RiverNorthPhotography

Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on January 21, 2023.

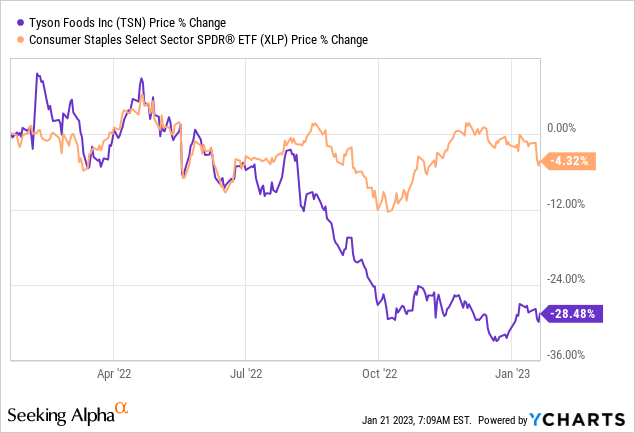

Tyson Foods (NYSE:TSN) delivered us some options premium as shares bounced off of the lows they touched in the latter part of 2022. There are certainly headwinds for this name, but the price has reflected much of that by the decimation it essentially took relative to its sector in the last year.

Ycharts

Consumer staples had done remarkably well through 2022 as defensive plays. Albeit, more recently, they took a big hit as recession fears crept back in. Talk about my unfortunate timing with selling puts on Kellogg Company (K) – but that’s a whole different topic! Today, we are looking at TSN, and that successful trade as the puts we had written expired worthless.

On December 8th, 2022, I shared that I was writing puts at a strike price of $60 while collecting $0.80. This was 43 days until expiration, and it worked out to a PAR of 11.32%. This is on the lower end of my usual target of roughly 15% PAR.

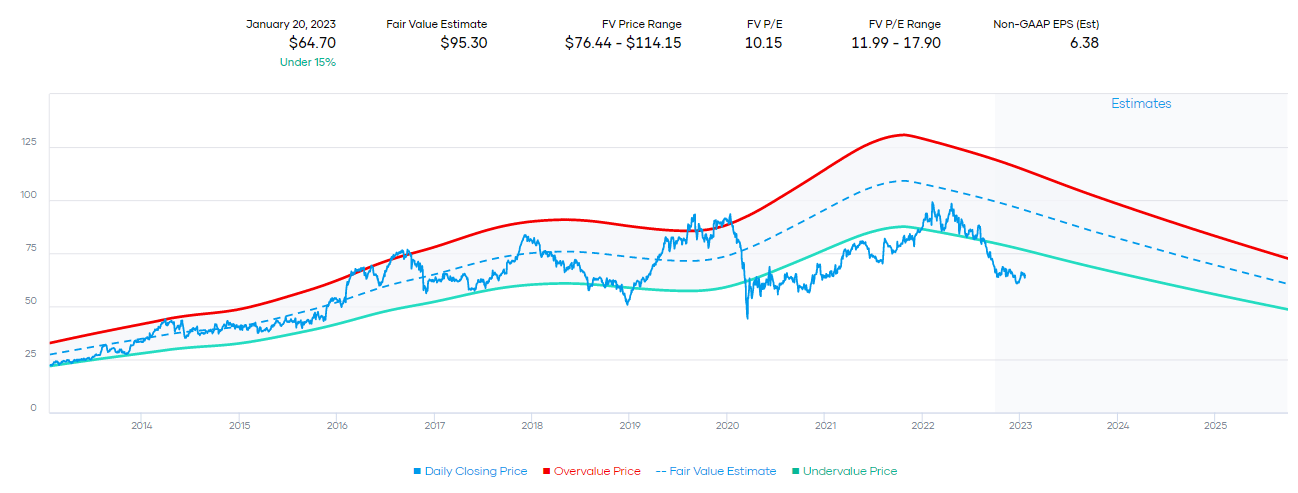

Still, it was a name that I wouldn’t mind holding, and it came down quite significantly, so I was feeling more comfortable. At the end of the day, it would have meant a breakeven of $59.20, and carrying shares at that price is fairly attractive. At least if you consider the fair value estimate of ~$95 according to the historical P/E range.

TSN Fair Value Based On Historical P/E (Portfolio Insight)

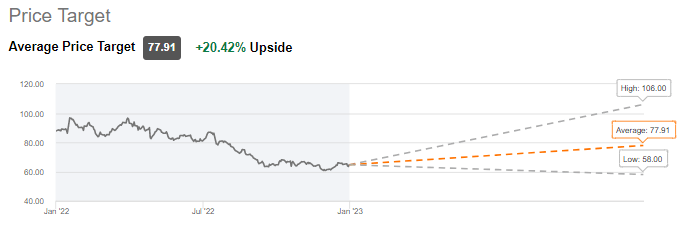

Wall Street analysts have a price target that comes in around $78 as the average price target of 13 different analysts. Currently, the stock is rated as a “Buy.” With a forward P/E of around 10x, it certainly is clear why it seems like such an attractive name.

TSN Price Target (Seeking Alpha)

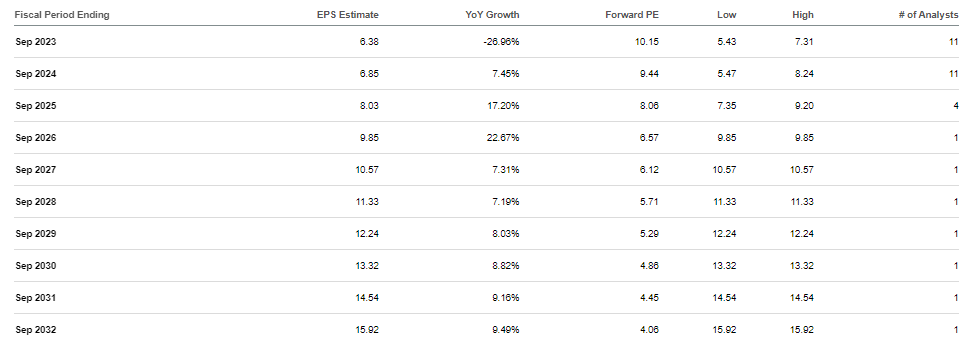

The earnings are expected to be soft in this next year, but that’s precisely why the stock looks more attractively valued at this time. When you look to “buy low and sell high,” it can often mean you are investing when things aren’t necessarily looking the greatest.

After this rough year, analysts expect TSN to start delivering some solid growth once again. You don’t have to go out too far before seeing that forward 10x earnings multiple turns into single-digit forward multiples.

TSN Earning Estimates (Seeking Alpha)

It hasn’t been so long since I provided an overview of TSN, with a posting on the name just in December. So I won’t try to drag this out too long.

However, two points were brought up in the public release of that article. The first was the bird flu, and the second was the closing of some of their corporate offices to pull more of those positions into their Arkansas headquarters.

I didn’t note them specifically because most of that is already priced in, in my opinion. It’s why we are looking at TSN at 10x. I also believe these are short-term speed bumps that won’t determine if TSN survives or not. At the end of the day, every investor needs to be comfortable with whatever they are investing in at a certain price – for me; we are already there for the shares of TSN.

Bird flu isn’t new; they happen quite often, or the same one lasts years. This latest one happens to be the worst, passing 2015, which was the previous record. CEO Donnie King had recently touched on the topic and how it pertains to Tyson. He mentioned that it certainly is having an impact, but it’s more disruptive to the egg-laying side of the equation. Instead, he mentioned the cost of grain is more of a factor in pushing prices higher. At the end of the day, it is something that they will work through.

With the corporate relocation and mass amounts of those employees walking off and not transferring to Arkansas headquarters, I view it as pretty much a non-issue. Giving them the benefit of the doubt, this is unlikely that it was a spur-of-the-moment decision. This is something that was more than likely expected.

If they wanted a certain employee, they would do what is necessary to retain this staff. Getting skinny is an emerging key theme in 2023, albeit more of the announcements are coming from the tech space. However, it isn’t restrained specifically to that sector. Overall, this seems like a non-event, in my opinion.

What’s Next?

Despite shares climbing from where they were when we originally sold puts, I’m still interested in writing more puts. Their earnings are expected on February 6th, 2023. Any expiration we selected would put us on the other side of that, so we are getting elevated premiums due to that event.

- February 17th, 2023, expiration at the $60 strike could net us $0.60 in premium. This is less than our last trade, but it’s also a reduced number of days. The PAR, in this case, comes out to an attractive 13.51%.

- Going with the same expiration date but bumping up the strike price to $62.50 is certainly tempting. That allows less of a downside cushion, but we could net $1.20 in premium. That would take in a juicy PAR of nearly 26%.

Their next ex-dividend date is February 28th, 2023. That would mean that if we took the assignment, it would be heading right into being able to receive a dividend. If an assignment happened, the options are fairly lively for TSN, so writing covered calls shouldn’t be a problem either.

Be the first to comment