JuSun

Many quality companies have been thrown out with the bathwater during the equity market volatility over the past year. While there are plenty of high yielding names out there that warrants attention, I continue to believe in building a well-diversified dividend ladder to minimize risk in any one sector.

This brings me to UGI Corporation (NYSE:UGI), which remains attractive at $37, sitting well below its 52-week high of $47. In this article, I highlight why UGI may be a great choice for dividend investors seeking a stock with a strong track record of capital returns.

Why UGI?

UGI Corporation is a conglomerate with a diverse set of businesses, including propane distribution, electric and natural gas utility, and energy marketing. This includes a utility in Pennsylvania, LPG distribution both domestically (through AmeriGas) and abroad, energy midstream assets in Pennsylvania, Ohio, and West Virginia, and renewable natural gas marketing in 12 states.

This diverse business model is a key differentiator for UGI, as it enables management to invest in categories with the highest potential returns. One such initiative is the expansion of the company’s propane distribution business, which includes building new storage facilities and acquiring smaller propane distributors. Management reiterated its commitment to growing this business during its recent conference call:

As you are aware, we are the leading propane distributor in the U.S., but this is a highly fragmented market with close to 4,000 independent retailers who hold in aggregate more than 3/4 of the market, exclusive of regional and national retailers. We intend to gain a higher market share, increase volumes and grow EPS by roughly 8% by fiscal 2026.

Meanwhile, UGI isn’t showing any signs of slowing down, as revenue grew by 13% YoY to $2.9 billion in its fiscal fourth quarter. Management also invested a record amount of capital ($562 million) during that quarter, and added over 14,000 residential and commercial heating customers in its Utilities segment. Notably, UGI is benefiting from energy strains in Europe, as it saw higher LPG volume and margins in Northwest Europe, with average propane cost increasing by 53% over last year.

Looking forward, management is seeking to shed some lower-growth energy marketing businesses in Europe, notably in the UK, France, Belgium, Netherlands. This could help the company to refocus resources in higher growth areas, as mentioned by management in the last conference call:

We operate in a constructive regulatory environments in both Pennsylvania and West Virginia that support the modernization of infrastructure to promote safety, reliability and growth. With over 18,500 miles of pipeline and a long track record of attractive customer growth, we have a great runway of opportunities to deploy capital.

Our plans to invest approximately $2.4 billion over the next four years demonstrate our commitment to investing in the business and infrastructure replacement. Our team continues to deploy record amounts of capital, both safely and effectively. In addition, with these investments, there is minimal regulatory lag as we recover approximately 90% of the costs incurred in less than 12 months at attractive rates of return.

Management also has a keen eye on leverage with a target leverage in the 3x to 3.5x range, which is reasonable for a utility company. UGI currently has a net debt to TTM EBITDA ratio of 3.2x, which fits squarely within that range.

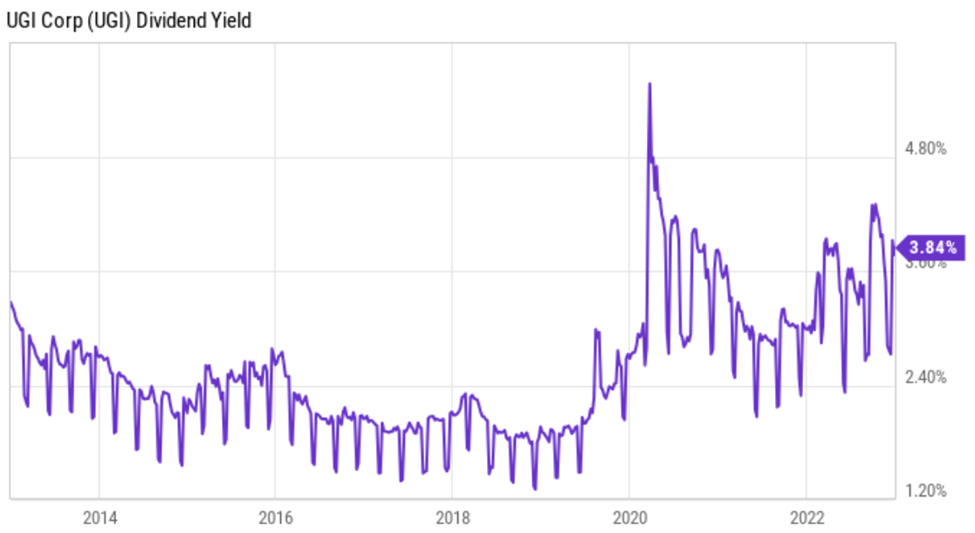

Importantly, UGI pays a safe 3.9% dividend yield that’s well covered by a 49% payout ratio. The dividend also has a 7.6% 5-year CAGR and UGI is a dividend aristocrat, with 35 years of consecutive annual raises under its belt. As shown below, the dividend yield currently sits at one of its highest points over the past decade.

(Note: the following chart shows TTM Yield, while the Forward Yield is 3.9%)

UGI Dividend Yield (YCharts)

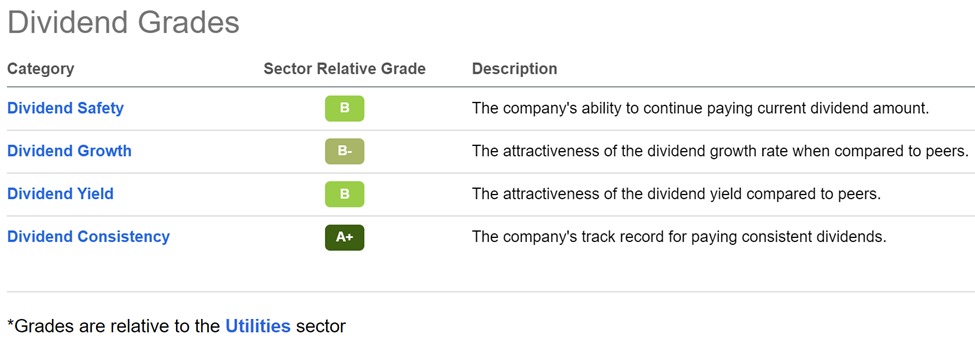

UGI also scores A and B scores for dividend safety, ,growth, yield, and consistency, as shown below.

UGI Dividend Grades (Seeking Alpha)

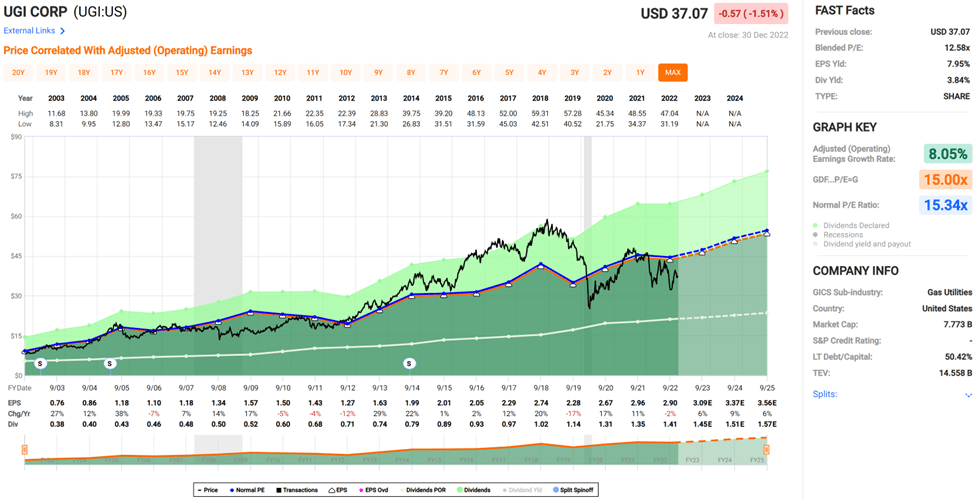

Lastly, UGI continues to trade in value territory at the current price of $37 with a forward PE of 12.4, sitting well below its normal PE of 15.3. This appears to be too cheap for UGI, considering the quality of the diversified enterprise and with analysts expecting 6% to 12% annual EPS growth over the next 2 years. Analysts have an average price target of $44.50, translating to a potential 24% total return from the present level.

UGI Valuation (FAST Graphs)

Investor Takeaway

UGI is a dividend aristocrat that has consistently increased its payout over three decades. The company has a well-diversified business model with attractive growth prospects. It also has a reasonable debt level that allows management to deploy capital towards high return projects. Finally, the stock is currently trading at a significant discount to its historical valuation and provides an attractive total return potential for dividend growth investors.

Be the first to comment