVID-19 was ~5,000 in China vs. 1.1 million in the US), China’s draconian policies took a major toll on its economy and threatened to tear apart China’s social fabric. By November, Chinese citizens were fed up with Zero-COVID and took to the streets in massive protests.

After the massive protests in November, we saw the Chinese government’s stance begin to change in early December. PCR test centers were dismantled virtually overnight and travel restrictions were lifted. Infected citizens no longer had to quarantine in ‘quarantine camps’ and contact tracing was canceled. Although this policy shift has led to an incredible surge of COVID cases in the short-term, it does pave the way for China to re-open its economy in the coming months.

Will China Use The 2009 Playbook In 2023?

I believe news that the Chinese government is rolling back its ‘three red lines’ policy will likely be followed by official stimulus measures designed to revive its flagging economy. One of the quickest ‘bang for the buck’ forms of stimulus is infrastructure and real estate investment, similar to the 4 trillion RMB stimulus program China announced in 2009 (amounting to 13% of GDP at the time).

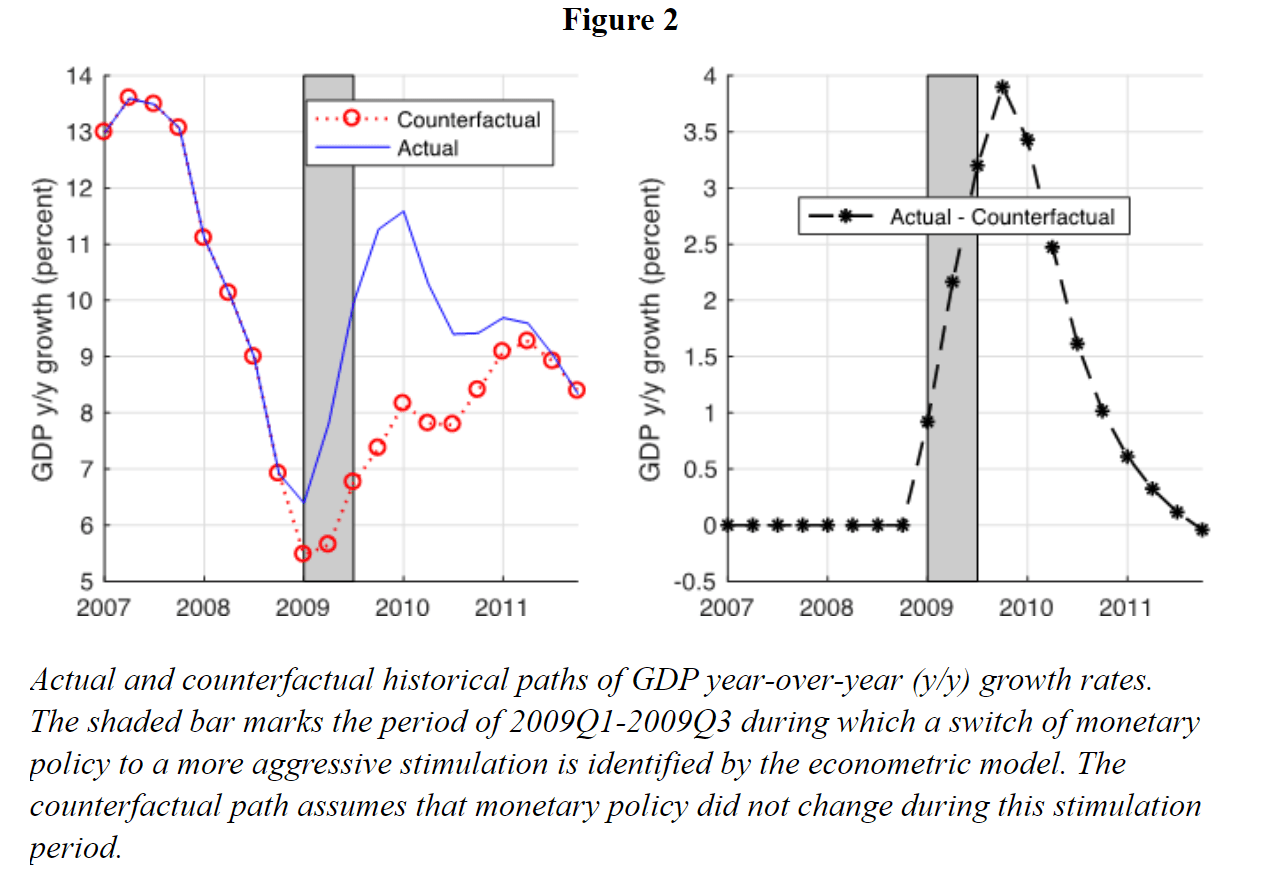

China’s massive 2009 stimulus boosted its GDP growth rate from sub-7% in 2009 to over 11% in 2010 (Figure 5).

