akinbostanci

The Quarter:

Tiptree (NASDAQ:TIPT) reported the second quarter a bit early today (August 8th). The conference call will be tomorrow morning. The quarterly results were a bit complicated due to the Warburg investment in Fortegra, the closing of the sale of a dry bulk ship, and some of the typical noise associated with Invesque.

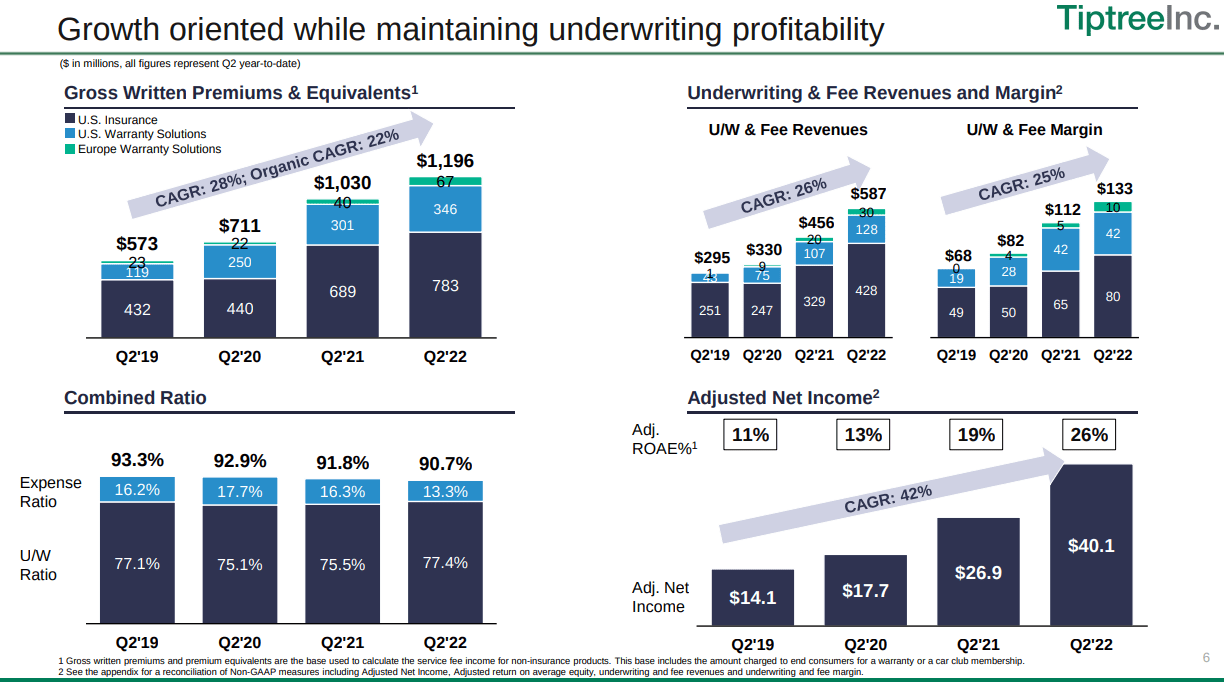

Fortegra is steadily becoming the only part of this company that matters. It is shooting the lights out. Unearned premiums and deferred revenue grew to $1.8Bn, a 26% increase year-over-year and underwriting and fee revenues increased to $301mm, up 21%. This revenue strength was followed by underwriting margin of $68mm, up 19%, driven by growth in U.S. Insurance and European lines and a combined ratio of 90.9% driven by excellent expense control. These metrics resulted in an Adjusted ROAE of 24.5% for Fortegra’s Q2 and 25.5% YTD, which should make any insurance company investor drool. They are simply magnificent returns and are the reason why I have been pounding the table for management to get rid of everything else and just focus its attention and the market’s on this crown jewel.

Bar Charts of Fortegra Operations (Q2 Tiptree Presentation)

There was some noise from the closing of the Warburg investment which resulted in a $63.2mm pre-tax impact to equity offset by a $39.6mm tax expense related to the tax deconsolidation of Fortegra, of which $25.5mm impacted net income. I’m not about to try to explain this charge. I hope the conference call does so for me. I just know it’s non-cash and is associated with Warburg making an investment in Fortegra at 2x book value while TIPT overall continues to trade at greater than a 50% discount to book.

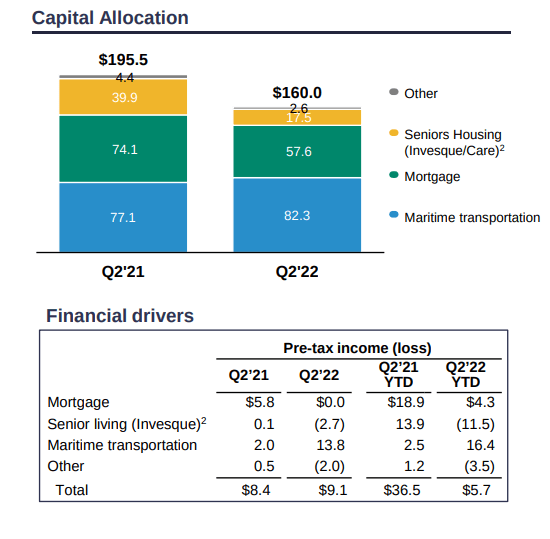

The mortgage business has dried up as can be expected with the rise in rates and Invesque resulted in yet another loss. The shipping business had a great quarter thanks to strong day rates and best yet the SALE OF BOATS. I look forward to the complete exit of shipping. As I have argued, Fortegra is a business that as a standalone gets a significant premium to book value and shipping is a business that gets a discount. There’s no reason to put an ugly sweater on such a beauty as Fortegra. I similarly look forward to the exit from Invesque, which remains P&L cancer.

Bar Charts of Tiptree Capital Performance (Q2 Tiptree Presentation)

Return on Equity and SotP

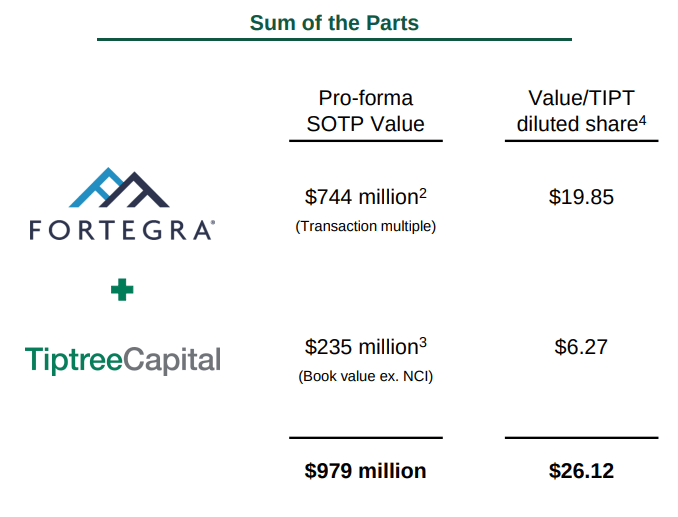

Even factoring in the lower profitability and returns at Tiptree Capital and a high (some argue too high) corporate overhead, the company sported a 12.3% adjusted ROAE for Q2 and 14.4% for the last twelve months. SotP (Sum of the Parts) continues to grow with Fortegra making up over 75% of the value. Moreover, with the closing of the Warburg investment, the company has eliminated its corporate level debt, derisking the business.

Tiptree Sum of the Parts (Q2 Tiptree Presentation)

Conclusion

It is taking a while, but this company is transforming into basically just standalone Fortegra. I wish the mortgage business had been sold last year and the shipping business were completely exited already, but the performance of Fortegra pretty much dwarfs any frustrations. There is almost a billion dollars over real equity value here priced at $420 million. Such an enormous discount is usually associated with businesses that are having real trouble or have risky balance sheets. The main economic driver here is growing revenue and double digits profits, the balance sheet is pristine, and the return profile is amazing. Let’s also not forget that Fortegra is the kind of bite size that any number of acquirers could scoop up, likely at a premium to what Warburg just paid. I continue to see upside to at least sum of the parts here.

Be the first to comment