tdub303

Thesis

Tri-Continental (NYSE:TY) is an equities CEF. The fund targets long term capital growth and current income by constructing a portfolio similar to the S&P 500. The CEF falls in the Large Cap / Value Morningstar box though, by being underweight Technology when compared to the index. Furthermore, the fund is overweight Energy when compared to the S&P 500, with Exxon featuring in its top holdings.

The CEF extracts dividends from the S&P 500 returns, and when looking at its total return graph we can see it has mirrored the index quite nicely in the past year. Long term (10-year lookback) the CEF has a performance in line with other golden standard index funds, namely GAM and ADX. They all underperform the index, however. TY has done what it is supposed to in the past year, and in our view is set to outperform in the near future, our view being that Value names are going to overtake Growth going forward. Prior market leaders are never the same ones going forward, and in our mind, higher rates for longer are going to translate into Value outperforming Growth.

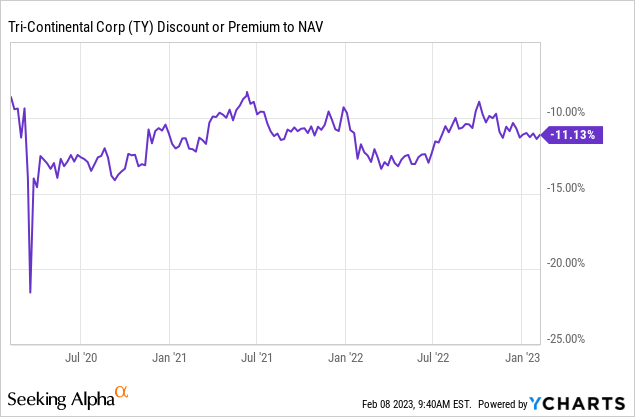

TY CEF is trading at a discount to NAV, but it has done so for many years. The fund’s discount to net asset value has a very low beta to market conditions, due to the ‘tried and tested’ nature of this CEF. Do not expect massive widenings in the discount here, nor substantial tightening moves. There is nothing overly exciting about this CEF. It does what it is supposed to – extract dividends from the S&P 500 and has performed in line with expectations.

Performance

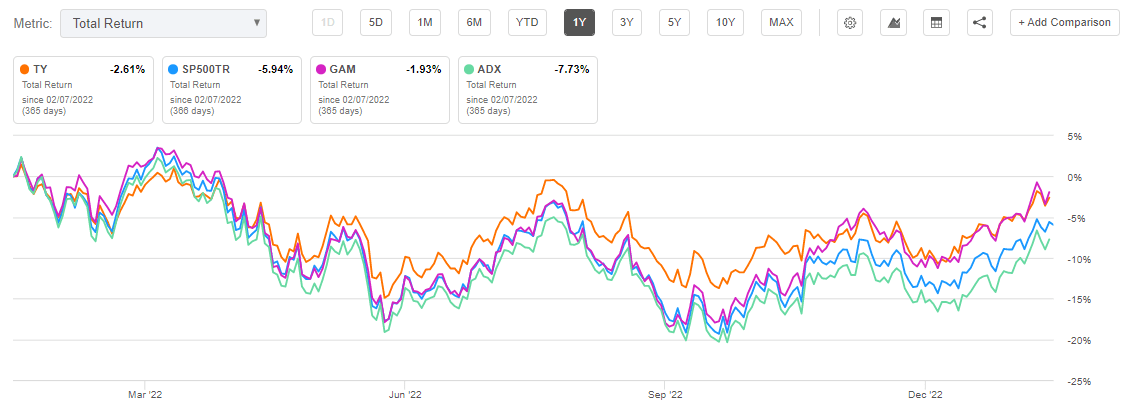

From a total return perspective, the CEF has nicely mirrored the S&P 500 return in the past year:

Total Return (Seeking Alpha)

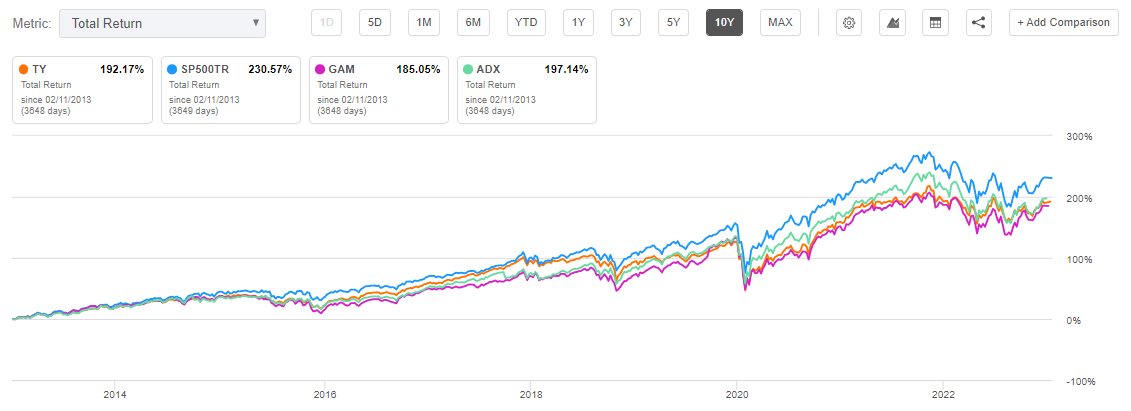

We can actually see from the above graph a slight outperformance by TY when compared to the index. Longer term the fund slightly lags the index, but performs in line with other S&P 500 CEFs:

Total Return (Seeking Alpha)

We can see the CEF equity cohort composed of TY, GAM, and ADX having a very similar performance when a very long lookback is put into place. This drives home the point that investors who want to be exposed to equities but do not need the dividends, are most likely better off by investing in the index outright than choosing the CEF structure. Again, this is a structural issue and involves enjoying capital gains and ancillary taxation better than the annual dividend income and related implications.

Holdings

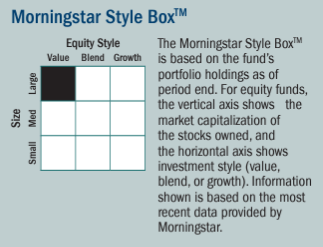

The fund falls in the Large Cap / Value Morningstar box:

TY Value Box (Fund Fact Sheet)

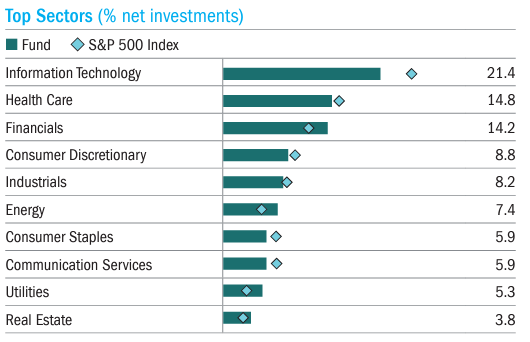

The above denomination is due to the fund’s composition, which is underweight technology when compared to the index, namely the S&P 500:

Sectors (Fund Fact Sheet)

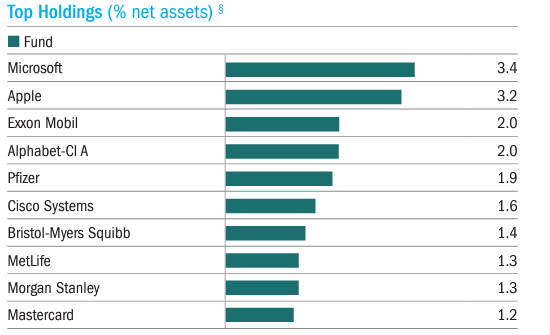

We can see the CEF being underweight IT when compared to the index, but overweight Financials, Energy and Utilities. That is a nice balance to have. To that end, its top holdings now include one of the Oil & Gas majors, namely Exxon (XOM):

Top Holdings (Fund Fact Sheet)

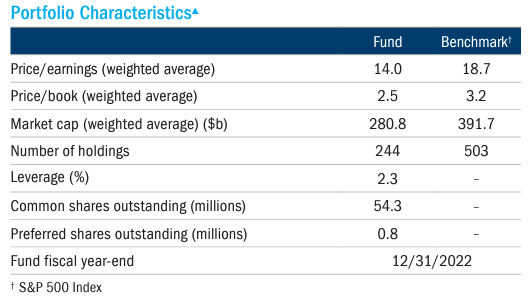

The fund tries to create alpha by choosing companies that have lower starting valuation points when compared to the wider index:

Portfolio Characteristics (Fund Fact Sheet)

Premium/Discount to NAV

Given its track record and history, the fund trades in a very tight discount to NAV window:

The past year has been no different, with very small divergences in the structure’s discount to NAV. Do not expect big jumps here that can be taken advantage of via trading decisions. The fund has been around for a long time and has a very clear cut mandate. There will not be big gap downs here in the discount. Expect more of the same.

Conclusion

TY is an equities CEF. The fund falls in the CEF category that extracts dividends from the S&P 500 returns. Simply put, investors who look for current income rather than capital gains from the index are better off investing in the likes of TY, GAM or ADX. TY does what it is supposed to and has posted a total return in the past year that has mirrored the S&P 500. The CEF has a Value tilt, being overweight Financials and Energy while underweight Technology when compared to the Index. In our mind this is a correct positioning, with Value set to outperform Growth going forward. In our view, higher rates for longer are going to translate into Value stocks outperforming. TY has a very sticky discount to NAV that does not change much. Do not try to trade a narrowing of the discount since it just does not happen. TY is a Hold and appropriate for those retail investors who are looking to extract quarterly coupons from the S&P 500 rather than target capital gains.

Be the first to comment