Tippapatt/iStock via Getty Images

Twilio (NYSE:TWLO) crashed amidst the tech stock crash, then crashed again after its analyst day. The company finally withdrew medium term guidance, citing the tough macro as the explanation. TWLO once traded like it was one of the highest quality stocks in the tech sector, but now trades as one of the cheapest. The company has a large net cash position and is guiding for non-GAAP profitability by next year. While it has been a painful ride, I expect the stock to eventually reflect the attractive fundamentals as this beatdown has been far overdone.

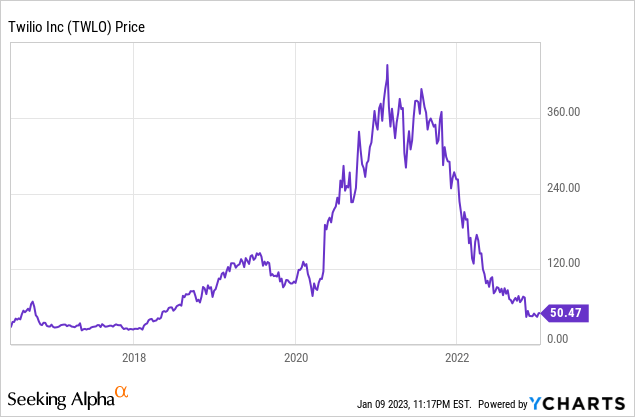

TWLO Stock Price

TWLO was far too overvalued in 2021 amidst the tech bubble. But was the stock overvalued before the pandemic, even in 2019? The current stock price seems to suggest so, with the stock down 70% from 2019 levels.

I last covered TWLO in October where I called it a “diamond in the tech bloodbath.” The company then proceeded to nosedive after reporting third quarter earnings which I found to be a curious reaction considering that the valuation had already been reset ahead of the pull down in guidance.

TWLO Stock Key Metrics

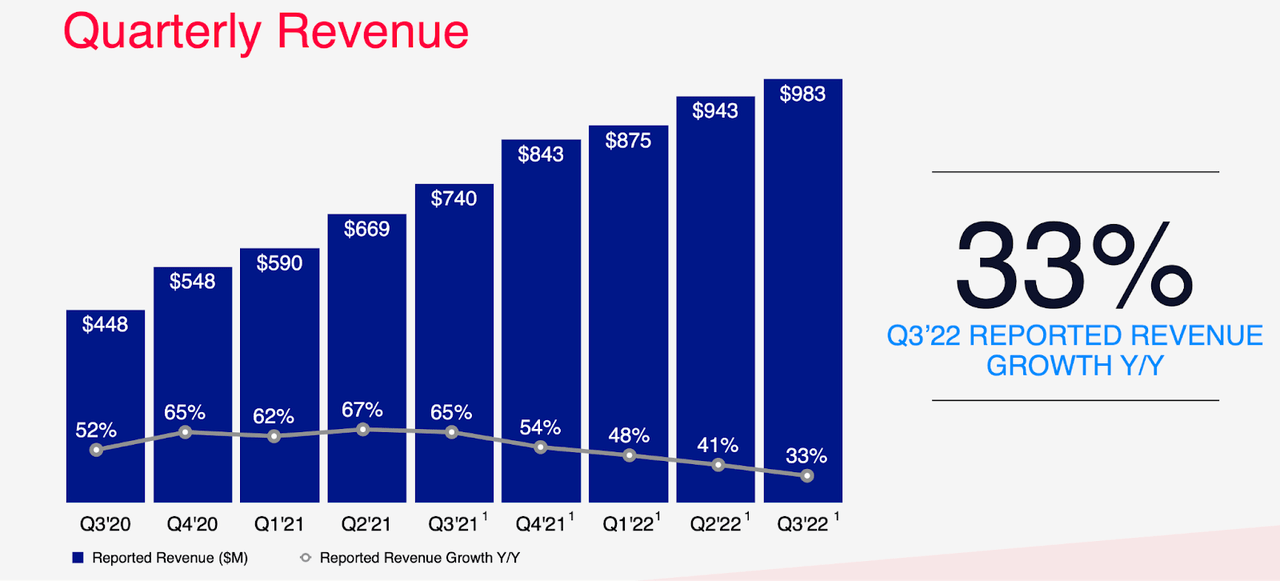

In the third quarter, TWLO continued to generate respectable growth at 33%, though that did reflect the 5th straight quarter of sequential deceleration.

