franckreporter

Lumber giant, UFP Industries, Inc. (NASDAQ:UFPI) has handily beaten the S&P 500 over the last five years, with the share price rising more than 145% in the last five years, compared to 47% for the S&P 500. The firm’s balanced business model, and competitive advantages, have helped the company through 67 straight years of profitability. The company has a coherent and successful capital allocation framework, a conservative capital structure, and a compensation program that ties shareholder interests with management. The firm is attractively valued and should be considered as a long-term investment.

Strong Stock Market Performance

In the last five years, UFP Industries has easily outperformed the S&P 500, with its share price rising by nearly 145.5%, compared to 47% for the S&P 500.

Source: Google Finance

The company’s strong performance seems driven by the supply chain disruption that has affected the global lumber market, as well as the company’s own excellent financial and operational performance.

Excellent Financial Results

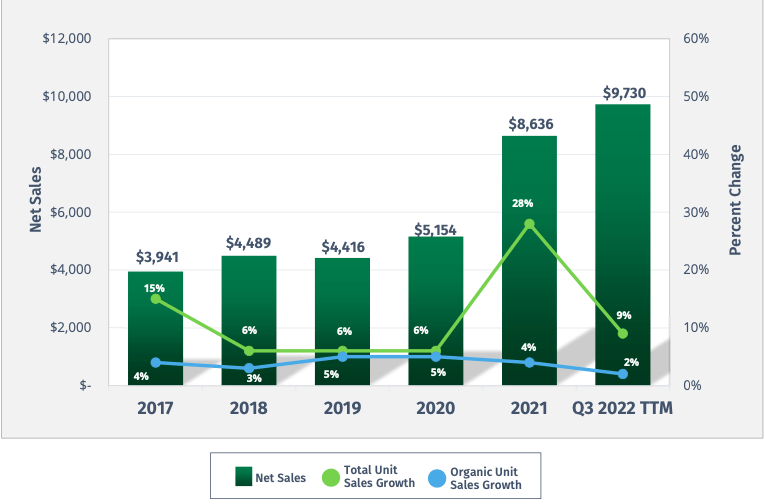

Revenues grew from $3.94 billion in 2017, to $8.64 billion in 2021, for a 5-year revenue compound annual growth rate (CAGR) of 16.99%. According to Credit Suisse’s (CS) The Base Rate Book, just 6% of firms between 1950 and 2015, enjoyed a similar rate of growth. This demonstrates the quality of the firm’s growth. In the first nine months of 2022, UFP Industries grew revenue to $9.73 billion, so we can expect full year 2022 results to be the best of the company’s history. The firm target’s unit sales growth of 5-7%, including small acquisitions.

Source: September 24, 2022 Investor Relations Presentation

Gross profitability rose from 0.37 in 2017 to 0.43 in 2021. According to Robert Novy-Marx’ research, 0.33 and above is the level of gross profitability that marks a firm out as being attractive. The firm’s gross profitability is well above the 0.33 threshold.

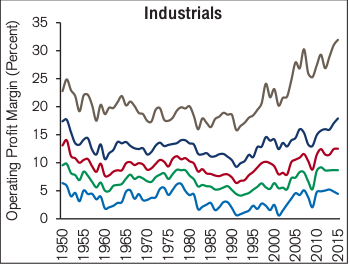

UFP Industries’ operating margin has grown from 4.6% in 2017, to 8.54% in 2021. While operating margin is not top tier, it is getting closer to double-digit, top tier levels. The operating margin for the highest quintile of firms grew from 21% in 1985 to 31% in 2015. That is clearly much higher than UFP Industries’ operating margin. In terms of the narrower, industrials segment, in the 1950-2015 period, the mean operating margin was 8.1%, and the median was 8.5%. This places the firm well above the industrial average. However, its operating margin is not among the top quintile in the segment.

Source: Credit Suisse

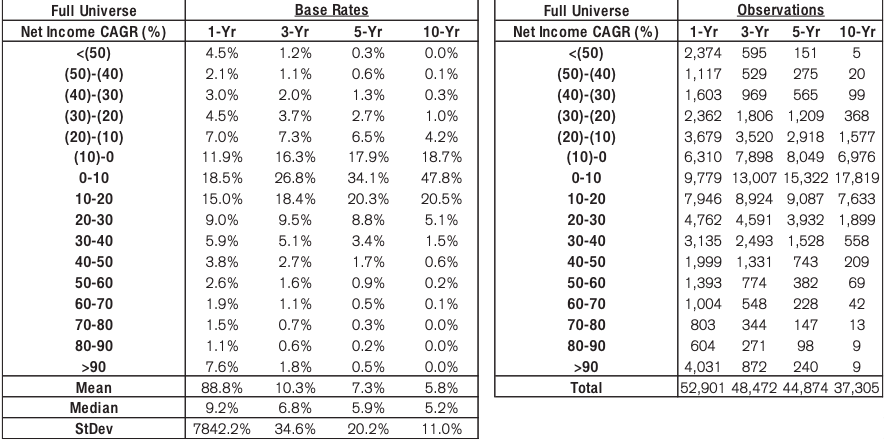

Net income rose from $119.51 million in 2017 to $535.64 million in 2021, for a 5-year earnings CAGR of 34.99%. Just 3.4% of firms enjoyed a similar rate of earnings growth in the 1950 to 2015 period, highlighting the uniqueness of the firm’s growth. In the first nine months of 2022, the firm earned a net income of $698 million, putting the firm in line to earn its highest ever net income. The company is no stranger to profitability, having enjoyed 67 straight years of profitability.

Source: Credit Suisse

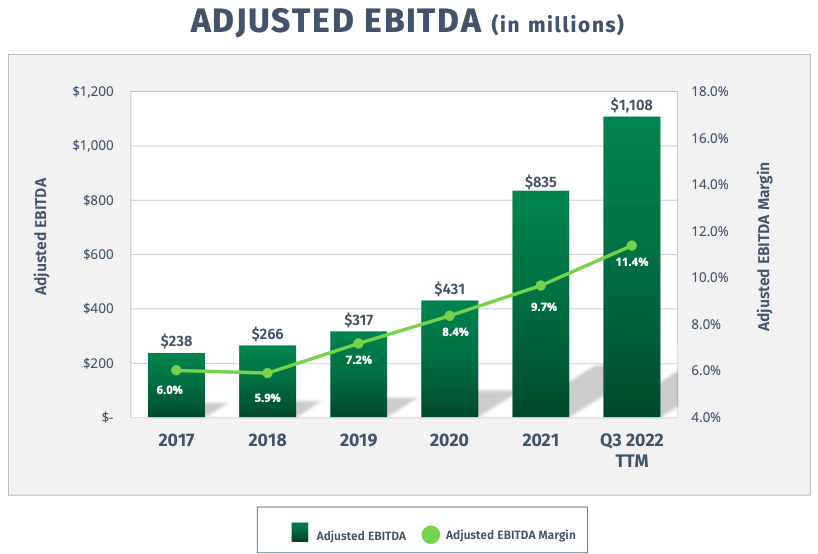

Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) rose from $238 million in 2017 to $835 million in 2021, for a 5-year EBITDA CAGR of 28.54%. In the first nine months of the year, EBITDA rose to $1.1 billion, promising record breaking EBITDA for the full 2022 year. Adjusted EBITDA margin rose from 6% to 11.4%, from 2017 and the first nine months of 2022. The firm has a target adjusted EBITDA margin of 10%, which it is likely to achieve in the 2022 full year results.

Source: September 24, 2022 Investor Relations Presentation

Free cash flow (FCF) rose from $68.39 million in 2017 to $391.28 million, for a 5-year FCF CAGR of 41.74%. In the trailing twelve months (TTM), the firm has earned $614.64 million in FCF.

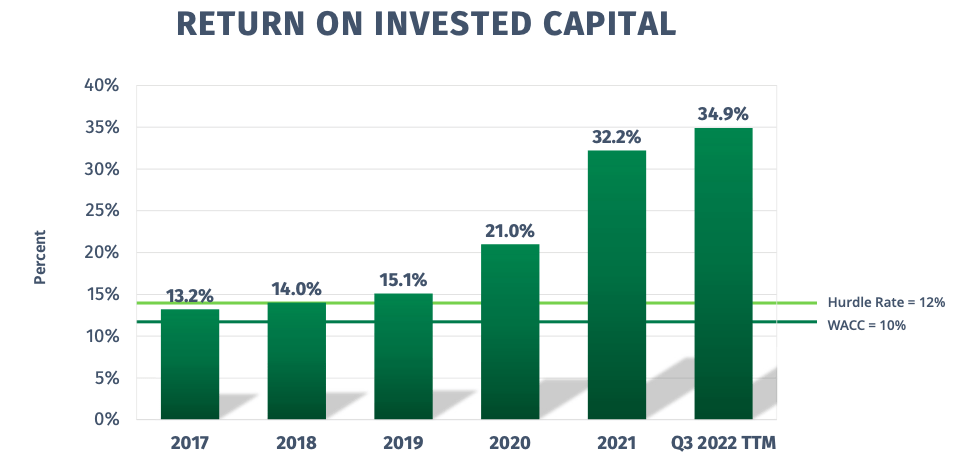

The firm’s competitive advantages have allowed it to earn very attractive returns on invested capital (ROIC), which have risen from 13.2% in 2017 to 32.2% in 2021. In the first nine months of 2022, ROIC further rose to 34.9%. The firm aims to earn a ROIC greater than 12% and assumes a base weighted average cost of capital of 10%.

Source: September 24, 2022 Investor Relations Presentation

Balanced Business Model

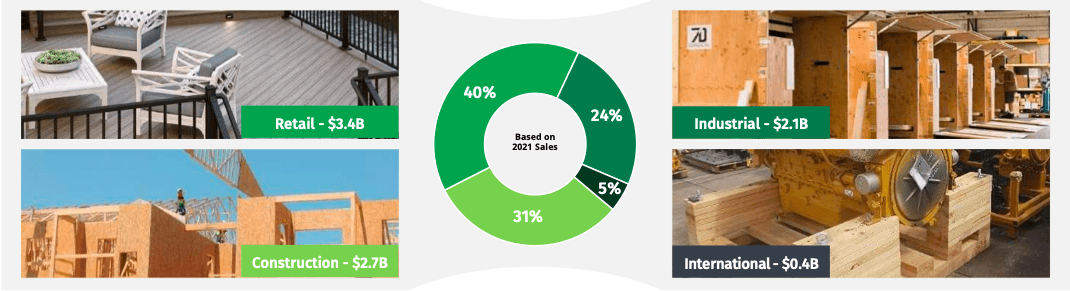

UFP Industries is a holding company whose operating subsidiaries, UFP Industrial, UFP Construction, UFP Retail Solutions, supply products made from wood, woon and non-wood composites, and other materials. These subsidiaries align with the end markets -retail, industrial and construction- that the company serves. The exception to this model is the UFP International segment, which serves Mexico, Canada, Europe, Asia, and Australia. The retail market is responsible for around 40% of revenues, followed by construction at 31%, industrial at 24%, and international at 5%.

Source: September 24, 2022 Investor Relations Presentation

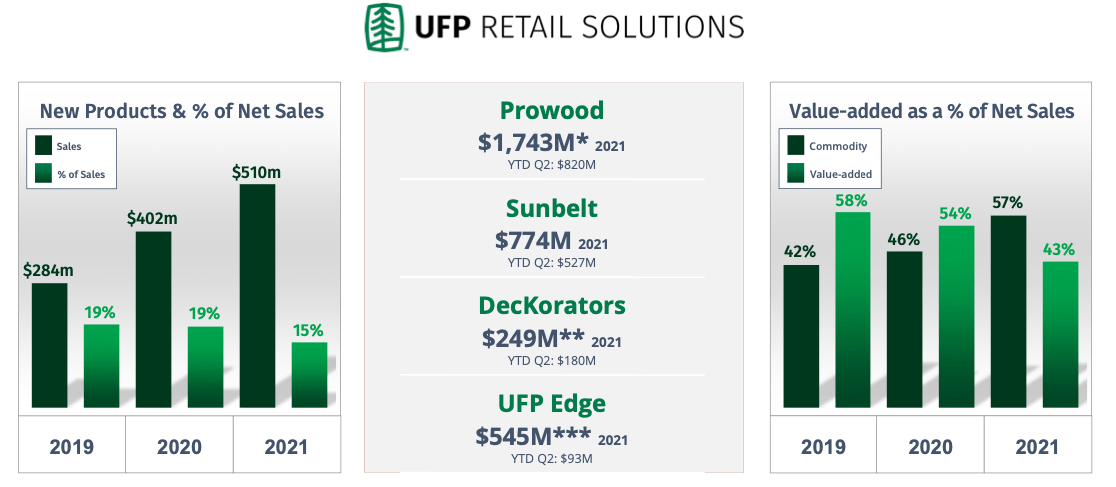

UFP Retail Solutions

According to the company’s 2021 Form 10-K, UFP Retail Solutions customers are “national home center retailers, retail-oriented regional lumberyards and contractor-oriented lumberyards”. Terms of sale are typically defined for annual or bi-annual periods. Customers place orders according to these terms of sale. The segment’s biggest customers are The Home Depot (HD) and Lowe’s (LOW), who, in 2021, were responsible for around 16% and 10%, respectively, of the firm’s revenues in 2021. In the 2019-2021 period, The Home Depot was responsible for an average of 19.67% of revenues, while Lowe’s was responsible for an average of 6% of the firm’s revenues.

Customers are supplied from one of the firm’s regional facilities. These facilities are able to supply mixed truckloads of products with quick turnaround times after receiving an order. The company works to ensure that it has a dense node of facilities and reduce the distance between the regional facilities and customers, in order to have high turnaround rates.

The segment supplies dimensional lumber, and other value-added products, as well as outdoor living products. The 2021 Form 10-K states that the segment produces around “27% of all treated wood, 8-10% of all composite decking and accessories, 8% of all wood and vinyl fencing and 1% of all lawn and garden products in the United States of America”. The segment is the only one in the United States that produces both value-added and commodity-based products at the national level.

The segment’s mix of product breadth, national scale, node density and reach, and expertise, provides the company with significant competitive advantages over its peers.

Source: June 30, 2022 Investor Relations Presentation

UFP Industrial

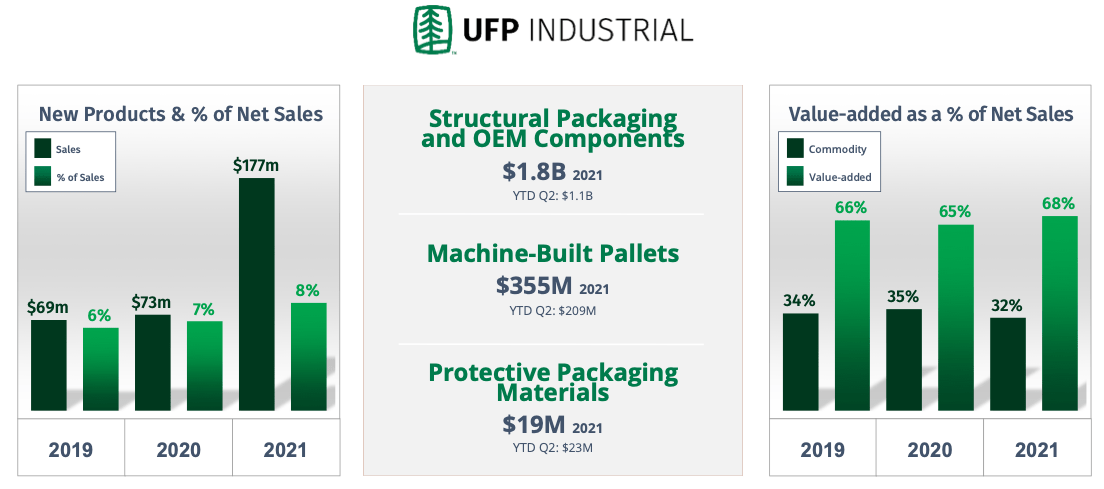

The segment serves manufacturing firms and agricultural producers with pallets, specialty crates, wooden boxes, and other containers that are used in packaging, shipping and material handling. The segment also supplies protective packaging, and other products. These products are typically made from the wood by-products of other products, which increases the yield from its raw materials.

The market is highly fragmented. This, notionally, makes it very difficult for any one firm to enjoy pricing power. The firm enjoys some economies of scale, with a national presence, and dense node network, that allows it to supply around 8% of all domestic wood packaging, including a market share of 7% of machine-built wood pallets and 13% market share of custom wood packaging.

Source: June 30, 2022 Investor Relations Presentation

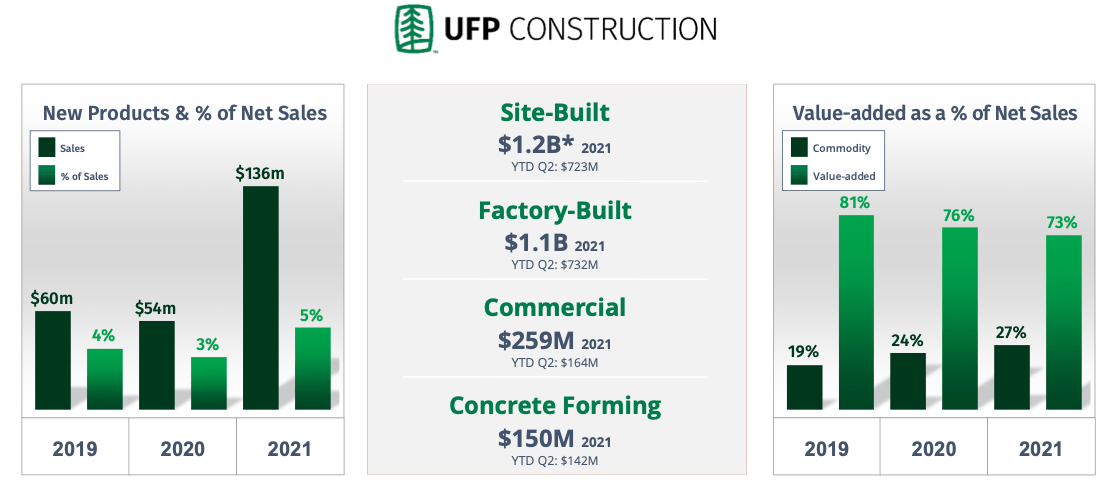

UFP Construction

The construction segment serves customers in four key markets: factory-built housing, site-built residential construction, commercial construction, and concrete forming. The factory-built housing market produces mobile, modular and prefabricated homes and recreational vehicles (RV). This market is served with roof trusses, cut lumber, plywood, oriented strand board and dimensional lumber. Again the firm’s most meaningful competitive advantage seems to be its economies of scale, given its national presence and dense node network. The firm supplies around 45% of roof trusses used in the U.S. factory-built housing market. The segment also produces such products as siding, electrical and plumbing products.

In the site-built residential construction market, the customers are mostly large-volume, multi-tract builders and smaller volume custom builders. The segment also serves builders involved in multi-family and light commercial construction. Once again the segment is highly fragmented, making it difficult to enjoy competitive advantages. Nevertheless, the firm can tap into its economies of scale and dense node network, to achieve competitive advantages. The segment produces around 5% of all engineered wood components used in U.S. housing. The terms of sale and pricing are negotiated in contracts with customers. The regional facilities used in this segment supply engineered wood components for frame residential or light commercial projects. The segment also supplies framing services for builders in various regional markets.

Source: June 30, 2022 Investor Relations Presentation

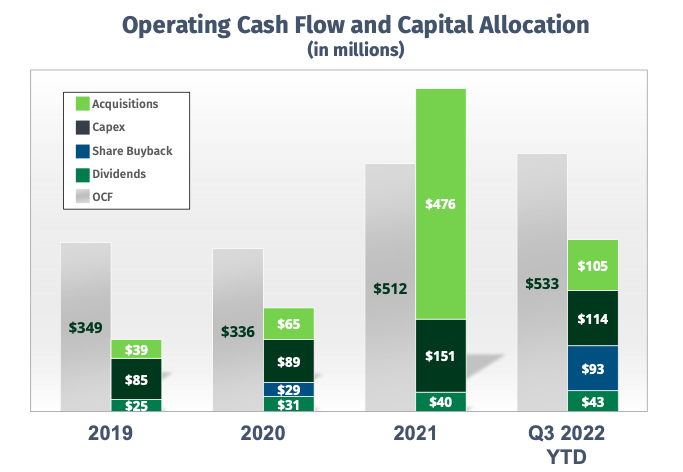

Capital Allocation Is Focused On Returns

The firm has a clear, robust and coherent capital allocation framework. The firm sets a hurdle rate of 12% for returns on new investment, and works with an average WACC of 10%. So the base scenario for decisions is that new investments must earn an economic margin of at least 2%. The firm’s ROIC shows that it has easily exceeded this demand. In terms of acquisitions, the firm looks to invest in growth markets, where it feels it is missing some capability. Acquisitions are driven by the need to shift from a commodity sales model to a value-added model, with the ultimate goal of scaling the business and creating synergies.

Source: June 30, 2022 Investor Relations Presentation

The company’s cash flow is deployed in a balanced way, with a return-focused perspective, toward acquisitions, capital expenditure, share buybacks, dividends, and operating cash flow. UFP Industries’ ROIC shows that this deployment has been very successful in creating shareholder value.

Source: September 24, 2022 Investor Relations Presentation

Incentives Aligned With Shareholder Interests

All plants are profit centers and bonuses are calculated based on returns on investment (ROI). In addition, the firm fosters an owner-operator mentality in management by requiring managers to own stock in the company. In this way, workers and managers have to eat their own cooking and take the same perspective as ordinary shareholders. With managers who have been with the business for an average of 23 years, there is a deep commitment to the business and fortunes are significantly tied to the business’ success.

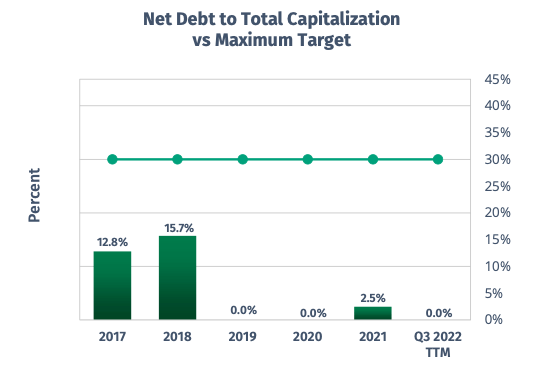

Conservative Capital Structure

There is an inverse relationship between asset growth and future returns. This is because managers typically overestimate their growth opportunities, raise too much capital and overinvest. Conservatism may not be exciting, but it is a protection against future mistakes, and against adverse economic changes. UFP Industries maintains a very conservative capital structure, which helps to protect the firm and de-risk it. The firm’s net debt to total capitalization is very low in comparison to the firm’s own maximum target, which puts a break on the firm potentially raising too much capital while chasing some growth opportunity.

Source: September 24, 2022 Investor Relations Presentation

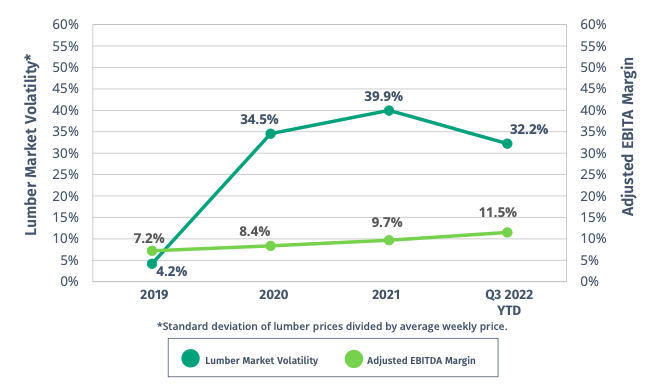

Profitability Is Not Dependent On A Lumber Market Boom

Typically, business in commodity industries tend to have boom-and-bust returns, but, as UFP Industries’ results show, the business has been able to be profitable across economic cycles. So, we can see that the level of lumber prices does not drive profitability. This suggests that the firm has true competitive advantages in a market in which we would assume that was not possible. As we saw in the discussion of the firm’s business model, it employs a blend of fixed and variable price products, which helps to reduce the risks in the business. So, while sequential trends impact profitability, the business model is very robust.

Source: September 24, 2022 Investor Relations Presentation

Valuation

UFP Industries has a price-earnings (PE) multiple of 8.06, compared to the S&P 500’s PE multiple of 21.75, showing significant relative undervaluation. In addition, with $614.64 million in FCF in the TTM period, and an enterprise value of $5.46 billion, the company has an FCF yield of 11.25%. In comparison, the 2,000 largest firms in the United States have an average FCF yield of 2.1%, according to New Constructs’ calculation. UFP Industries’ FCF has a yield 536% greater than the market, suggesting greater future market performance, and a superior model.

Conclusion

UFP Industries has easily outperformed the market over the last five years. This success is built on a balanced business model that enjoys significant economies of scale and dense, far-flung node networks, that allow the business to serve customers across the country, with very high turnaround rates, and at very competitive pricing. The firm has a capital allocation process that is focused on returns, and that has clearly earned returns greater than the hurdle rate. Managers and shareholders have interests that are aligned, with bonuses tied to ROI, and managers obliged to own stock in the company. As owner-operators, managers have developed a conservative capital structure and ensured that the firm has enjoyed 67 straight years of profitability, regardless of the business cycle. With an attractive PE multiple and a very attractive FCF yield, the firm should be considered by investors.

Be the first to comment