Authentic Images/E+ via Getty Images

2022 was not a particularly pleasant year for most companies related to the construction market. But one firm that ended up performing quite well in the second half of the year compared to the broader market is TopBuild (NYSE:BLD). Driven by robust performance in both its top and bottom lines, the insulation installation and distribution company has seen some appreciation in its share price. Add on top of this fundamental performance the fact that shares look cheap compared to most similar enterprises, and I believe that the ‘buy’ rating I assigned the company previously is still warranted.

Building value

Back in the middle of July of 2022, I wrote an article discussing my bullish stance on TopBuild. In that article, I talked about how attractive the revenue and cash flow picture of the company had been. This robust performance made shares cheap on a forward basis, even though the company was a bit pricey compared to other firms I stacked it up against. But at the end of the day, the attractive growth of the firm was appealing enough for me to keep the ‘buy’ rating I had previously attached to the company. Although it hasn’t been by a great deal, the company has managed to outperform the market during this time. While the S&P 500 is up 0.9%, shares of TopBuild have seen upside of 3.6%.

Author – SEC EDGAR Data

Had the numbers the company reported come out during any normal year, I would have expected the performance of shares relative to the market to be far greater. But at the end of the day, the supreme pessimism that’s reigning in this space has prevented this upside from transpiring. The reason why I say that shares would have risen more in a typical market is because the overall fundamental performance of the company has been incredible. Sales, for instance, in the third quarter of the company’s 2022 fiscal year came in at $1.30 billion. That’s 53.8% higher than the $845.8 million reported the same time one year earlier. To be clear, acquisitions the company made added 31.2% to its top line. But that doesn’t change the fact that the company benefited to the tune of 13.6% from higher selling prices on its products and to the tune of 9.1% from a rise in sales volume.

The bottom line for the company followed the top line. Net income jumped from $95.4 million to $153.7 million. In addition to benefiting from an increase in sales, the company saw its gross profit margin climb from 29.6% to 30.4%. This is a testament to the company’s ability to increase selling prices while simultaneously experiencing a rise in sales volume. Selling, general, and administrative costs also improved relative to revenue, dropping from 13.8% to 13.3%. Naturally, other profitability metrics followed a similar trajectory. Operating cash flow went from $107.3 million in the third quarter of 2021 to $117.9 million in the third quarter of 2022. If we adjust for changes in working capital, the picture was even better, with the metric rising from $119 million to $193 million. And over that same window of time, EBITDA for the company jumped from $158.2 million to $259.2 million.

Author – SEC EDGAR Data

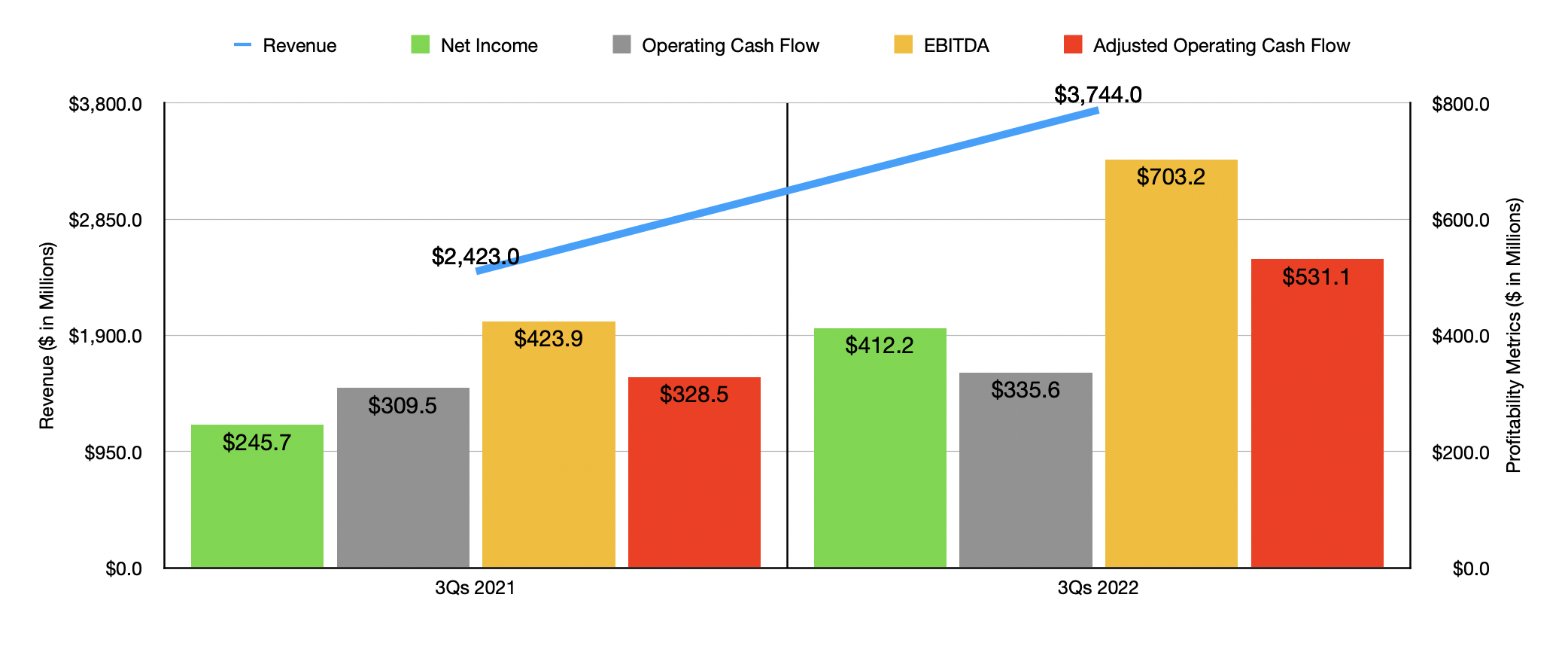

For the first nine months of 2022, the fundamental performance achieved by TopBuild was quite robust. Sales jumped from $2.42 billion to $3.74 billion. That translates to a year-over-year increase of 54.5%. Profitability followed a very similar path. Net income, for instance, skyrocketed 67.8% from $245.7 million to $412.2 million. Operating cash flow rose from $309.5 million to $335.6 million, while the adjusted figure for this grew from $328.5 million to $531.1 million. And finally, EBITDA for the company increased from $328.5 million to $531.1 million. When it comes to 2022 as a whole, management anticipates revenue of between $4.95 billion and $5 billion. At the midpoint, that would translate to a year-over-year increase of 42.7%. Naturally, the aforementioned acquisition activities that the company engaged in led the way. Meanwhile, EBITDA is forecasted to be between $915 million and $935 million. If we assume that other profitability metrics will grow by as much as EBITDA has been forecasted to, then we should anticipate net income of $494.6 million and adjusted operating cash flow of $670.7 million.

