jiefeng jiang

Investment Thesis

The undergoing semiconductor sector downturn, the ongoing geopolitical tensions, and the Chip wars between the US and China have crashed the industry’s valuation. However, the downturn has offered long-term investors the chance to buy companies that will dominate our increasingly digital world that become the “new oil”.

When Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) approached its bottom, I opened a position for Yiazou’s Model portfolio. I have no plans to sell anytime soon, and I remain bullish on TSM and the sector for the following 1-2 years.

Expanding Its US Fab Presence

TSMC is expanding its investments in Arizona significantly, adding a second Fab, focusing on N3 process technology (commencing production in 2026), in addition to the first Fab announced in 2020, which would ramp up N4 process production in 2024. TSMC expects the capital outlay for the two Fabs to reach $40 billion. In addition, the company has indicated that the total capacity of the two Fabs together could exceed 50,000 Wafer Starts Per Month (WSPM) when it is fully ramped.

In addition, TSMC is well positioned to build 10-15% of its leading-edge capacity from here on in the US as a result of demand from customers for geographical diversification. However, despite increased construction and operating costs for overseas expansion, margin dilution is likely to be manageable due to higher wafer prices, subsidies from different countries, and its stronger pricing power. Moreover, TSM’s commitment to long-term overseas expansion would ensure TSMC’s dominant market share in the leading-edge field and address some concerns regarding geopolitics.

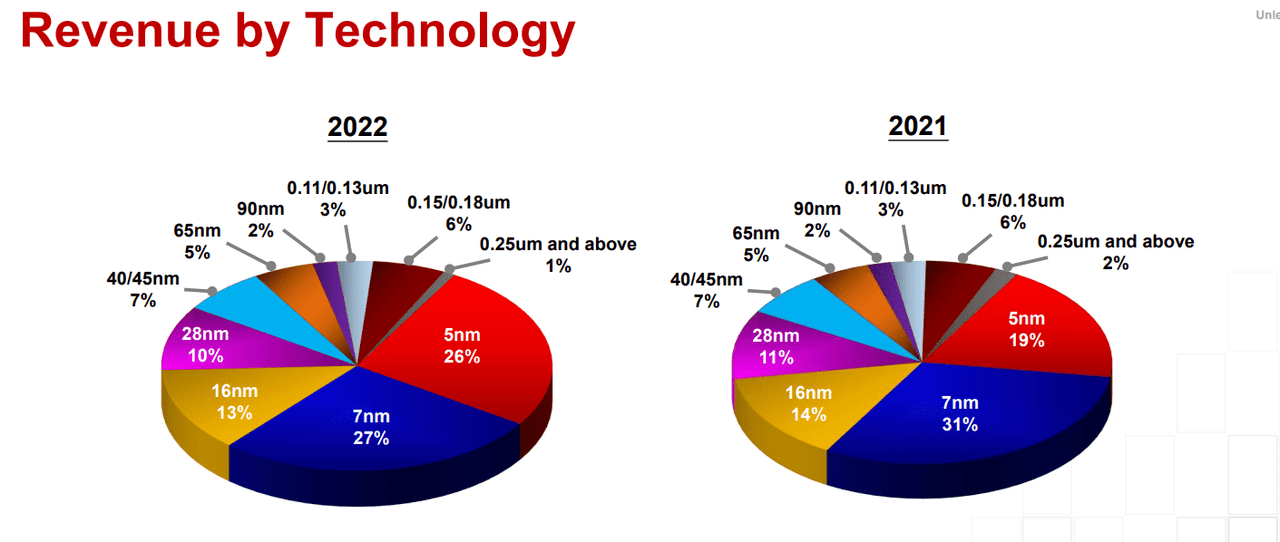

N5 Order Cuts Weigh In & Revenue Mix

Reports indicate that N5 utilizations will likely drop in 1Q23 and 2Q23 due to order cuts from Advanced Micro Devices, Inc. (AMD), NVIDIA Corporation (NVDA), Qualcomm Incorporated (QCOM), and Apple Inc. (AAPL). Favorably, QCOM has shifted its latest flagship 5G SoC (Snapdragon 8 Gen 2) to the TSMC N5 family (based on the N4 process node) starting from 2H22. However, due to a softer demand outlook for high-end smartphones (i.e., in developed markets such as Western Europe and the US) and disciplined inventory management, QCOM is likely to cut wafer starting at N5, resulting in lower N5 revenues in 1Q23.

In addition, NVDA and AMD have also pushed out N5 wafer-start in 4Q22/1Q23 due to ongoing weakness in gaming GPUs, inventory correction in the PC market, and a more conservative ramp for new HPC products (NVDA RTX40 gaming GPU, AMD Genoa) in 2023, leading to lower N5 revenues for TSM in 1Q23. Finally, with lukewarm demand, an improving supply-chain situation, and prudent inventory management, I expect Apple to cut upstream orders at TSMC N5/N4 in 1Q23 for iPhone, iPad, and MacBook processors, weighing on 2Q23 revenue momentum for TSMC.

TSMC’s Presentation (investor.tsmc.com)

Due to widespread order cuts at mature nodes, TSMC is unlikely to be completely immune to a semiconductor downturn and will see capacity slack at mature nodes (similar to other mature Foundries like UMC, VIS, SMIC, etc.). As a result, I expect N7 revenue to drop in 2023 due to smartphone/PC inventory correction and a slower-than-expected process node migration amidst a semi-market downturn.

However, in 2024, as inventory destocking completes, successive waves of applications (AMD I/O chiplet, RF transceiver, TV SoC, WiFi 7, SSD controllers, etc.) will drive N7 demand. TSM’s design activities are increasing at the N3 family, led by the rising number of new tape-outs and shuttles (Multi Project Wafer) from various leading-edge customers. Notably, TSMC also indicated the number of new tape-out at the N3 family is more than 2x that of N5 during the first year of the ramp.

www.anandtech.com/show/17452/tsmc-readies-five-3nm-process-technologies-with-finflex

Many smartphones and HPC customers continue their partnerships with TSMC to execute their future product roadmap, including Apple, QCOM, MediaTek, AMD, Intel, NVDA, multiple AI start-ups, Autonomous Driving processors, etc. Thus, I expect TSMC to maintain its technology leadership with a dominant market share in N3, supported by its more compatible design rule (due to no change for transistor structure, still FinFET), stronger Open Innovation Platform ecosystem (OIP), stronger power, performance, and area (PPA) and higher production yields.

It is reasonable to assume that TSMC will remain the sole supplier for key clients (Apple, AMD, MediaTek) and capture dominant shares in the swing customers (NVDA, QCOM) in 2024 and beyond. In addition, the growing demand for in-house silicon from hyper scalers (Amazon (AMZN) Graviton) will be a strong growth driver for the N3 family.

Furthermore, rising Automated Driving demand is also creating more demand for ADAS and Full Self Drive chip tape-outs from Tesla (TSLA), NVDA, STMicro (Mobileye), NXP, Renesas, etc. Last but not least, TSMC’s N3 platform should become a key enabler for AI start-ups targeting HPC applications.

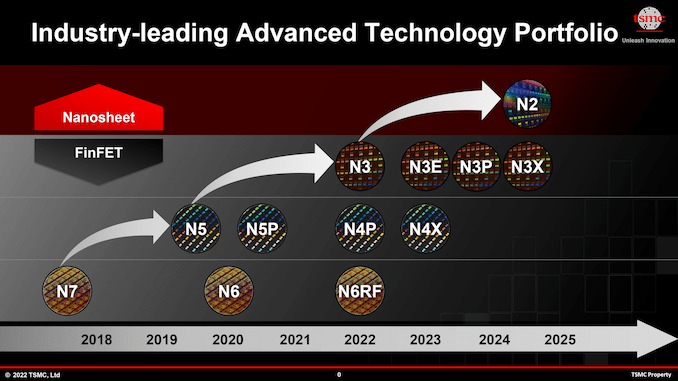

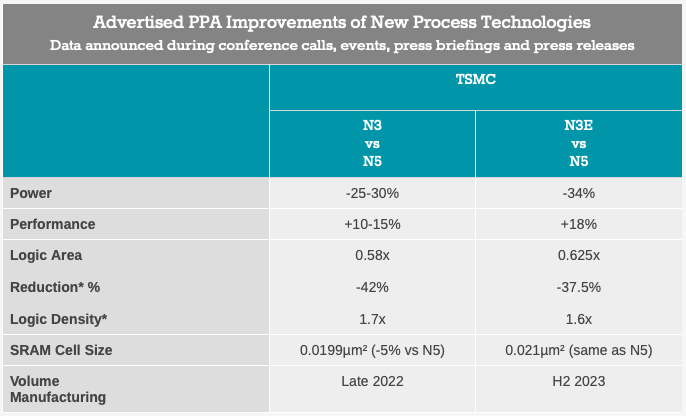

N3E Is Coming In 2H23

TSMC commenced N3 mass production, in December 2022, according to the company, but the meaningful ramp-up will be in 2H23E when the optimized version, N3E, is ready. N3E, characterized by 19 EUV layers in total, or six fewer than the generic N3, promises more straightforward process complexity, intrinsic cost, and manufacturing cycle time, albeit having less density gain. In addition, single-patterning EUV will be applied to the critical layers fabbed on N3E instead of the multiple-patterning approach in N3.

TSMC will also introduce FinFLEX technology from N3E onward to give customers the flexibility to design the fin types (3-2 for maximum speed, 2-2 for a good balance of PPA benefits, 2-1 for maximum density) and tailor the attribute PPA that they care the most about for each of the critical functional blocks on the same die with the same design toolset, rendering some moat against the competition.

www.anandtech.com

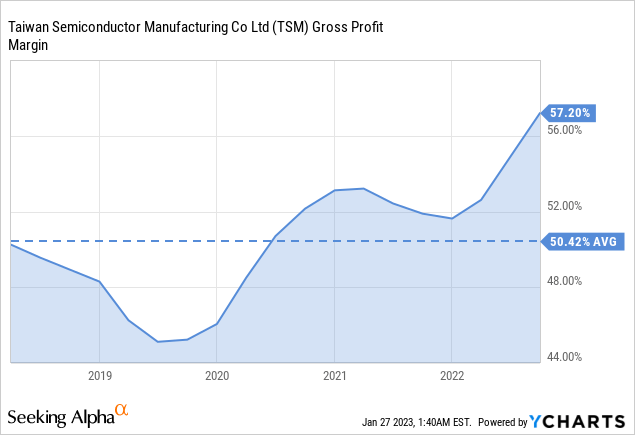

Pricing Power Will Support Margins

During the earnings call, management remained confident about its near-term and long-term Gross profit margin (GM) outlook. Notably, TSMC reiterated a long-term GM outlook of 53+%. Also, TSMC expects to maintain GMs at or above 53% even in 2023 amidst the industry downturn, indicating at least ~700 bps GM uptick compared to the last downturn (2019).

TSMC has continued to expand its structural GM over the last few years, led by stronger pricing power, continued cost improvement, and improved manufacturing efficiency. Not surprisingly, TSMC’s pricing power is derived from its higher production yields, stronger technology leadership, the healthier competitive landscape at leading-edge, and its broader specialty technology portfolio.

Therefore, I think TSMC can easily maintain 53+% GM throughout the downturn in 2023. Looking ahead, TSMC GMs have now moved to a new and higher range and expect it to rebound to 55-56% in 2024, entering the industry upturn.

Confidence For A Recovery In 2H23

TSMC pointed out that semi-inventory peaked in 3Q22, reduced in 4Q22, and will further move down throughout 1H23. Management expects inventory to be back to normal levels exiting 2Q23. Thus, with the semi-inventory situation improving, new products ramping up (N3 led by ApAAI), and ramping new HPC and AI design, TSMC expects 2H23 revenue to rebound swiftly, driving revenue in 2023 slightly higher.

Although 2H23 recovery may be slower than expected, investors are likely to look beyond it, given that 2023 revenue growth/earnings expectations have now been partially reset. Into 2H23, the market focus will likely shift to the recovery in 2024. I expect TSMC revenue to grow above trend, driven by a strong N3 design pipeline from many leading-edge customers, leading market share in N3, and cyclical rebound in N7.

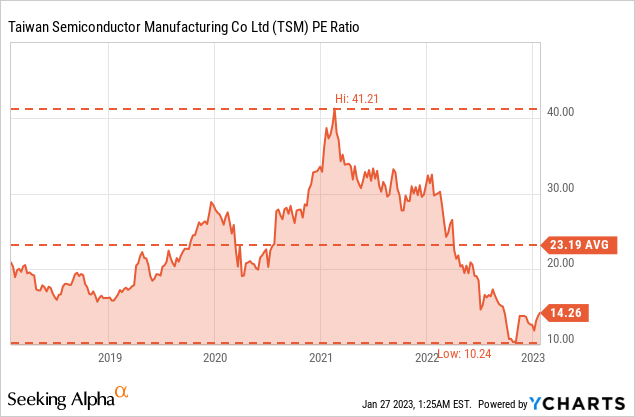

Still Room For Higher Multiples

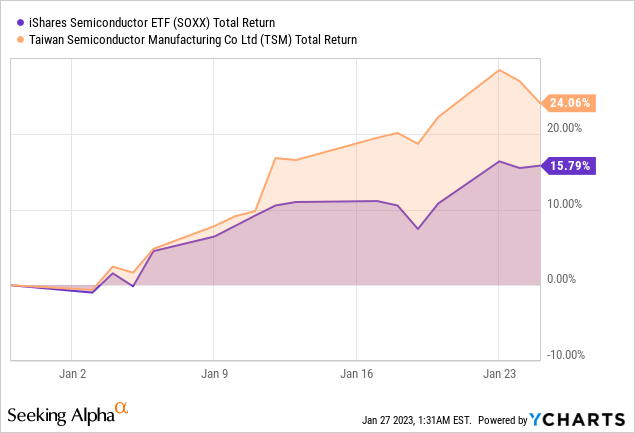

The cyclical nature of the semiconductor industry caused investors to be more cautious in valuing companies in the sector, and TSM is no exception. However, the company’s investments in advanced technologies and capacity expansion could lead to higher future growth, which is not fully reflected in its P/E ratio yet. Despite the strong 25% bull run in the stock last month, TSM still trades at historically low levels. Considering the semi’s potential recovery in the year’s second half, TSM has substantial upside potential.

Conclusion

Undoubtedly, TSM should maintain its market-leading position while capitalizing on the industry’s growth. The company’s higher production yields, stronger technology leadership, a healthier competitive landscape at the leading edge, and broader specialty technology portfolio will support its economic moat, dominance, and growth in the market.

Be the first to comment