Figure 5 – Chinese GDP figures circa 2009 (voxchina.org)

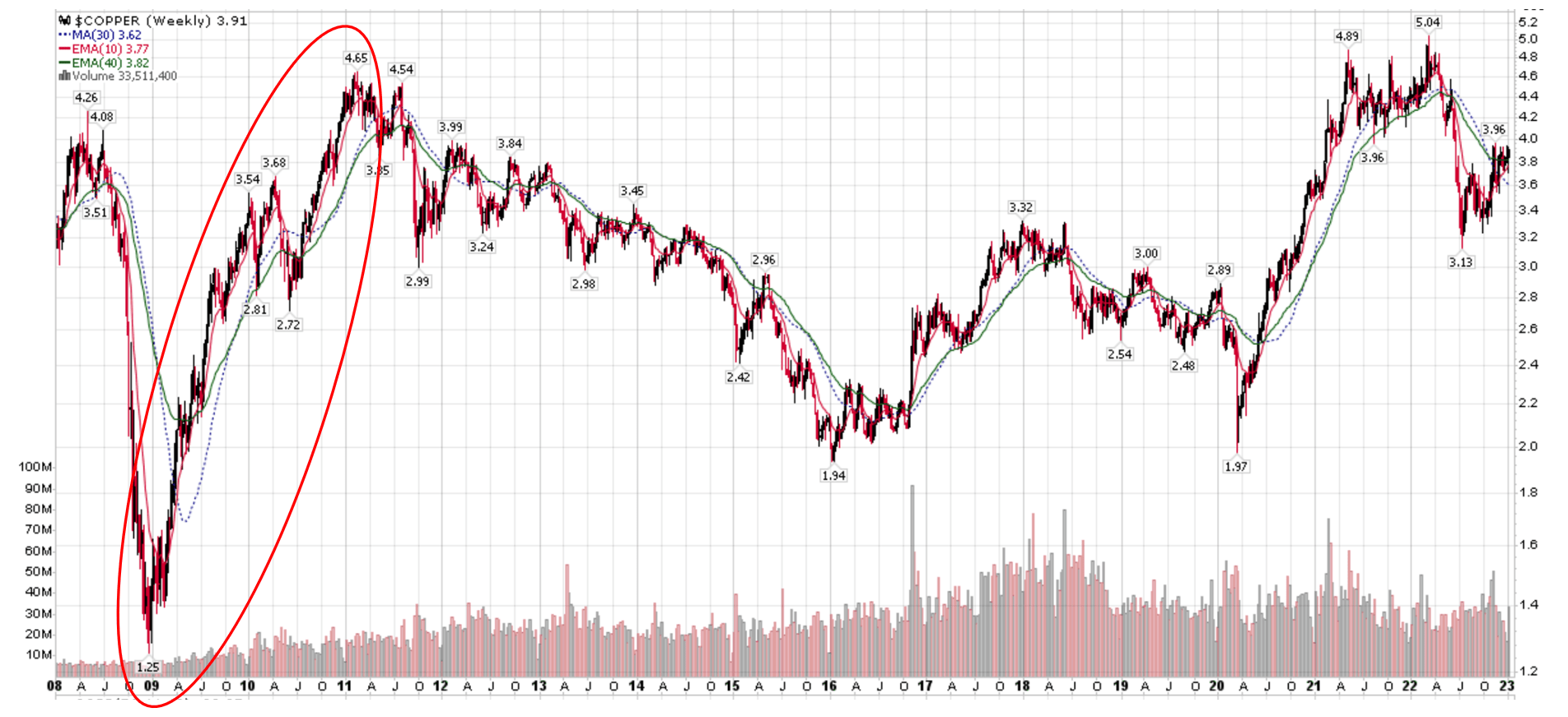

The infrastructure-heavy stimulus program turbo-charged the price of many commodities like copper, which rallied from a low of $1.25 in early 2009 to $4.65 in early 2011 (Figure 6).

Figure 6 – Commodities were prime beneficiaries of China’s 2009 stimulus (Author created with price chart from stockcharts.com)

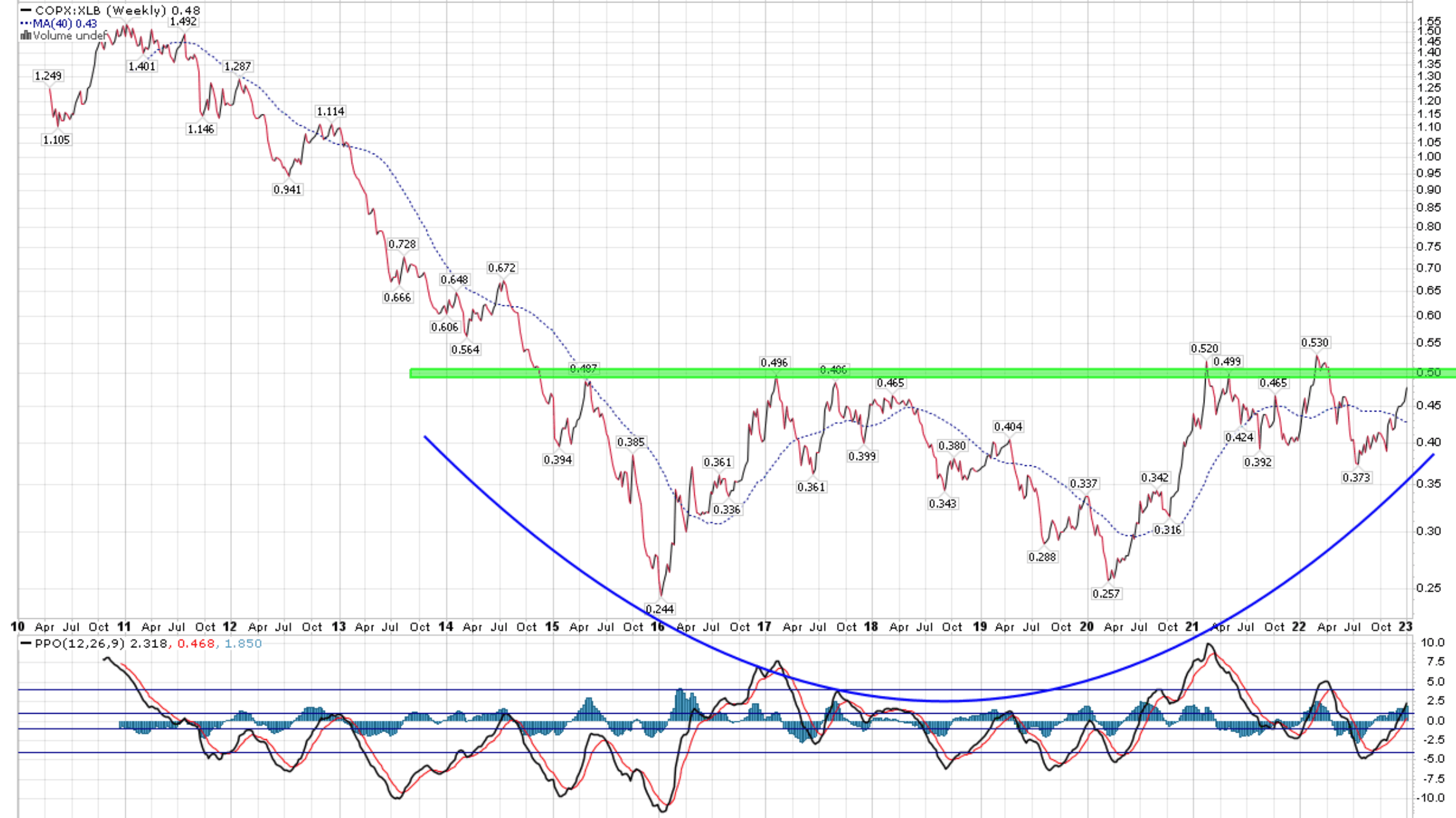

If history repeats, we could see a strong price response in copper in the coming quarters, which should drive outperformance of the COPX ETF relative to the rest of the materials sector. Already, we are seeing the ratio of the COPX ETF relative to the XLB ETF form a multi-decade bottoming pattern, with a breakout pending at around ~0.50 (Figure 7).

Figure 7 – COPX forming multi-decade bottoming pattern relative to XLB (Author created with price chart from stockcharts.com)