2022 Q3 Presentation

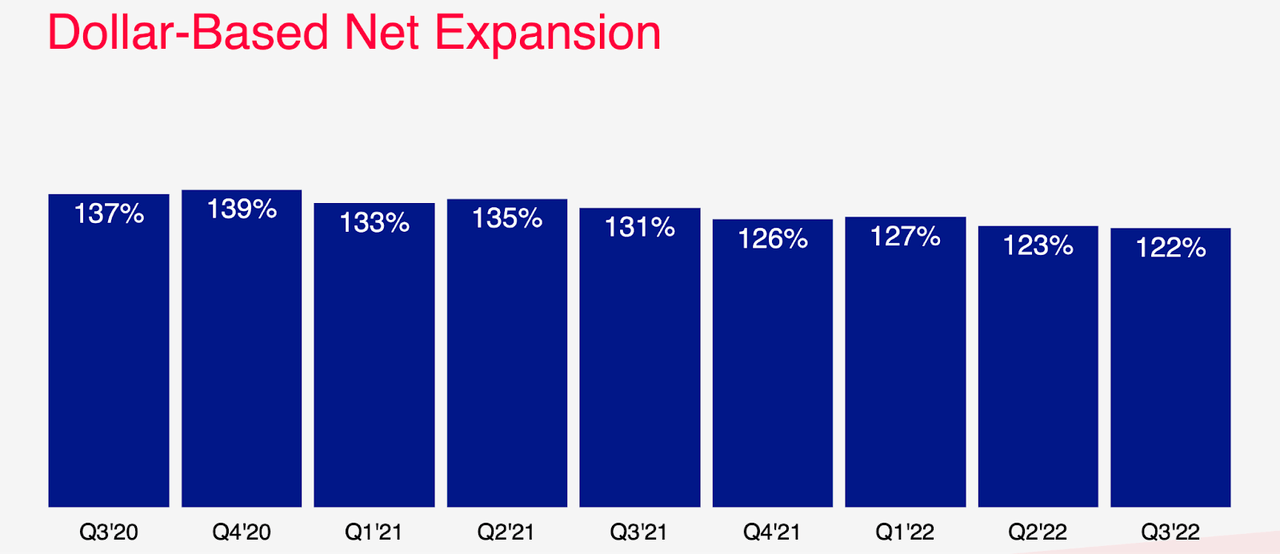

As usual, a high 122% dollar-based net expansion rate was the primary driver of that strong growth.