Author – SEC EDGAR Data

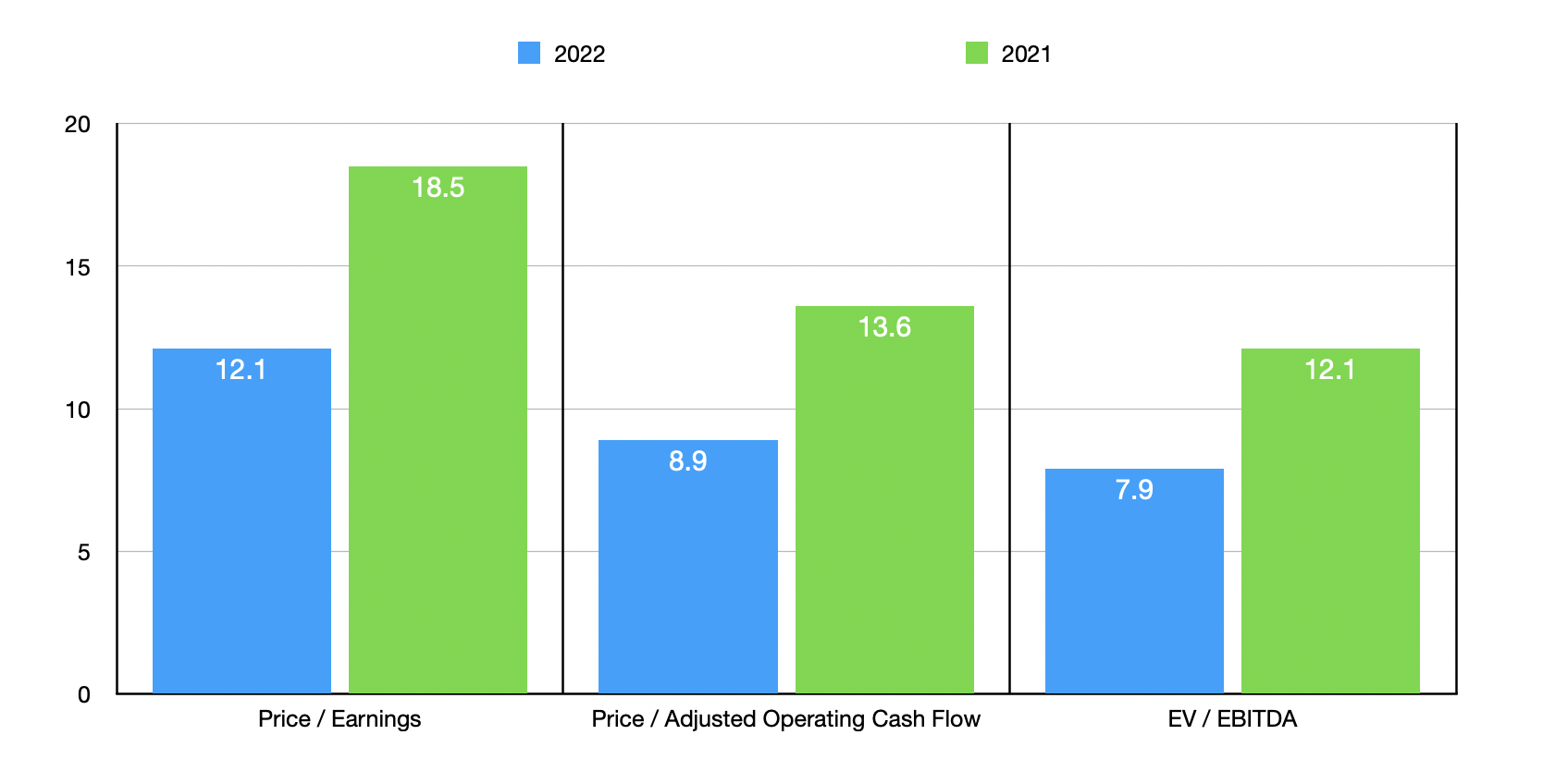

Based on these numbers, the company should be trading at a price-to-earnings multiple of 12.1. The price to adjusted operating cash flow multiple should be considerably lower at 8.9, while the EV to EBITDA multiple should be roughly 7.9. Even if we assume that the company experiences weakness moving forward and reverts back to what it generated in 2021, it’s hard to imagine shares being considered overvalued. As you can see in the chart above, these multiples in that instance would be 18.5, 13.6, and 12.1, respectively. Also, as I do with most companies that I analyze, I decided to compare TopBuild to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 12.1 to a high of 23.5. In this instance, TopBuild was tied as being the cheapest. Using the price to operating cash flow approach, the range was from 13.4 to 25.8. In this scenario, our prospect was the cheapest of the group. And finally, when it comes to the EV to EBITDA approach, the range should be 7.1 to 14. In this scenario, only one of the five firms was cheaper than our target.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| TopBuild | 12.1 | 8.9 | 7.9 |

| Installed Building Products (IBP) | 16.0 | 13.4 | 8.5 |

| Masonite International (DOOR) | 12.1 | 14.0 | 7.1 |

| CSW Industrials (CSWI) | 23.5 | 25.8 | 14.0 |

| JELD-WEN Holdings (JELD) | 19.2 | 25.7 | 8.3 |

| Gibraltar Industries (ROCK) | 17.8 | 20.3 | 10.9 |

Takeaway

From the data at my disposal today, it seems to me as though TopBuild is doing quite well for itself. Yes, I do understand that there could be some uncertainty moving forward because of broader economic concerns, the most significant of which could be the impact that interest rate hikes will have on this market. But in the worst case, I cannot imagine the company being considered any worse off than fairly valued. And in the best case, strong performance moving forward could push shares even higher. Because of this, I have no problem keeping the company rated ‘buy’ like I had it at previously.

Be the first to comment