memoriesarecaptured

Shares of Tootsie Roll (NYSE:TR) have significantly outperformed the broader market thus far in 2022 with shares up more than 15% year-to-date. The company has seen a sharp increase in revenue and operating profit as the pandemic has waned and consumers have stocked up on Halloween candy.

While the return of trick-or-treaters has been a boon for Tootsie Roll in 2022, the long-term outlook is for slow growth in revenue and operating profit. Despite an unexciting fundamental outlook, shares trade at more than 25x operating profit suggesting disappointing future returns.

Overview

Tootsie Roll has a stable of iconic brands – in addition to Tootsie it owns Charms/Blowpops, Dots, Junior Mints, Charleston Chew, Sugar Daddy, and Dubble Bubble.

The company is controlled by the Gordon family who own over 50% of shares outstanding. While the confectionary industry has seen consolidation over the past couple of decades, there is no indication that Tootsie Roll will be sold.

Current Results

While the confectionary business is generally a very stable business (over the past decade Tootsie Roll has seen revenues increase or decrease less than 4% per year), Tootsie Roll suffered during the pandemic as social distancing protocols led to a decline in trick-or-treating. This caused a 10% decline in revenue in 2020.

Revenue rebounded 21% in 2021 and has seen a further increase in 2022. While 2021’s bounce-back was largely due to the return of normal consumer behavior, 2022 has seen a benefit from increased pricing as it has passed inflationary pressure on to customers.

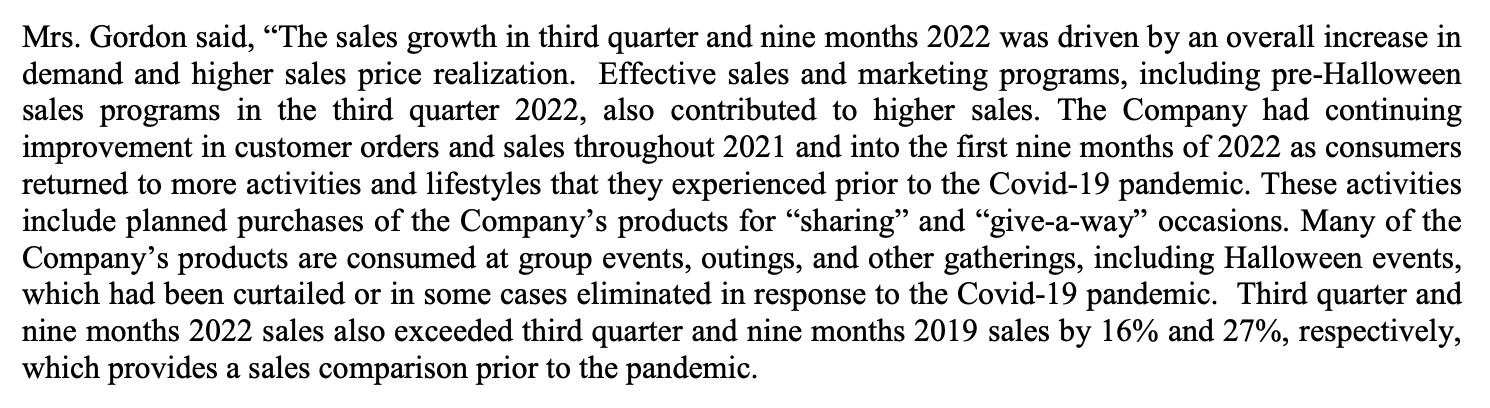

9 month results (Tootsie Roll 3Q Earnings release)

Historical Performance

While current results have been strong, Tootsie Roll actually saw revenue decline between 2012 to 2019 (last ‘normal’ year before pandemic impact). This is partially due to the low growth nature of the business as consumption of sugary sweets is growing below GDP in most developed markets as consumers eschew sugar in favor of healthy snacks

However, Tootsie Roll’s declining sales are in contrast to peers like Hershey’s (HSY) which grew revenue 2.6% annually during the period. Tootsie Roll appears to have lost market share over the past decade as it has been slow to introduce new products to market.

In fact, going all the way back to 1999, Tootsie Roll’s operating profit has been basically flat with expected 2022 results.

Valuation & Conclusion

As we sit today, Tootsie Roll trades at just over 25x 2022 expected operating profit and has a P/E ratio of about 40x. Despite having a long-history of zero growth in operating profit, Tootsie Roll trades at a significant premium to the overall stock market which trades at 16-17x earnings.

One of the reasons frequently cited for Tootsie Roll’s high valuation is that the company could be an acquisition target. As mentioned above, the company is family controlled and there is nothing to indicate a change to the status quo. However, for the sake of argument, let’s consider what Tootsie Roll might be worth to an acquirer.

Over the past decade, Tootsie Roll has generated operating margins of 14-17% whereas Hershey has achieved low 20s operating margins. Were we to assume that an acquirer could boost Tootsie Roll margins to 21%, this would imply that the stock is trading at about 19x operating profit (25x earnings). This is roughly equal to Hershey’s valuation of 26x 2023 estimated EPS suggesting limited upside even in what I consider to be a best-case scenario.

Conclusion

I see a very poor risk return for Tootsie Roll shares at current prices. At $41, shares appear to be pricing in an unlikely ‘best case’ scenario (an acquisition with the acquirer paying for all synergies). More realistically, Tootsie Roll trades at a significant premium to both the overall market and peer Hershey’s despite Tootsie Roll having an inferior long-term growth profile.

Be the first to comment