2022 Q3 Presentation

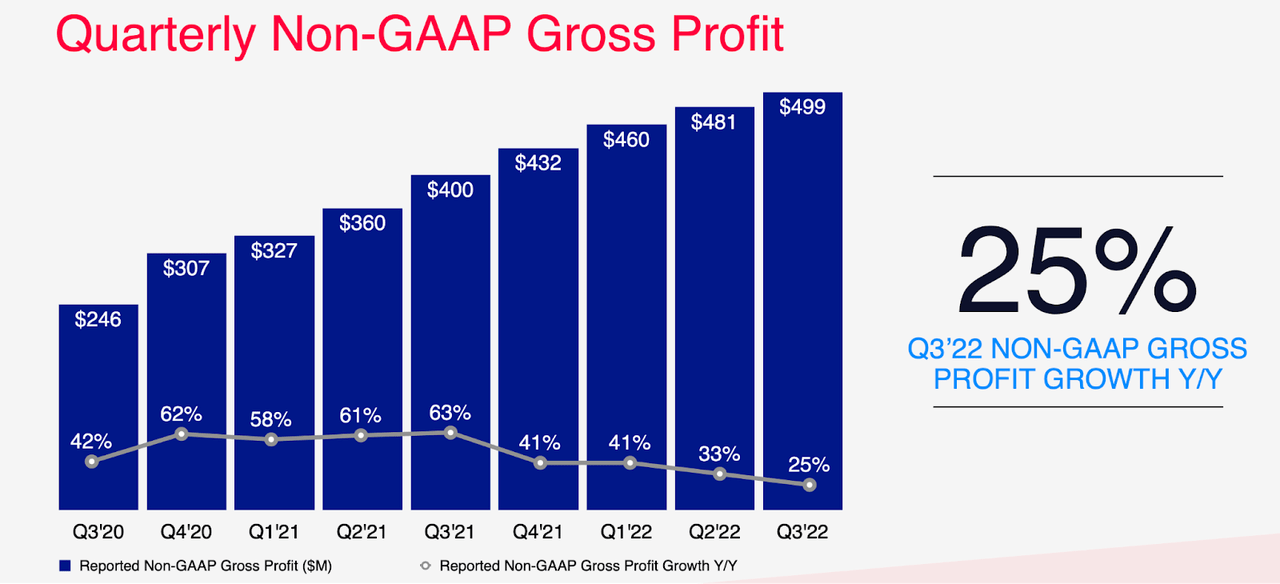

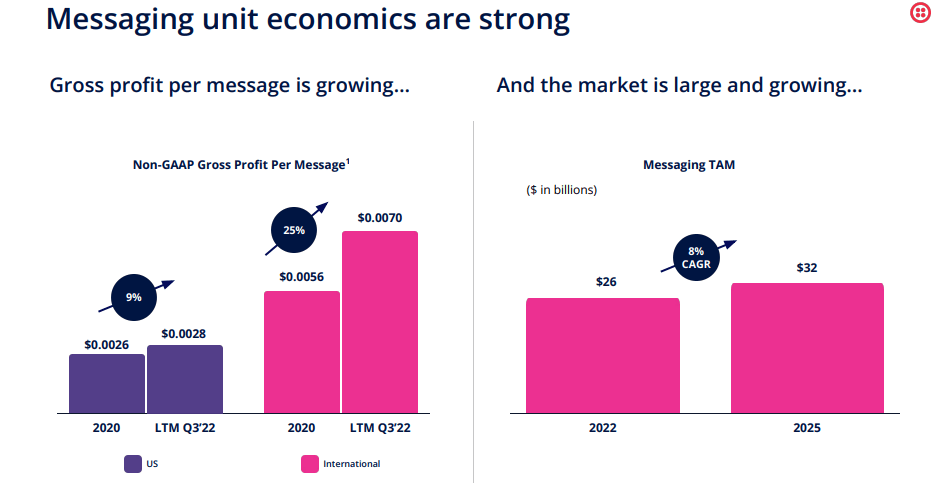

While revenues grew by 33%, gross profits grew by only 25% as the company saw its strongest growth in lower-margin messaging business segments.

2022 Q3 Presentation

On the conference call, management explained the discrepancy as follows. Telephone carriers charge TWLO a fee to access their customers – that fee is then passed along to customers. That access fee is typically higher for international customers. Thus TWLO reports revenues inclusive of that fee, leading to lower gross margins on messaging revenues. Management believes that gross profit per message is a more important metric – that has increased robustly since 2020.

2022 Investor Day

TWLO saw its non-GAAP operating loss widen from $8.2 million to $35.1 million, reflecting higher headcount in R&D and S&M.

