Drew Angerer

Thesis

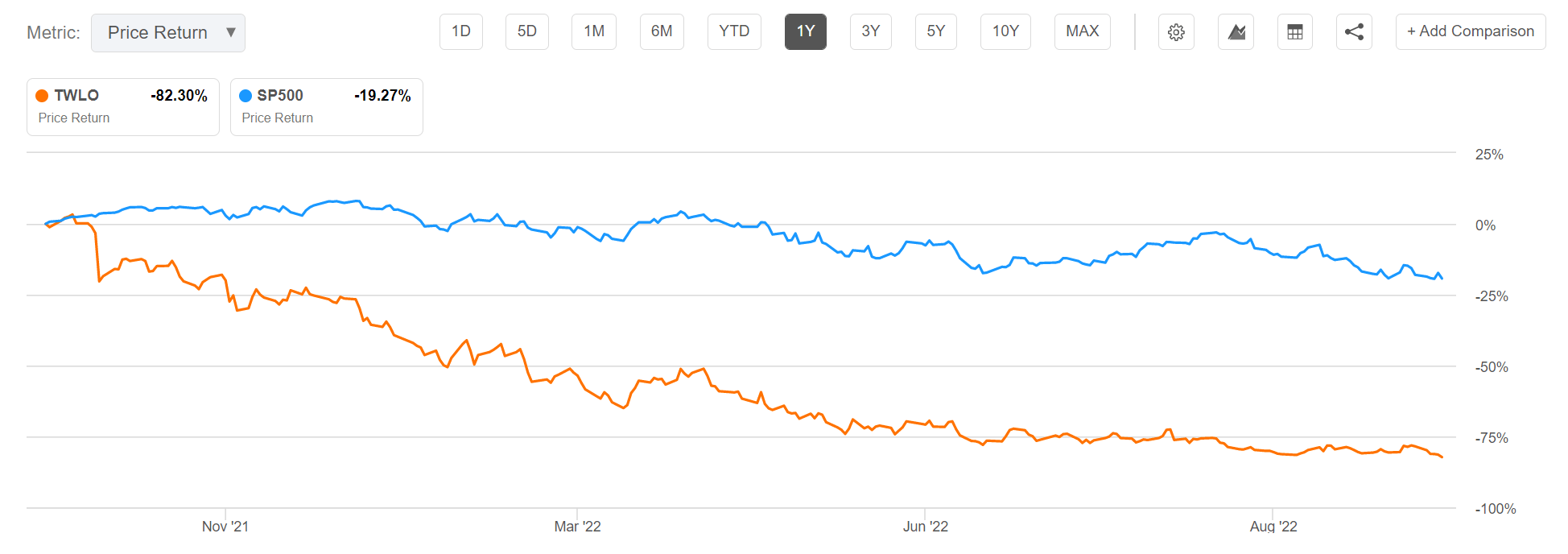

Twilio stock (NYSE:TWLO) is down by about 76% year to date and 85% from all-time highs. The valuation is now very attractive – trading at a one year forward EV/Sales of about x2.3. And given a reasonable 3-year CAGR outlook of about 30%, this ratio should contract towards x1 by 2025 (assuming flat market capitalization and net debt).

Moreover, profitability doubts should soon disappear, as CEO Jeff Lawson is convinced that the company will achieve positive operating income as early as 2023.

Seeking Alpha

Still A Growth Story

On the backdrop of enterprise digitalization and increased adoption of cloud-based communications solutions, Twilio’s business has expanded at a rapid pace. From 2017 to 2022 (TTM reference) Twilio’s revenues have increased at a greater than 50% CAGR, growing from $399 million in 2017 to $3,902 million for the trailing twelve months. Over the same period, gross profit increased at a 50% CAGR: jumping from $216 million to $1,631 million.

While in 2022 growth has slowed sharply for many businesses, Twilio still managed to perform – despite the challenging macroeconomic backdrop. In Q2, the company generated $943 million of sales, reflecting a 41% year over year increase. Moreover, although Twilio guided somewhat cautiously for Q3, expecting only $965 – $976 of revenues, analysts remain confident that Twilio could defend a greater than 25% CAGR through at least 2025 (Source: Bloomberg Terminal, EEO, October 14).

Expecting Profitability For 2023

Like many high-growth companies, Twilio has yet to prove operating profitability. In the past few years, this pressure has not been a problem for management, given that investors valued aggressive growth more than profits, and growth capital was cheap. But the environment has turned viciously in late 2021/2022.

That said, Twilio CEO Jeff Lawson is very confident that the company will reach operating profitability in 2023:

we continue to affirm that for the year 2023 we are targeting operating profitability .. which we have been telling investors all along. And we are laser focused on delivering on this goal.

When asked if this goal would be connected to an improving macro environment, Jeff answered:

I do not think so. We monitor macro trends. But (so far) we have not seen a broad based impact or demand change in our business. We have seen certain categories that have enjoyed strength actually – like financial services, [and] IT.

In my opinion, profitability should be achievable on the backdrop of reducing employee count and other ‘efficiency levers’. Only a few weeks ago, Twilio announced to lay off about 11% of its work-force, which could likely support as much as $120 million in lower operating costs.

Moreover, looking at Twilio’s income statement, the company could likely target a material reduction in the annual $1,723 billion of SG&A and $953 million of R&D expenses (TTM reference), which consume as much as 50.5% and 28% of revenues.

Attractive Valuation

The problem with many growth companies is that they are priced at an excessively high valuation. But as of October 2022, Twilio is not trading at such levels anymore – having lost about 85% of equity value from all-time highs.

TWLO stock is now valued at an EV/Sales of about x2.3, which compares to a x4.7 EV/Sales for Salesforce (CRM).

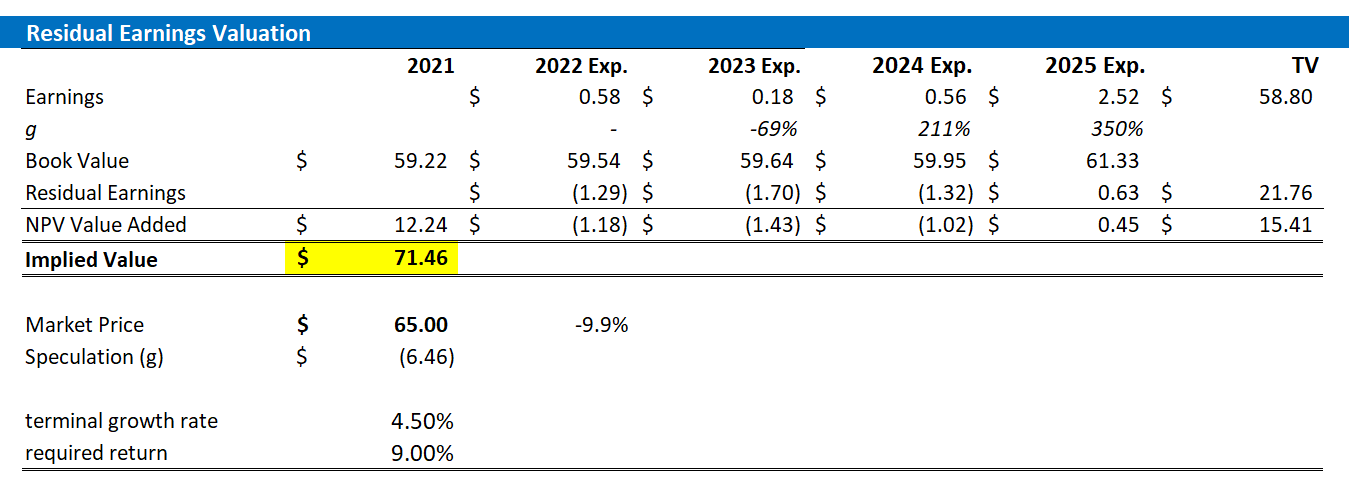

Residual Earnings Valuation

To get derive a more precise estimate of a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my TWLO stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise

- To estimate the capital charge, I anchor on TWLO’s cost of equity at 9%.

- For the terminal growth rate after 2025, I apply 4.5%, which (about two percentage point higher than estimated nominal global GDP growth)

Given these assumptions, I calculate a base-case target price for TWLO of about 71.46/share.

Analyst Consensus Estimates; Author’s Calculations

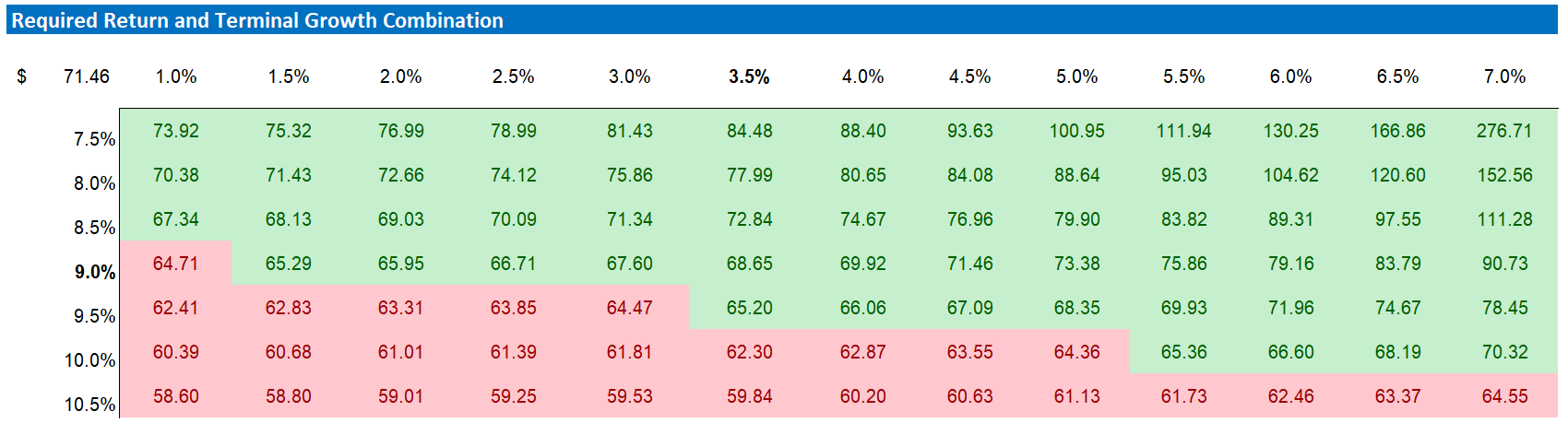

My base case target price does not calculate a lot of upside. But investors should also consider the risk reward profile. To test various assumptions of TWLO’s cost of equity and terminal growth rate, I have constructed a sensitivity table. Note that the matrix looks very favorable from a risk/reward perspective. With bearish assumptions, the downside case is somewhere around $59/share, while with bullish assumptions, the upside case could be as much as $277/share.

Analyst Consensus Estimates; Author’s Calculations

Risks

Reflecting on Twilio’s strong Q2 quarter, and the company’s CEO confident comments about the business’ resiliency, I do not see any material risk to Twilio’s growth outlook and/or competitive positioning. But investors should note that the company might fail (simply a function of probabilities and uncertainty) to deliver operating profitability in 2023. This would definitely be taken as a strong disappointment from investors and the stock would probably sell-down to the low $50/share, if not to the all-time lows around $30/share.

Investors should also consider that much of TWLO’S share price volatility is driven by investor sentiment towards risk and growth assets in general. Thus, investors should expect price volatility even though Twilio’s business outlook remains unchanged. Finally, rising real yields could add significant headwinds to Twilio’s stock price, as the higher discount rates affect the net-present value of long-dated cash-flows.

Conclusion

I like the risk/reward from buying TWLO stock at prices below $70/share. In my opinion, a valuation of x2.3 EV/Sales simply does not correctly account for the company’s strong growth outlook, and (hopefully) operating profitability by 2023.

According to my model – which I anchor on a residual earnings valuation – TWLO stock should trade at $71.46/share. Buy.

Be the first to comment