Michael Burrell/iStock via Getty Images

General Overview

For those amiss for money management ideas moving into 2023, the treasury market may be a good start. As 2022 comes to an abrupt close, its checkered record marked by conflict, inflation, and policy tightening has left many portfolios heaped in red ink. Yet, there are little signs of this abating into the new year.

Sovereign yield curves have put to shame any Tom Foolery inversion tactics once seen in the celebrated Top Gun movie. Negative 5g inverted dive? Just looking at the term structure of interest rates makes for perhaps just as entertaining viewing.

On the other side of the Pacific, Governor Kuroda has maybe caught on. His latest gambit, by extending target rates on the front end of the Japanese yield curve, has been a policy curve ball sending the Yen North, Japanese equity markets South, and Japanese investor funds shunning US treasuries for increasingly enticing yields back home.

It’s a ballsy move as the Governor of the Bank of Japan, whose term ends in April, seeks perchance some monetary stardom.

It leads us fittingly to our fixed income friend – Direxion Daily’s 20+ Year Treasury Bill 3x Shares (NYSEARCA:TMF). It’s a leveraged bet on the long end of the yield curve where future economic expectations weigh more than front-end ones related to monetary policy.

After a panoply of brutal policy hikes choking US equity markets, the likelihood of a recession moving into 2023 is pressing. A recession-driven dampening of aggregate demand is possibly grounds enough to stave off continued inflationary pressures.

That makes a continuation of those very policy hikes unlikely. Through a moderation of rates or even a gradual Fed policy reversal, yields are likely to go lower, forcing prices upwards.

In summary, if you are a believer in a recession scenario into 2023, then sovereign fixed income is prime stomping ground for returns. Accordingly, my outlook for rates, and Direxion Daily’s 20+ Year Treasury Bill 3x Shares, is positive.

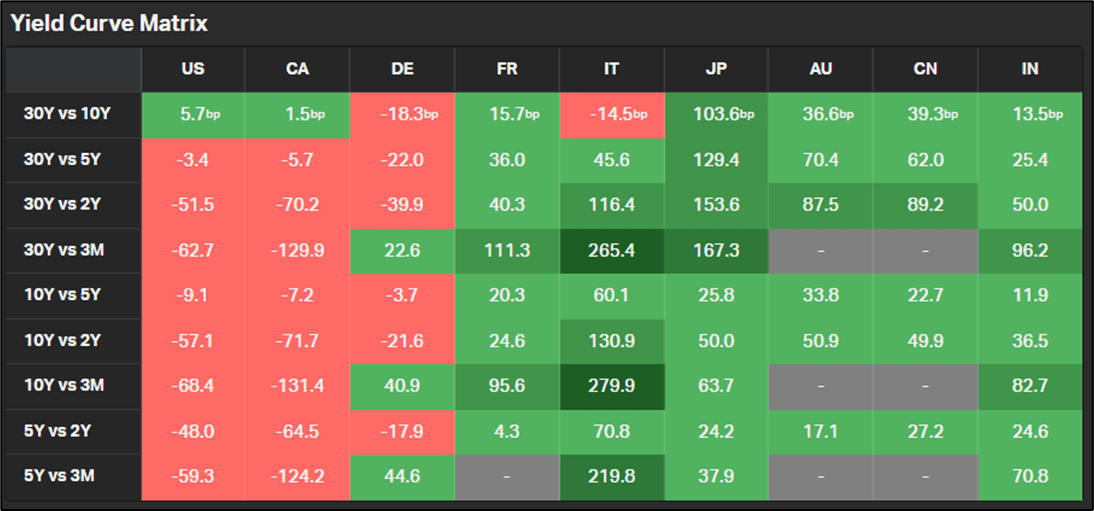

Koyfin

Yield curve inversion has been lasting and prominent in both the US & Canada

Product Overview

But hold on. A resoundingly positive outlook for the long end of the yield curve does not equate to a long holding of TMF. Like other leveraged plays, this here is a tactical trading tool for money managers to actively navigate the intricacies of interest sensitive securities only.

It’s a trading tool for near-term positioning or minor adjustments to a basket of risky assets. But in no way is this a buy-and-hold security.

Like other Direxion Daily products I have covered, this fund has sizable leverage. 3x to be precise, delivered by a cocktail of OTC derivatives brokered between financial intermediaries.

Consequently, this package is exposed not only to counterparty risk, but the usual suspects commonly found in leveraged ETFs – such as daily resets and compounding. These are explicitly the very reasons that this package does not make a great long-term holding.

Product Structure

The ETF provides investors with 3x daily exposure to a basket of market value weighted US treasury bonds with over 20 years to maturity. One key word here is daily – with resets meaning this product will only imperfectly replicate those 3x returns.

