everythingpossible/iStock via Getty Images

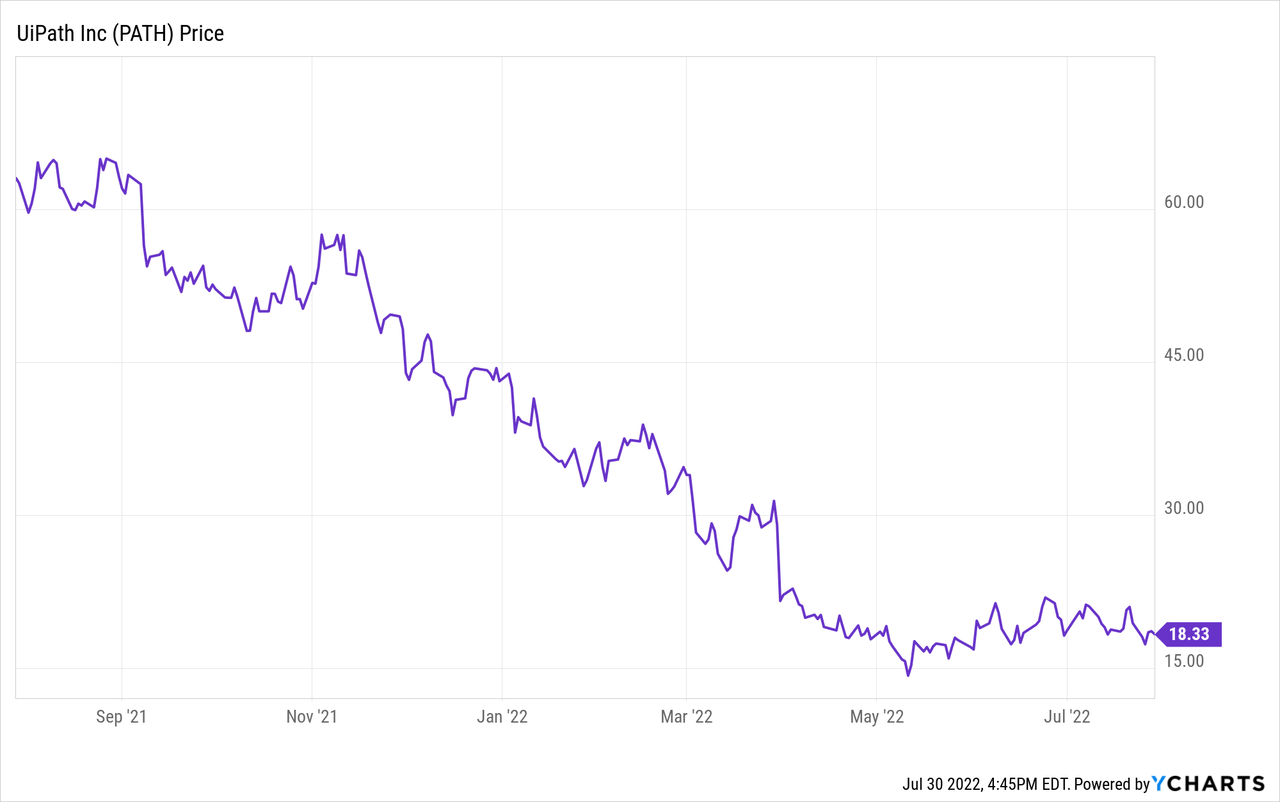

UiPath (NYSE:PATH) reported FQ1 earnings in early June and since then, the stock has gone up over 5%, though the stock remains down almost 60% since the beginning of the year.

Revenue continues to remain very healthy, growing over 30% yoy and consistently beating expectations. However, profitability remains challenging with the company reported a non-GAAP operating loss of $11 million during FQ1, including a free cash flow loss of $54 million.

During a time where investors are placing more emphasis on profitability, UiPath may continue to have a negative sentiment overhang on the stock.

With the company reporting earnings sometime in late August, I believe management may need to provide a more cautious tone related to guidance. The macro environment continues to remain challenging and with the US dollar strengthening, foreign currency could become a bigger headwind. UiPath has 50% of revenue from international currencies, so the stronger USD has a negative impact to their international revenue.

On top of that, investors continue to focus on profitable companies that may fare off better during a potential recession. While UiPath could continue to see strong demand, their profitably remains a bit concerning.

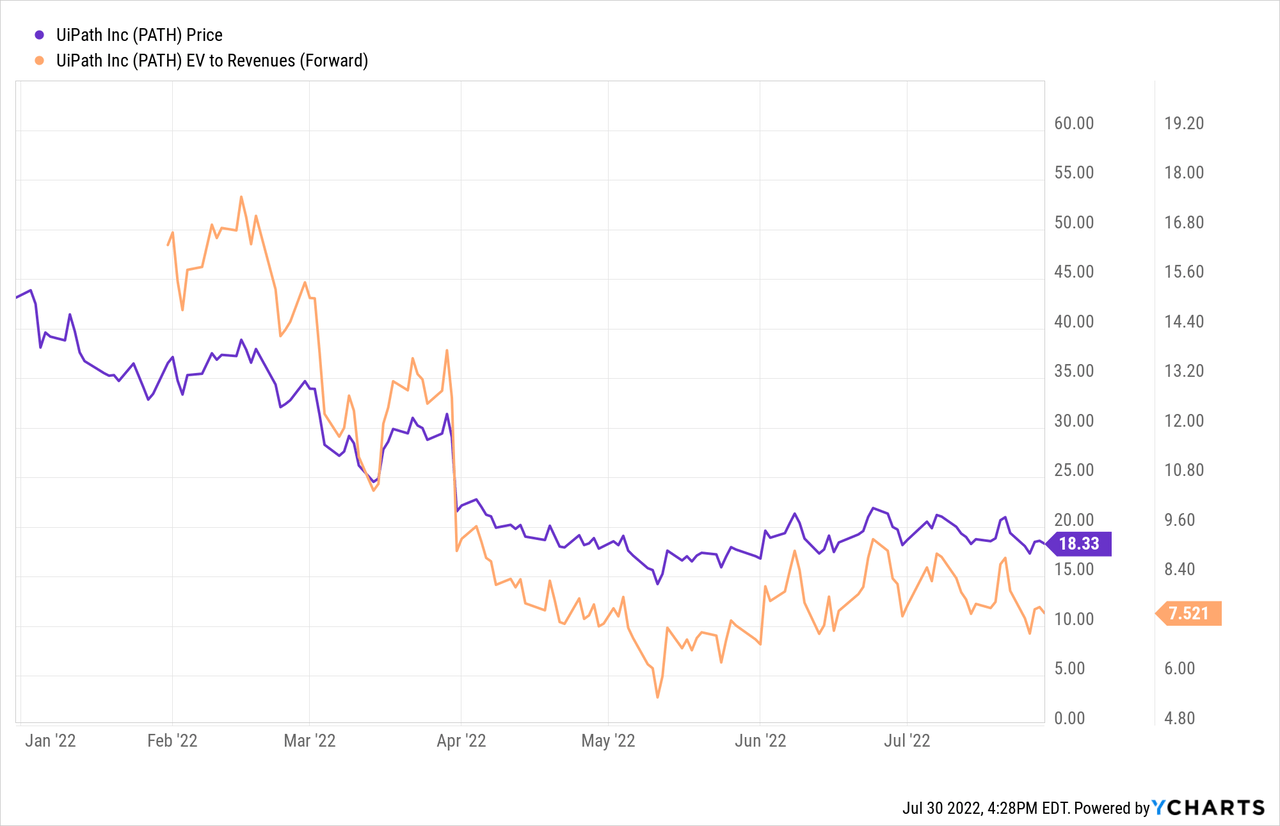

Valuation is also currently 7.5x FY23 revenue, which remains quite expensive given the current challenging macro environment. Even in a bullish scenario on FY24 revenue, valuation is still around 5.5x, which does not screen cheap.

For now, I am cautious around the company heading into FQ2 earnings with the potential for management to lower their guidance expectations. While I am a long-term believer in the company, there appears to be some risk heading into earnings.

Company Overview

UiPath provides an automation platform that uses computer vision and AI to build software robots. These robots will emulate human behavior and complete repetitive tasks, thus automating that process. Essentially, UiPath uses software to help companies automate simple tasks that employees would otherwise complete, thus making the company more efficient.

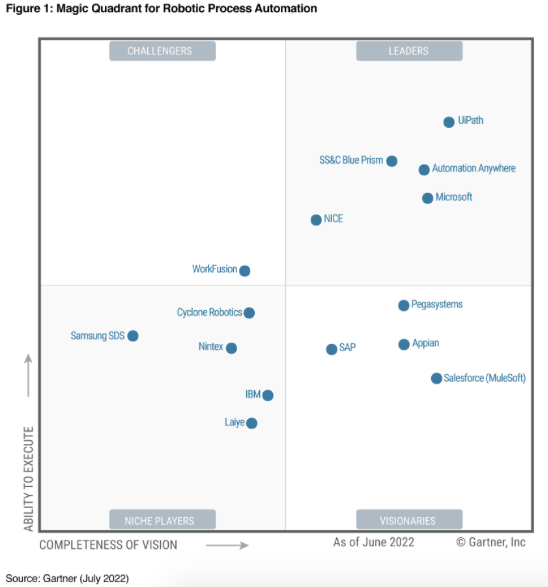

While Microsoft (MSFT) is UiPath’s biggest competitor, UiPath has consistently been named the robotics process automation leader by Gartner.

Gartner

Even though UiPath is smaller in size, they continue to compete well against Microsoft, Automation Anywhere, and SS&C Blue Prism. The market remains competitive as businesses look to automate certain processes and the global pandemic certainly accelerated the pace of digitization.

Financial Review

Though the company reported earnings in early June, we are still several weeks away from another update from the company.

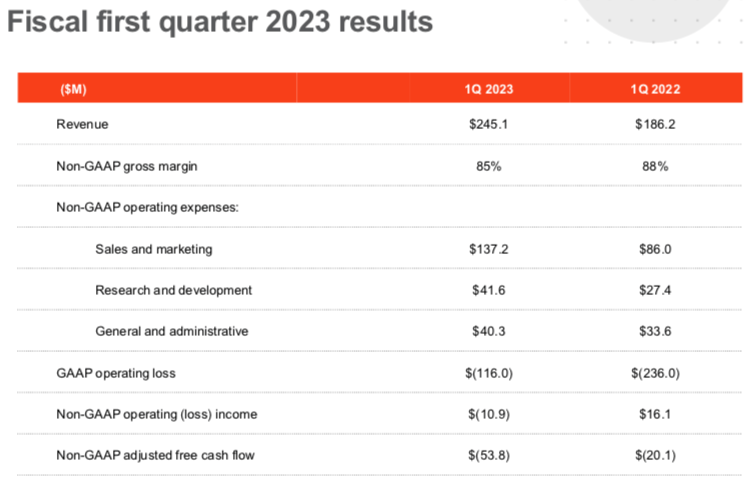

During their FQ1, the company grew revenue 32% yoy to $245 million, which beat expectations by $20 million, implying an 8% revenue beat. The company’s non-GAAP gross margin remained strong at 85%, though this was down a bit from 88% in the year-ago period. Higher wage and expense inflation certainly impacted the company’s gross margins, though investors will likely continue to see gross margins around that 85% level.

UiPath

In addition, non-GAAP operating loss during the quarter was $11 million, which was nearly $30 million lower than the $16 million profit seen in the year-ago period. The biggest driver was the $50 million increase in sales and marketing expense. Given the significantly growing market and the company’s consistent 30%+ revenue growth, it’s no surprise they are investing heavily into sales and marketing.

And these benefits are paying off. During the quarter, ARR reached $977 million, representing a 50% yoy increase and reflects net new ARR of $52 million. In addition, dollar based net retention rate was 138%, which clearly demonstrates UiPath’s customers desire to spend more with the company over time.

UiPath

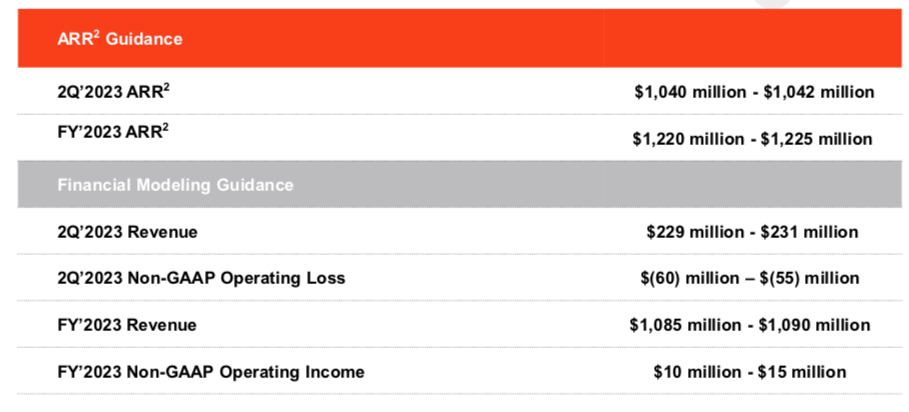

For the upcoming FQ2, the company expects revenue of $229-231 million and ARR of $1,040-1,042 million. However, the non-GAAP operating loss of $55-60 million was a dark spot on the upcoming quarter outlook.

For the full year, revenue is expected to be $1,085-1,090 million and ARR of $1,220-1,225 million. Non-GAAP operating income is expected to be $10-15 million, which would reflect a 1-2% margin.

Given the current challenging macro environment and currency headwinds become more challenging given the strong U.S. dollar, the company may be forced to lower their guidance. During the company’s FQ1 earnings call, management addressed some of these headwinds.

One of UiPath’s strengths is our global presence which gives us diverse perspectives and access to talent. We price in local currency and with more than 50% of our business conducted outside North America, our results are subject to foreign exchange volatility. We recognize that macroeconomic and geopolitical issues are impacting global markets and the strengthening of the U.S. dollar continues to create a currency headwind for our business. As we did in March, the guidance we are providing this afternoon contemplates the current operating environment and includes an FX headwind offset by growing momentum in the business.

These challenging macro factors have continued over the past few months and may continue for the remainder of the year. Thus, it would not be surprising to see the company lower their full year expectations given the bigger currency headwind and more challenging macro environment.

Valuation

The stock has pulled back almost 60% year to date as investors pivoted away from high-valuation, unprofitable companies. However, since the company reported earnings, the stock is up over 5%.

The biggest concern with UiPath remains around profitability. With non-GAAP adjusted free cash flow loss of $54 million, investors may continue to hold this against the company in the current environment. With fears around a potential recession and interest rates continuing to rise, investors have shifted their focus to more stable and profitable companies.

The company has a current market cap around $10 billion and with $1.8 billion of net cash, enterprise value currently stands around $8.2 billion.

UiPath’s full year revenue guidance of $1,085-1,090 million implies a FY23 revenue multiple of around 7.5x. While the stock previously traded at forward revenue multiples well over 10x, it does not seem likely that we return to an environment where investors are willing to pay up that much for growth stocks.

Yes, revenue growth could remain very strong over the coming years, but profitability becomes increasingly important as we potentially enter into a recession.

Even if we see FY24 revenue reach $1,500 million, which would be above consensus expectations for $1,390 million (per Yahoo Finance), the implied FY24 revenue multiple of 5.5x is still expense for a company with barely breakeven profitability.

For now, I remain cautious around this name heading into their FQ2 earnings report, as we could see management becoming more cautious around their outlook given the challenging macro landscape.

Be the first to comment