DoubleAnti/iStock via Getty Images

After the bell on Wednesday, we received fourth quarter results from customer engagement platform Twilio (NYSE:TWLO). Shares of the company soared in 2020 thanks to revenue growth that accelerated during the pandemic. The past two years have not been pretty, as growth has slowed tremendously, and Q4 results showed a number of similar patterns.

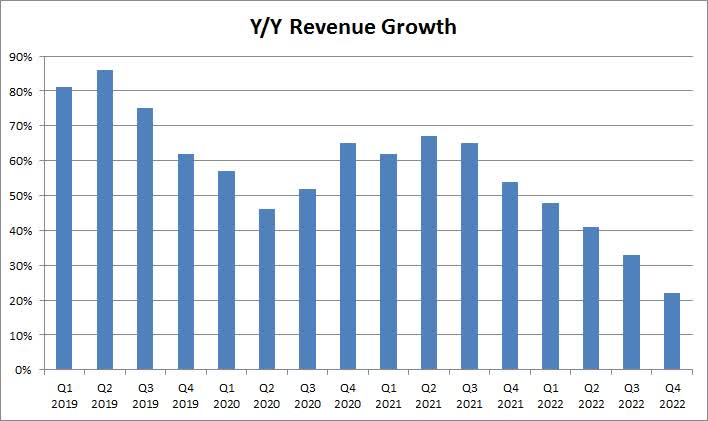

For the quarter, Twilio reported revenues of $1.025 billion. While this number beat street estimates for $1 billion, we must remember that expectations came down quite a bit. When the company gave guidance back in November, estimates were calling for $1.07 billion. This quarterly revenue number represented 22% growth over the prior-year period. While that figure seems nice, it’s the lowest percentage reported in a number of years, as seen below.

Twilio Revenue Growth (Company Earnings Reports)

The company seems to have a history of providing low guidance, so it can beat expectations in the end. In the past five years, the company has not missed street estimates for its top line, so maybe analysts need to do a little more work here. As a result of the big revenue beat, the 22-cent adjusted profit beat by 30 cents, and again, there has not been a miss anytime recently. Of course, the company still lost nearly $230 million on a GAAP basis, although that wasn’t nearly as bad as the $291 million loss a year earlier.

When it came to the quarterly metrics, the picture was quite mixed. Twilio added about 10,000 new active accounts in the period, which was the second-best quarter of the year. Customer growth still remains well off pandemic-era levels, with growth in the low teens percentage-wise, but this quarter was better than we’ve seen recently. The one area where things were not good was the dollar-based net expansion rate (“DBNRR”), which the company says “provides a more meaningful indication of the performance of the company’s efforts to increase revenue from existing customers”. As the chart below shows, the DBNRR crashed in Q4 by 12 percentage points, coming in at its lowest point in years.

Dollar-Based Net Retention Rate (Company Filings)

When it comes to guidance, Twilio again disappointed the street. Management is calling for revenues of $1 billion, plus or minus $5 million, which represents growth of 14% to 15%. However, the street was looking for an almost 17% increase, or around $1.02 billion. Bulls will likely say that the company is just being conservative as usual, but that crashing DBNRR does seem to increase uncertainty here a little bit. Even if the company comes in with better-than-expected results, the overall revenue growth rate is likely to again hit a new multi-year low.

One reason why investors might be pleased in the short term is that the company announced a $1 billion share repurchase plan. This buyback will expire at the end of 2024, and will primarily be used to offset the company’s large stock-based compensation. The Q4 diluted share count was up more than 6 million shares over the prior year period, and for the year Twilio reported nearly $800 million in stock-based compensation including restructuring. This key expense shouldn’t be as burdensome moving forward, however, as the company recently announced a 17% workforce reduction.

After the bell, shares surged by about 12% to $74 a share, despite these mixed results. A lot of times this earnings season, we’ve seen companies jump after so-so numbers just because these stocks have been beaten down so much in recent years. Since the last earnings report, the average price target on the street has come down from $120 to $75, which basically is where the stock is now. Twilio shares peaked at more than $435 in early 2021, at a time when analysts thought the name could be worth more than $500 a share. Investors are now celebrating being at a fraction of that level, having bounced considerably percentage-wise from their 52-week low of $41.

In the end, Twilio shares rallied after a mixed Q4 report. The company was able to beat meaningfully reduced estimates for the period, but the revenue growth rate continues to slow. Investors have cheered recent cost-cutting measures and the stock buyback, although guidance yet again was a bit below expectations. With the DBNRR falling, the next few quarters will be interesting to see if revenue growth can stabilize or collapse further towards the flat line. While shares are up in the after-hours session, they are basically right at the average price target on the street, and I don’t see too many analysts making major moves on today’s news.

Be the first to comment