landbysea/iStock Unreleased via Getty Images

Image: “Deepwater Horizon” offshore oil rig and Tidewater supply vessel.

Review of Share Price Action Over Last Seven Weeks

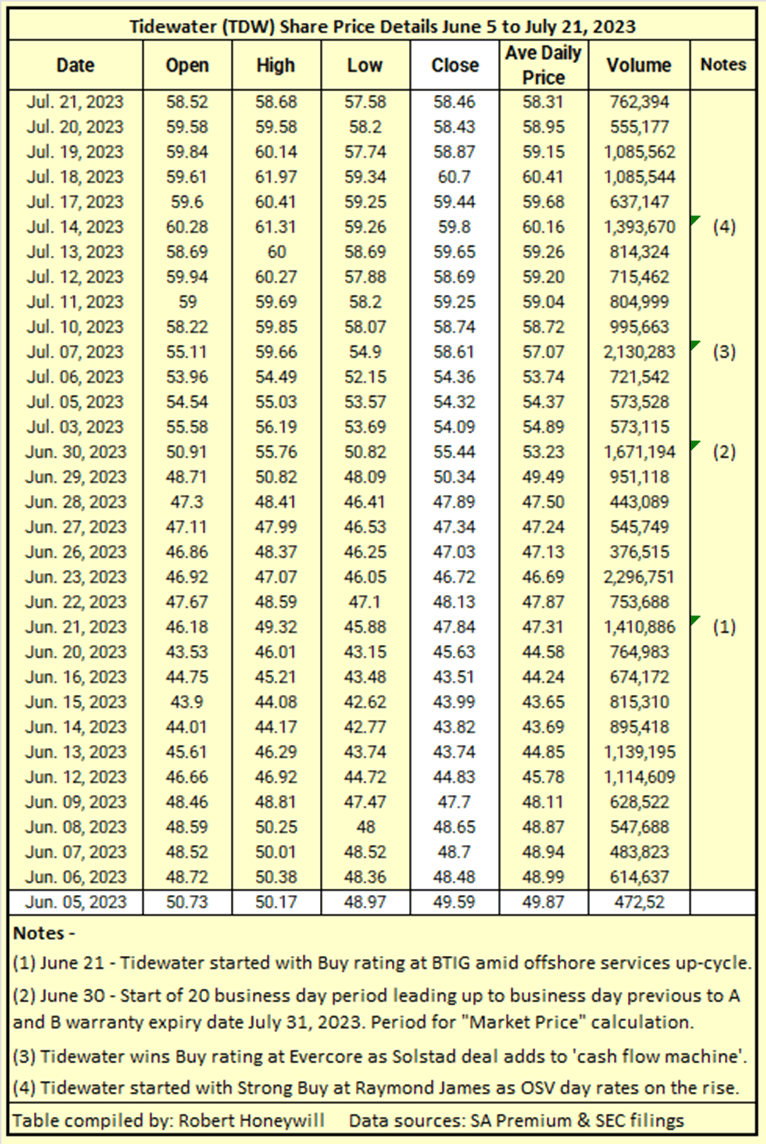

I believe a review of Tidewater (NYSE:TDW) share price movements over the last seven weeks is informative. In my June 5, 2023 article, “Tidewater: This Might Be As Good As It Gets“, I wrote:

Things might look very rosy at the moment, with strong oil prices having driven up day rates, but this might be as good as it gets. I rate Tidewater at best a Hold in the short term, with existing shareholders needing to keep a close eye on the future direction of oil prices and the impact on Tidewater day rates. I rate Tidewater a Sell for those wishing to exit around the high point for a cyclical business, and with a preparedness to possibly leave some money on the table.

At the time of publication of my June 5 article the Tidewater share price was $50.73 at open as shown in Table 1 below.

Table 1

SA Premium and SEC filings

Comments on Table 1 –

- Table 1 shows the share price firstly declined to a low of $42.62 on June 15, 2023 before trending back upwards to a high of $50.82 on 29 June, 2023, closing at $49.49 on that day.

- The stock traded as low as $50.82 on the following day, June 30, but was up $4.62 to $55.44 at end of day, and averaged $53.23 unweighted.

- Per Note 2, Tidewater has A and B warrants expiring on July 31. The June 30 date is 20 business days previous to the July 31 expiry date. The relevance of the 20 days, and why the July 3 share price might have increased $6.20 (13%) above the June 28 closing price of $47.89 is discussed in more detail below.

