The Tortoise Power & Energy Infrastructure Fund (NYSE:TPZ) is a closed-end fund (“CEF”) that invests primarily in power and energy infrastructure companies. According to the Prospectus and Fact Sheet:

Our primary investment objective is to provide a high level of current income, with a secondary objective of capital appreciation. There can be no assurance that we will achieve our investment objectives.”

TPZ seeks to invest in fixed income and dividend-paying equity securities of power and energy infrastructure companies that provide stable and defensive characteristics throughout economic cycles.

TPZ seeks to provide:

• Attractive total return potential emphasizing current distributions

• Exposure to power and energy infrastructure companies operating real, long-lived, essential power and energy assets

• Investor simplicity through one 1099, no K-1s, no unrelated business taxable income, IRA suitability

• Expertise of Tortoise, a leading and pioneering energy investment firm.”

Tortoise

Tortoise

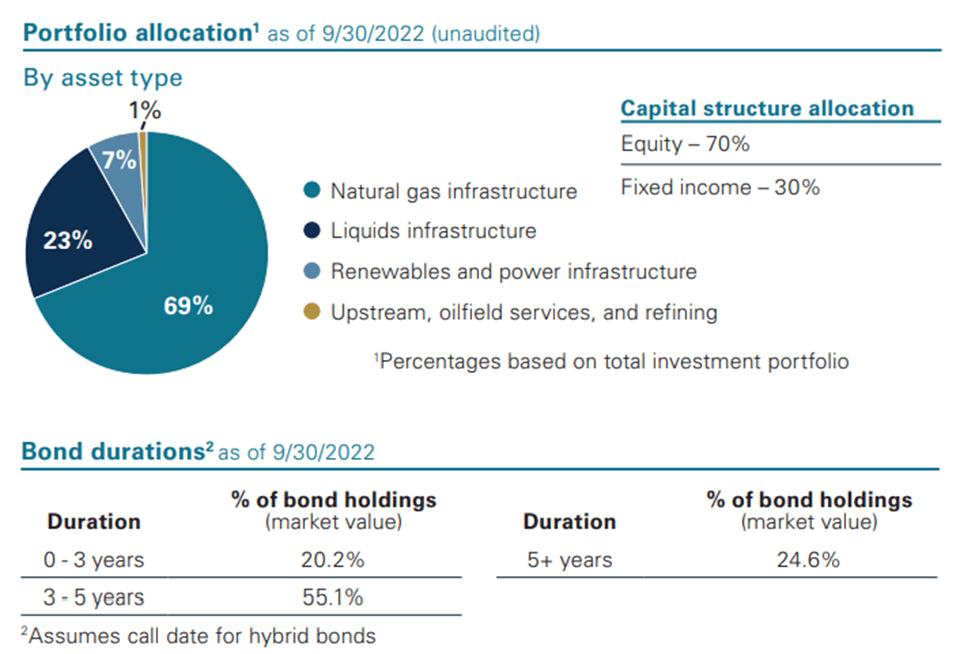

The most recently disclosed allocation is as follows:

Tortoise

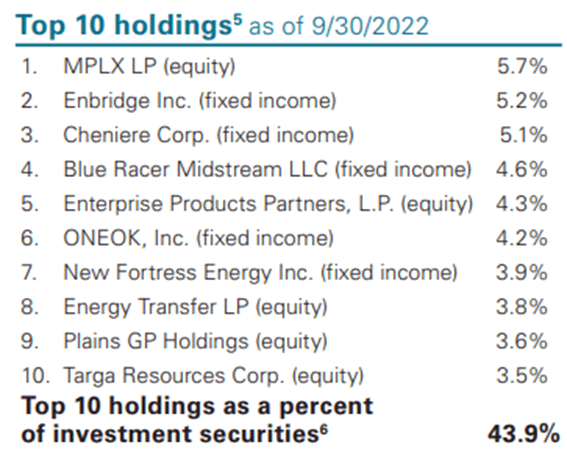

And the largest holdings are:

Tortoise

Four of the five portfolio managers are chartered financial analysts (“CFAs”):

Tortoise

A CFA is:

a globally-recognized professional designation that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas, such as accounting, economics, ethics, money management, and security analysis”

Expenses and AUM

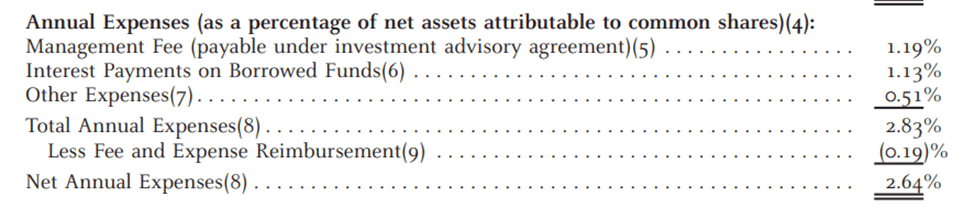

In the original Prospectus, Net Annual Expenses was set at 2.64%. A major reason for expenses to be so high is that they include interest payments on borrowed funds because CEFs can be debt-leveraged to provide a higher return to investors. But leverage also implies higher risk as well.

Tortoise

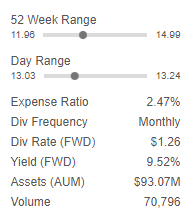

Most recently, the expense ratio has been quoted at 2.47%. The Assets Under Management (“AUM”) is about $93 million.

Seeking Alpha

Tender Offer

Tortoise announced the commencement of cash tender offers for TPZ as well as other Funds. Up to 5% of TPZ’s outstanding shares are subject to the offer:

Each tender offer will be conducted at a price equal to 98% of each Fund’s net asset value (“NAV”) per share as of the close of regular trading on the New York Stock Exchange on November 1, 2022 or on such later date to which the offer is extended.

If the number of shares tendered exceeds the maximum amount of a tender offer, the Fund will purchase shares from tendering shareholders on a pro-rata basis (disregarding fractional shares).”

The SEC provides tender offer FAQs on this webpage.

For information on how to participate in a tender offer, carta provides step-by-step guidance.

A company may make a tender offer to existing shareholders to buy back a quantity of its own stock to regain a larger equity interest in the company and as a way to offer additional return to shareholders.”

As noted below, TPZ’s performance has lagged the broader equity market, and so an additional return to attract shareholders is in order.

Performance

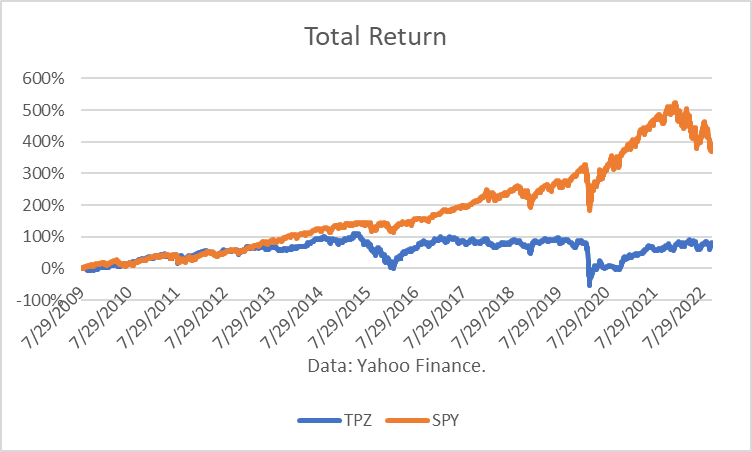

Since inception in mid-2009, the total return of TPZ was 75.5%. That compares unfavorably to the S&P (SPY) return of 370.4% over the same period.

Yahoo Finance data

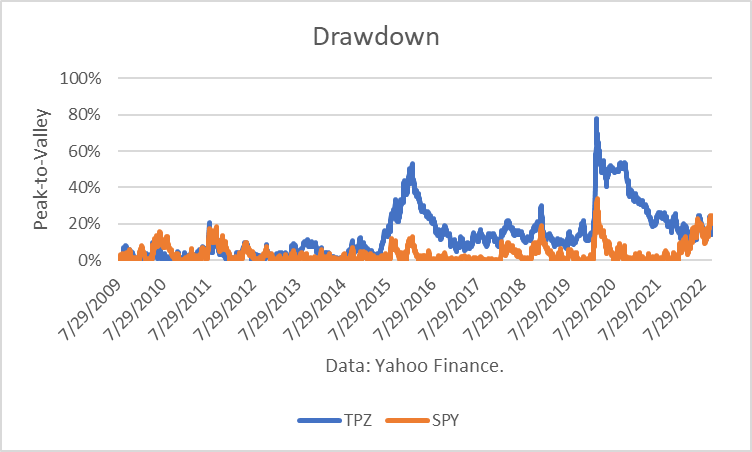

The Maximum Drawdown (“MD”) of holding TPZ was 78%. The MD is the risk measure I find to be most meaningful because it represents the maximum loss. The MD of SPY was 34%.

Yahoo Finance data

Over the past year, TPZ returned 5.13%, as compared to a loss of 16.03% in the SP500TR.

Seeking Alpha

Midstream Energy Infrastructure Sector Analysis

The energy value chain consists of three sectors: upstream, midstream and downstream. The upstream sector is focused on producing hydrocarbons at the wellhead, and the downstream sector sells and delivers products to end users. The midstream is concerned with the gathering and processing, transportation, and storage and logistics of products from the upstream to the downstream sectors.

There are three distinct value chains: oil, natural gas and natural gas liquids (“NGLs”). Midstream companies generally charge fees for services and are not exposed to commodity price risk. This provides a more predictable cash flow from which it can pay dividends to investors. However, processing facilities often charge margin-based fees, which can provide a higher or lower cash flow than the fee-based revenue model.

Midstream companies may have a particular market niche or may operate across the entire value chain. They may also be a master limited partnership (“MLP”) or operate in a traditional C-Corp structure. MLPs provide Schedule K-1 to investors instead of a 1099 Form. Potential investor should consult their financial advisors or tax accountants for advice regarding their particular circumstances.

TPZ provides “Investor simplicity through one 1099, no K-1s, no unrelated business taxable income, IRA suitability,” according to its Fact Sheet.

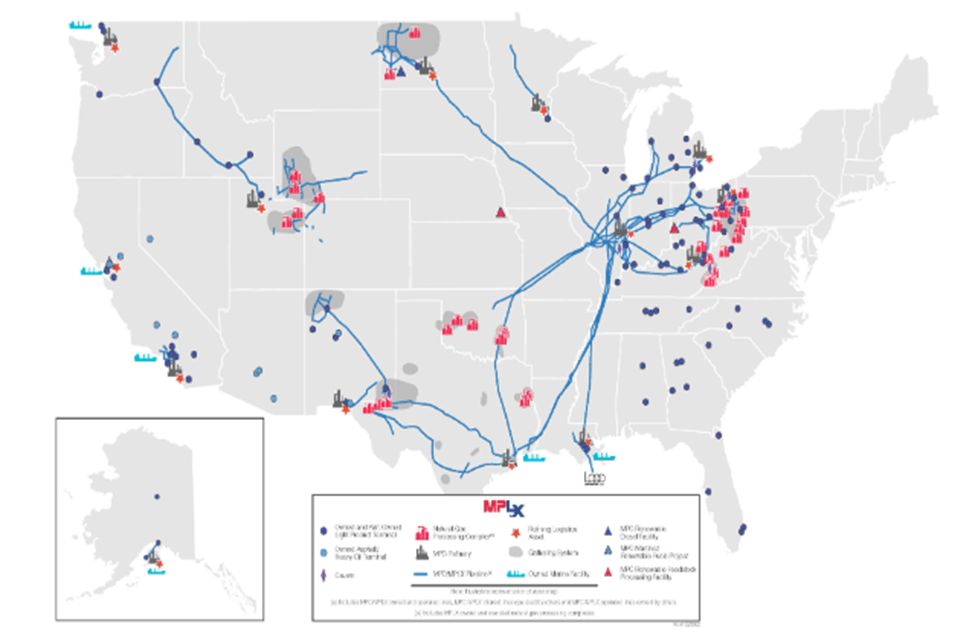

MPLX LP (MPLX) is currently listed as the largest holding of TPZ and thus serves as a good example. It is a diversified, large-cap MLP formed in 2012 by Marathon Petroleum Corporation (MPC).

It owns and operates midstream energy infrastructure and logistics assets, and provides fuels distribution services. Our assets include a network of crude oil and refined product pipelines; an inland marine business; light-product, asphalt, heavy oil and marine terminals; storage caverns; refinery tanks, docks, loading racks, and associated piping; crude oil and natural gas gathering systems and pipelines; as well as natural gas and NGL processing and fractionation facilities.

The operation of these assets are conducted in our Logistics and Storage (“L&S”) and Gathering and Processing (“G&P”) operating segments. Our assets are positioned throughout the United States as depicted in the map below.

MPLX

Our L&S segment primarily engages in the gathering, transportation, storage, and distribution of crude oil, refined products and other hydrocarbon-based products. We also operate refining logistics, fuels distribution and inland marine businesses, terminals, rail facilities and storage caverns.

Our G&P segment primarily engages in the gathering, processing and transportation of natural gas as well as the gathering, transportation, fractionation, storage and marketing of NGLs.”

Market Outlook

For midstream companies that provide fee-for-service, the volume of products handled is key to its future revenues. Therefore, future consumption and trade projections are most relevant. It is also important to view both short-term and long-term forecasts to understand how the prices of midstream assets may evolve.

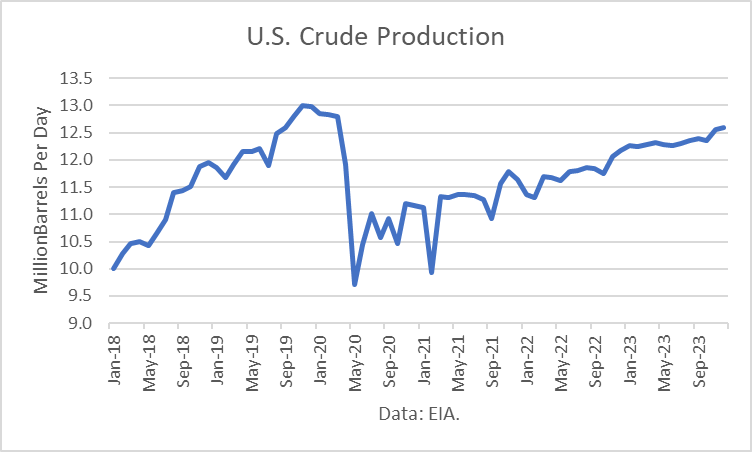

In the short-term, through 2023, the October 2022 EIA Short-Term Energy Outlook (“STEO”) for crude oil is for lower volumes of production and inputs to refineries than the pre-pandemic period. Although crude production is projected to rise slowly, it is not expected to exceed its 13.1 million barrels per day (“mmbd”) peak.

EIA

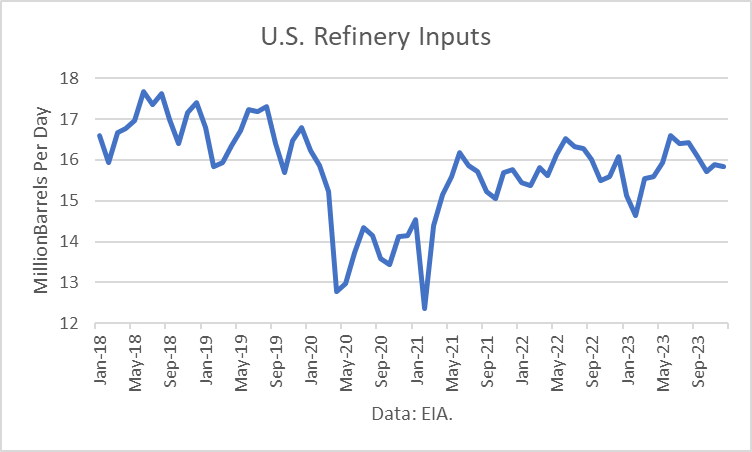

Likewise, inputs to refineries are expected to remain below 2019 levels.

EIA

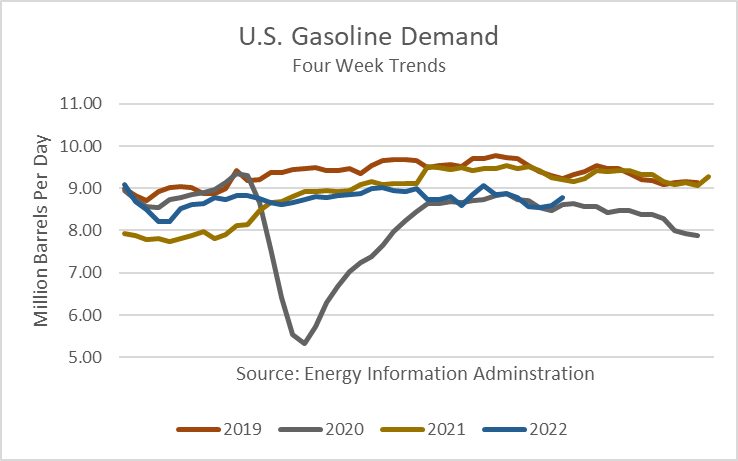

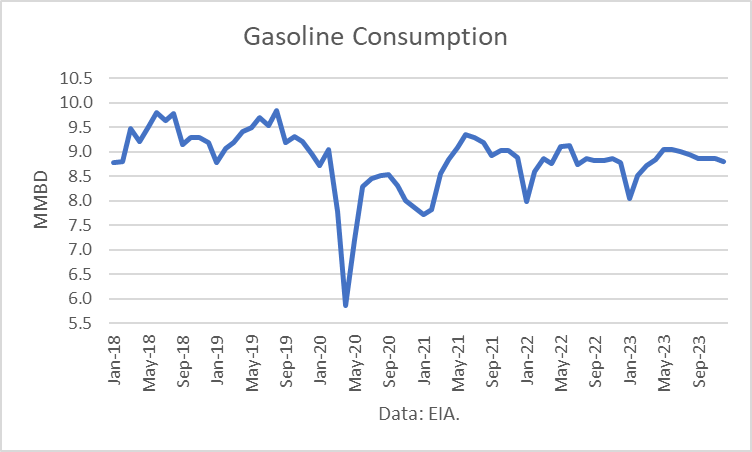

The two largest petroleum product outputs are gasoline and distillate fuels, which include diesel and heating oil. Gasoline demand is near its pandemic-lows for this time of year.

EIA

And the forecast shows that it will not recover to its 2019 level.

EIA

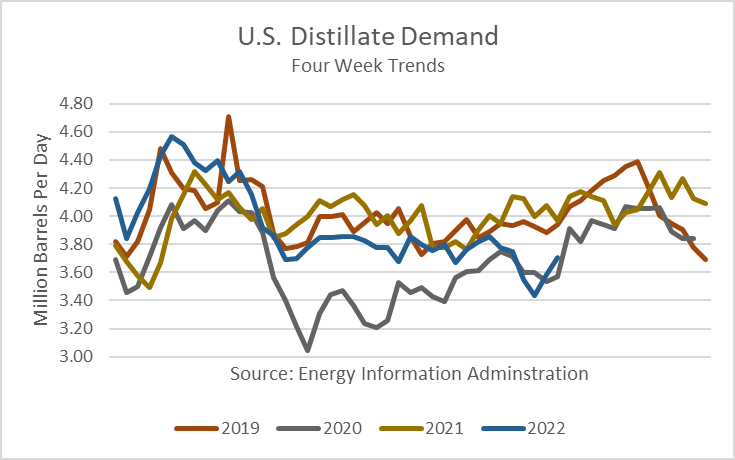

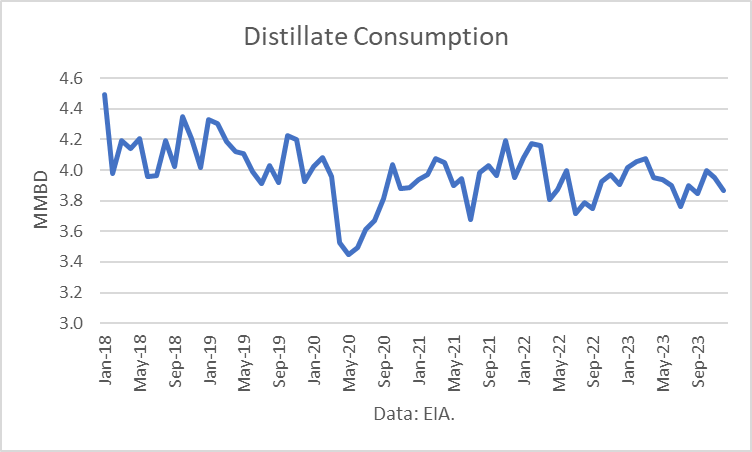

Distillate demand is also about where it was during the pandemic at this time of year.

EIA

And the near-term future does not indicate a recovery.

EIA

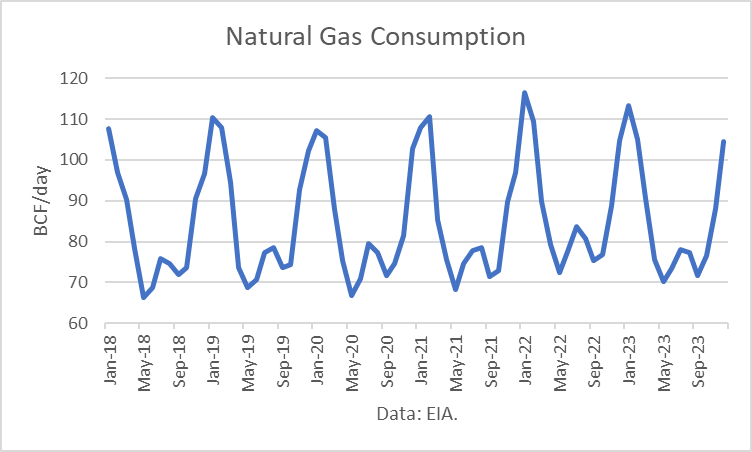

The demand for natural gas is highly dependent on weather conditions. But assuming normal temperatures, demand is projected to be lower.

EIA

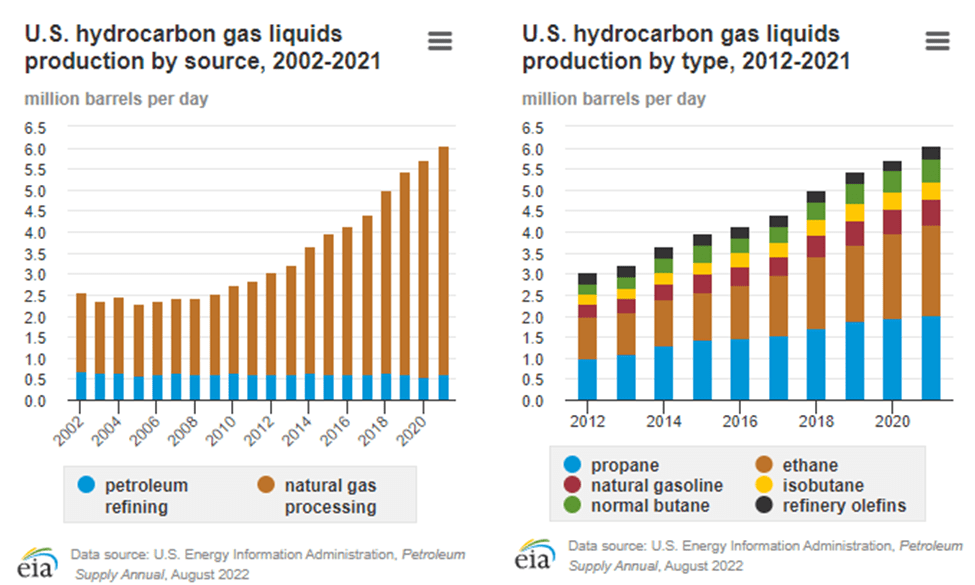

The brightest outlook is for Hydrocarbon Gas Liquids (“HGLs”). They are:

HCF

Hydrocarbons that occur as gases at atmospheric pressure and as liquids under higher pressures. HGLs can also be liquefied by cooling. The specific pressures and temperatures at which the gases liquefy vary by the type of HGLs. Natural Gas Liquids (“NGLs”) account for most of HGL production in the United States.”

Their use has increased rapidly in the past and is projected to continue in the near term.

HCF

Looking into the long-term, the EIA’s Annual Outlook through 2050 shows that petroleum seems destined to decline over the next 20 or 30 years. I previously outlined the specifics of the 2022 EIA Outlook in my article, Kayne Anderson Energy Infrastructure Prospects And DIY Portfolio (Part 2).

Highlights are that gasoline demand peaked in 2019 and NGLs demand and exports are likely to flourish over the long-term. The desire by the EU to replace Russian natural gas imports strongly supports that projection.

One of the biggest concerns at fossil-fuel companies now is the risk of ‘stranded assets’—big projects that could rapidly lose value as the market for fossil fuels dries up. In that type of environment, nobody wants to invest in assets that could become obsolete before they’ve generated a return,” according to one article.

Conclusions

With a Maximum Drawdown of 79%, TPZ is not a suitable long-term investment, in my opinion. It has also far underperformed the broader equity market.

It presents a portfolio allocation that is heavily natural gas-oriented. I do not have its historical allocations, but that appears to be a much better allocation than a petroleum-centric portfolio. Best of all would be one that is heavily oriented toward NGLs. That could be a better do-it-yourself alternative for investors willing to build their own portfolios.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment