Christian Petersen

Thesis

Ubisoft (OTCPK:UBSFY) stock slumped as much as 25% since I argued the company could be the most ‘undervalued game studio’ – only two months ago. Apologies for my too early enthusiasm about Ubisoft’s valuation. However, I still strongly believe that the company’s equity is likely worth more than $5 billion. And in my opinion, the latest sell-off only makes Ubisoft stock more attractive. In fact, I disagree with the market that Ubisoft’s ambition to cut costs (such as cancel speculative game developments) is a negative.

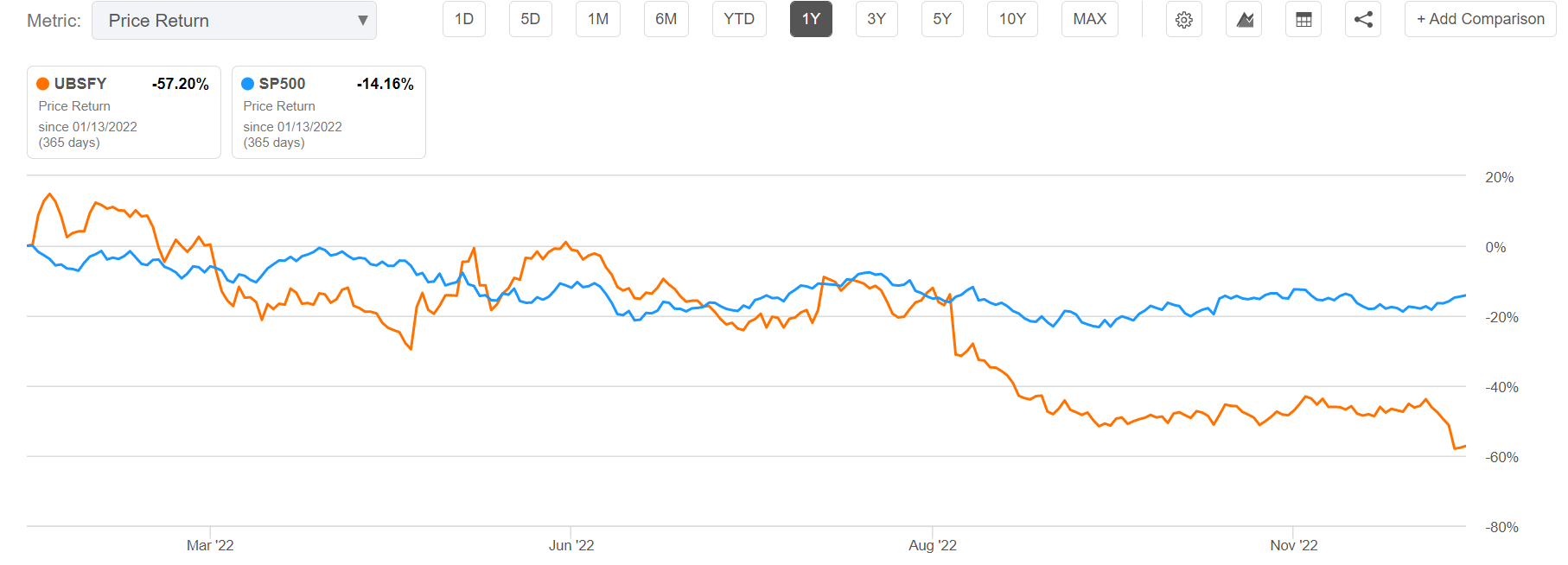

For reference, Ubisoft stock is down approximately 57% for the trailing twelve months, as compared to a loss of about 14% for the S&P 500 (SPY).

Seeking Alpha

Why Ubisoft Crashed More Than 20 Percent

Ubisoft has shown weak price action after the game studio Frontier Developments (OTC:FRRDF) warned that sales and profits for Q4 2022 will likely come in materially lower than what has been expected. Only two days later, Ubisoft issued a press release: The company warned that management now anticipates a FY 2022 operating loss of approximately €500 million, as compared to a €400 million profit predicted less than 3 months ago. In addition, revenue for the December quarter is now expected to be only €725 million, versus a previous guidance of around €830 million.

There are a few challenges to highlight: First, a weaker than expected sales record for Mario + Rabbids: Sparks of Hope, as well as a disappointing customer reception for Just Dance 2023, pressure the company’s topline. Second, Ubisoft failed to capture lost revenue with Skull and Bones, a game whose release has been postponed once again, to early 2023-2024. Third, Ubisoft cut a few speculative projects, including three unannounced new games. According to the company, these decisions will likely result in a depreciation of approximately around €500 million of capitalized R&D.

It’s Not All Bad

With lower than expected revenues in the December quarter, another Skull and Bones game delay (the sixth now), and the cancellation of three unannounced games, it is no surprise that investors are disappointed. Investors should acknowledge, however, that not everything is only bad. First of all, the worse than expected performance during the 2022 holiday season could be due to macroeconomic challenges (for sure Ubisoft is not the only game studio affected) and these challenges might be temporary. Secondly, Skull and Bones will eventually launch. And third, investors might appreciate the cancellation of unannounced games as a cost-cutting initiative with the benefits of a likely margin expansion.

Long-term, I would say for the next 3-4 years, Ubisoft has a strong enough pipeline to stomach working on fewer games. In fact, successfully expanding existing strong franchises, such as Assassin’s Creed, Far Cry, Tom Clancy’s Ghost Recon, Tom Clancy’s Rainbow Six, Tom Clancy’s Splintercell and Tom Clancy’s The Division, will likely be enough to support revenue expansion through 2025. Moreover, investors should consider that Ubisoft continues to work on Avatar Way Of The Water and an unannounced Star Wars Game – two games that are almost guaranteed to attract a large customer base. Reportedly, Ubisoft is already testing the gameplay of these titles and working to conceptualize potential monetization opportunities. Personally, I believe it is reasonable to expect that Avatar Way Of The Water will be released sometime in early 2024, and the Star Wars game could likely be released later the same year.

Focus On The Financials

With all the noise and headwinds surrounding Ubisoft, I argue it would be wise to focus on the company’s financials. With $2.35 billion of revenues and $387 million of operating profit in FY 2022, Ubisoft is effectively trading at an FY 2022 EV/Sales of about x1.6 and a EV/EBIT of less than x10. And with the increased focus on cost discipline, as well as the increased focus on further developing existing AAA franchises that already attract a strong consumer base, there is, in my opinion, little doubt that Ubisoft will disappoint on the current valuation.

In fact, Ubisoft said that the company expects to generate approximately €400 million of operating income in FY 2023-2024, a number that is ‘reflecting necessary prudence’. In addition, with about $1.5 billion of cash and cash equivalents, Ubisoft’s balance sheet remains strong enough to push through the eventual release of key titles. In my opinion, at below $3 billion of market cap, Ubisoft is simply too attractive to ignore.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment