Antonio_Diaz

Uber Technologies, Inc. (NYSE:UBER) released its FQ4 2022 earnings today (February 8) and saw significant investor attention. This saw its stock spike pre-market. However, the enthusiasm has abated, as savvy investors likely capitalized on the surge to cut exposure.

UBER had recovered remarkably from its late December lows, up nearly 60% through this morning’s highs. As such, we believe investor optimism has likely been reflected, even as Uber assured investors with a double beat on revenue and profitability.

Consumers have continued to spend on services, which also lifted Uber’s operating performance. In addition, management articulated that the record inflation rates have driven more driver-partners to join the platform to earn extra income.

Management highlighted that Uber’s “driver supply is growing, with drivers up 35% and new driver count up 34% year-over-year.” The company remains focused on driving growth and profitability, with “efficiency” mentioned no less than 12 times between analysts and Uber in the conference call.

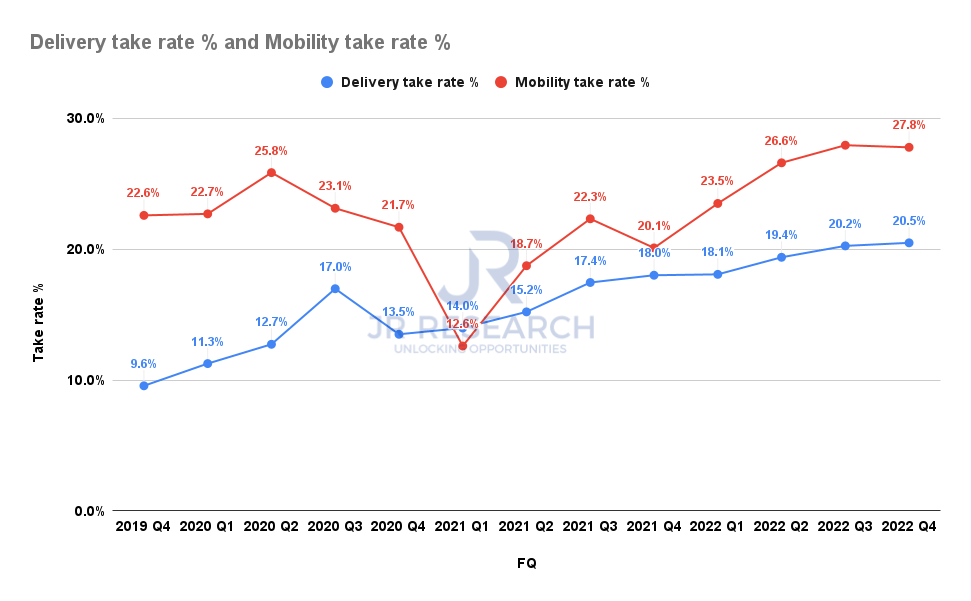

Uber take rates % (Company filings)

As such, the company demonstrated the stickiness and pricing leadership of its platform, as Uber’s take rates remained robust in Q4.

Mobility’s take rate was down 0.1% QoQ to 27.8%, impacted by “pass-through fuel surcharges.” However, Delivery continued to make solid gains, as its take rate improved to 20.5% in FQ4, up 0.3% QoQ, benefiting from “business model changes.”

Therefore, it has been instrumental in helping Uber outperform the Street’s consensus, as Uber delivered an adjusted EBITDA margin against Gross Bookings of 2.2%. Moreover, it represented an adjusted EBITDA margin of 7.7% relative to revenue, well ahead of the analysts’ estimates of 7.3%.

Investors with firm conviction in Uber’s H2’22 recovery likely added aggressively in July, when we pointed out that UBER seemed cheap. However, the sentiments in UBER back then were highly pessimistic, as the market was worried about the impact on its path toward profitability.

Therefore, we believe management’s assurance to continue its journey toward profitable growth should lift investors’ confidence further. With that in mind, we don’t think UBER will retrace back toward those lows, in line with our expectations of a market bottom in October.

Despite that, questions remain on whether consumer spending will continue to be robust, as the Fed will likely stay hawkish through the end of 2023. The strength of the labor market should help to mitigate that risk, but consumers have been drawing down their pandemic savings buffer.

Still, Uber has also likely benefited from the cost rationalization in its competitive space in H2, as the equities bear market forced its smaller competitors to cut back on unsustainable spending. CEO Dara Khosrowshahi accentuated:

“In Europe, we are seeing many of our competitors pull back significantly from what were unhealthy spend levels in the past that didn’t make any sense.”

Therefore, Uber has been able to leverage the cross-platform strategy between Delivery and Mobility, augmented by its Uber One membership, which lifted spending levels by 4.1x more than non-members.

However, as UBER has outperformed the market since its lows in December, does it make sense for investors to consider taking a pause here to allow for a healthy correction and consolidation?

UBER last traded at an NTM EBITDA multiple of 26.1x, which is pretty aggressive for a company with relatively low adjusted EBITDA margins. However, as the market typically looks ahead, UBER bulls could argue that its FY24 EBITDA multiple of 15x isn’t aggressive, based on management’s FY24 outlook.

Therefore, the critical question depends on whether investors are convinced that management remains on track to meet its FY24 target. Based on its FY22 adjusted EBITDA metric of $1.71B, Uber needs to deliver a 2Y adjusted EBITDA CAGR of more than 70% to meet its target guidance.

Management guided for a Q1 adjusted EBITDA of $680M (annualized run rate of $2.72B). However, the company will need to ramp up its profitability improvement through FY23 to close the gap with its $5B outlook.

Uber’s advertising revenue could be a constructive driver, which crossed the $500M annualized run rate, and is on track to meet its $1B target. Given the ad headwinds in 2022, Uber’s performance demonstrated that it has managed to dodge the broad challenges impacting the industry. We believe the performance in ads could be instrumental toward its adjusted EBITDA outlook, bolstering its margins profile.

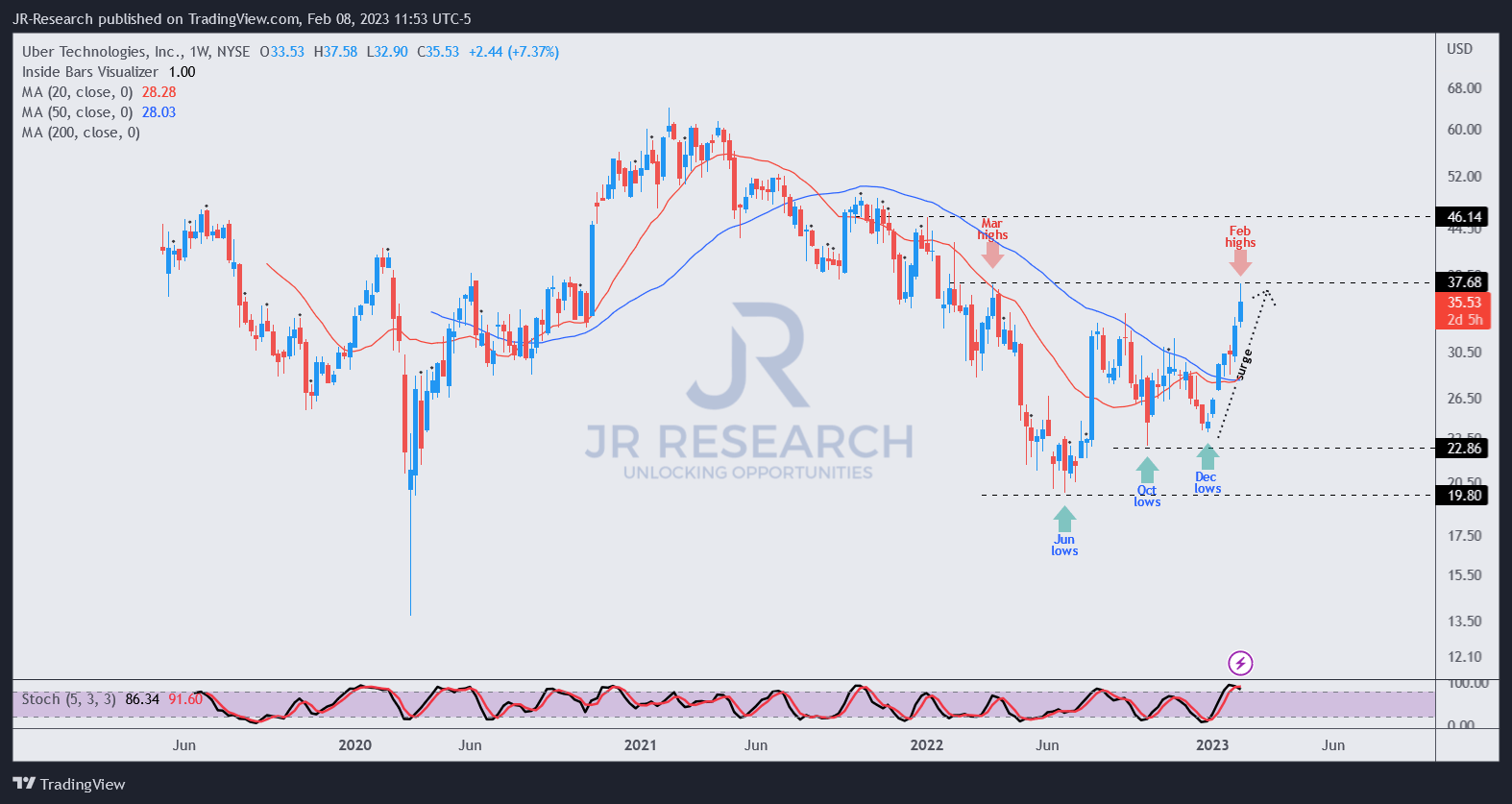

UBER price chart (weekly) (TradingView)

However, investors considering joining the recent buying frenzy need to be wary about the surge over the past six to seven weeks.

Even though we don’t expect UBER to revisit its July lows, we don’t see lower-risk entry levels for Uber Technologies, Inc. currently and believe a pullback should help improve reward/risk.

However, it’s important to note that near-term momentum could continue for Uber Technologies, Inc., drawing more buyers fearing they would miss its recovery. But, we believe investors should let the market digest the froth that has built up, as investors’ optimism could dissipate quickly when market operators start taking profits en masse. That would be a better time to strike Uber Technologies, Inc. – when there’s blood on the Street.

Rating: Hold (Reiterated).

Be the first to comment