- Successive buy ratings have gone from BTG starting Buy rating on June 21, followed by Evercore Buy rating coupled with ‘cash flow machine’ comment on July 7, and one week later on July 14, Raymond James started with a Strong Buy as OSV rates are on the rise.

- The foregoing is all consistent with Tidewater doing well in a period of OSV rate growth and a policy of acquisitions to take advantage of that growth. But none of this is new information that was not available between June 5 and June 28 when the closing share price of $47.89 was still $2.84 below the price of $50.73 at time of publication of my article. So why did the share price suddenly take off? Below, I discuss whether there might be another factor driving share price growth subsequent to June 28.

Exercise of Tidewater Warrants: Potential Arbitrage Opportunity

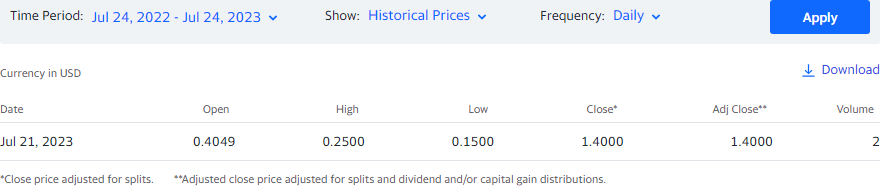

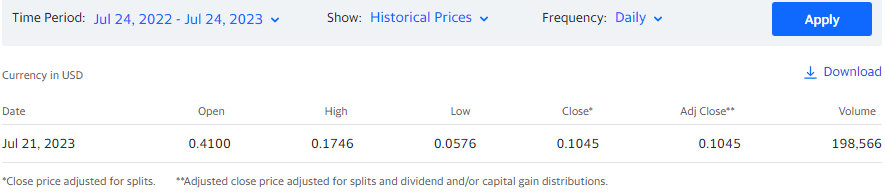

Both the Series A and B warrants expire July 31, 2023. The Series A are exerciseable at $57.06 and the Series B at $62.28. At the July 21, 2023 closing share price for Tidewater stock of $58.31, the Series A (TWD-WTA) are currently $1.25 in the money and the Series B (TWD-WTB) are well out of the money. Figures 1.1 and 1.2 below sourced from finance/yahoo.com show warrant transactions over the last 12 months.

Figure 1.1 Tidewater Inc. Series A (TDW-WTA)

Finance/Yahoo

Figure 1.2 Tidewater Inc. Series B (TDW-WTB)

Finance/Yahoo

It can be seen the only transactions in the last 12 months for both warrants, Series A and B, were on July 21, 2023 and volumes were small.

If the share price remains around the July 21 closing price of $58.46, then it can be expected all Series A warrants will be exercised at $57.06 through July 31, 2023, provided the holders have the necessary cash to provide with the exercise notice. If the holders either do not have the cash or do not wish to exercise the warrants and receive shares with a risk of share price decrease between exercise and receipt of tradeable stock, there is a cashless exercise option, based on a “Market Price”. How this works is explained in detail in a publication in the Investor Relations section of Tidewater’s website. Below is an extract from the publication in relation to exercise of Series A warrants (the wording for Series B is identical bar the exercise price of $62.28 versus $57.06 for Series A).

Tidewater Series A Warrants

Under the Warrant Agreement, Tidewater Series A Warrants (CUSIP number 88642R117) have an exercise price of $57.06. There are two methods of exercising the warrants: (1) a cash payment or (2) a cashless exercise.

- For a cash payment, you will wire $57.06 per warrant to receive one share of Tidewater common stock.

- For a cashless exercise, you will need to calculate the current conversion rate pursuant to the formula provided in the Warrant Agreement. The relevant provisions of the Warrant Agreement are included below. The cashless exercise formula is based on a “Market Price” which is the trailing average of the daily VWAP of Tidewater common stock as published by Bloomberg for the 20 trading days immediately preceding the date of notice of exercise; therefore, the formula is likely to fluctuate on a daily basis. Note that if the Market Price is less than the exercise price of $57.06, then the cashless exercise will result in the issuance of no shares of common stock and the forfeiture of your warrants.