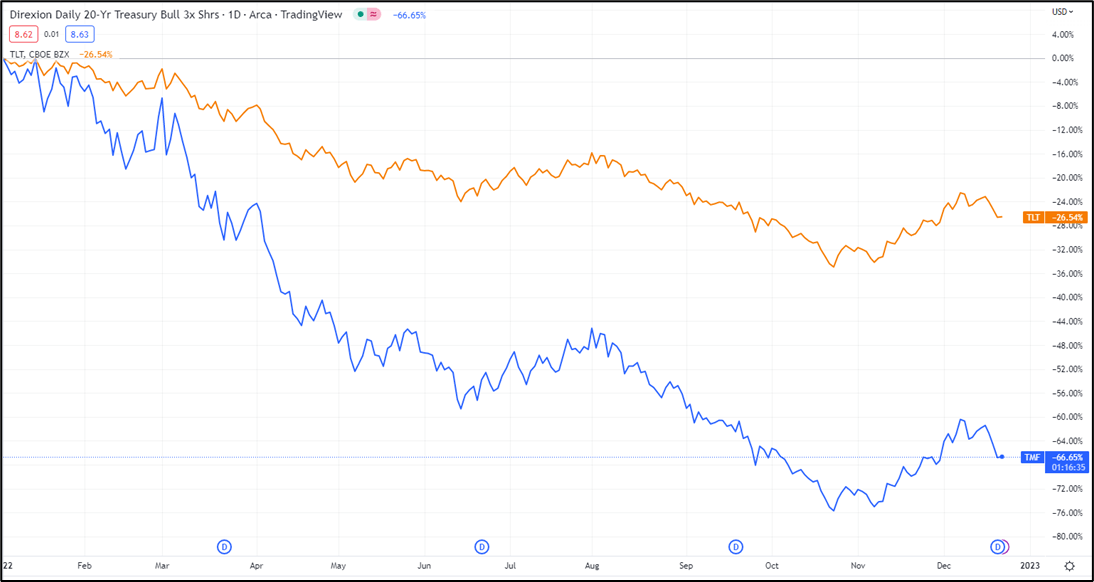

Take iShares 20+ Year Treasury Bond ETF (TLT) and chart it against TMF over any holding period and you will find that divergence exists between what theoretically should be 3x upside or downside.

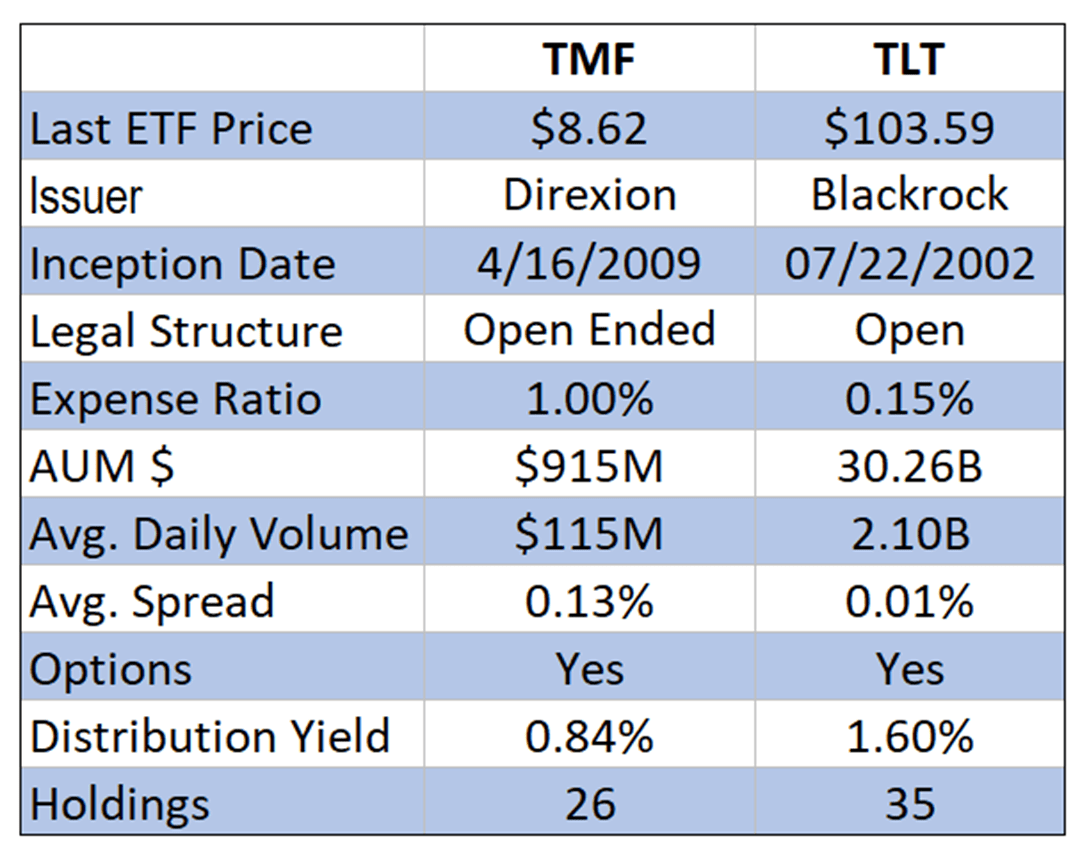

The $870M of assets under management are all logically made up of fixed income securities. Roughly 70% of the wrapper is made up of the fund’s big brother, TLT – an ETF fixed income staple needing little in terms of introduction.

Matched with this are a range of OTC derivatives, namely swaps used to provide leverage. Evidently, fund composition is heavily exposed to capital markets and fixed income treasuries, neither of which have had a bumper year. TLT is down some -28% year-to-date and represents the lion’s share of TMF’s losses (2,813 bps).

TradingView

Year-to-date price action TMF (-66.65%) v TLT (-26.56%)

Options are available to combine with a holding in TMF, making risk management more customizable. Traders can hold the ETF or engineer synthetic positions on options markets to replicate defined directional risk.

Like most leveraged funds, TMF charges a higher expense ratio and naturally has greater turnover given its short-term pedigree. Presently there is not much on the ETF market in terms of competition. Skilled traders could use TLT options markets and build their own TMF if need be.

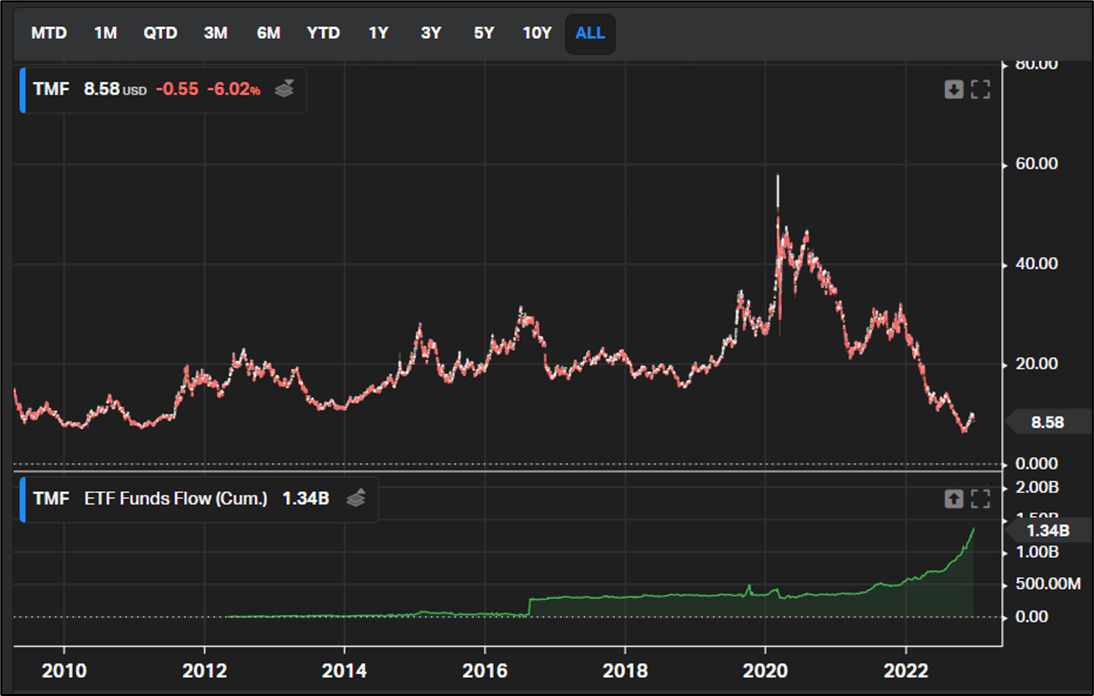

Koyfin

All time returns have shown a collapse in TMF’s price level while sustaining increased fund inflows.

The fund has seen a high degree of cash inflows – some ~$550M over the past 90 days as money managers prepare for an eventual easing of the barrage of rate rises seen in 2022.

Spreadsheet developed by author

Comparative analysis TMF vs. TLT

Risks

The risk register for this product is intrinsically linked to those seen in all leveraged products. Beyond leverage itself, the fund holds counterparty risk generated by how the package generates leverage.

As described earlier, daily resets and compounding also figure prominently. The US treasury market is considered risk free so here most of the fund’s risk exposure is linked to how the package is engineered, more so than the underlying securities.

Key Takeaways

If rates subside and a recession takes hold in 2023, it’s likely that equity markets will suffer. Over time, dampened demand will be cure enough for a multi-year inflationary spike, that Federal Reserve action will take a back seat.

Progressively as the Federal Reserve takes its foot off the rate-hiking accelerator pedal, the back end of the curve is likely to recede as treasury prices rise. There are little signs of a market boom into 2023, making fixed income markets, particularly on the long end perhaps a fitting place to be.

Be the first to comment