Mohammed Haneefa Nizamudeen Travere

“Price is what you pay, value is what you get.” – Warren Buffett

Author’s note: This is an abbreviated version of an article originally published in advance on Feb. 08, inside Integrated BioSci Investing for our members.

In biotech investing, you need to continually sift through the market to find lucrative investment opportunities. The more companies that you assess, the keener your intuition is in picking upcoming winners. It’s just like buying a new house. The more properties you evaluate over the years, the easier it is for you to know which home is an excellent buy.

That being said, I’ve been researching the vast biotech market to deliver promising companies for your investing/trading consideration. On that note, I recently learned about Travere Therapeutics (NASDAQ:TVTX), a promising biotech innovator for the orphan (i.e., rare) disease market. Already generating significant topline, Travere has powerful upcoming catalysts that can substantially boost its investing fundamentals. In this research, I’ll feature a fundamental analysis of Travere while focusing on the transformative catalysts.

StockCharts

Figure 1: Travere chart

About The Company

As usual, I’ll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Based in San Diego, California, Travere Therapeutics is focused on the development and commercialization of novel drugs to treat rare diseases. Formerly Retrophin, the company changed its name to Travere in 2020.

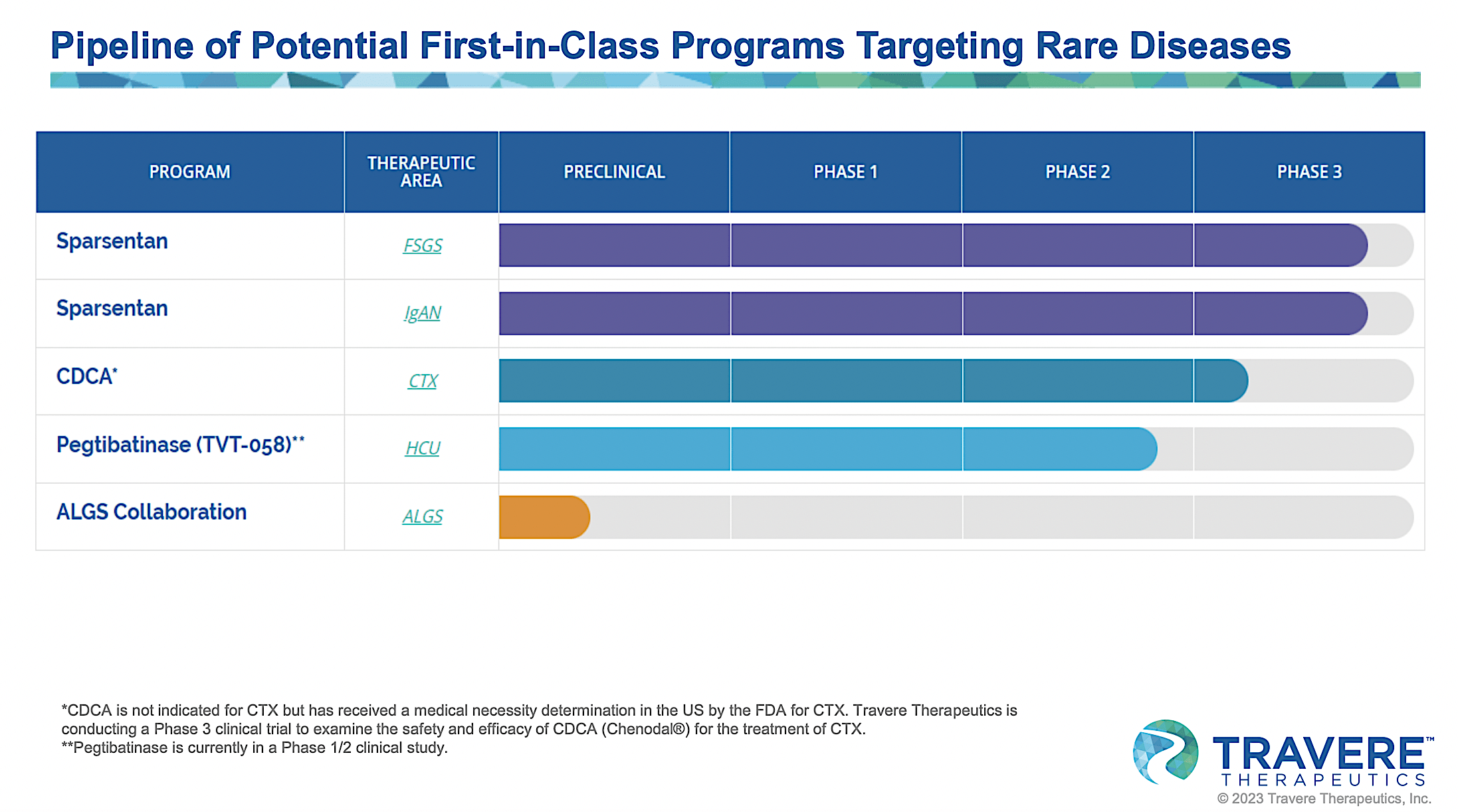

Viewing the pipeline below, you can see that Travere is brewing drugs to treat Alagille Syndrome (i.e., ALGS), homocystinuria (HCU), cerebrotendinous xanthomatosis (i.e., CTX), and focal segmental glomerulosclerosis (FSGS). Of those molecules, the crown jewel of the pipeline is sparsentan which is currently in Phase 3 studies for both IgA nephropathy (IgAN) and FSGS.

Travere

Figure 2: Therapeutic pipeline

Drug And Technology – Sparsentan

As a dual endothelin angiotensin receptor antagonist, I strongly believe that Sparsentan is ideal to tackle kidney diseases where there is protein leakage into the urine and compromised eGFR. Through various Mechanisms of Action (as depicted below), sparsentan ultimately reduces protein spilling into the urine (i.e., proteinuria) and thereby halts the disease progression to kidney failure.

Travere

Figure 3: Mechanisms of action of Spartsentan

Sparsentan for IgA Nephropathy

As you know, the lead franchise for Sparsentan development is for the orphan kidney condition coined IgAN. Also known as Berger’s disease, IgAN results in the build-up of the antibody (IGA) in the kidneys which compromises the kidney’s function over time.

Notably, the disease course is different for different people with some patients progressing to end-stage kidney failure while others achieve complete remission. Currently, there is no cure. The only management is to optimize blood pressure and reduce protein leakage in the urine.

Travere

Figure 4: Spartsentan for IgAN

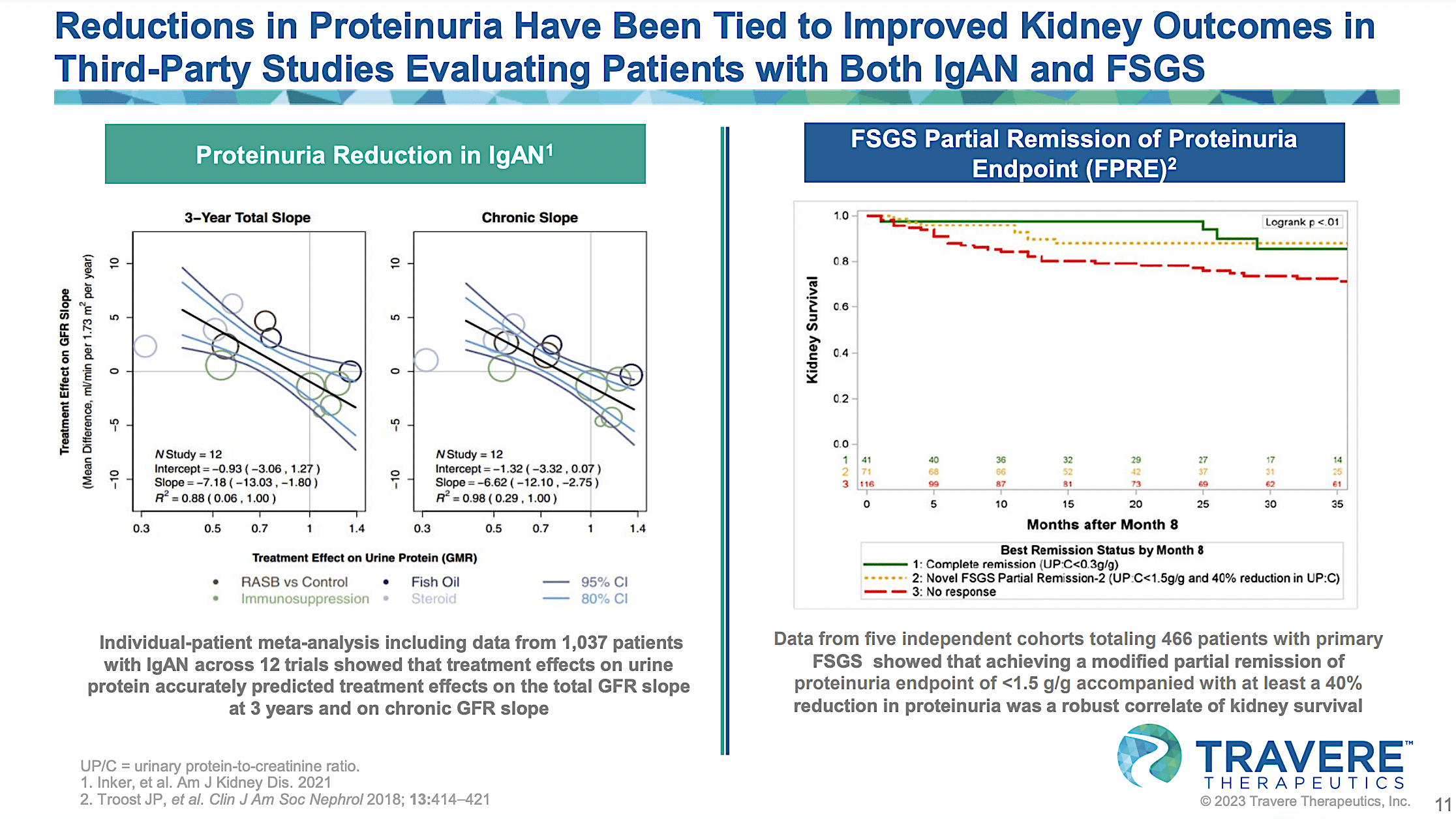

Robust Sparsentan Data With Clinical Significance for IgAN and Beyond

As you can see, Travere reported extremely strong interim data for its ongoing Phase 3 (PROTECT) trial that assesses sparsentan for IgAN. It is remarkable that sparsentan achieved a 49.8% proteinuria reduction compared to only a 15.1% reduction for the current standard of care (irbesartan). Given that the p-value is 0.0001, you can bet that the efficacy is due to sparsentan rather than random occurrences. That aside, the drug was well tolerated.

Travere

Figure 5: Robust sparsentan clinical data

From the figure below, you can appreciate that proteinuria reduction translates into improved kidney health. As such, that would make sparsentan useful for IgAN and FSGS. From the nutritional viewpoint, you can see that the body needs proteins for adequate functioning. If the proteins are constantly lost through the kidneys/urine, your body won’t have adequate building blocks (proteins) to maintain itself.

Travere

Figure 6: Proteinuria reduction lead to improved clinical outcomes

Asides from preliminary data, PROTECT is now fully enrolled and is scheduled to assess the eGFT slope over 110 weeks. As a measure of the filtration rate by the kidney, eGFT is an excellent assessment of the kidneys’ function. Full data is expected to be reported in 2H this year.

Upcoming Regulatory Catalysts For Sparsentan In IgAN

Riding excellent interim data, the FDA already accepted Travere’s New Drug Application (i.e., NDA) for sparsentan’s accelerated approval as a treatment for IgAN. Travere also completed its late-cycle review meeting with the FDA and thereby got its Prescription Drug User Fee Act (PDUFA) date set for February 17.

Additionally, Travere and its ex-USA sales/marketing partner (CSL Vifor) announced that the EMA accepted their application back in August last year. With the milestones cleared, you can also expect an approval decision from the EMA in H2 this year. If positive, this could give Travere a huge boost in its share price.

Subsequent Catalyst – Sparsentan for FSGS

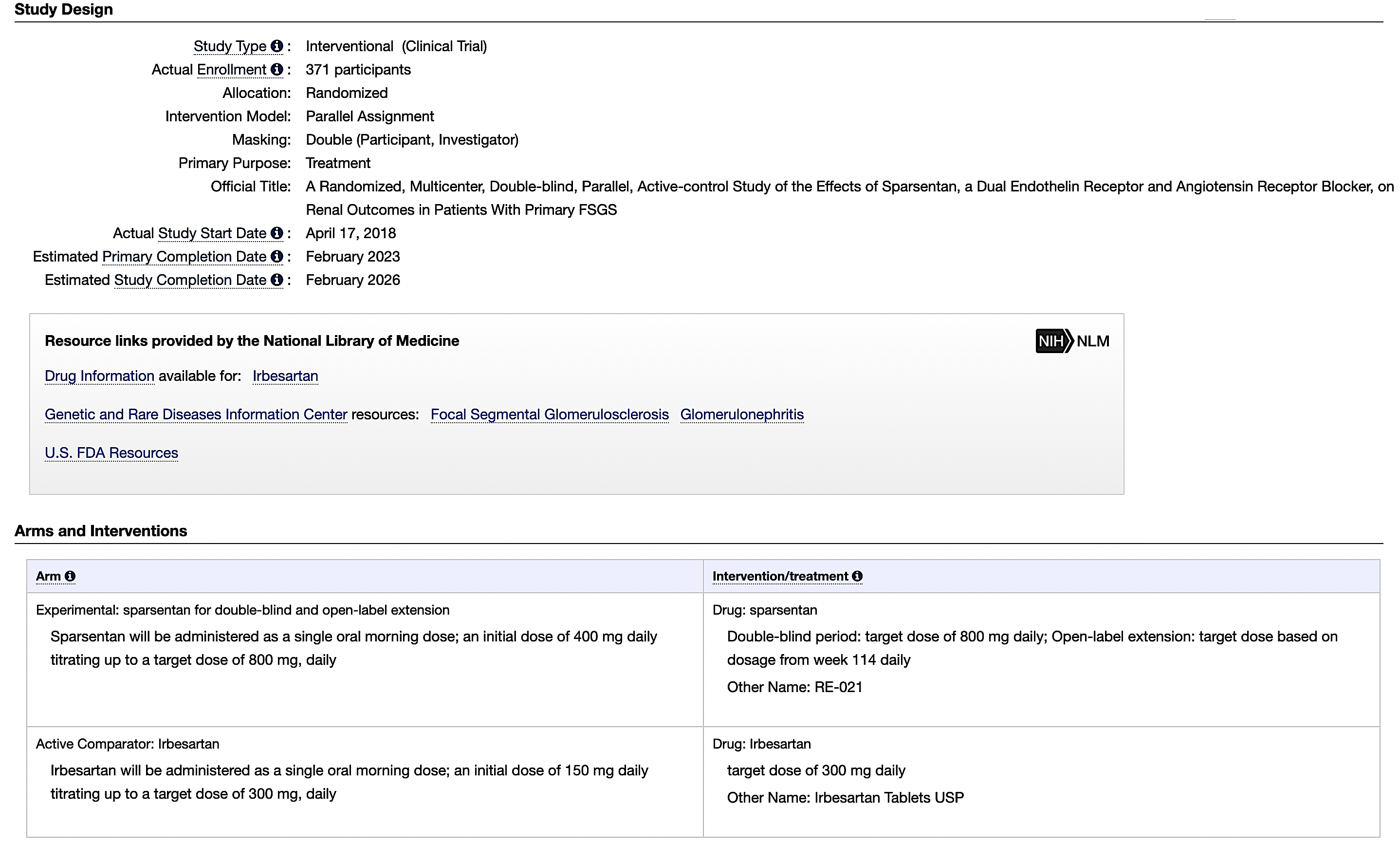

Beyond IgAN, Travere is prudently advancing sparsentan for focal segmental glomerulosclerosis (FSGS) through the Phase 3 (DUPLEX) study. As a serious condition, FSGS is characterized by scarring of the kidney’s small functional units, i.e., the glomeruli. Consequently, it can lead to kidney failure, thus subjecting the patient to a kidney transplant.

Being fully enrolled with 371 patients, DUPLEX is the largest study to date for the orphan (i.e., rare) condition, FSGS. The study’s primary endpoints include both proteinuria and eGFR. In H2 this year, you can anticipate Travere to release DUPLEX’s topline data. Pending the study results, the company would file for marketing applications later this year.

ClinicalTrial.gov

Figure 7: DUPLEX study design

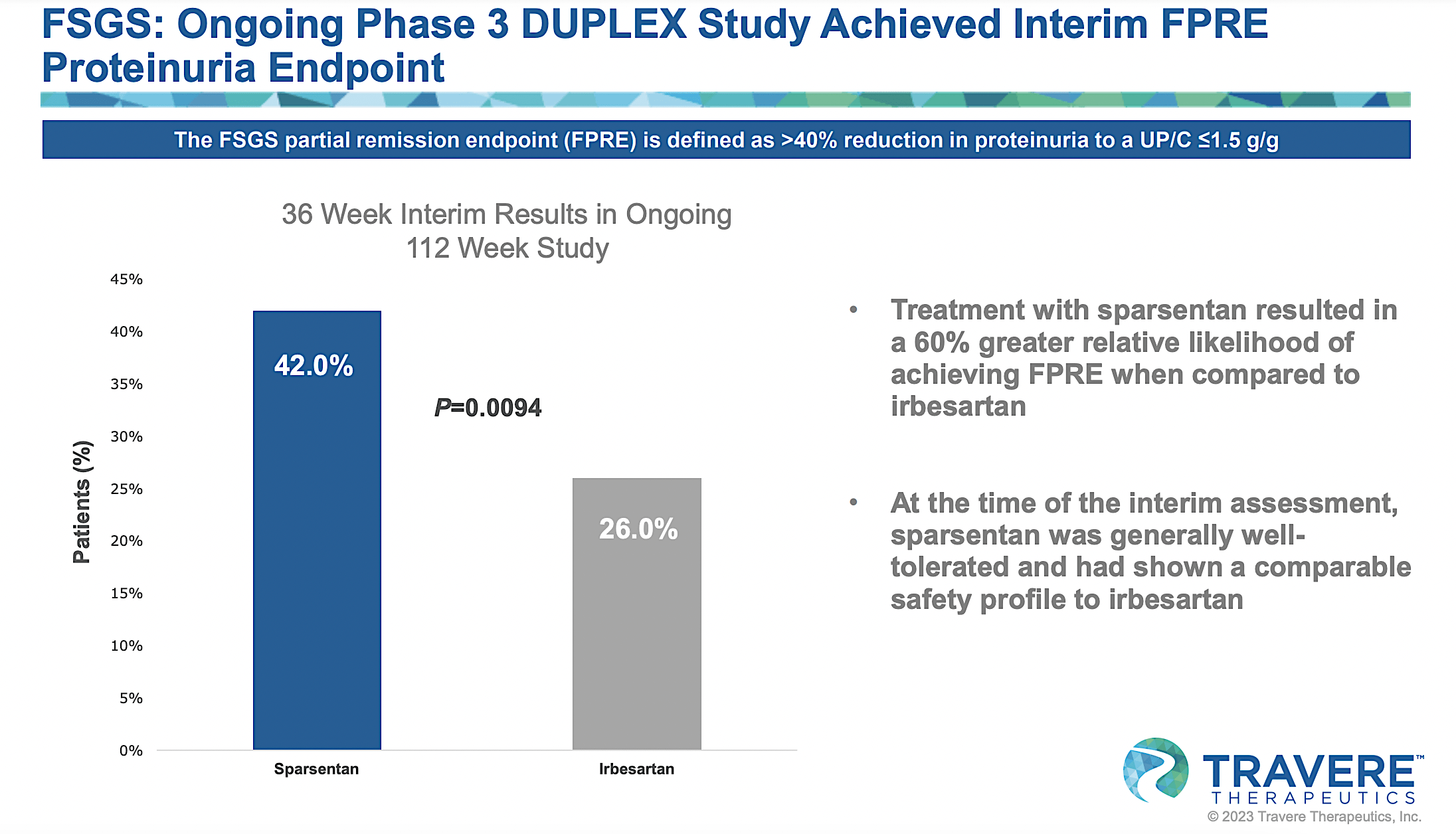

Per the figure below, you can appreciate that sparsentan posted extremely robust interim data for DUPLEX. Specifically, sparsentan generated a 42.0% proteinuria reduction compared to 26.0% for irbesartan at the 36-Week analysis. As you would expect, sparsentan also has an excellent safety profile.

Travere

Figure 8: DUPLEX’s interim results

Substantial Market And High Demand

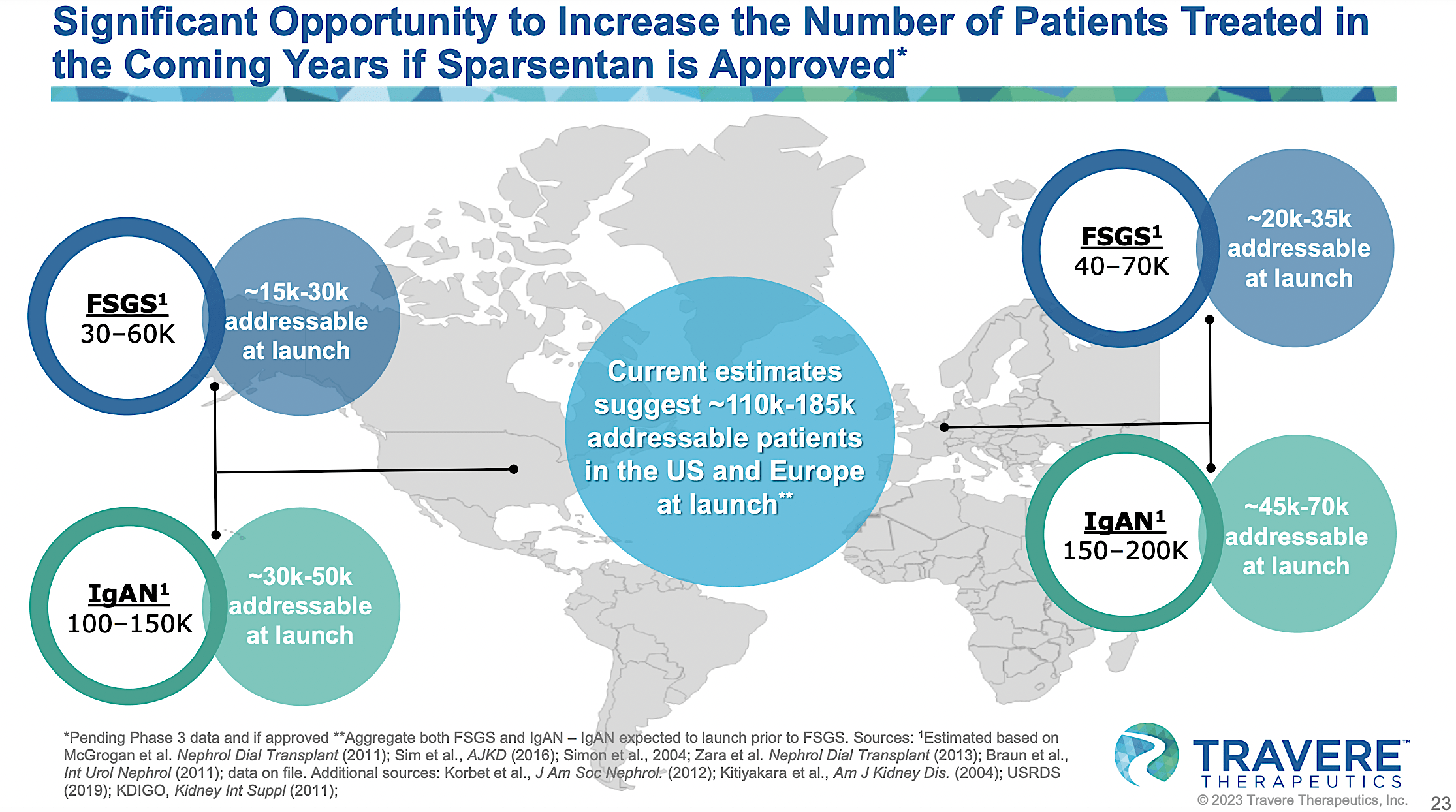

As you can imagine, sparsentan would have a substantial market due to the high demand for novel treatments for both IgAN and FSGS. Even when their occurrences are less than 200K annually, these rare diseases command a premium treatment. On average, an orphan drug gets reimbursed at $140K annually to offset the lengthy and low success rate of the innovation process. As such, you can see that there is definitely a sizeable market for sparsentan.

Travere

Figure 9: Substantial market for sparsentan

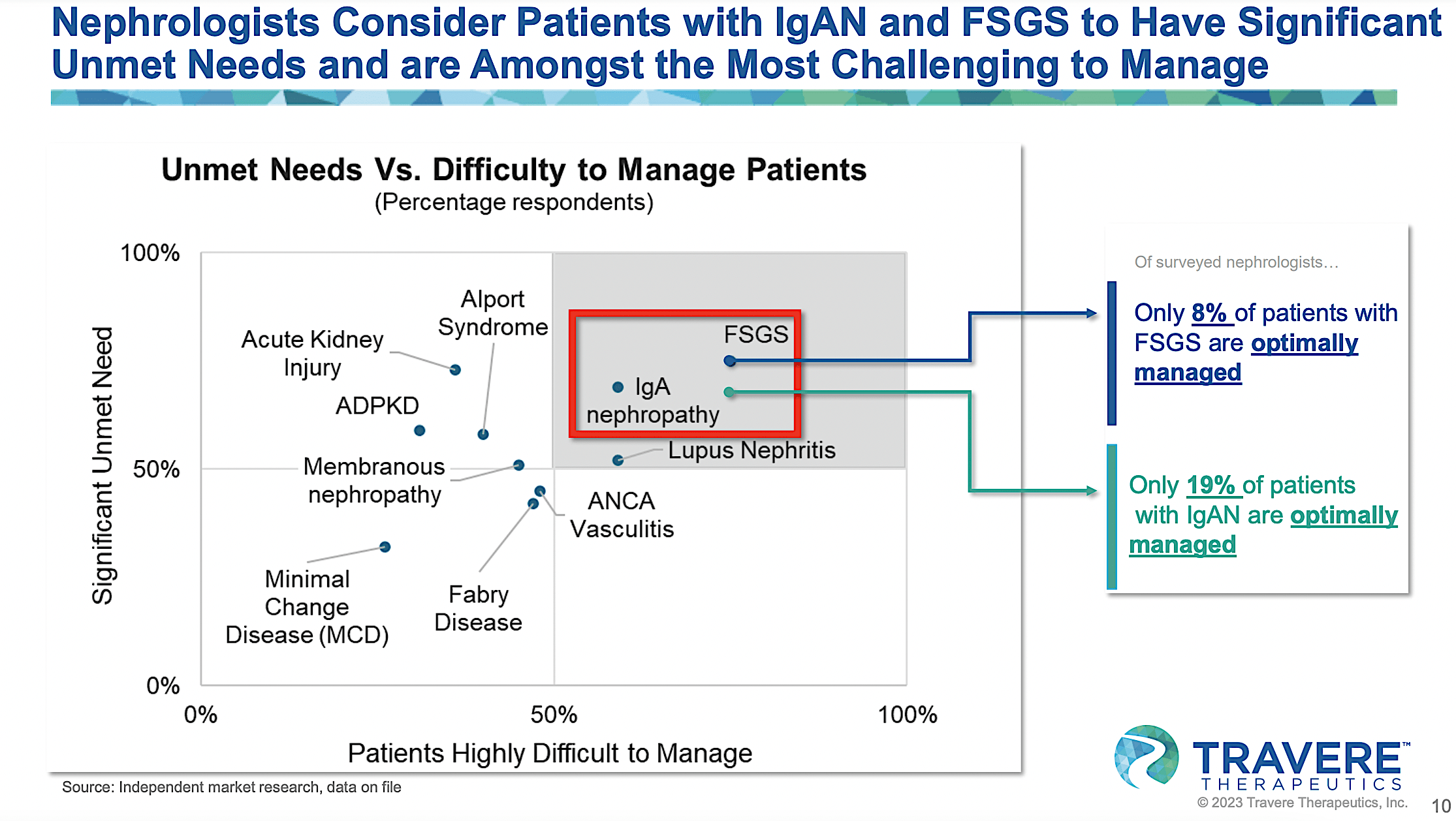

Given that only 19% and 8% of patients afflicted by IgAN and FSGS are correspondingly well managed, you can bet that the demand for sparsentan is extremely high. If the drug can gain approval, sales should be quite significant due to high market adoption.

Travere

Figure 10: Sparsentan to fill high unmet needs

Financial Assessment

Just as you would get an annual physical for your well-being, it’s important to check the financial health of your stock. For instance, your health is affected by “blood flow” as your stock’s viability is dependent on the “cash flow.” With that in mind, I’ll assess the 3Q2022 earnings report for the period that ended on September 31.

As follows, Travere procured $53.4M in revenues compared to $68.2M for the same period a year prior. On a year-over-year basis, the revenues are reduced by 21.7% which is due to lower Thiola sales.

That aside, the research and development (R&D) for the respective periods registered at $48.4M and $59.2M. I viewed the 22.3% R&D increase positively because the capital invested today can turn into blockbuster profits tomorrow. After all, you have to plant a tree to enjoy its fruits.

Additionally, there were $69.6M ($1.09 per share) net losses compared to $35.6M ($0.59 per share) declines for the same comparison. On a per-share basis, the bottom-line depreciation widens by 81.3%.

Travere

Figure 11: Key financial metrics

About the balance sheet, there were $506.3M in cash, equivalents, and investments. Against the $68.1M quarterly OpEx and on top of the $54.3M, there shouldn’t be a concern for cash flow constraints any time soon. Simply put, the cash position is robust relative to the revenue and burn rate.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strengths. More importantly, the risks are “growth-cycle dependent.” At this point in its life cycle, the main concern for Travere is whether the company can gain FDA approval for sparsentan by February 17. Moreover, the other important risk is whether sparsentan can generate positive data for both PROTECT in Q3 and DUPLEX in Q2.

Conclusion

In all, I recommend Travere as a speculative buy with a 4.8/5 stars rating. Already commercializing a medicine that procured roughly a quarter of a billion dollars in annual sales, Travere will get its accelerated approval decision for the lead medicine (sparsentan) for the lucrative orphan kidney diseases (IgAN) soon. Advanced data being released thus far are stellar for IgAN and FSGS. That aside, Travere is stacked on the immediate catalyst in the upcoming Phase 3 (DUPLEX) data release for FSGS in Q2 and the Phase 3 (PROTECT) eGFR data for IgAN in Q3. If positive, you’re likely to see Travere shares trade much higher than the current valuation.

Be the first to comment