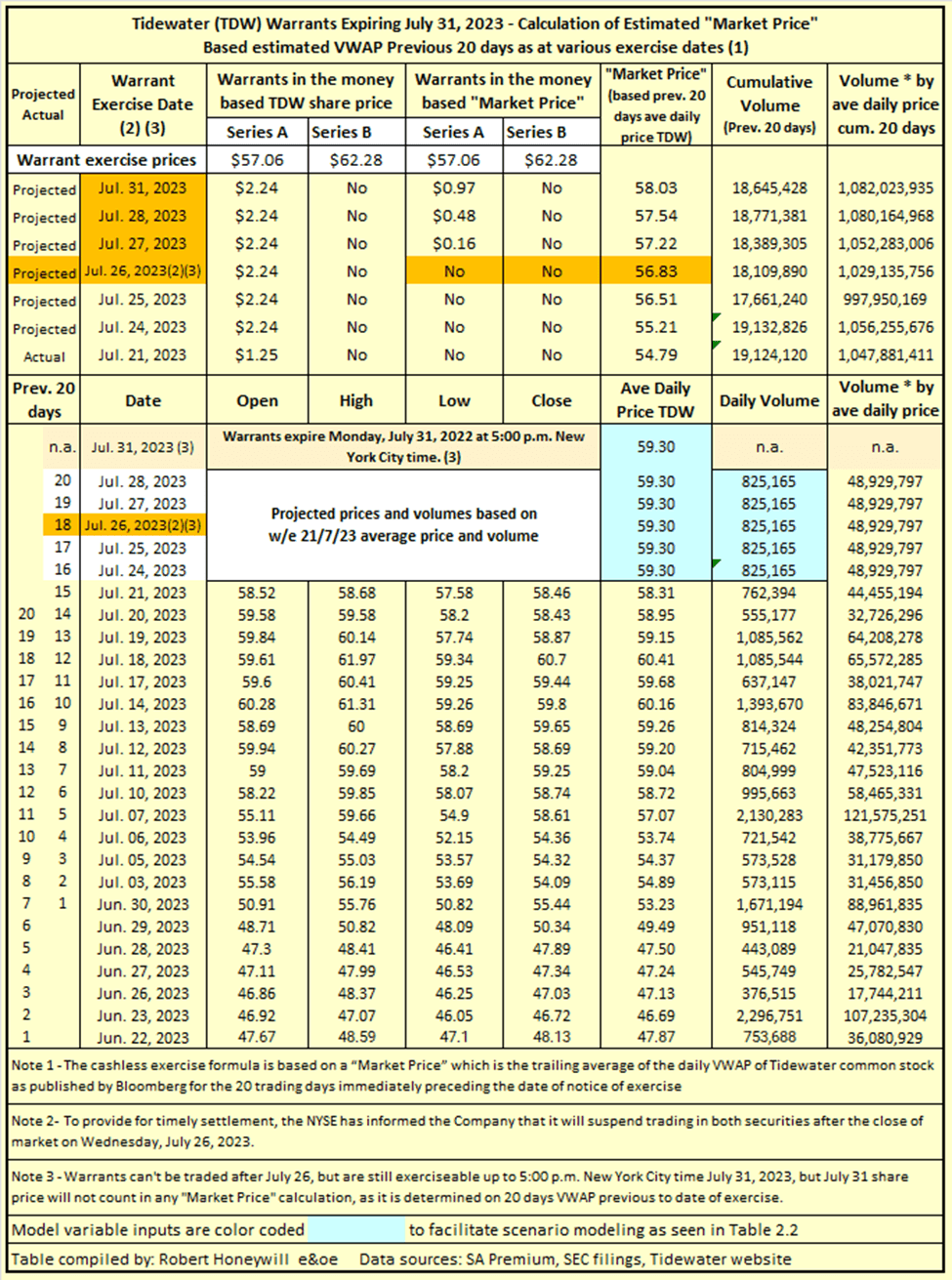

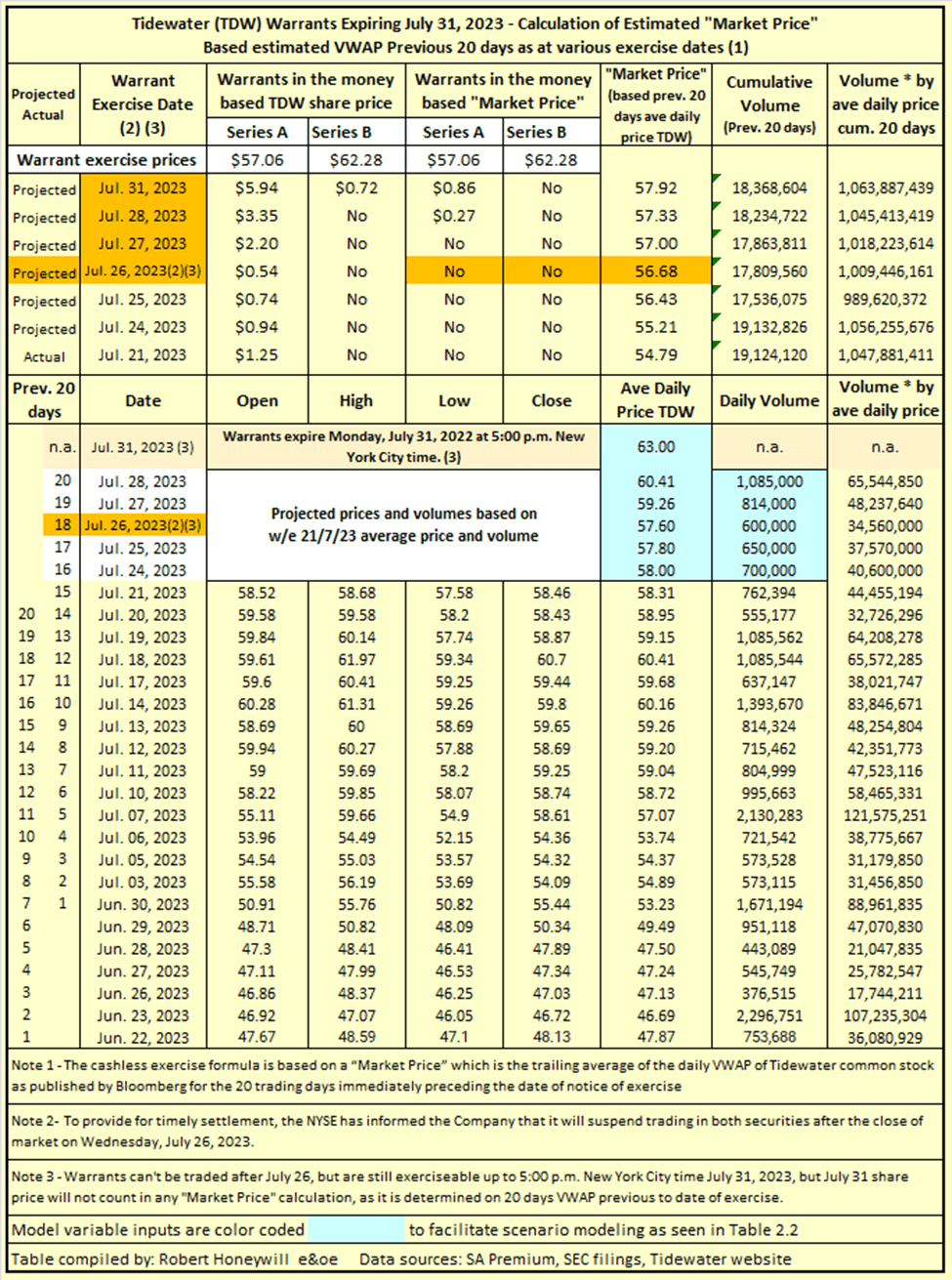

While a holder can exercise the warrants by paying cash at any time up until 5:00 p.m. New York City time on July 31, the cashless exercise is only available if the “Market Price” is above the exercise price of the warrant. As of July 21, 2023 the calculated “Market Price” has at no time been above the exercise prices of either Series A or Series B. That may change between July 21 and July 31, and Table 2.1 below shows one possible scenario.

Table 2.1

SA Premium, SEC filings, Tidewater website

Note: I do not have access to Bloomberg’s published VWAP for calculating “Market Price”. Instead I have used an average of daily opening, high, low, and closing share prices for TDW sourced from SA Premium, which is an unweighted average. These unweighted daily averages have been multiplied by daily volumes and the result summed for the 20 days over which the “Market Price” is calculated, and the resultant sum divided by the sum of the daily volumes for the 20 days, to provide an estimated weighted average “Market Price” for the 20 day period over which the “Market Price” is calculated. It is believed these estimates should be sufficiently close to actual “Market Price” calculations for the purpose of this exercise.

Available options for warrant exercise at July 21 –

Table 2.1 shows, at close on July 21, the Series A warrants were ‘in the money” $1.25, compared to the average share price for the day of $58.31. Series B’s exercise price of $62.28 was $1.97 above the July 21 average share price, so exercise at that price is not likely. The estimated “Market Price” of Tidewater shares at July 21 was below the exercise prices of both Series A and B, so cashless exercise was not available for either.

Available options for warrant exercise from July 24 through July 31 –

Cash exercise of warrants –

The blue colored cells in Table 2.1 are for entering estimates of TDW average daily share prices and volumes for the remaining trading days from July 24 to July 28 and for July 31, when the warrants expire at 5:00 p.m. NY City time. For the purpose of this exercise, I have input to the ‘blue cells’ average share prices and volumes, based on averages for the week ended July 21, 2023, for each remaining trading day through July 31. On this basis the Series A warrants ‘in the money’ value increases from $1.25 to $2.24, while the Series B warrants exercise price of $62.28 remains above the projected share price of $59.30. For Series A that leaves three options, (1) sell the warrants on market for a price that is likely well below the ‘in the money’ value of $2.24, (2) exercise the warrants with the hope the share price will remain above the exercise price pending availability of scrip to sell, (3) hold on and hope the “Market Price” increases sufficiently by July 31 to allow a cashless exercise.

Cashless exercise of warrants –

At the projected share prices and volumes, the estimated “Market Price” increases from $54.79 at July 21, to $56.83 at July 26, and to $58.03 at July 31. The July 26 date is particularly relevant because at the end of that day, trading in the warrants will be suspended. The projection shows the cashless exercise is not available at July 26. For a cashless exercise, that leaves only two options, (1) sell the warrants on market for cash at whatever price is on offer on the day of July 26, or hold on to the warrants through July 31, with the hope the cashless option will become available by then, but if it isn’t the opportunity to sell on July 26 will have been lost.

Indications Market Makers are at Work

Looking at Table 1 and Table 2.1, I have the perception the upward movement in Tidewater’s share price from June 30 onwards may have far more to do with market maker activity in relation to the exercise of the Series A warrants in particular, but maybe also the Series B warrants, rather than OSV rates and vessel acquisitions. After all, the share price had already had a strong run up from $42.81 at the time of Q1-2023 earnings release, to $50.73 at time of my June 5 article, and there does not seem to be anything in the public domain now that was not fully understood at June 5. If there is significant market maker activity in relation to the warrants, I believe it is useful to look at what pattern of share price movements we might expect from July 24 to July 31. On this basis I have changed the inputs in the ‘blue cells’ in Table 2.1 to create Table 2.2 with revised outputs.

Table 2.2

SA Premium, SEC filings, Tidewater website

The assumptions for average share price and volume for July 24 to July 28 are within the range of share price fluctuations in the preceding trading days leading up to July 24, so they appear to be quite achievable. The average share price assumption of $63.00 for July 31 has a lower likelihood of occurring, but it is certainly not impossible if we have further starts of Strong Buy announcements coming from additional analysts to those who have already given support to the TDW share price, arguably contributing to share price increases over the last few weeks.

Available Options From The Perspective of Various Parties at July 26, 2023 –

Series A Warrants –

Warrant holders – Based on the projections in Table 2.1, Series A, warrant holders might consider they have only two options at July 26, 2023, (1) sell the warrants on the market for whatever pennies they could get, considering the warrants are not ‘in the money’ for either a cash exercise or a cashless exercise, or (2) hold in the hope the share price will improve by July 31 to justify a cash exercise, with the risk the share price will fall back again before they are issued the shares to enable sale. Of course, if the share price did improve as shown in Table 2.2, it would be possible for a cashless exercise on July 31, but holders might not consider that a possibility at July 26.

The company – The company no doubt would want the warrants exercised to provide additional capital to facilitate further expansion of its OSV fleet. It probably goes without saying, the company would want to see the share price increase, quite apart from any desire to see the warrants converted.

