NicoElNino

UiPath (NYSE:PATH) is a leader in software automation tools and has created a platform to help organizations save employees time and improve the efficiency of their operations. The Robotic Process automation [RPA] industry was valued at $10 billion in 2022 and is forecast to grow at a rapid 23.4% compounded annual growth rate, reaching $43.52 billion by 2029. UiPath is poised to benefit from this growth trend as it serves an elite range of customers from General Electric (GE), to Autodesk (ADSK), Virgin Media to Google (GOOG) (GOOGL), and even NASA. In the third quarter of fiscal year 2023, the company reported strong financial results beating both top and bottom-line analyst estimates. In this post I’m going to break down its business model, financials, and valuation, let’s dive in.

Business Model

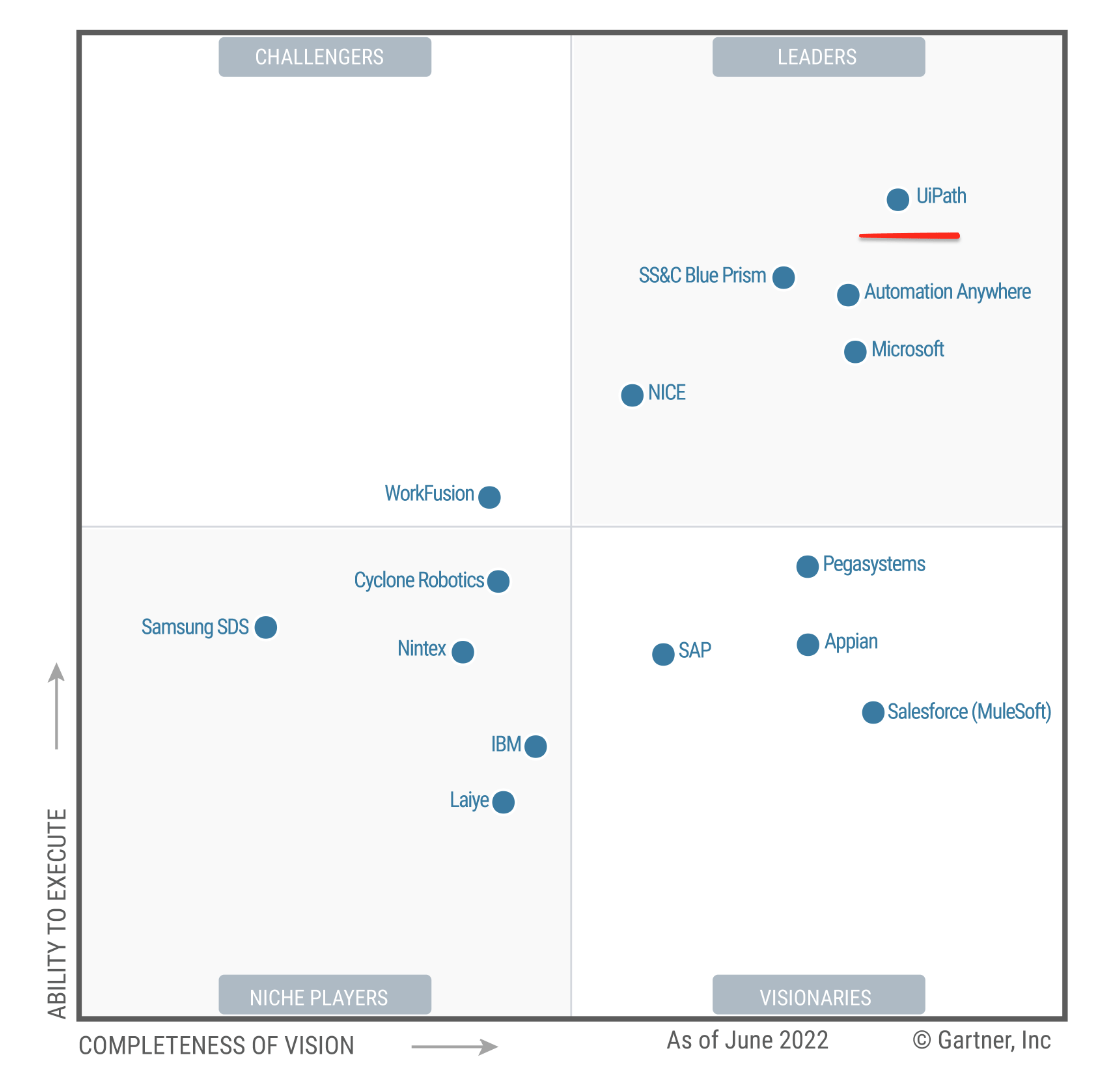

UiPath is a Gartner magic quadrant leader in “Robotic Process Automation”, or RPA. The company develops what it calls “software robots” to help organizations automate repetitive tasks, saving time and improving operational efficiency.

UiPath (Gartner)

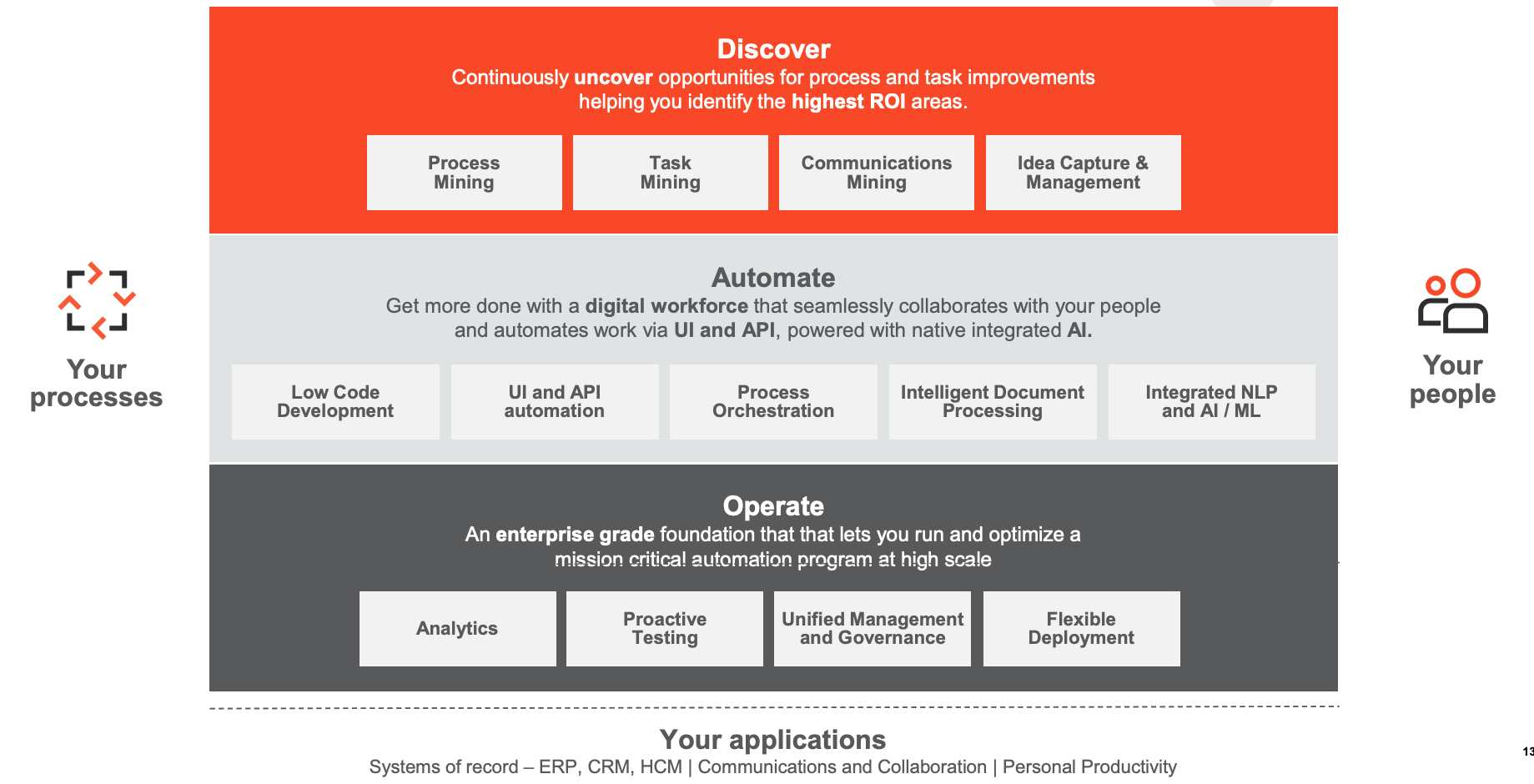

Adoption of the UiPath platform starts with the “Discover” stage in which business customers do “Process mining” and “Task mining” in order to identify areas of automation with the highest ROI. After which a simple business person, can use the “low code” platform to orchestrate automation of the process or task. The beauty of this system is it does not require a software engineer and therefore democratizes software automation for the masses. However, if software developers want to customize the platform in advanced ways they can do this also. Once a process is automated, analytics can be collected and the process further optimized.

Business Model (Investor Day Presentation)

A popular process to automate is repeated back-and-forth emails which require default answers 90% of the time. For example, I used to run a travel blogging website which was often emailed hundreds of times per month with requests from people to become a guest writer. If I created a unique email for each person this would be very time-consuming from an admin point of view. My solution to this was to create an email template, which eliminated the back and forth. However, a solution by UiPath could automate this process very easily. UiPath gives an example, of Uber (UBER) which uses UiPath to automate 70% its freight invoices, as well as other processes with estimated savings of over $22 million over three years, which is outstanding. The benefit of automation machines/software doesn’t make traditional “mistakes” like humans and are very good at delivering consistent service. Spotify also utilizes UiPath to automate over 100 processes and save over 45,500 hours. The company has gradually expanded the sales of its platform through a combination of self-service adoption for SMBs and Partner ecosystem growth for enterprises.

