NickyLloyd/E+ via Getty Images

Investment Summary

Since our last publication on U.S. Physical Therapy, Inc. (NYSE:USPH), urging investors to hold their positions, we’ve noted the stock has caught a strong bid into the new year. Shares are up ~19% at the time of writing after “we estimate[d] the market has overshot its selloff of USPH” longs have re-entered and repriced the stock price back above its previous highs. This is pleasing to see and we are turning more constructive on the name as 1) the broad market’s gain in risk appetite; 2) momentum in the stock price with a break above previous highs and rating higher the last 5 weeks in a row; 3) economics of its injury prevention/occupational rehab division [see: last publication]. I encourage you to discover more on the company’s economics in our original USPH publication.

However, there’s still many hurdles must overcome in the realms of economic profitability, value creation for shareholders, and fair valuation of its stock price. These facts support our neutral stance into its FY22′ earnings, hoping for a strong earnings surprise to the upside.

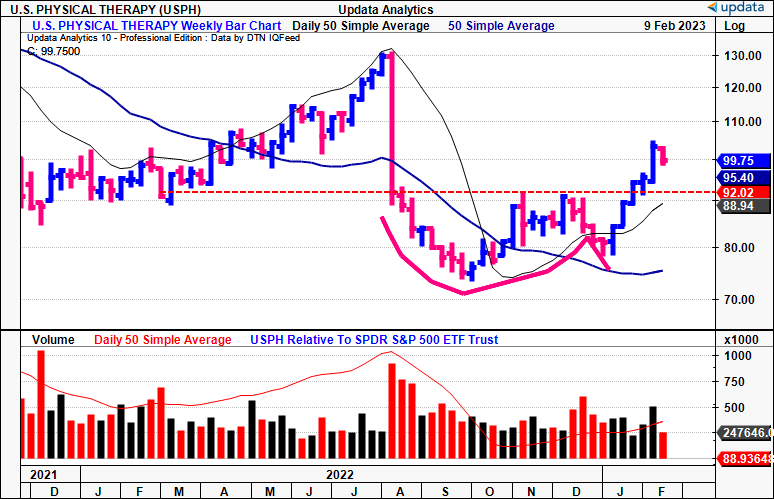

Exhibit 1. USPH breakout above previous resistance, thrust off 23-week cup and handle

Data: Updata

Profitability momentum hurting valuation upside

The company operates 640 outpatient physical therapy clinics in 40 states [as of Q4 FY22′] and continues to build out new stores/acquisitions. We mentioned this in our original thesis on USPH: “a key factor to appreciation in USPH shares over the previous 3 to 5-year period has stemmed largely on the back of a successful acquisition schedule over this time. The benefits here lie in that, the company can leverage a low fixed and variable cost base [being in a service based industry], plus also realise high cash-flow turnover with low OPEX tied into the mix. This formula equates to a widening revenue/OPEX spread over time. As much occurs because the company relies on acquisitions and already running Physiotherapy clinics to drive revenues, instead of allocating expenditures towards opening new facilities”. On this note, the company delivers additional growth via same facility revenues in addition to its new facility count growth. In this vein, we need to see its incremental ROIC>historical ROIC for this growth model to work, where new facilities are equally as, or more profitable, than legacy stores. It added 41 new stores last reporting period with daily patient growth of 1.6 patients YoY to ~29.5, whereas costs per visit rose 600bps YoY to $81.09 producing a net rate of $103.18 for its physical therapy operations.

To examine this leading into the company’s FY22′ numbers we looked at rolling TTM periods from Q1 FY20–Q3 FY22′ [see: Exhibit 2]. We took the operating approach to analyzing post-tax earnings and ROIC, and noted that it accumulated $598mm in NOPAT over this time, for an additional growth of $5.74mm in post-tax earnings. Similar figures for net earnings are observed in Exhibit 3. ROIC has hovered ~8–10%, as seen. Note, we included goodwill in the calculations, as it represents the premium paid for an acquisition, and therefore a transfer of wealth from equity holders to the target company.

Exhibit 2.

Data: Author, using data from USPH SEC Filings

For it to generate this growth, $130mm in capital investment was required, claiming ~22% of post-tax earnings as reinvestment for the future growth [Exhibit 3]. Unfortunately, the incremental ROIC on this is tight at 4.42%, clamping overall company growth rates. A highlight from this model, is the CapEx and investment schedule still allowed USPH to distribute ~78% of post-tax earnings to equity holders, securing its dividend.

Exhibit 3.

Data: Author, using data from USPH SEC Filings

Three main observations are drawn from Exhibit 2 and 3:

- The rolling TTM (“periodic”) ROIC hasn’t grown since Q1 FY20′

- Since Q3 FY21′ the periodic ROIC is less than the cost of capital, leading to an economic loss since Q3 FY21′ at least [see below]

- The incremental ROIC<historical ROIC.

Alas, despite consecutive YoY growth percentages throughout the last 2-years, new facility growth doesn’t look to have been accretive to value just yet. Further, and supporting our hold re-rating, is that the company’s growth has hurt its valuation due to the economic loss. As a reminder, a firm creates additional value when the ROIC exceeds the hurdle rate, otherwise, growth is destructive to value. This is observed with USPH in our testing period.

Exhibit 4.

Data: Author

Subsequently it’s imperative that USPH come in with a strong set of numbers for FY22′ in order to demonstrate the success of its growth engine. New-added centres need to pull their weight, and the company needs to pay a fair price for each. This will be evidenced in the metrics presented in the 10-K, and so we are eagerly awaiting this.

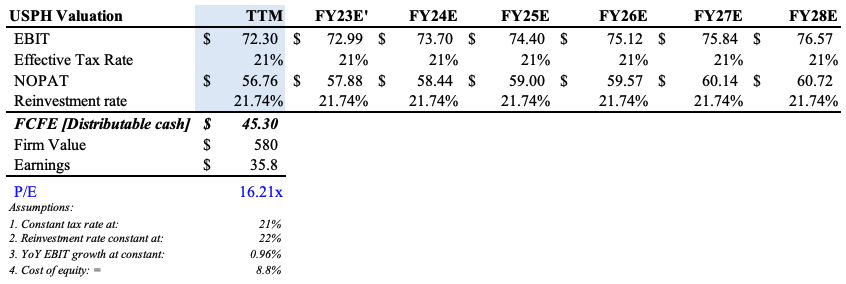

Valuation and conclusion

The stock is richly priced at 37x forward earnings and the question turns to is this a fair price? It depends on how one looks at it. Growth has been negligent since pre-pandemic times and we’ve shown it has come at a cost to the company’s corporate value. We took an opportunity cost of equity at ~9% combining the S&P 500 earnings yield, USPH’s growth and reinvestment rates, plus the risk-free rate, and discounted the estimated FCF’s to equity holders into FY28′ and derived a fair P/E of 16.2x. Key supportive factors to this valuation include:

- Tight growth rates after reinvestment for growth

- Negative ROIC/WACC spread, as above

- Incremental ROIC<Historical ROIC

Exhibit 5.

Note: Earnings are FY22E’ earnings estimates (Data: Author’s Estimates)

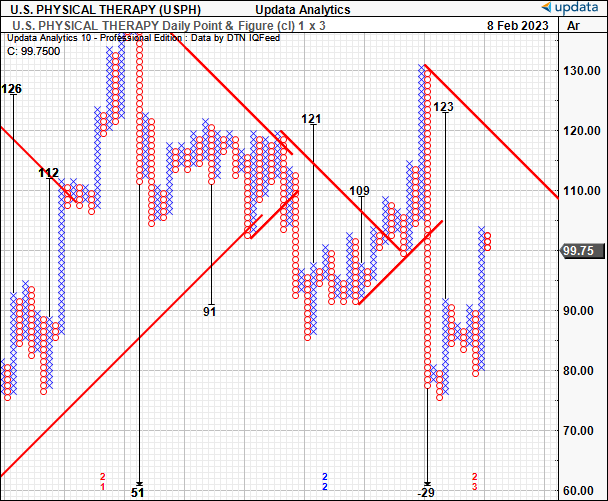

Interestingly, we have upside targets to $123 on our point and figure studies. We can arrive at this valuation using the above model, with USPH at 45.95x earnings, derived from NOPAT growth of ~5%, and using the company’s earnings yield and growth rates, per Roberts (1991) at ~8%. Consequently, we need USPH to deliver ~5% YoY growth in post-tax earnings in its FY22′ numbers to justify this valuation.

Exhibit 6. USPH valuation at 45.95x earnings with 5% NOPAT growth

Data: Author

Exhibit 7.

Data: Updata

Net-net, we reiterate our hold thesis on USPH until we have more clarity on its capital budgeting and returns on capital for FY22′. Over the last few years, the long-term predictable capital hasn’t pulled through, and low returns of capital have been sticky for the company across this period. It’s business model has propensity to deliver on this front, so we are hoping for a strong earnings surprise in its upcoming FY22′ numbers. Net-net, reiterate hold.

Be the first to comment