Market Makers – Here I would include all parties who could gain from the warrant conversions, through provision of services for fee, or from trading in the Tidewater stock or warrants. Table 2.2 shows an opportunity to potentially buy a large number of warrants for pennies on July 26, in anticipation of placing the shares received at prices above the warrant buy price plus exercise price, ahead of exercise of warrants by July 31 expiry date. One might ask why not just buy the same quantity of shares and avoid the cost of the warrant – because the volume of shares available through purchase and execution of warrants is likely to be far greater than the volume of stock available on market at the same or similar price. And buying in those volumes on market would inevitably push up the share price well beyond the exercise price.

Series B Warrants –

Warrant holders – The Series B warrant holders will find themselves with similar options to those listed above for Series A holders, except their options are even less attractive. It would likely come down to selling on market, subject to there even being offers to buy at any price.

The company – Similar comments to those for Series A warrants apply.

Market Makers – An opportunity to acquire a large quantity of stock for placement, at a likely negligible warrant price, thus allowing undertaking of market making activities, placing stock at prices above known exercise price, ahead of exercise of warrants by July 31 expiry.

Tidewater Upcoming Q2-2023 Earnings Release

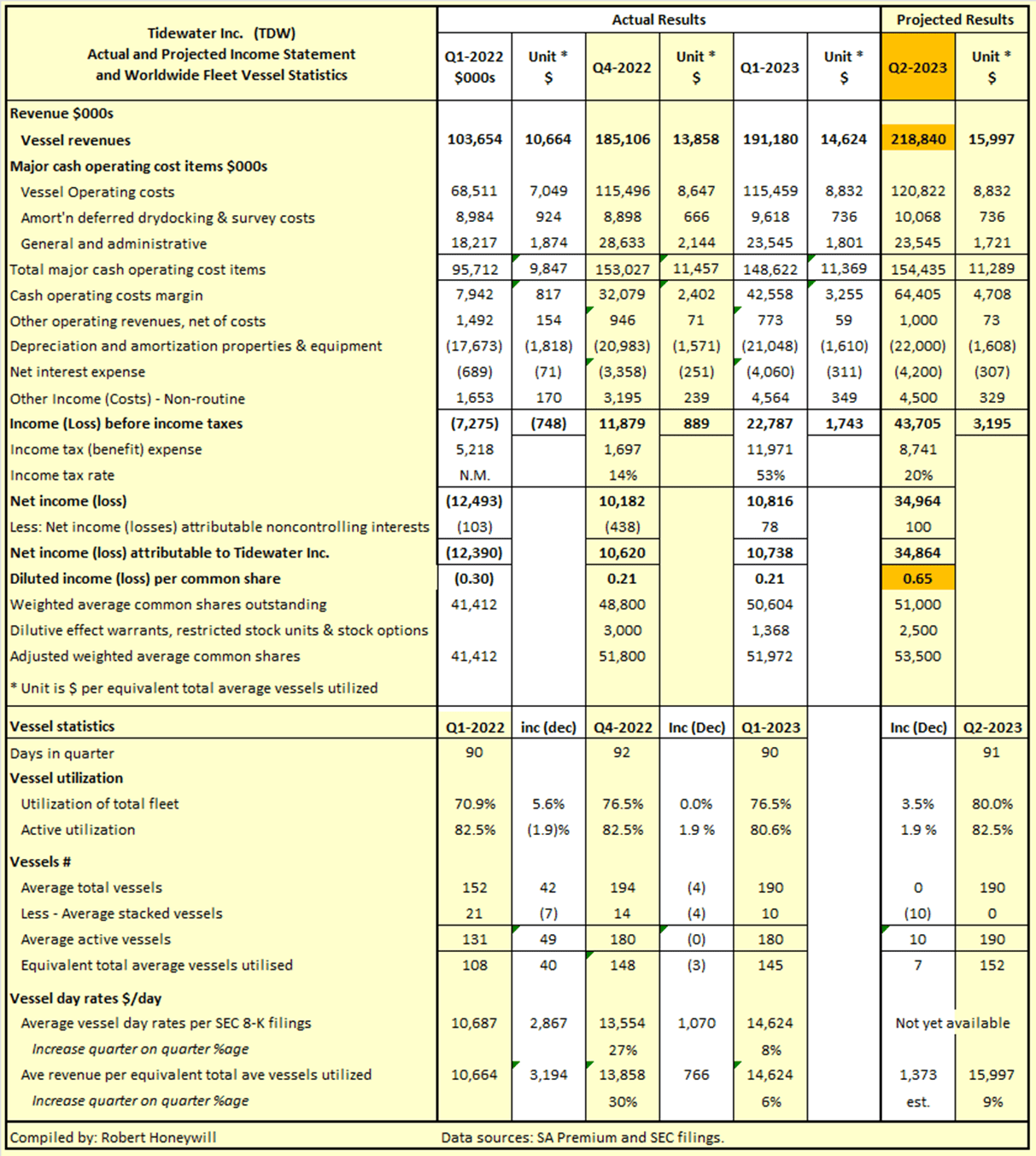

In considering the future direction of Tidewater share price, it is relevant to consider the impact on the share price of a beat or a miss on revenue and/or EPS in the upcoming Q2-2023 earnings release due August 8, 2023, post market. In my June 5 article, linked above, I argued the consensus EPS of $3.23 for 2023 was insufficient to justify a share price of $50.73. I will not repeat all of the arguments here, except to say that a P/E ratio of ~18.0 for a business in an industry that has a history of extreme volatility and recent wholesale bankruptcies is far too high. Even if the EPS increases further in 2024 and 2025, and there is no certainty of that, there has to be concern of the effects of another downturn in the industry in subsequent years. In addition to an excessively high P/E ratio, I do have concerns analysts consensus estimates for EPS and revenue will not be met. In order to be able to better understand the reasons for a beat or miss, I have compiled Table 3 below providing projections for Q2-2023.

Table 3

SA Premium and SEC filings

