Hiroshi Watanabe

I think Uber’s (NYSE:UBER) premium valuation at the moment could be tolerable over the long term, based on the considerable upside expected from high profitability growth driven by Uber’s autonomous vehicle plans. I think Uber could be one of the best companies to own over the next decade for exposure to AI transport. However, the short term could see negative returns if the shares are bought at this time.

Essential Operating Segments

Operational since 2009, Uber now has three core segments: Mobility, Delivery, and Freight. In 2024, the company’s Mobility segment will connect consumers with a range of transportation types, including taxis, ridesharing, rentals, public transit, and more. Its delivery segment allows customers to order meals from local restaurants or from local grocery, convenience, or other stores. Notably, it also offers Delivery-as-a-Service for retailers and restaurants who do not want deliveries to have the Uber brand attached. Its Freight segment bridges shippers with carriers, offering a transportation and logistics network with competitive pricing, shipment booking, and on-demand software for improved customer satisfaction.

Stock Price & Autonomous Future Outlook

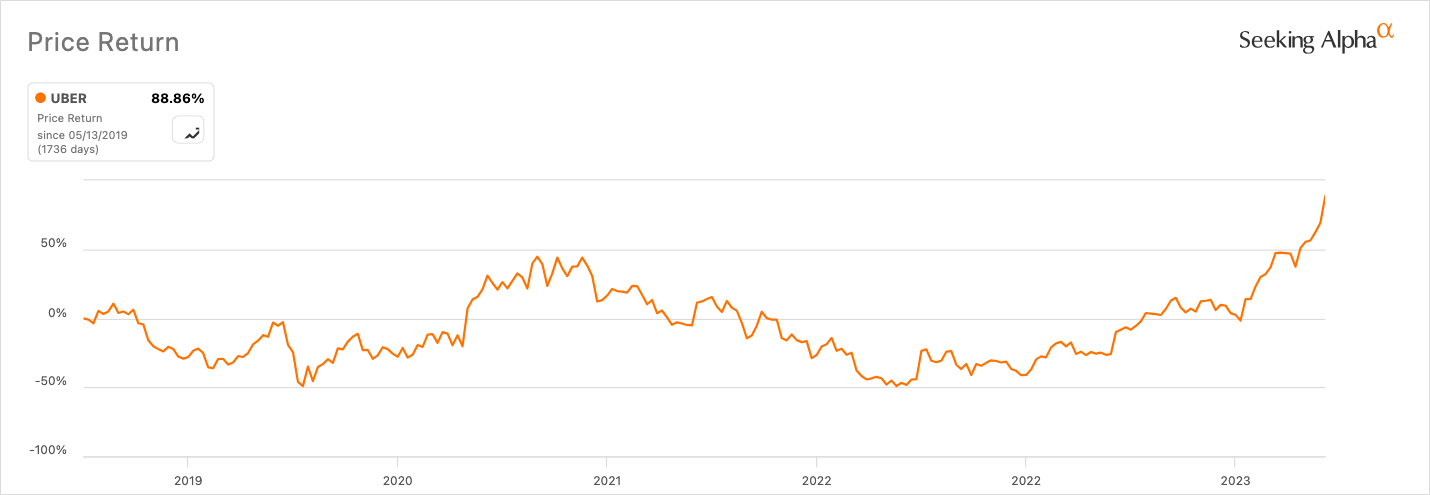

Uber stock is currently at all-time highs, and investors should be happy about this if they have held the shares since the beginning, and even more so if they bought in 2021. But now, shareholders are growing concerned about whether the results will last. There is some argument to be said that the stock is now overvalued, which I will comment on in my valuation discussion to come.

Seeking Alpha

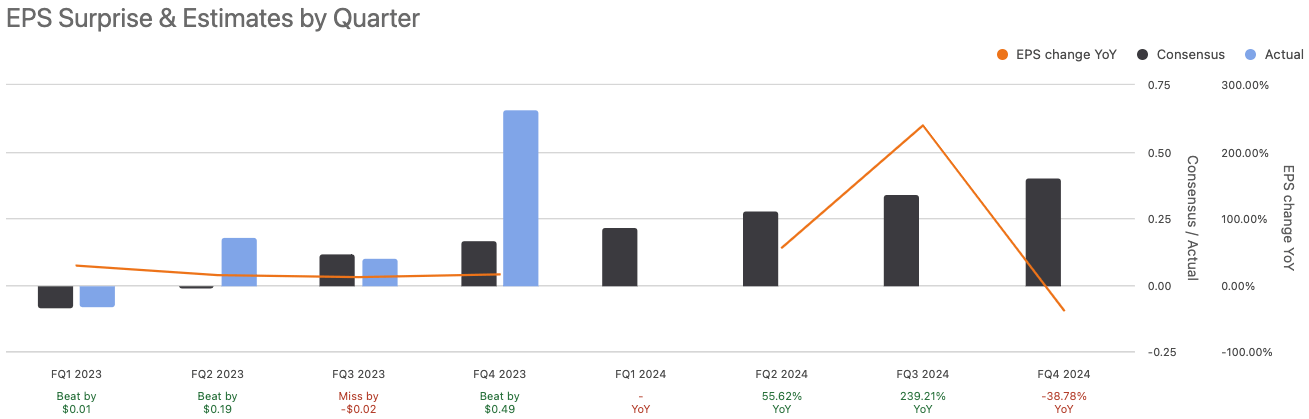

Uber’s Q4 earnings results were on the 7th of February, and it reported significant YoY revenue growth of 34% in its Mobility segment and 19% growth in Delivery Gross Bookings. Its Freight segment, on the other hand, experienced a YoY 17% revenue decline, which is indicative of broader challenges in the freight market at this time. Income from operations was up $794 million YoY and $258 million QoQ, with net income attributable to Uber of $1.4 billion.

The firm beat EPS expectations by $0.49:

Seeking Alpha

As a long-term investor, I am interested in how Uber is planning on integrating automation into its taxi services to become competitive with Tesla’s (TSLA) potential autonomous taxi service, among others. I believe this will be a critical juncture for Uber to face and will determine high levels of profitability in the long term or relative stagnation over time.

Uber has established a 10-year agreement with Aptiv (APTV) & Hyundai’s (OTCPK:HYMTF) Motional to deploy robotaxis across major cities in North America. It will initially focus on autonomous delivery in California but wants to introduce the all-electric Hyundai Ioniq-5-based autonomous vehicles into Uber’s taxi service, dramatically shifting the narrative of the taxi industry for good. This is going to be a significant boost to Uber’s long-term profitability, and it positions the firm to be exceptionally well-off over the next decade if it can execute its strategy effectively. It wants to maintain a hybrid network of human and robot drivers. Motional’s robotaxis have already been launched in Las Vegas.

Uber has also entered a 10-year deal with Nuro, an autonomous vehicle startup, so that it can use its delivery robots for Uber Eats in Houston and Mountain View, California. Nuro is one of the few companies with the necessary approvals to operate autonomous delivery in California at this time.

Uber has also partnered with Waymo to integrate its autonomous driving technology into the Uber platform, beginning in Phoenix. Waymo’s leading technology will combine with Uber’s ride-sharing and delivery infrastructure to enhance safety and accessibility for Uber customers.

Additionally, Uber chose Nvidia (NVDA) as the provider of its technology for the computing systems in its autonomous vehicles. By leveraging Nvidia’s AI technology, Uber is positioning itself to be a leader in the space of autonomous taxi, delivery, freight, and other transport services.

Finally, Uber and Toyota (TM) have expanded their collaboration in an effort to improve autonomous ride-sharing. Toyota is investing $500 million in Uber, and its technology will be integrated into purpose-built Toyota vehicles for deployment on Uber’s network.

Valuation Commentary

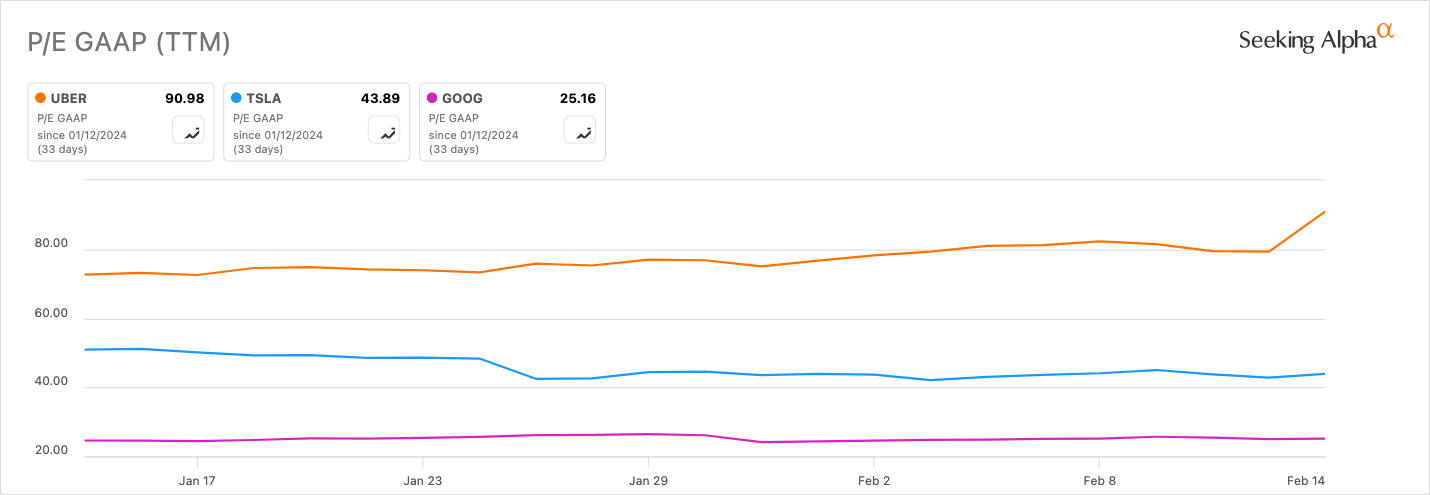

I think it is evident that Uber is significantly overvalued at this time, however, similar to Tesla, the present price could be tolerable if taking into consideration the potential upside for a 10+ year holding period. Uber’s TTM P/E GAAP ratio is 90.98, which is 289.56% higher than the sector median of 23.35. Its forward ratio, however, is a more promising 66.4, 204.75% higher than the sector median of 21.79.

With Uber commanding a P/E GAAP ratio higher than Tesla at the moment, investors should be worried about the present price being sustainable:

Seeking Alpha

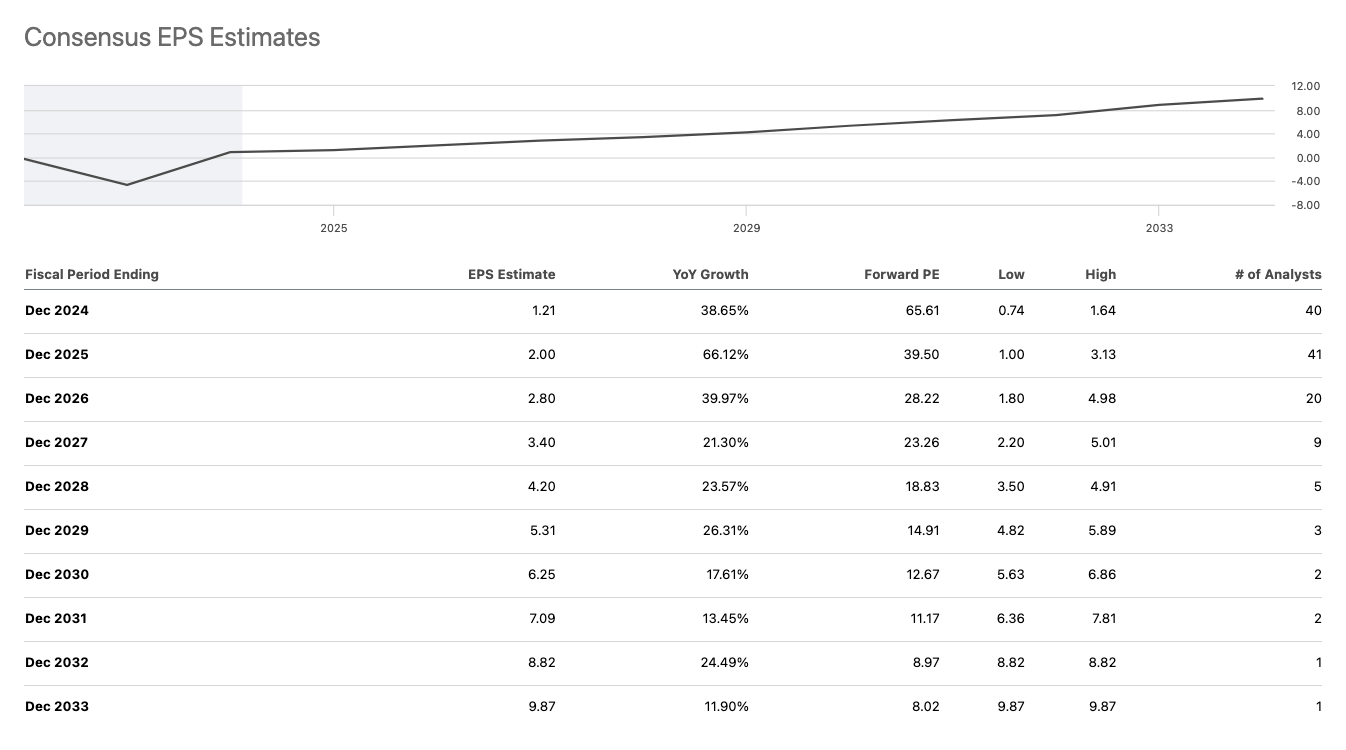

I believe Uber could be considered around 25% overvalued at this time based on my discounted cash flow analysis that takes into consideration a 28% annual average earnings growth over the next 10 years based on these Seeking Alpha analyst estimates:

Seeking Alpha

I used the 2024 EPS estimate as my starting figure, and I also computed a 4% terminal-stage growth rate and an 11% discount rate. My result was a fair value of $64.5 compared to the present stock price of $81.5.

Regulatory Risks

The incredible upside potential hinged on autonomous vehicle operations for Uber is at risk primarily from regulatory hurdles and inhibitions. The US has a diverse range of autonomous vehicle laws, and different states have different regulations that present a network of hurdles for companies like Uber to challenge and navigate. While California has expanded its testing rules for remote monitoring of autonomous vehicles, Arizona and Nevada permit testing without a safety driver.

Uber has already faced hurdles in international markets, like in London, where it struggled with license renewals due to safety concerns raised by Transport for London. Unauthorized drivers using legitimate accounts to offer rides quite rightly raised safety concerns, and Uber’s compliance with protocols is both paramount for long-term success and an inhibitor of fast traction in the market.

The National Highway Traffic Administration has been collecting data on autonomous technologies involved in crashes. Up to June 2022, vehicles with Advanced Driver Assistance Systems were involved in 392 crashes, six being fatal, in one year. There were also 130 crashes from autonomous driving systems and 16 injuries as a result.

Yet, another report notes that autonomous vehicles had fewer instances when they were at fault in a collision. Autonomous mode could actually mitigate certain types of accidents, specifically ones involving human error, making driving safer over the long term. However, convincing regulators of this and proving it through evidence over time is a medium-to-long-term task. Therefore, do not expect results overnight.

Conclusion

I’m not buying Uber at this time because the valuation is too high for me. Yet, if I was already a shareholder, I would hold my stake for the long term. There seems to be a large potential upside here from the advent of autonomous transport, which Uber is positioned to capitalize on. My analyst rating for Uber stock is a Hold.

Be the first to comment