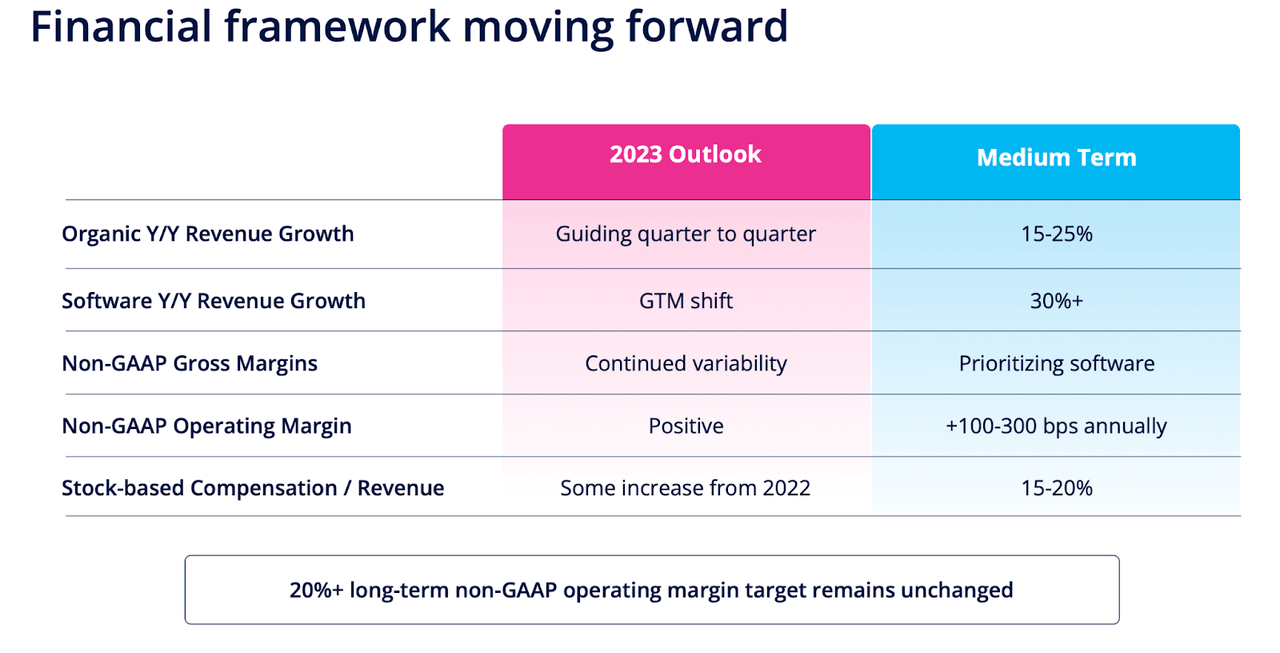

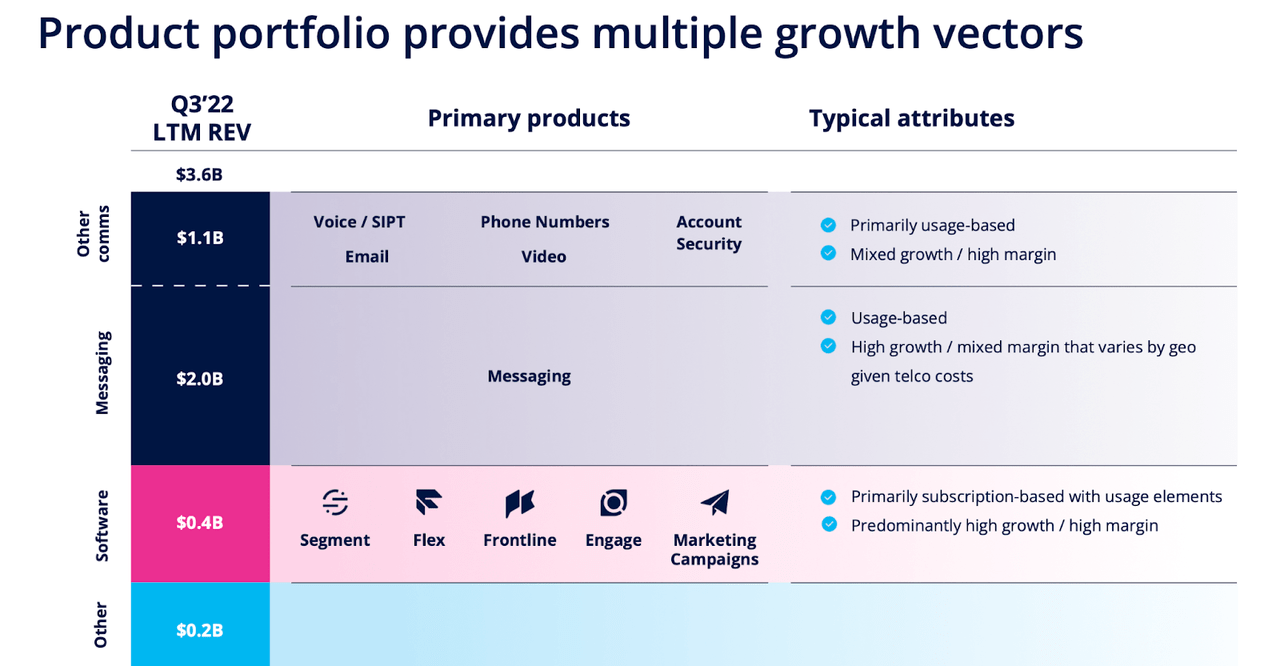

Looking ahead, TWLO guided for up to 19% revenue growth in the fourth quarter and $15 million in non-GAAP losses. That disappointing near term outlook was came with even more disappointing medium term outlook, as TWLO withdrew its previous 30+% guidance and instead issued guidance for 15% to 25% organic revenue growth over the medium term. That outlook comes as the company aims to switch from a primarily consumption-based pricing model to a subscription model. TWLO expects software revenues to grow rapidly at over 30%, but it will take time for software revenues to become a greater proportion of overall revenues.

2022 Q3 Presentation

On the call, management blamed “current macro headwinds” for the reduced outlook. That does seem to imply that an improving macro picture may lead to an acceleration in the medium term growth outlook, but management stopped short of directly implying that. The market had sold the heavily into the report, indicating that a reduction in guidance was already somewhat expected, but the stock’s plunge after releasing earnings indicated that the magnitude of that reduction in guidance came at a surprise.

TWLO ended the quarter with $987 million of debt vs $4.2 billion of cash (this is ignoring a $750 million equity investment in Syniverse). That $3.2 billion net cash position is worth around 38% of the current market cap. That strong balance sheet is all the more notable considering that management stated that they expect to deliver non-GAAP profitability starting next year.

Is TWLO Stock A Buy, Sell, or Hold?

The reduction in guidance was a poor development, but I’d argue that it was already priced into the stock heading into the report. TWLO is now trading at 5x gross profits and around 2.4x sales.

Seeking Alpha

With valuations – and expectations – effectively reset, I like the current setup for TWLO from here. Management has guided for long term 20% operating margins. Assuming 18% growth and a 1.5x price to earnings growth ratio (‘PEG ratio’), I see fair value at being around 5.4x sales, or $114 per share. Upside may be even more pronounced as growth returns and as the company executes on profitability targets (justifying higher multiples).

I continue to find TWLO as benefitting from secular growth drivers of improving communication with customers, known as Communication Platform as a Service (‘CPaas’). Companies are constantly looking for ways to connect with customers and drive greater sales conversion – TWLO’s products help satisfy those goals in a digital world.

2022 Q3 Presentation

With the stock so cheap, is management considering a share repurchase? Management stated the following regarding prospects for share repurchase program:

I think that for us, it’s been important to have a fortress balance sheet. That’s why we have the amount of cash that we do. I think certainly during economic down times; it’s good to be more cash rich than otherwise. That said, I think you’re right that as we become more profitable and as we start to generate free cash flow, you do have different directions that you can take that I think historically we’ve done M&A, but a share buyback is certainly not something I would take off the table either. It wouldn’t take signal from that, that’s something that we’re necessarily planning, but I think it’s got to be among a list of options.

While TWLO is not yet profitable on a GAAP basis, the large net cash position, modest cash burn, and commitment to non-GAAP profitability by next year help to greatly reduce the financial risk of the company. Couple that with a de-risked valuation and the stock looks highly compelling here.

What are the key risks? Just like how Meta Platforms (META) has been negatively affected by data privacy changes at Apple (AAPL), TWLO can be negatively affected if AAPL (or Alphabet (GOOGL) for that matter) change the way they identify spam for text messaging. TWLO also has a much lower gross margin than typical tech peers, with gross margin standing at 47% in the latest quarter. TWLO expects gross margins to improve over time, but the path to profitability (and high margins for that matter) may be more difficult here than at peers with higher gross margins. Unlike cloud-based enterprise tech companies, at which gross margins can naturally expand on increasing scale, TWLO may always have to share portions of revenue with telecom carriers. Besides those risks, however, I view TWLO as being a company benefiting from long term structural trends as customer communication goes digital. As discussed with subscribers to Best of Breed Growth Stocks, I view a carefully constructed portfolio of undervalued tech stocks as being the best way to take advantage of the tech stock crash. I continue to rate TWLO as being a strong buy and worthy of being a core holding in such a portfolio.

Be the first to comment