The orange highlighted figures in Table 3, reflect SA Premium analysts’ Q1 2023 consensus estimates for Tidewater of revenue $218.84 million, and EPS of $0.65. The assumptions I needed to adopt to achieve these results required some that I feel are stretched. In order to achieve the revenue figure of $218.84 million I have assumed all 10 stacked vessels at the beginning of the quarter were fully active for the whole of the quarter. I have also assumed an increase of 3.5 percentage points in utilization of the total fleet, and I have increased the estimated average OSV day rate by $1,373 (9%) from $14,624 for Q1, to $15,997 for Q2. To achieve the EPS of $0.65 I have left variable and fixed costs in Q2 at similar levels to Q1, despite reported significant increases in crewing costs and availability. I have increased adjusted average weighted shares from 51,972 to an estimated 53,500, and this figure might be affected by warrant exercise outcomes. I intend to compare the above projections against actual results, to better understand reasons for a miss or a beat. A significant miss or beat for Q2 could have a large downward or upward impact on the share price following the announcement.

Summary and Conclusions

If one believes the recent increases in the Tidewater share price are entirely due to expectations of increasingly higher earnings due to higher OSV rates and continuing additions to the OSV fleet, then it is reasonable to expect the current share price level to be maintained and grow. However, if the increases are due in large part to market maker activity related to the exercise of warrants, then once that influence is no longer active, share price decreases are likely. I still consider the Tidewater share price is far above intrinsic value, but might increase further for a period ahead as reflected in Tables 2.1 and 2.2. I maintain the stock is more than fully priced at present, and therefore a sell, with the caveat, that it might become even more over priced in the period ahead. As regards the warrants, there appears likely to be an opportunity to buy Series A warrants at a very low price between July 24 and July 26, particularly on July 26. The potential upside is significant, with Table 2.2 projecting $0.72 receipt per warrant in exchange for a cashless exercise on July 31, with little downside risk, apart from the outlay to buy the warrants. The only outlay would be the purchase of the warrants which could be available for pennies. Alternatively, the Series A warrants could be exchanged for shares in a cash exercise, and sold at a gain of ~$2 to $6 based on the assumptions in Table 2.2, but with a greater attendant risk than the cashless exercise. It is likely only parties such as market makers could consider the purchase of Series B warrants, as it is fairly inconceivable there would be a cashless exercise become available, and a cash exercise would require upfront cash outlay, with significant risk of share price fall before any sale could be executed. I understand a market maker would have the ability to place Tidewater shares at a known price, at or before entering into a commitment to acquire the warrants and/or undertake a cash exercise of the warrants for conversion to shares. It will be possible to monitor average daily share prices and volumes from July 24 through 26 to better discern likely outcomes through the balance of the period to warrant expiry on July 31.

Be the first to comment