porcorex/iStock via Getty Images

All values are in CAD unless noted otherwise.

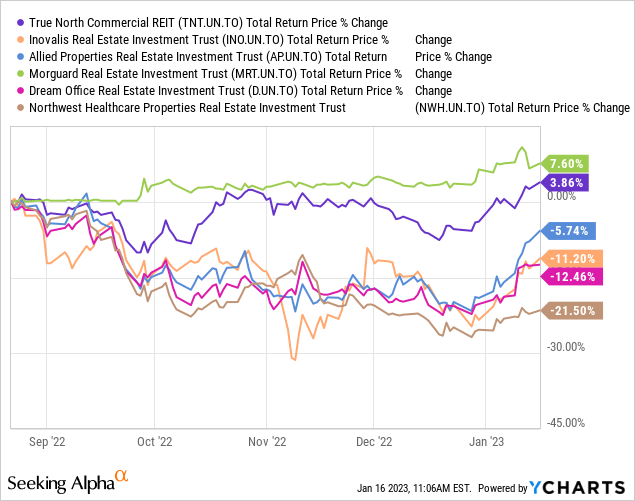

We mentioned True North Commercial REIT (TSX:TNT.UN:CA) in a recent piece focusing on Allied Properties Real Estate Investment Trust (OTCMKTS: APYRF)(TSX: AP.UN:CA). That prompted us to revisit this anomalous office REIT that trades at a premium to its published NAV. While majority of True North’s portfolio is in Ontario, it has properties in British Columbia, Alberta, New Brunswick and Nova Scotia too.

Q3-2022 Presentation

To recap our previous coverage on this REIT, we were impressed by the management, its higher occupancy levels compared to its peers, and superior returns in an era where the office space is being cold shouldered. It maintained its dividend during challenging times and its high yield made it the darling of the income investor. It continues to lead most of its peers since that article.

We had given it a pass back in August 2022 as we felt that the high payout and interest rate, competition, and lease renewals would make for challenging times ahead. We gave this one a high probability of a dividend cut within the year.

We think this probability will increase over time unless we see a rather abrupt change in office market fundamentals. Keep in mind that managers can defer and delay this decision, sometimes more than they should. Look at how bad things got for Inovalis in Q4-2021 (198% payout ratio???) and they cut after Q2-2022.

we think True North will likely take appropriate steps before things get too bad and help preserve value in the REIT. We are giving this a “hold” rating despite the challenges, as the management has earned some latitude for its good performance.

Source: True North Commercial REIT: Are We Going The Way Of Inovalis

Today, we go over most recently published financial numbers in a bid to provide our readers with an updated thesis.

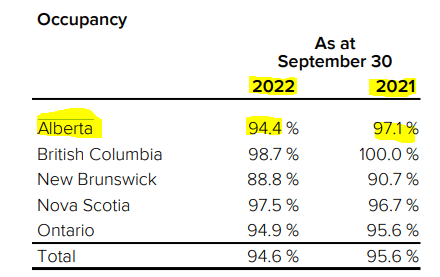

Occupancy

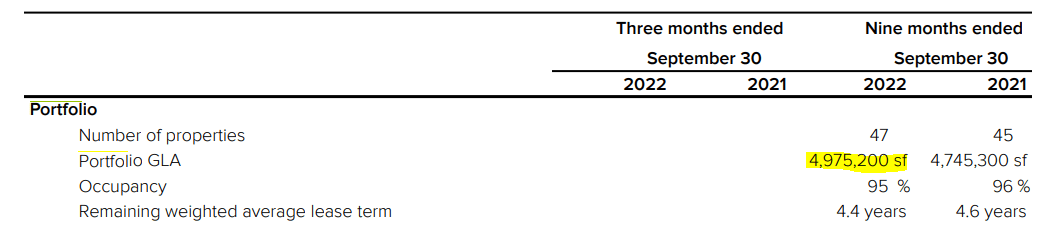

The crux of the issue for True North remains its declining occupancy levels. So far the effect has been very gradual. At year end 2020, the occupancy levels were at a ridiculously high 98%. As we get to the end of 2022, we are seeing the slow impact as leases come up for renewals. In the most recent quarter we saw yet another 1% drop.

Portfolio occupancy declined 1% to 95% when compared to Q2-2022. Occupancy was negatively impacted due to the early surrender of 25,800 square feet of upcoming vacancy to allow the releasing of the space.

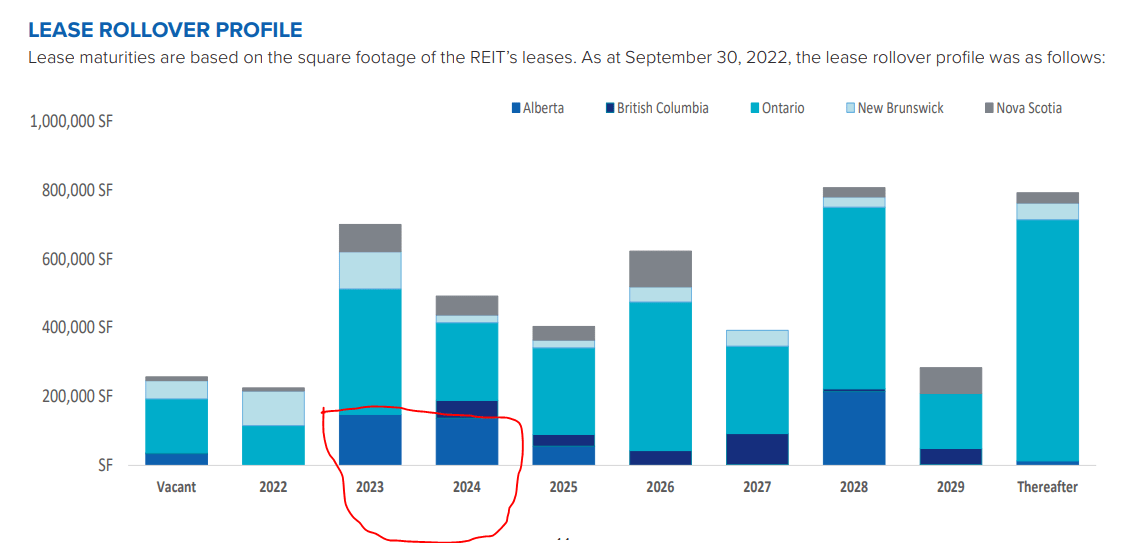

This is just the pregame warm up. In 2023 and 2024, we have about 1.2 million square feet coming up for renewals.

True North Q3-2022 Results

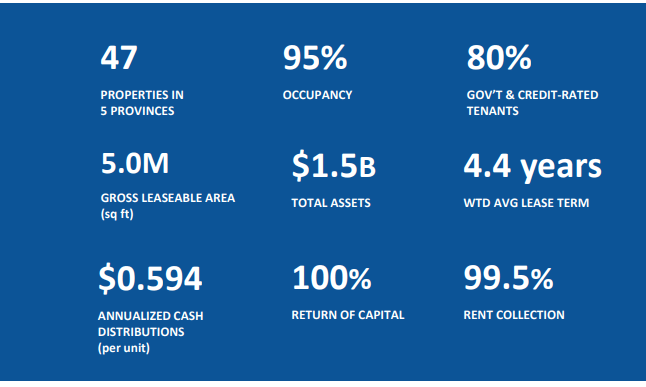

True North’s total portfolio size is a shade under 5 million square feet.

True North Q3-2022 Results

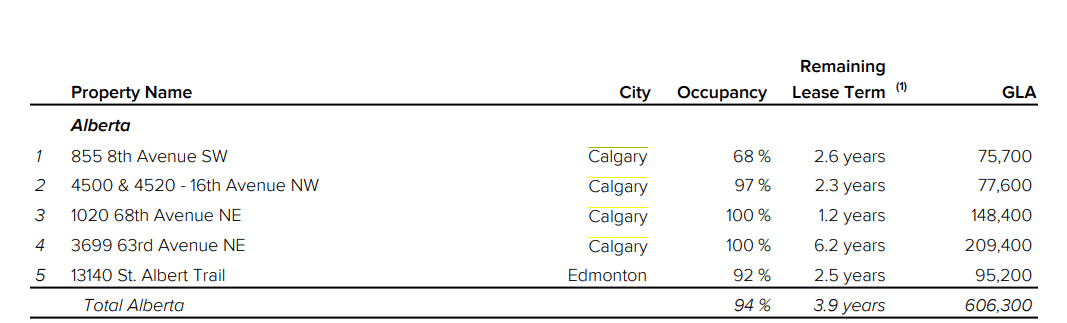

So 25% is coming up for renewal in the next 24 months, including large portions in Alberta. So far, Alberta occupancy has dropped the hardest amongst the provinces in True North’s portfolio.

True North Q3-2022 Results

We are going to bet dollars to doughnuts here that we will see an “8” handle on that occupancy number in 2 years. True North’s Alberta portfolio is concentrated in Calgary with very average short leases.

True North Q3-2022 Results

Calgary’s office vacancy rates are on another planet relative to where the portfolio stands.

Calgary downtown office activity picked up, with vacancy down 80 basis points to 32.9% and overall market vacancy decreasing to 29.7% from 30.3%.

Source: True North Q3-2022 Results

You can bet that True North’s Alberta occupancy levels will converge with that of Calgary, and /or its renewal rates will take a steep fall.

Interest Rates Beginning To Chew In

Alongside the extremely short leases, True North also has a rather short debt maturity profile.

True North Q3-2022 Results

During 2022 that short debt maturity profile got even shorter as extensions did not keep pace with time dropping off. Despite that, the weighted average rate has climbed higher. Keep that 3.46% in mind as you look at what the Q3-2022 and beyond renewal rates have been.

As at September 30, 2022, the REIT’s mortgage portfolio carried a weighted average maturity of 3.31 years and a weighted average fixed interest rate of 3.46%. During the quarter, the REIT refinanced a total of $51,250 (YTD-2022 – $82,820) of mortgages with a weighted average fixed interest rate of 4.68% (YTD-2022 – 4.16%) for one to five year terms (YTD-2022 – one to seven year terms), providing the REIT with additional liquidity of approximately $15,000 (YTD-2022 – $20,600). Subsequent to quarter end, the REIT refinanced $23,800 of mortgages with a weighted average fixed interest rate of 5.32% for a five year term, providing the REIT with additional liquidity of approximately $5,500.

Source: True North Q3-2022 Results

If we assume that only interest rates move to even 4.68% over time on True North’s entire debt, Q3 funds from operations would drop by about 20%. That is independent of any occupancy drop cited in reason 1.

Dividend Is Not Really Covered, Even Today

The headline numbers include lease termination fees.

While occupancy has decreased in the REIT’s Ontario portfolio, Same Property NOI increased by 10.6% mainly due to termination fees. Termination fees relate to a tenant in the REIT’s GTA portfolio that is downsizing a portion of their space effective December 2022, of which approximately 28% has been contractually re-leased. Excluding termination fees, Q3-2022 Same Property NOI decreased 2.8% and 2.1% YTD-2022.

Excluding termination fees, Q3-2022 FFO and AFFO basic and diluted per Unit would be $0.13 and YTD-2022 FFO and AFFO basic and diluted per Unit would be $0.40. Q3-2022 AFFO basic and diluted payout ratio would be 113% and YTD-2022 AFFO basic and diluted payout ratio would be 112%.

Source: True North Q3-2022 Results

In the absence of those payout ratios already look quite horrible.

Timeline

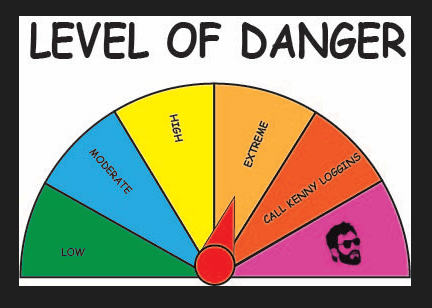

At present the overpayment is modest and of course the lease termination fees have helped bridge the hole. There is no definite urgency here so we would not expect an immediate cut. The more probable outcome is in the middle of 2023 as all these factors take on more weight. Our base case is that by end of 2023, payout ratio excluding termination fees will reach well over 125%, if the dividend is kept constant. Rationally, one would not expect things to get that bad before the dividend is cut, so we think end of 2023, beginning of 2024 would be the latest we would expect to see it. Based on all the information we have looked at, True North has a “Extreme” level of danger of a dividend cut on our proprietary Kenny Loggins Scale.

Trapping Value

This rating signifies a 50-75% probability of a dividend cut in the next 12 months.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment