Mohammed Haneefa Nizamudeen

Investment Overview

Travere Therapeutics, Inc. (NASDAQ:TVTX) – a $1.4bn market cap (at the time of writing) commercial stage, San Diego-headquartered biotech – ought to be on investors’ watchlists ahead of a pivotal upcoming Prescription Drug User Fee Act (“PDUFA”) date on Feb 17th for its lead clinical asset Sparsentan.

Travere has guided for revenues of ~$212m in FY22 from its commercialized assets Thiola and Thiola EC – FDA-approved for the treatment of cystinuria – a rare genetic cystine transport disorder that causes the formation of recurring kidney stones, and Chenodal and Cholbam – approved for gallstone and bile acid disorders, respectively – but revenues from these sources are falling in the case of the former owing to generic competition, and flat in the case of the latter, as we can see below.

Travere revenues to Q322 – tipronin and bile acid products (Q322 10Q submission)

Travere reported a net loss of $213m across the 9m to Q322, or $(3.34) per share, and current assets of $534m. Across the same period, the company spent $176m on R&D, versus $157m on SG&A, so it is clear that Travere’s priority is its pipeline, as opposed to its commercialized product portfolio.

Sparsentan is a Dual Endothelin Angiotensin Receptor Antagonist (DEARA) indicated for the treatment of Immunoglobulin A nephropathy (“IgAN”) and Focal segmental glomerulosclerosis (“FSGS”), and the upcoming PDUFA date – the date by which the Food and Drug Agency promises to rule on whether a New Drug Application (“NDA”) submitted to it by a drug developer will be approved for commercial use – is in relation to IgAN.

In its 10Q Travere, writes about Sparsentan:

Pre-clinical data have shown that blockade of both endothelin type A and angiotensin II type 1 pathways in forms of rare chronic kidney disease, reduces proteinuria, protects podocytes and prevents glomerulosclerosis and mesangial cell proliferation

Sparsentan has been granted Orphan Drug status for both IgAN and FSGS in the U.S. and EU, and Travere submitted for an accelerated approval of the drug to the FDA in March. The original PDUFA date was scheduled for November 17th, 2022, but prior to that date the FDA requested that Travere:

expand our proposed REMS to include liver monitoring, consistent with certain other approved products in the endothelin receptor antagonist class.

REMS stands for Risk Evaluation and Mitigation Strategies, and although the 3-month delay of the PDUFA date must have been frustrating for Travere, the company is now expectant that it will receive an accelerated approval next month, based on interim data from its pivotal 404 patient PROTECT study in IgAN relating to the endpoint of reduction in proteinuria. The data showed that Sparsentan:

demonstrated a greater than 3x reduction of proteinuria from baseline after 36 weeks of treatment, compared to the active control irbesartan

Sparsentan achieved a 49.8% reduction, versus irbesartan’s 15.1%, which meets the study’s requirement to “detect a 30% difference in the geometric mean ratio (“GMR”) of proteinuria reduction between sparsentan and irbesartan.”

Later this year – around Q323 – Travere will present more data from the PROTECT study. This time, it will be based on an estimated glomerular filtration rate (eGFR) endpoint; preliminary eGFR data is “believed to be indicative of a potential clinically meaningful treatment effect,” according to a Travere corporate presentation.

Should that prove to be the case when the full data set is available, Travere plans to submit for a full approval of Sparsentan in IgAN, and potentially a conditional approval in Europe, where it has struck a deal with kidney disease specialist Vifor Pharma, who will commercialize the drug in Europe – and potentially Australia and New Zealand also – with up to $845m milestone and upfront payments on the table, plus “tiered double digit royalties up to 40% on net sales of Sparsentan.”

By mid-2023, Travere also expects to have 2-year topline data from its DUPLEX study of Sparsentan in FSGS, which, if positive, will allow the company to file a supplementary NDA (“sNDA”) for approval in that indication also, which would likely happen sometime in 2024.

Sparsentan projected approval pathway (Travere presentation)

Analysts have suggested that Sparsentan could achieve peak sales of ~$1.4bn in IgAN alone, which is a higher figure than Travere’s current market cap, suggesting that the company’s share price – which has hit highs of >$30 in December 2021, and as recently as April last year – could reach new heights if the FDA’s decides to grant Sparsentan accelerated approval next month.

On the other hand, if the FDA declines to approve Sparsentan, although Travere will still have its commercialized assets, plus a label expansion opportunity for Chenodal as a therapy for Cerebrotendinous Xanthomatosis (“CTX”), and a second pipeline asset in Pegtibatinase, indicated for classical homocystinuria (“HCU”) and progressing through Phase 2 studies. These are small markets, and the share price outlook for a loss-making company with peak revenue potential of not much more than $250m per annum will be a negative one.

As such, although Travere could earn a second shot at approval for Sparsentan in IgAN with its eGFR data layer this year, the February decision looks to be a critical moment in Travere’s development as a company.

In this note, I’ll attempt to provide more context around the data, market opportunity, likely FDA decision, and a target share price in a best and worst case scenario.

Data – Will Travere’s Study Results Meet FDA Expectations?

According to a statement in Travere’s 2021 10K submission:

In December 2021, the FDA approved Calliditas’ budesonide delayed release capsules to reduce proteinuria in adults with primary IgAN at risk of rapid disease progression, generally at urine protein-to-creatinine ratio (UPCR) ≥1.5 g/g. Although there are currently no pharmacological treatments approved by the EMA for IgAN in Europe (or the UK), public sources indicate that Calliditas (along with EU/UK licensee, Stada Arzneimittel) submitted their MAA dossier for budesonide delayed release capsules in 2021.

Based on public sources, AstraZeneca (AZN) (Alexion Pharmaceuticals), Alnylam Pharmaceuticals (ALNY), Arrowhead Pharmaceuticals (ARWR), BioCryst Pharmaceuticals (BCRX), Calliditas Therapeutics (CALT) / Stada / Everest, Chinook Therapeutics (KDNY) / SanReno Therapeutics, DiaMedica Therapeutics (DMAC), Eledon Pharmaceuticals (ELDN), Ionis Pharmaceuticals (IONS) / Roche (OTCQX:RHHBY), MorphoSys (MOR), Novartis (NVS), Omeros Corporation (OMER), Otsuka (Visterra), Reata Pharmaceuticals (RETA), RemeGen, Takeda Pharmaceutical (TAK), and Vera Therapeutics (VERA) may have programs in clinical development for the treatment of IgAN.

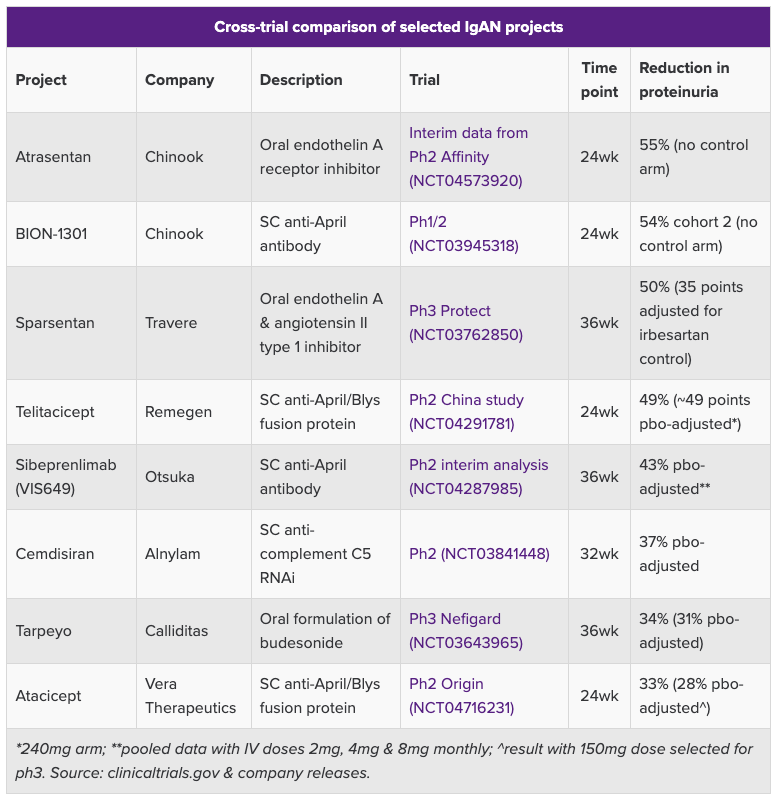

It is a long list, although comparisons of trial data to date – with the caveat that comparing rival biotech’s studies is not always a good idea, due to differences in design, study population, etc. – appear to suggest Travere is close to best-in-class.

Comparison of IgAN study data (Evaluate Pharma)

Additionally, Sparsentan has advanced further in the clinic than most of its rivals, meaning that, if approved, and along with Calliditas, Travere ought to have a significant first mover advantage.

Another plus is that Calliditas’ Tarpeyo was approved based on a “statistically significant” 34% reduction in proteinuria from baseline vs. 5% with renin angiotensin system inhibitors (“RASi”) – the current standard of care treatment in IgAN – which suggests that Sparsentan’s data ought to be sufficient to win accelerated approval.

Sparsentan’s Achilles Heel could be its safety profile, however, based on the FDA’s request for more REMS data, specifically with regard to liver toxicity, and Travere’s own admission, in a press release discussing the 3-month delay, that:

The Company faces the risk that the Phase 3 PROTECT Study of sparsentan in IgAN will not demonstrate that sparsentan is safe or effective or serve as the basis for accelerated approval of sparsentan as planned.

Sparsentan itself has not been specifically associated with any liver toxicity related risks in its clinical studies, but the endothelin receptor antagonist (“ERA”) class of drugs has been, notably Pfizer’s (PFE) Sitaxsentan – indicated for Pulmonary Arterial Hypertension (“PAH”) and pulled from the market in 2010, and Johnson & Johnson’s (JNJ) Bosentan – marketed and sold as Tracleer and also indicated for PAH – which is known to be hepatotoxic.

On a more positive note, JNJ’s Opsumit, another PAH therapy and an ERA, earned $1.8bn of revenues in 2021, despite carrying a warning about hepatotoxicity.

It could be the case that the FDA is simply showing an abundance of caution, although where liver disease is concerned the list of companies that have come so close to approvals only to be denied by safety issues includes companies such as Akebia Therapeutics (AKBA), FibroGen (FGEN), and Ardelyx (ARDX) – all 3 companies have suffered devastating share price losses.

It should be noted that these companies drug candidates’ targeted Chronic Kidney Disease as opposed to IgAN or FSGS. Nevertheless, when it comes to kidney disease, as an investor I would advocate extreme caution, even when an approval shot appears to be a formality.

With Travere’s pivotal PROTECT study having enrolled 404 patients, and the pivotal FSGS DUPLEX study having enrolled 371 patients, with no major safety concerns flagged to date, it’s hard to see the approval push being derailed on safety grounds, although Travere is still collecting data from the trial and it would not necessarily be surprising to me if the FDA opted to wait for the eGFR readouts as opposed to granting accelerated approval.

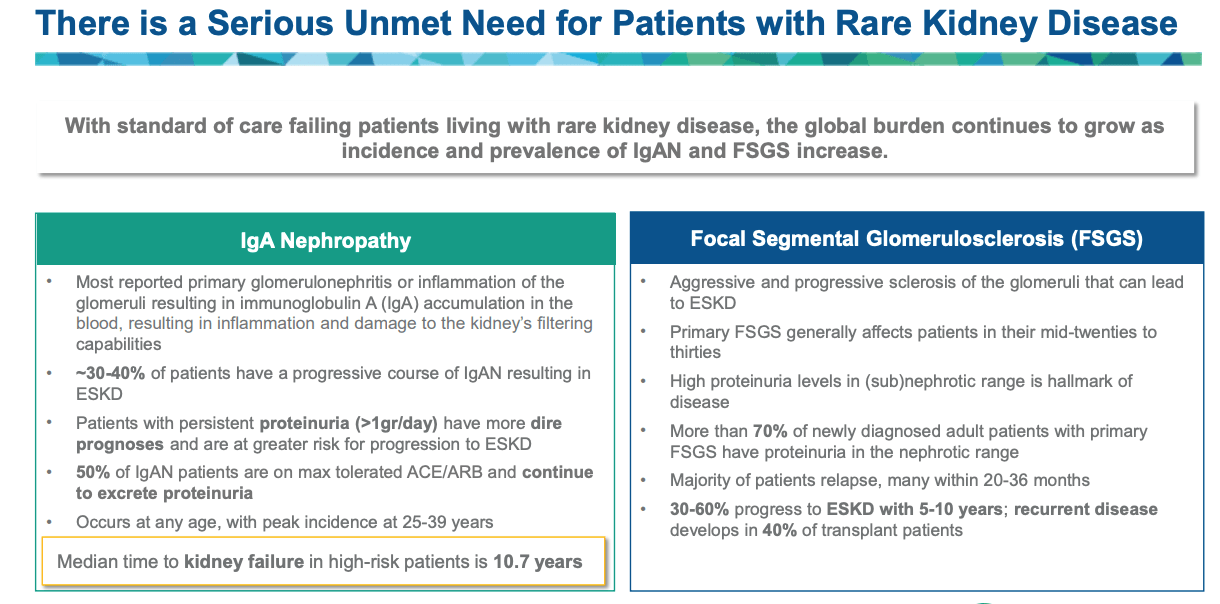

Market Opportunity – IgAN > FSGS – Unmet Need High In Both Indications

rare kidney disease – unmet need (Travere presentation)

Based on the above, it seems fair to say that the unmet medical need in both IgAN and FSGS is high – which perhaps explains why there are so many Pharmas and biotechs developing drugs for this indication. Travere management, after surveying nephrologists, concluded that only 8% of FSGS, and 19% of IgAN patients are optimally managed.

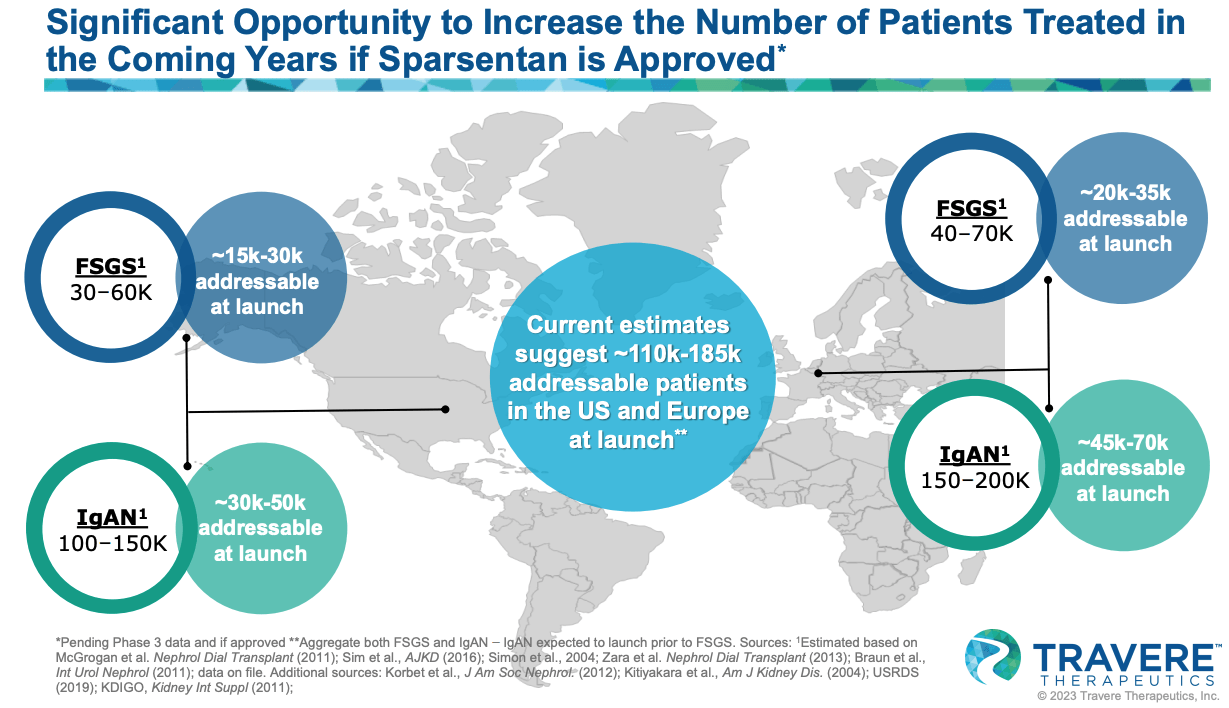

market opportunity in IgAN and FSGS (Travere presentation)

As we can see above, Travere rates IgAN as the larger opportunity, with 30-50k patients to be initially targeted at launch in Europe, and 45 – 70k in Europe.

Analysts have suggested that Tarpeyo sales could peak at ~$900m in 2028, and the drug costs ~$170k per annum, so the peak sales figure seems to imply a target patient population of ~5k patients. Conversely, multiplying 125k patients – the midpoint of Travere’s total estimated IgAN population – by $170k results in a market opportunity of >$20bn.

Rebates, reimbursement, and complex drug pricing regulations means that we can likely reduce that figure by at least half, and for Sparsentan alone we should probably reduce that figure by 75% since the drug – if approved – will compete against Tarpeyo and quite possibly Chinook’s BION-1301 and Novartis’ (NVS) oral complement factor B inhibitor Iptacopan – both of these drugs will post pivotal Phase 3 data in 2023.

Ultimately, even a 25% market share may be too high an assumption – and certainly not achievable in the short term – sales of Tarpeyo, for example, were just $12.1m in Q322. This may also indicate a reluctance on the part of physicians to prescribe a drug with accelerated approval and no confirmatory data to establish if Tarpeyo slows kidney function decline.

In other words, Travere may have more to lose than to win when it comes to February’s decision. If the drug is rejected on safety grounds – the most likely rationale for rejection – it will likely struggle to secure full approval, opening up the larger market, even if eGFR data is positive. If Sparsentan is approved in February, it will still need to deliver on eGFR if it is to fulfil analysts’ peak sales expectations.

Some analysts are more skeptical about Sparsentan’s approval chances in FSGS than IgAN – although the available data for FSGS is less mature, the drug has been able to show slower decline in eGFR vs “natural history” estimates, and “sustained reductions in proteinuria.”

Conclusion – A Decisive Day In Travere’s Development That Will Dictate Future Performance Of Share Price For Years

We can look at 3 different scenarios for Travere as follows. An FDA rejection of Sparsentan next month would result in a very gloomy prognosis. If the rejection were on safety grounds, then it could be the case that Sparsentan is a busted flush, and will not make it to market.

As discussed, Travere would have a realistic long term revenue potential of <$250m per annum based on the remainder of its portfolio, and a significant downward correction in the share price would be the only viable outcome. I could see the company’s share price falling by as much as 50%, giving the company a valuation of ~$700m, a little less than 3x my forecast peak revenue opportunity of $250m per annum ex-Sparsentan.

Now let’s say that the FDA opts to wait for the eGFR results and the rejection is therefore efficacy as opposed to safety related. Travere could potentially come back from this, but the initial market reaction would likely drag the share price down by ~50%. I would consider that a potential buying opportunity, knowing that eGFR data could reverse the FDA’s decision ~9 – 12 months’ down the line.

Now let’s assume Sparsentan is approved. In this scenario, I suspect analysts would concur that the drug has blockbuster (>$1bn sales per annum) potential, and again assuming a forward price to sales ratio of ~3x, my expectation would be that Travere’s share price would likely double in value initially, or reach a value of >$40, giving the company a >$3bn market cap valuation.

That price may not last, as Travere would likely complete a fundraising at that point, diluting investors, and the launch process and likely competition may end up being more challenging than initially expected.

My feeling is that Travere will secure the accelerated approval. It is not quite the case that the FDA must approve Sparsentan since it approved Tarpeyo on similar grounds, but having established an approval bar, the FDA is likely to stick with it. It would seem unfair of the agency to rule that Sparsentan is unsafe because drugs in the same class have proven to be unsafe. Sparsentan’s safety profile – to date at least – appears satisfactory, although Travere must continue to prove this with each new data readout.

Since this is kidney disease, and kidney disease outcomes are unpredictable, and the FDA has the luxury of choosing between a handful of late stage candidates, I will stop short of recommending Travere stock as a “BUY” opportunity.

What seems certain is that the FDA’s decision will create massive share price volatility, but the tougher question is whether it will be to the upside, or to the downside.

Sparsentan is Travere’s most important drug by a long way. Travere began life as Retrophin, a company created by the now-disgraced hedge fund manager Martin Shkreli, who resigned from the company in 2014, before being sentenced to 7 years in prison for securities fraud. Shkreli was accused of hiking the price of Thiola during his time at Retrophin.

After changing the name and direction of Retrophin, current CEO Eric Dube would take another step toward restoring Travere’s reputation with a FDA accelerated approval for Sparsentan. It has been a long and difficult journey to get to this point, and it’s hard to say for certain what the future may hold, but February’s decision is undoubtedly the most important date yet in Travere’s short history.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment