JHVEPhoto/iStock Editorial via Getty Images

Thesis

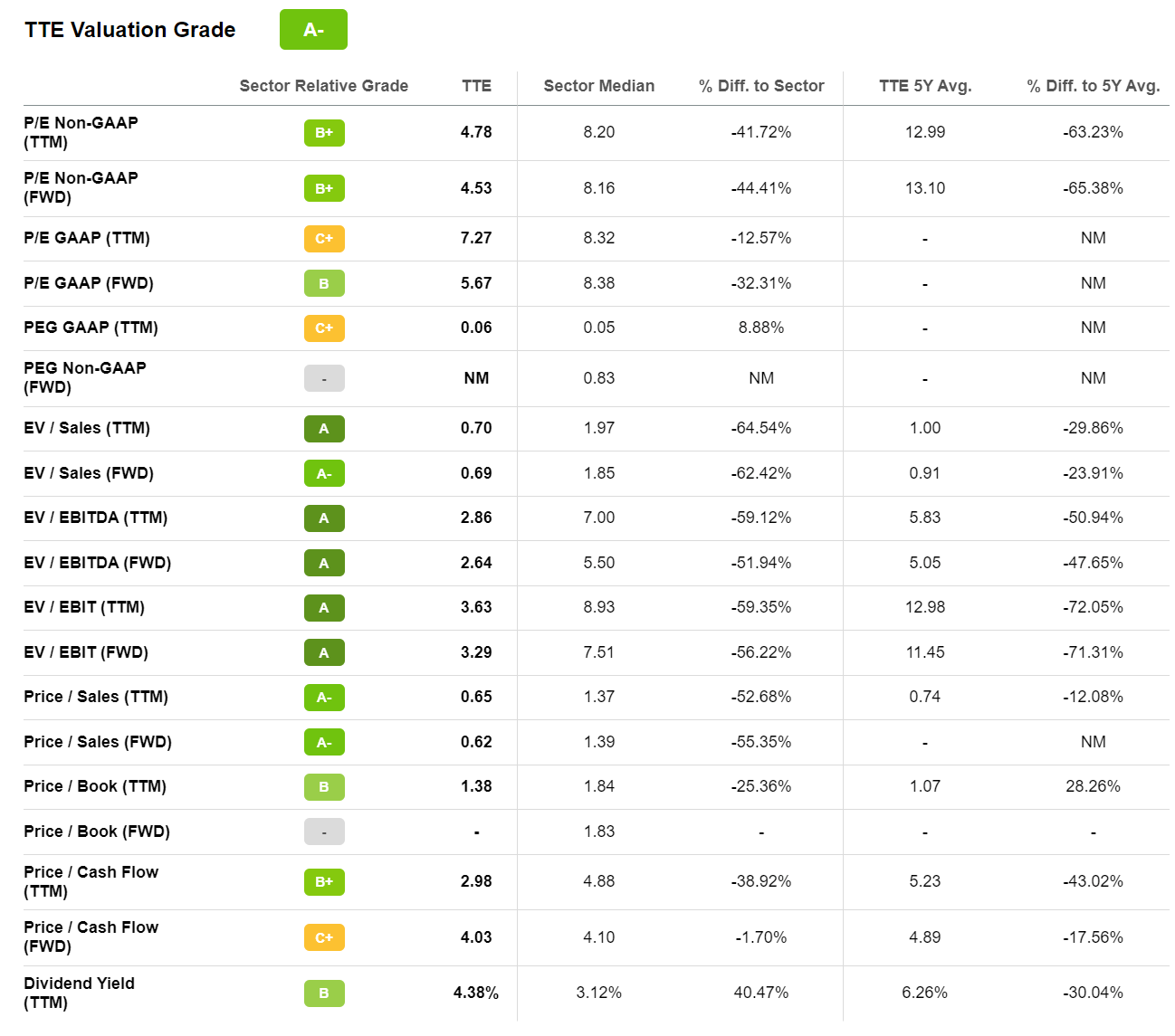

Although TotalEnergies SE (NYSE:TTE) is up by approximately 32% since I last covered the stock, as compared to a gain of only 3% for the S&P 500 (SP500), I still believe that TTE is strongly undervalued. Investors should consider that the European oil major is currently trading at a FWD EV/Sales of 0.7 and a EV/EBIT of 3.2. These multiples are simply too attractive to ignore.

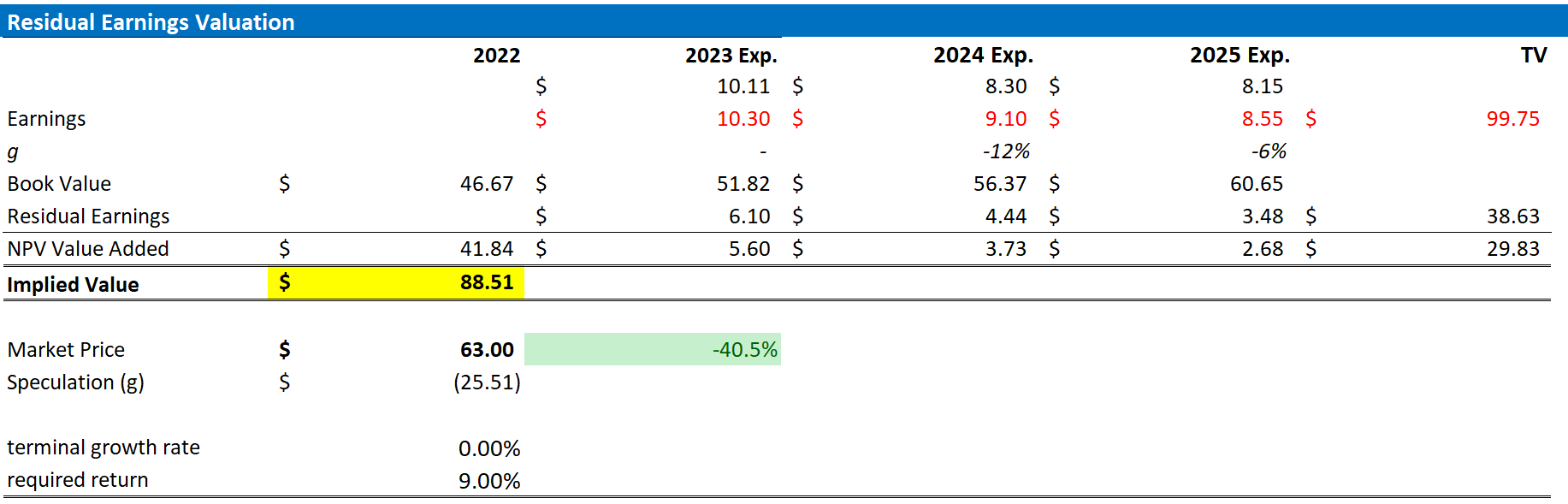

My previous target price for TTE has been about $71/share. However, on the backdrop of a stronger than expected earnings outlook through 2025, I now calculate a fair implied share price of $88.51. TTE is a clear “Buy” for me.

Strong Q3 Results Support Bullish Thesis

During the period from July to the end of September, TotalEnergies generated total revenues of $65 billion, a 32% year-over-year growth as compared to the same period in 2021. The company’s Q3 EBITDA expanded to $19.4 billion (98% year-over-year growth) and the IFRS net income grow to $6.6 billion (69% year-over-year growth). Notably, the IFRS net income included a $3.1 billion impairment related to the company’s operations in Russia. Without these non-recurring headwind, TTE’s net income would have been 9.9 billion.

Total Q3 press release

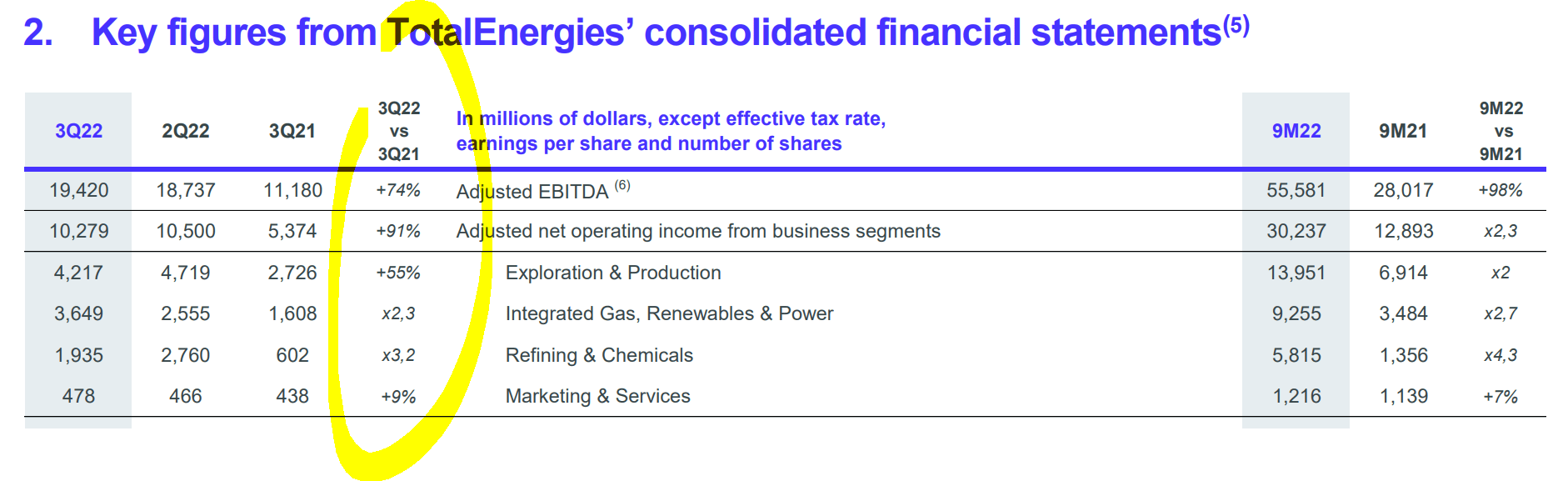

Notably, all of Total’s operating segments recorded a significant jump in earnings as compared to the same period one year earlier.

- Exploration & Production contributed $4.2 billion to the group’s EBITDA, a 55% year over year increase.

- Integrated Gas, Renewables & Power achieved an EBITDA of $3.6 billion, a 230% growth vs Q3 2021.

- Refining & Chemicals contributed $2.8 billion to the group’s EBITDA, a 320% growth versus the same period one year earlier respectively.

- And, Marketing & Services expanded EBITDA by 9% year over year, to $466 million.

Total Q3 press release

Confident Going Into Q4 2022 & Early 2023

Although energy prices have started to trade down to somewhat more reasonable prices, the WTI reference is now trading at around $80 as compared to almost $120 in the first half of 2022, the energy price level is still very supportive for energy producing assets.

For reference, for the trailing twelve months, TTE has distributed approximately $14.8 billion of cash to shareholders, of which $8 billion in form of dividends and $6.8 billion in form of share repurchases.

Seeking Alpha

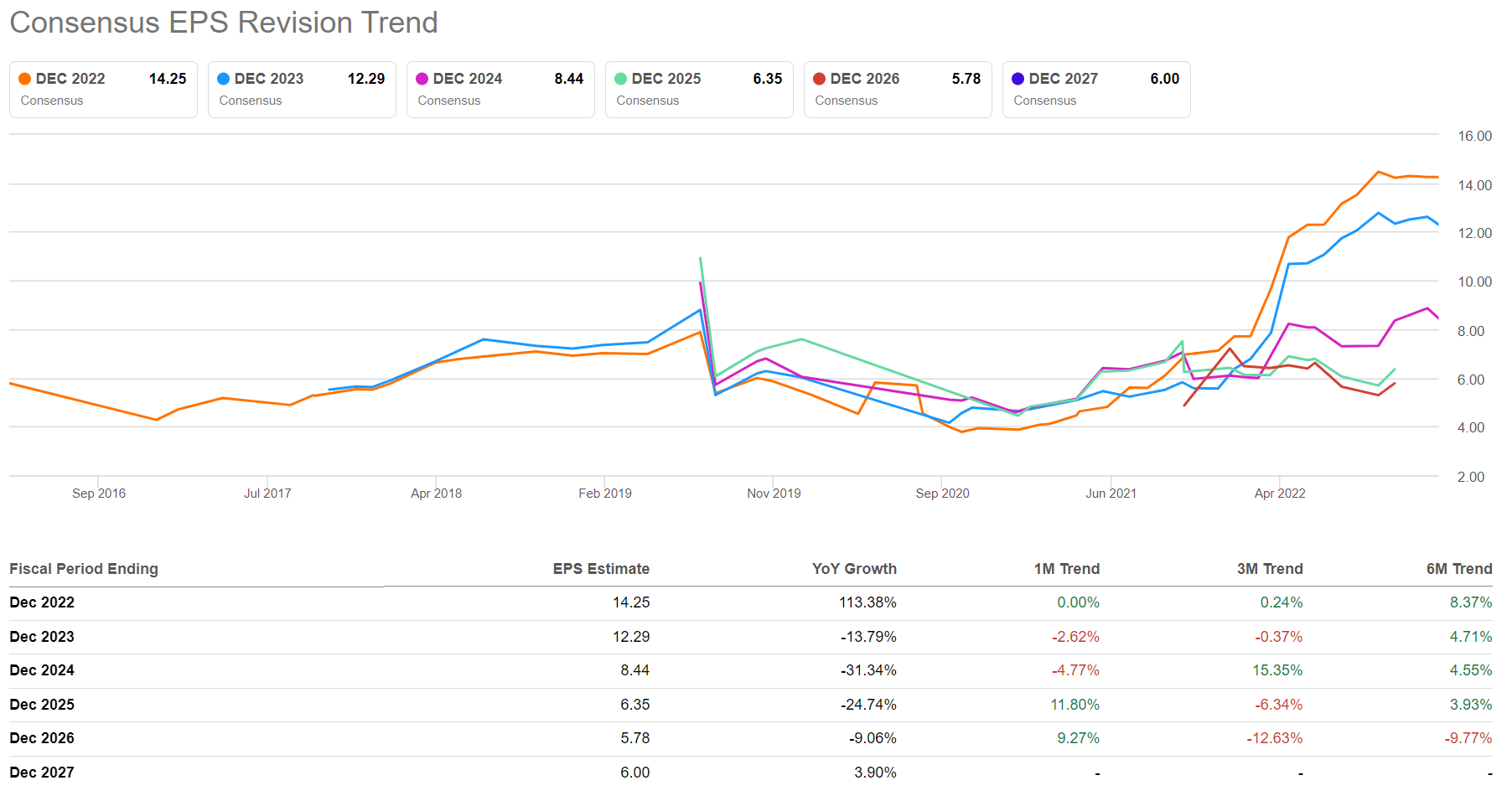

Given the current price level, analyst consensus estimates that TTE could generate $3.34 of EPS in Q4 2022. For the full year of 2023, analysts believe that TTE could achieve earnings as high as $12.3/share — which would mean a FWD P/E of less than x5.

Seeking Alpha

It is understandable that recession concerns continue to pressure the outlook for energy prices, and the valuation of energy-producing assets. Investors should consider, however, that the macro environment also has a few positive factors. Notably, oil prices continue to be supported by: (1) the OPEC+, which has voiced willingness to push oil prices towards $100/ barrel, (2), Europe’s ban of Russian sea oil effective December 5, 2022, (3) and the demand optimism coming from the more aggressive than expected COVID reopening push in China.

Valuation Remains Too Attractive To Ignore

Reflecting on TotalEnergies’s exceptional profitability in light of still elevated energy prices, I argue the investment opportunity is too attractive to ignore. Investors should consider that TTE is currently trading at an EV/Sales of about x0.7, which reflects a 62% discount to the comparable industry median. Similarly, TTE’s FWD EV/EBIT is x3.3, which is a 56% discount respectively.

Think about it: at TotalEnergies’s current valuation, analysts expect that the company will amortize its entire enterprise value within less than three and a half years. While I do understand that oil majors will likely struggle to manage a seamless energy transition towards renewables — which most certainly requires lots of investments — in 3.5 years out, TTE investors could likely own any residual book equity value, as well as any future earnings, “for free.”

Seeking Alpha Seeking Alpha

Update Target Price: Raise To $88.51

Expecting a sharp economic rebound in China, which strongly supports Baidu’s advertising business, I estimate that TTE’s EPS in 2023 will likely expand to somewhere between $10 and $10.5. Moreover, I also raise my EPS expectations for 2024 and 2025 to $9.10 and $18.55, respectively.

I continue to anchor on a 0% terminal growth rate, as well as on a 9% cost of equity.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price of $88.51, as compared to $71.52 prior.

Author’s EPS Estimates; Author’s Calculations

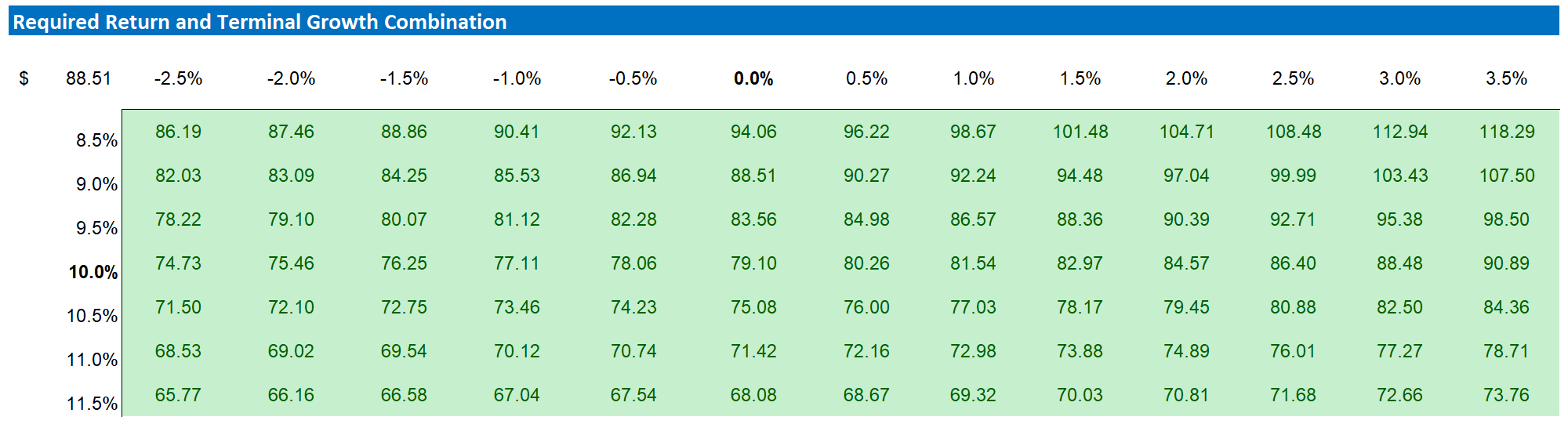

Below also the updated sensitivity table.

Author’s EPS Estimates; Author’s Calculations

Conclusion

I remain very bullish on TotalEnergies SE stock, due to strong Q3 reporting and a supportive outlook going into early 2023. Investors should consider that TTE is currently trading at an EV/Ebit of less than x3.5, which I believe is simply too low independent of how an investor would like to think about the energy market. My analysis, using a residual earnings model, estimates that TotalEnergies SE stock should be priced at around $88.51/share. It’s a clear Buy, in my opinion.

Be the first to comment