Roman Mykhalchuk/iStock via Getty Images

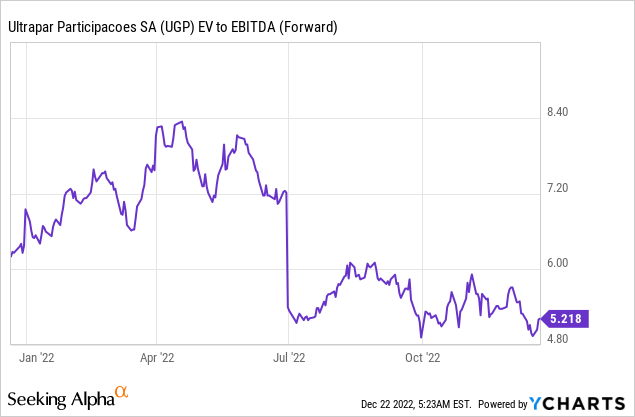

Brazilian fuel distribution leader Ultrapar (NYSE:UGP) confirmed its growth ambitions with an aggressive new capex plan for FY23. Unsurprisingly, most of the capex dollars will be allocated to fuel distribution subsidiary Ipiranga and the LNG distribution arm Ultragaz, where EBITDA margins continue to trend strongly. My only concern is free cash generation – despite outperforming in Q3 on a headline basis, FCF would have been negative after adjusting for working capital benefits. While the balance sheet should support most of the funding needs for now, the sustainability of the FY23 capex run rate and the resulting impact on the yield are areas to monitor going forward. The valuation seems undemanding at ~5x fwd EV/EBITDA. Still, the funding risk is a concern, along with potential post-election changes to the regulatory regime (e.g., a return of federal taxes on fuels next year). On balance, I remain neutral.

An Aggressive FY23 Capex Update

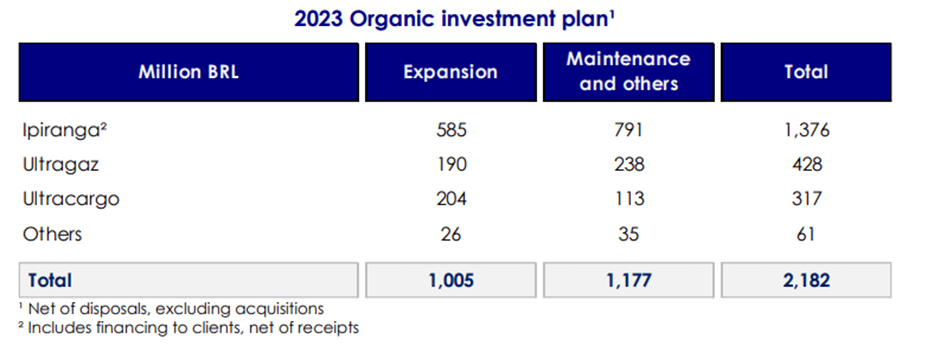

Ultrapar has outlined a bold new investment plan for FY23 amounting to ~R$2.2bn. Per management, the capex will be allocated across business portfolio expansion, with key initiatives including capacity expansions and efficiency gains, as well as points of sale optimization. Most of the capex dollars (~R$1.2bn) will go toward maintenance, though the remaining >R$1bn earmarked for expansion is significant as well. While management didn’t commit to a specific return target, prior guidance for a return rate of >15% for new projects likely remains intact.

Ultrapar

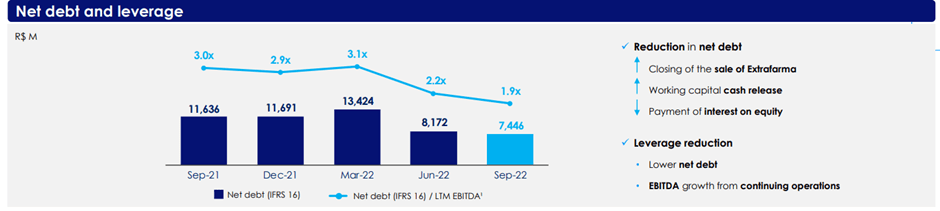

The higher growth capex guide should come as no surprise – recall that management had previously flagged its increased cash generation as supportive of a bigger allocation. While Ultrapar’s Q3 headline free cash generation was indeed impressive, it was propped up by a favorable >R$600m working capital inflow from the recent fuel price declines. So while fuel distributors freed up working capital in Q3, this should reverse over the coming quarters, weighing on FCF. Given that Ultrapar’s free cash generation would have been negative excluding the working capital contribution, I am concerned about future capex ramp-ups. For now, though, the expanded balance sheet capacity should fund any capex needs – in addition to the Q3 deleveraging, pending receivables related to the divestments of Oxiteno and Extrafarma should keep the net debt/EBITDA well below ~2x.

Ultrapar

Ipiranga As The Key Growth Driver

Given its relative contribution and recent outperformance, Ultrapar’s decision to allocate most of its capex to the fuel distribution arm Ipiranga makes sense. From an industry perspective, Ipiranga’s supply capacity has also proven valuable in a tight market, giving it an advantage in the domestic market. All in all, the company has guided to R$1.4bn of investments here in FY23, of which R$585m will be for expansion and R$791m for maintenance and other investments.

Of note, expansion capex will be mainly directed to the branding of service stations with higher throughput, as well as the expansion of capacity and logistics infrastructure across the existing base. The size of the additional capex allocation for service station branding at R$265m is a particularly positive readthrough for the sector, in my view, reinforcing the value proposition for more service station owners signing branding deals with distributors over time.

The mid to long-term growth potential needs to be balanced, however, against near-term margin pressure from lower domestic fuel prices and service disruptions (e.g., the trucker protests last month). Pending measures to address these headwinds, Ipiranga could still underwhelm in the coming quarters, in my view.

Ultragaz Gets A Hefty Capex Allocation Post NEOgás Acquisition

Meanwhile, the LNG distribution subsidiary Ultragaz will be allocated R$428m of investments for next year. Of this allocation, growth capex will amount to R$190m for customer acquisition in the bulk segment (e.g., by opening new points of sales), as well as optimizing infrastructure and exploring energy diversification projects. The segment has benefited from innovation and efficiency gains thus far, with the recent Q3 EBITDA outperformance mostly down to efficiency and productivity initiatives. Thus, deploying more capex to unlock more of these benefits makes sense, in my view.

Of note, the capex update comes on the heels of Ultrapar’s acquisition of a 100% stake in NEOgás via Ultragaz for an enterprise value of R$165m. For context, NEOgás is currently the leading Brazil-based compressed natural gas transport company covering industries and vehicles. Based on the disclosed terms, the deal appears to be a positive step – entering the compressed natural gas distribution segment not only adds scale and breadth to the Ultragaz energy solutions offering, but also opens up new long-term growth opportunities in biomethane distribution. The transaction is still pending antitrust approval, but given the limited size of the NEOgás acquisition, it should face few hurdles.

On Hold Despite The Ambitious New Capex Plan

Overall, the latest capex update highlights Ultrapar’s growth ambitions coming off an earnings beat led by strong margin results in Ipiranga and Ultragaz. The reduced net debt post-Q3 also means there is ample balance sheet capacity to balance a more aggressive capex plan with shareholder return. Beyond FY23, though, the weaker free cash generation could be an issue. The Q3 FCF outperformance was mostly down to working capital; excluding the positive one-off impact, FCF would have been significantly negative. At first glance, the valuation seems undemanding at ~5x fwd EV/EBITDA, but given the funding risks and possible post-election regulatory hurdles (mainly related to federal taxes on fuels and government price intervention), I view the risk/reward as balanced here.

Be the first to comment