Strong Quarter Financials

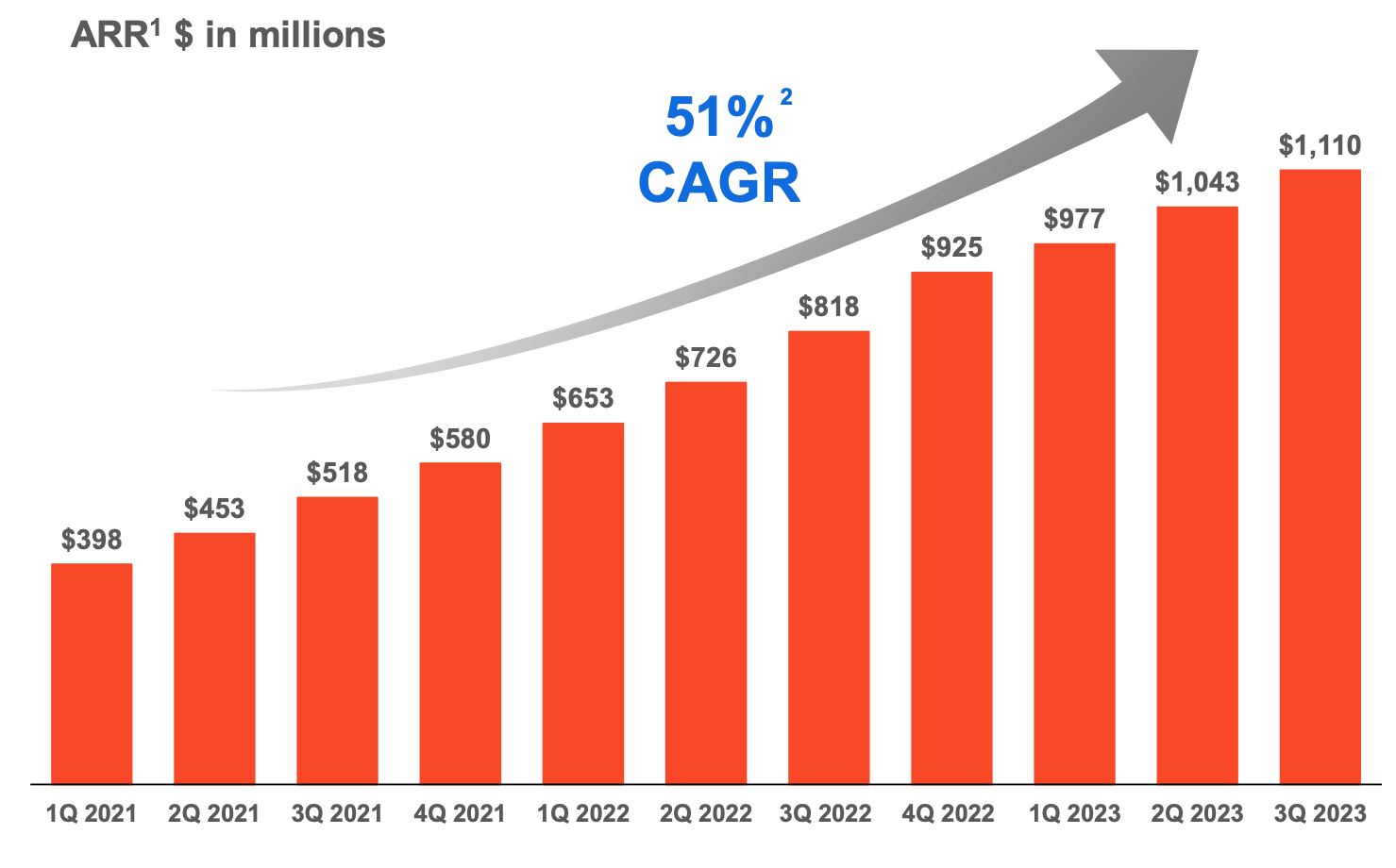

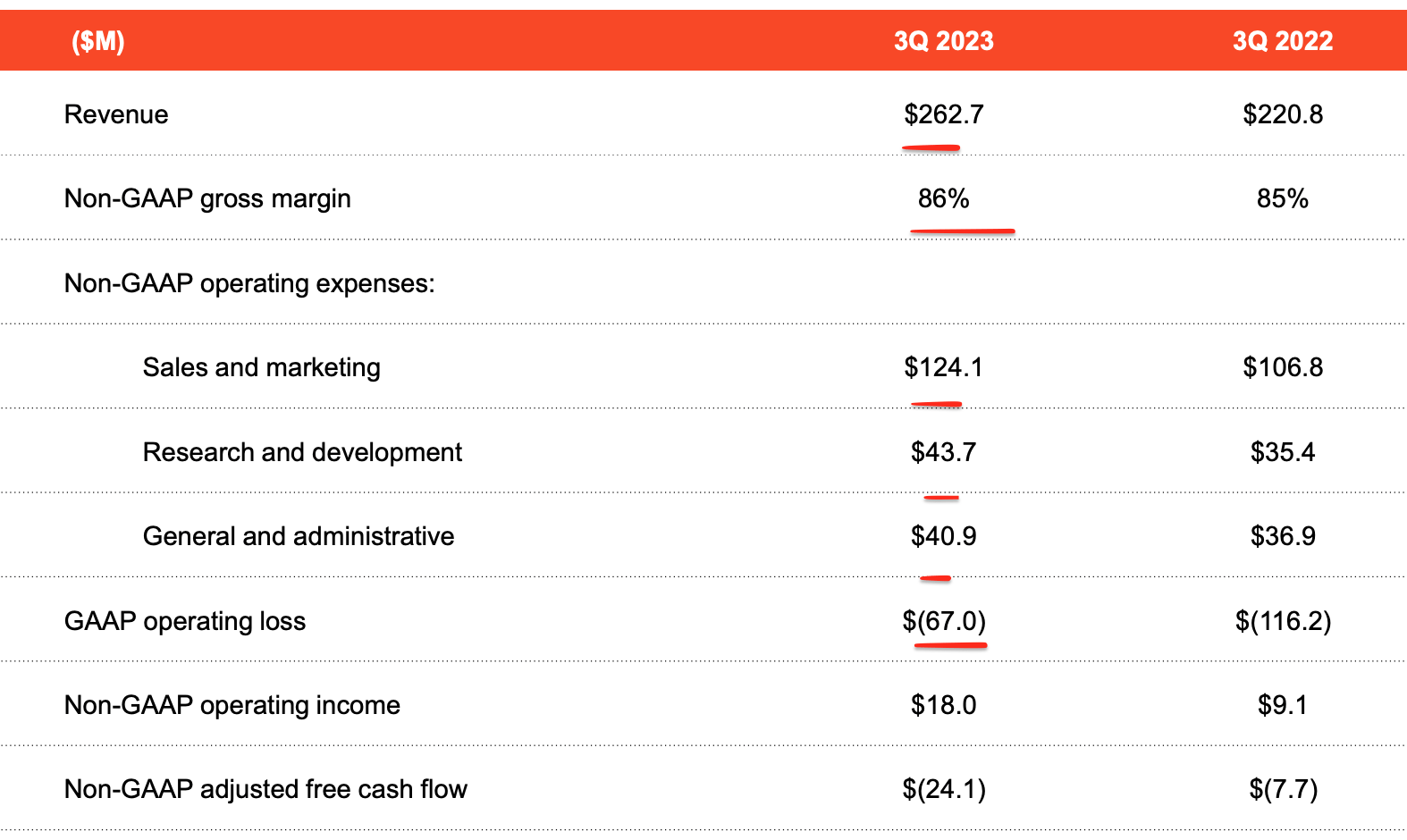

UiPath reported strong financial results for the third quarter of FY23. Revenue was $262.74 million, which beat analyst estimates by $6.81 million and increased by 18.99% year over year. This growth rate was slower than the 49.2% in the equivalent quarter last year. However, if we exclude a $22 million foreign exchange headwind, from a strong U.S dollar. FX neutral Revenue increased by 29% year over year, which was much better. Annual recurring revenue [ARR] also reported a similar trend. Net new ARR was $67 million in Q3,FY23 and excluding the $22 million headwind, it increased by 38% year over year. Total ARR rose by 36% to $1.1 billion.

ARR (Q3,22 report)

UiPath’s growth strategy is to utilize a classic SaaS “land and expand” strategy which starts with a business customer automating just a few specific use cases, before expanding to a greater number of services. This is a great strategy and is utilized by rapidly growing cybersecurity companies such as CrowdStrike (CRWD). As of the third quarter of FY23, UiPath has a dollar-based net retention rate of 126%, which means customers are sticking with the platform and spending more.

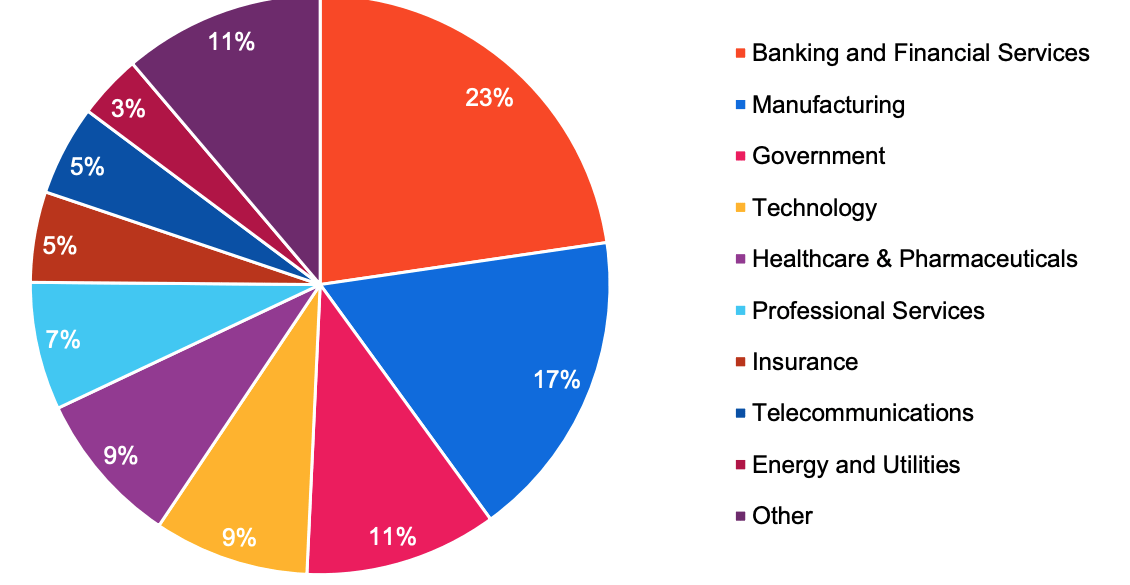

In the third quarter of FY23, the company increased its customer base to 10,650, which rose by 10.6% year over year. New customers included Pet food retail giant Petco, fitness company Nautilus, and Wisconsin energy. These customers offer a great sample of UiPath’s diverse customer base, which means it isn’t prone to cyclical downturns in any single industry. For example, on the chart below you can see the company makes approximately 23% of its ARR from the Banking and Financial Services industry, followed by Manufacturing at 17% and Government at 11%. Government agencies are a fantastic customer base as despite longer sales cycles initially, these customers tend to offer large account expansion opportunities. In the third quarter of 20FY23, UiPath expanded its accounts with both the U.S. Air Force and the U.S. Department of Homeland Security. Government customers also give credit to the platform’s cybersecurity credentials. In Q1, FY23 Uipath released a press statement, which said it was on the way to achieving FedRAMP certification.

Industry Diversification (Investor relations presentation)

UiPath works with customers across all sizes from SMBs to midmarket and enterprises. The company is executing its “growing upmarket” strategy to a tee. In the third quarter of FY23, it increased its “large customers” with over $100,000 in ARR by 26% year over year to 1,711. UiPath also grew its customers with over $1 million in ARR by 48.9% year over year. Selling into the enterprise is a challenge, but once a company has gained initial traction (like UiPath) it can be immensely lucrative. The reason for this is enterprise customers tend to have higher retention rates, and many more account expansion and upsell opportunities.

Larger customers (Q3,22 report)

Margins and Expenses

In Q3,FY23, UiPath reported a solid growth margin of 86% which increased by 1% year over year, thanks to cloud infrastructure efficiencies.

The company is still operating at a loss of $67 million, however this does include $81 million in stock-based compensation [SBC]. As someone who has worked for large tech companies in the past, I do believe stock-based compensation is necessary to attract the best talent, while also creating alignment in teams. However, companies should use this carefully to avoid diluting shareholders. Overtime, I would like to see stock-based compensation making up a smaller portion of revenue as the company scales. The positive is on a non-GAAP basis, the company reported positive operating income of $18 million. In addition, to non-GAAP earnings per share of $0.05, which beat analyst estimates by $0.06.

Sales and Marketing expenses increased by 16.2% year over year to $262.7 million or 47% of revenue. This was a slight improvement over the 48% of revenue figure in the comparable quarter last year. As the business scales, I would like to see its Sales and Marketing expenses as a portion of revenue decline further. General & Administrative expenses increased by 10.8% year over year to $40.9 million. G&A expenses did show an improvement in operating leverage as it was 15.6% of revenue in Q3,FY3, down from 16.7% of revenue in Q3,21 despite increasing on an absolute basis. This is a positive sign and means the company is generating operational efficiency. In addition, management has initiated a “hiring freeze’ and is restructuring the company. R&D expenses were $40.9 million in Q3,FY23, which increased by 10.8% year over year. I don’t believe increasing R&D investments are a bad sign, as many studies indicate companies that do this tend to generate greater shareholder returns long-term think Meta Platforms (META) and Google.

Earnings (Q3,22 report)

UiPath has a robust balance sheet, with $1.7 billion in cash, cash equivalents and marketable securities and virtually no debt. This is a positive given the rising interest rate environment, as it means the company isn’t vulnerable to rising debt servicing costs.

Moving forward management has shown confidence by raising its ARR guidance for Q4,FY23 to the range between $1.174 billion and $1.176 billion. This would represent an increase of 26.9% year over year. This is greater than the 18.99% year-over-year produced this quarter and a strong positive, especially given the macroeconomic conditions.

Advanced Valuation

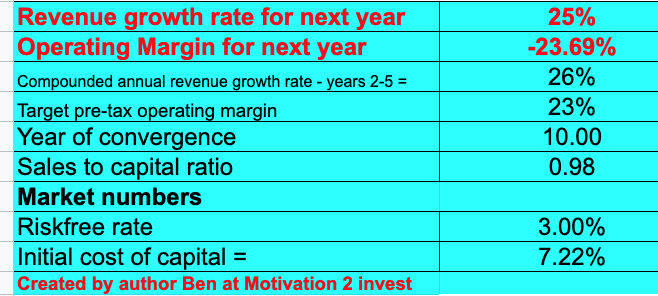

In order to value UiPath, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow method of valuation. I have forecasted 25% revenue growth for next year which is conservative given management guidance for Q4 would represent growth of 26.9%. I have been prudent here due to uncertain economic conditions. In addition, I have forecasted a faster 26% growth rate in years 2 to 5, as I forecast economic conditions to improve and sales cycles to shorten.

UiPath stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have also capitalized R&D expenses which has lifted net income. In addition, I forecast the company to improve its operating margin to 23% over the next 10 years, which is the average of the software industry. I forecast this improvement to be driven by increased operating leverage as the company continues to manage its expenses.

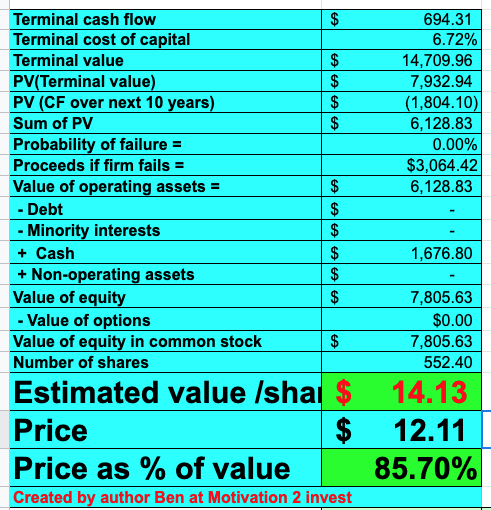

UiPath stock valuation 2 (created by author Ben at Motivation 2 Invest)

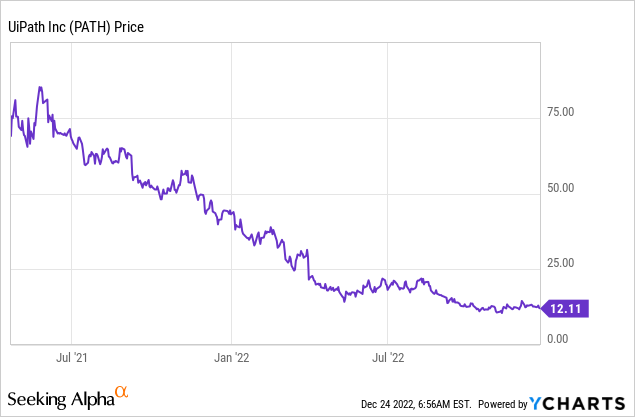

Given these factors I get a fair value of $14.13 per share, the stock is trading at $12.11 per share at the time of writing and thus is ~14% undervalued.

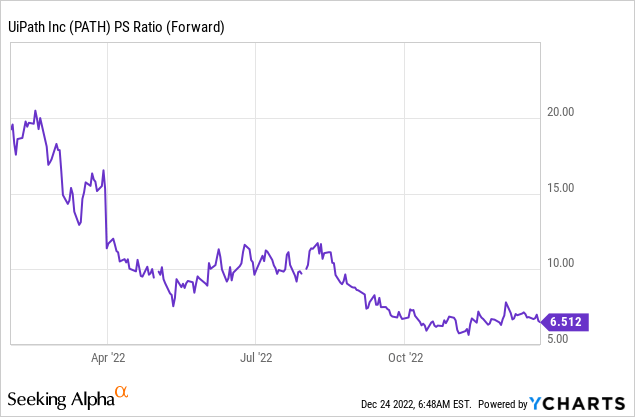

As an extra datapoint, UiPath trades at a Price to sales ratio = 6.34, which is cheaper than historical levels.

Risks

Competition

The automation of tasks has surged in popularity recently with the viral adoption of AI model ChatGPT by Open AI. This platform offers many automation solutions and could compete with UiPath. Then we have many traditional competitors such as Salesforce (CRM) with MuleSoft, Microsoft (MSFT) and IBM (IBM).

Recession/Longer Sales cycles

Many analysts are currently forecasting a recession in 2023. This will likely result in longer sales cycles, as companies delay spending. This could then result in slower growth for UiPath. A positive is the company is extremely good at selling “business outcomes” and recording ROI, therefore this could still entice enterprises to sign up.

Final Thoughts

UiPath is an established leader in Robotic Process Automation [RPA] and the company has marketed itself as a thought leader in the space. Its customers are enterprise giants and well-diversified across a range of industries. The company has continued to produce strong financial results despite tough economic conditions. Given the stock is undervalued intrinsically and relative to historical multiples, it could be a great long-term investment.

Be the first to comment