Mongkol Onnuan

UDR, Inc. (NYSE:UDR) is a multifamily-focused real estate investment trust (“REIT”) with a diversified presence across the U.S. Among three primary regions, the West Coast and the Northeast/Mid-Atlantic markets make up about 80% of their total operations. Supplementing this is their Sunbelt exposure, which accounts for a quarter of their operating income.

Compared to peers, UDR has less concentration risk and has a more stable base of tenants, which in turn enables high occupancy levels in excess of 95%.

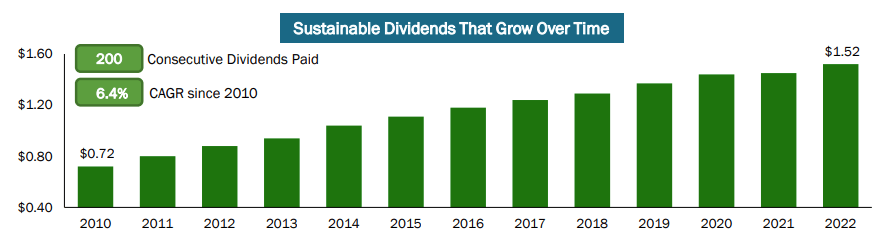

The company is also a top dividend payer, with a notably strong track record of continuous payments and steady increases. Most recently, management announced a 10.5% increase to the current payout.

November 2022 Investor Presentation – Dividend Payout Growth Since 2010

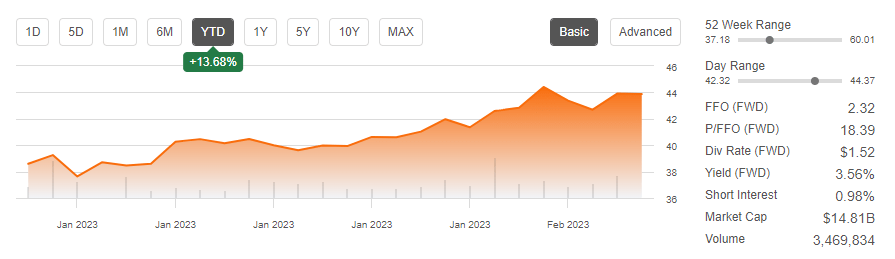

For investors, the reoccurring payments provide a fresh sense of security and stability in an otherwise volatile market environment. In addition, the stock has outperformed at the start of 2023, up over 13% YTD.

Seeking Alpha – YTD Share Price Performance Of UDR

While the gains have provided the stock some breathing room from their 52-week lows, further upside will likely be harder to come by. Following a stellar year in 2022 marked with double-digit revenue and earnings growth, growth in 2023 is expected to be much more moderated. And at present, shares don’t trade at a significant discount to related peers. While the regular dividend payout is certainly a standout feature of the stock, it doesn’t yield enough to cause much excitement. For investors, this warrants a neutral position on the stock.

Q4FY22 Earnings Recap

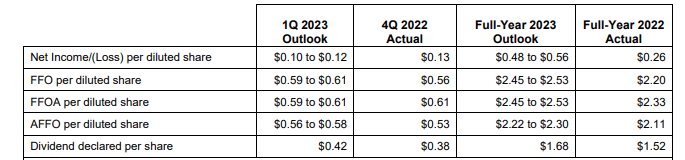

In 2022, UDR posted 16% growth in adjusted funds from operations (“FFO”) and turned in earnings that were in line with previously provided guidance. In Q4, specifically, adjusted FFO was up 13% from last year and within their targeted range.

The quarterly results came with total revenues that were up 14.8% YOY, driven by both their same-store portfolio and the accretive contributions from prior external investments.

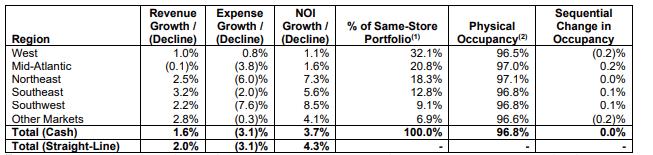

Within that same-store portfolio, overall cash-basis YOY net operating income (“NOI”) was up 11.5% on double-digit revenue growth. It was also up on a sequential basis by 3.7%, due primarily to a 3.1% reduction in operating expenses.

In individual regions, YOY quarterly same-store strength was pronounced in all regions, with the exception of their Western and Mid-Atlantic regions, which posted upper-single-digit NOI growth compared to the upper-teens reported in their other regions.

And in the Western region, which accounts for over 30% of their same-store portfolio, YOY quarterly occupancy declined by 20 basis points (“bps”). Still, overall occupancy remained high at 96.5%, not far off the quarterly same-store average of 96.8%.

Sequentially, the same-store portfolio benefitted from a significant decline in operating expenses, resulting in an overall cash-basis NOI growth of 3.7%.

Q4FY22 Investor Supplement – Summary Of Quarter-Over-Quarter Operating Metrics By Region

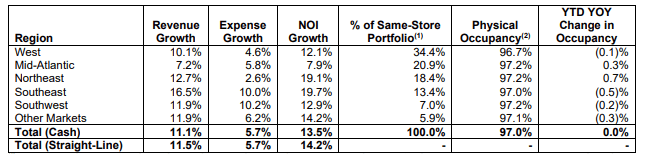

For the full year, it was even better, with 13.5% cash-basis NOI growth and virtually no change in YOY occupancy levels.

Q4FY22 Investor Supplement – Summary Of Full Year Operating Metrics By Region

While current year results reflected double-digit revenue growth on largely controlled expenses, management is expecting a comedown in 2023, with same-store cash revenues and NOI expected to grow just 7.5% and 8.5%, respectively. And this would be paired with comparable expense growth in relation to the current year. Altogether, earnings are expected to be up to comparable on a sequential basis and about 5% higher on a full year basis at the top end of the targeted range.

Q4FY22 Investor Supplement – Summary Of 2023 Guidance

Liquidity And Debt Profile

UDR is currently maintaining their investment-grade credit rating from both Moody’s and S&P Global, with a stable outlook.

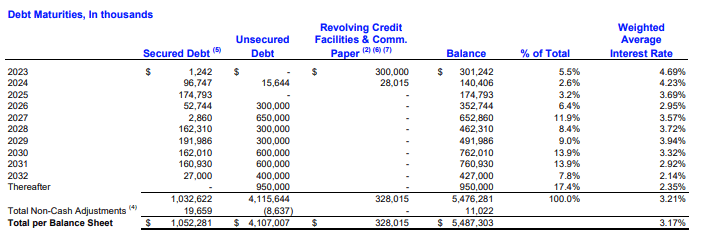

The favorable rating is accompanied by a sector-low weighted average interest rate on their outstanding debt obligations of 3.1%. This is on total leverage that is on the lower end of the spectrum. At year-end, their leverage as a percentage of their total enterprise value stood at about 30%, well below the 60% maximum permitted under their existing debt covenants.

In addition, as a multiple of EBITDAre, net debt stood at 5.6x on an adjusted basis at year-end. This was within their targeted range. Furthermore, of the total outstanding, just 20% matures over the next five years, with the average duration being just 6.7 years.

Q4FY22 Investor Supplement – Debt Maturity Schedule

While the revolver is coming due in 2023, there are limited concerns regarding UDR’s ability to satisfy both their upcoming and ongoing obligations. For one, just 2% of their total debt is scheduled to mature through 2024. And second, total liquidity currently stands at +$1.0B, comprised of cash on hand and availability on their revolving credit facilities. Strong reoccurring operating cash flows further complement their existing liquidity position.

Dividend Safety

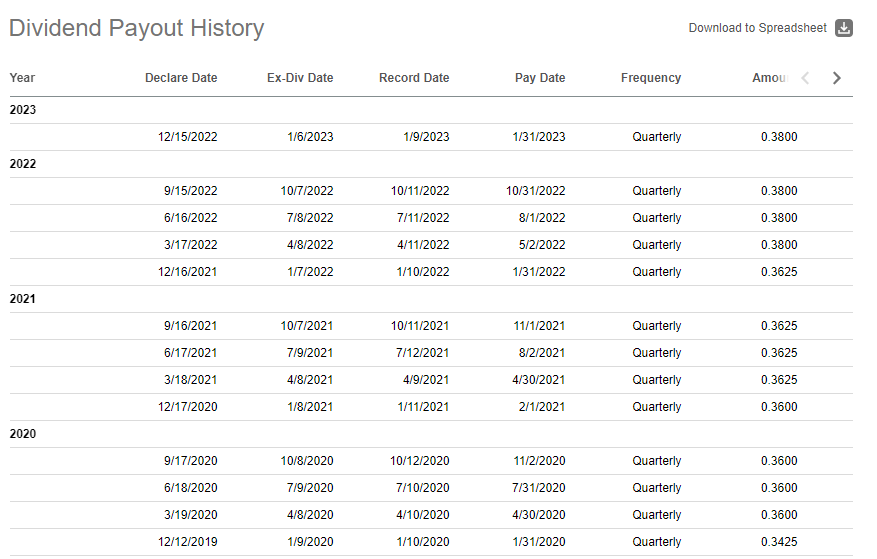

UDR’s most recent quarterly payout amounted to $0.38/share. This represented an annualized yield of about 3.5% at current pricing. Furthermore, this was their 201st consecutive quarterly payout.

Seeking Alpha – UDR Recent Dividend Payout History

In addition to its regularity, the payout is backed by one of the strongest track records of continuous growth, with a five-year compound growth rate of about 4%.

In fact, management announced yet another increase in their Q4 release. For 2023, their annual payout is now set to be $1.68/share. That would represent a 10.5% increase over 2022 and would provide investors with a 30bps uptick in yield.

While that still may not be enough for most investors seeking greater yield, the continued commitment to steady increases is one standout aspect of the company that provides credibility to their underlying portfolio of assets and cash flow potential.

Investors could also take comfort knowing that the dividend is fully covered by their operating funds. In 2022, the payout was about 70% of their annual adjusted funds from operations (“FFO”). In 2023, based on current projections, it is expected to be slightly higher than the low end of their guidance range, at 75%, but comparable to 2022 payout levels at the top end of the range. Compared to sector averages, this is on par with the industry.

Main Takeaways

UDR maintained their operating strength throughout 2022, and their portfolio remains well-anchored by strong occupancy levels and high operating margins.

Their same-store portfolio, which represents 90% of their total NOI, had a weighted average occupancy rate of 96.8% at year-end, little changed from last quarter and down just 20bps from last year despite higher rental rates.

The higher rental rates in turn drove revenues to double-digit gains in the current year. And this was paired with adequate expense control, resulting in a year-end operating margin of 70.2% in their same-store portfolio. This was up 140bps sequentially and 90bps YOY.

Growth, however, is expected to moderate in 2023, though management does expect to realize improved collection trends during the year. The current figure on that is a range of 98.3% and 98.7%, representing a 10bps improvement at the midpoint from 2022 results.

The strong results in the current year enabled the announcement of a 10.5% increase in their annual dividend payout. For income investors seeking steady growth and reliable income checks, few are as trustworthy as UDR. Unfortunately for yield-seekers, the higher payout still yields less than an annualized 4%. For many, this is not enough to get excited about.

While shares can ride higher on general market momentum, the upside appeal appears to be capped in the near-medium term. Shares are already up over 13% YTD and comfortably off their 52-week lows. And at 18x forward earnings, the stock trades in line with their peer set. Mid-America Apartment Communities (MAA), for example, currently fetches 18x, while Apartment Income REIT (AIRC) trades at a more discounted 16x multiple.

For investors seeking new positioning, UDR is a stock that can reliably provide reoccurring dividend checks. But this doesn’t mean it can continue outperforming the market through the remainder of 2023.

Be the first to comment