Technicals Suggest A Re-test Of 2022 Highs Is In The Cards

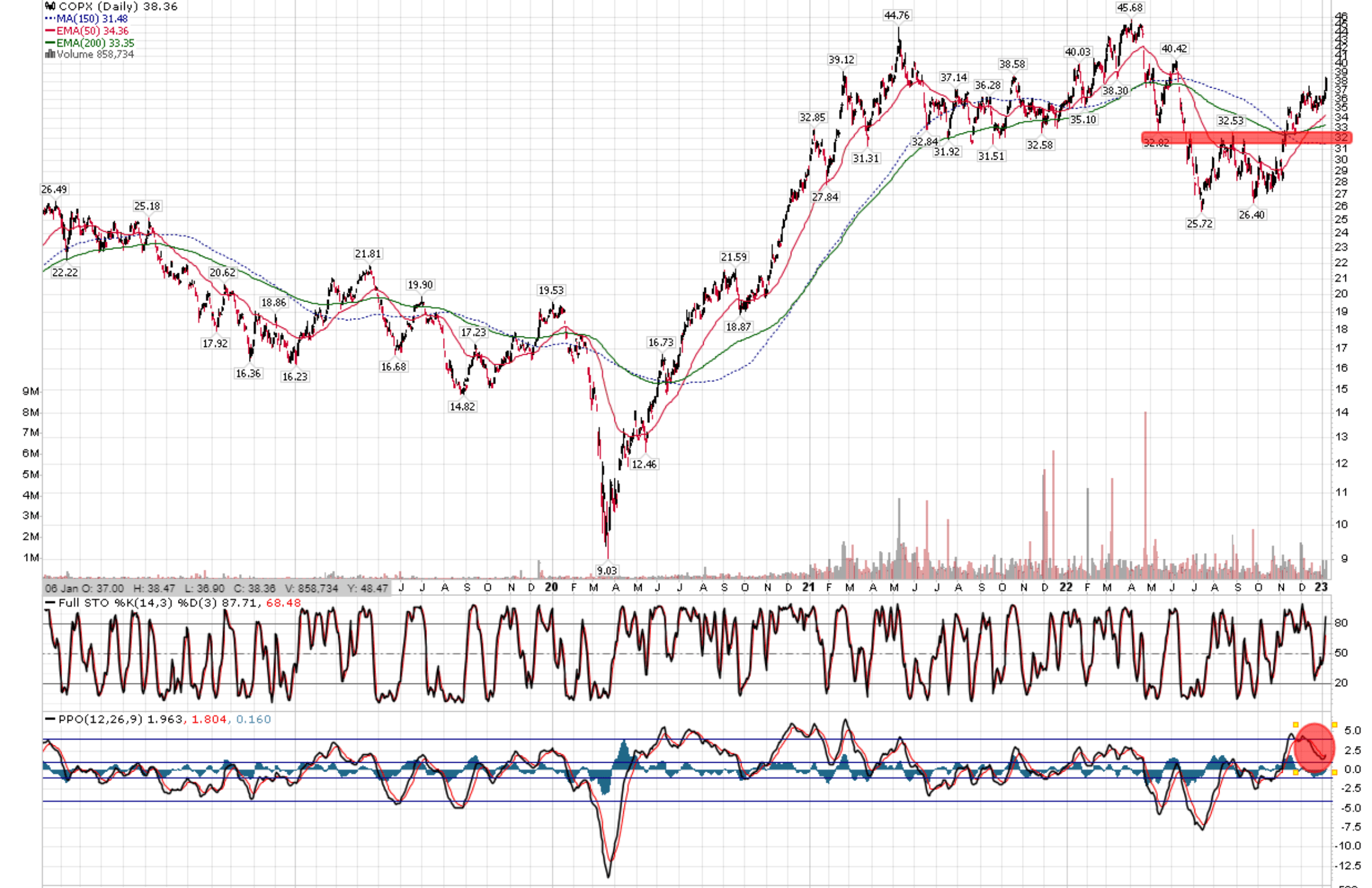

Technically, the COPX ETF looks poised to re-test 2022 highs at around ~$45 after triggering a mechanical buy signal on the PPO indicator. I would use the 2022 breakout level of ~$32 as a stop loss / reassessment level (Figure 8).

Figure 8 – COPX looks poised to retest $45 (Author created with price chart from stockcharts.com)

Risk

The biggest risk to my bullish thesis for COPX is that the current macro environment is quite different than 2009. In 2009, the Great Financial Crisis (“GFC”) caused a synchronized global recession, and governments and central banks stimulated their economies at around the same time.

In contrast, currently, western governments and central banks are grappling with an inflation problem and are actively trying to slow down their economies. In fact, many economists like the IMF and the World Bank are forecasting a global recession in 2023 partly because of restrictive policies. So the pending Chinese stimulus’ impact on copper prices could be tempered by economic slowdown in the rest of the world.

Furthermore, China’s 2009 stimulus program arguably led to a decade of corruption and dozens of ‘ghost cities’ – misdirected infrastructure spending that wasted government resources. China may be hesitant to unleash a stimulus plan as large and broad as the 2009 stimulus.

Conclusion

The COPX ETF provides exposure to a basket of copper producers and related companies. In my opinion, commodity producers like copper miners will likely benefit the most if China uses a replay of its 2009 playbook to stimulate its moribund economy in 2023. I expect COPX to outperform on the back of pending Chinese stimulus, as long as the rest of the world does not suffer a severe recession.

Be the first to comment