D4Fish

Article Thesis

Snowflake Inc. (NYSE:SNOW) is a fast-growing company with market growth tailwinds. But despite the fall in its share price, shares remain very expensive, especially when we look at GAAP results instead of adjusted results. Investors thus shouldn’t get greedy yet, as I believe that Snowflake is not a good investment yet. In the current interest rate environment where investors can get risk-free returns of 4% and more via treasuries, paying 300x forward profits for a company like Snowflake does not seem like a great deal.

Snowflake: Compelling Business Growth

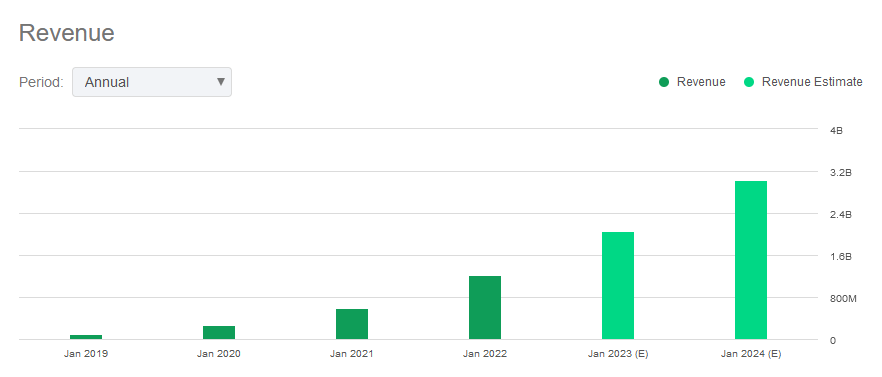

Snowflake Inc. is a cloud-based data platform company that offers services to its customers that help them visualize and integrate data via cloud-based solutions. This helps Snowflake’s customers in areas such as decision-making, sharing data and data-driven insights, and so on. This is helpful and useful for customers and it benefits from the cloud computing megatrend, thus it is not too surprising to see that Snowflake has done well when it comes to growing its business in recent years:

Seeking Alpha

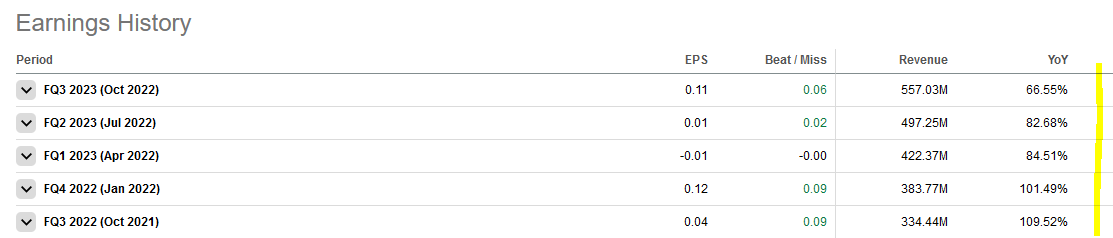

Revenue exploded upwards between 2018 and 2022, and revenue growth for the current year (which ends in two weeks) and for the upcoming year is forecasted to be compelling as well. On the other hand, it is pretty clear that relative growth is slowing down: While revenue growth was 109% one year ago, the company’s revenue growth rate slowed down to 67% as of the most recent quarter. While that is still outstanding, it’s a meaningful deceleration versus the relative growth rate Snowflake has showcased one year earlier. For the upcoming fiscal year, Wall Street analysts are currently predicting a revenue growth rate of 47%, which will mean another substantial decline in Snowflake’s business growth.

This has to be expected, however. Mathematics guarantee that maintaining an extremely high growth rate forever is impossible — doubling annual revenue becomes harder and harder, the larger a company becomes. Eventually, it’s impossible. The law of large numbers guarantees that business growth will slow down further, as maintaining a revenue growth rate of 40% eventually becomes impossible as well. While that does not have to be a disaster — many stocks have performed well over prolonged periods of time with revenue growth of well below 40% — investors should be clear about the fact that Snowflake’s historic growth will not repeat in the future. In fact, analysts predict that revenue growth will slow down further in the following years — 41% in the year ending January 2025, and then eventually dropping to around 20% by the fiscal year that ends in January 2028, five years from now.

Based on the fact that relative business growth has to slow down over time due to the law of large numbers and since the market does not grow at a very high rate forever, and due to the fact that a growing market will attract competitors over time, I believe that these expectations seem pretty reasonable. Snowflake will continue to deliver above-average revenue growth for the coming years for sure, but it is, I believe, highly likely that we will see ongoing declines in Snowflake’s revenue growth rate — a trend that has clearly been in place for a while already:

Seeking Alpha

Of course, declining business growth does not necessarily translate into problems for the stock. First, revenue growth will remain attractive, despite the fact that the relative growth rate will decline. On top of that, earnings growth and revenue growth do not necessarily go hand in hand — it is possible that a company generates earnings growth that is way higher than its revenue growth rate, e.g. due to margin improvements. This gets us to the next point, Snowflake’s profitability — or lack thereof.

SNOW’s Profitability

Snowflake recorded a non-GAAP or adjusted net profit of $0.11 for the most recent quarter. That’s $0.44 annualized, which would translate into an earnings multiple of 320. Those adjusted earnings back out a range of items, however, and one can argue that not all of these adjustments should be made. An important adjustment is the impact of share-based compensation. When a company issues shares to its employees and management, that is not a cash expense for the company. But it still is a real cost for shareholders, as their stake in the company gets diluted over time. On top of that, share-based compensation is not a one-time item, as companies issue shares repeatedly.

While many other companies offer share-based compensation to their employees and management team as well, and while many of those companies make the same adjustment when reporting non-GAAP results, the impact for an average company isn’t as large as it is at Snowflake:

Seeking Alpha

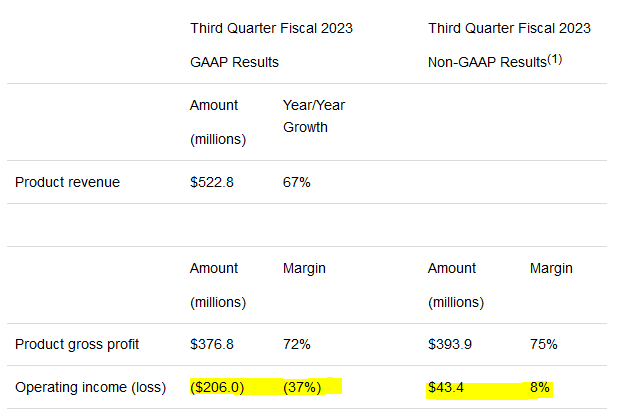

While Snowflake reports a reasonable, although far from spectacular, operating margin of 8% after making adjustments, its GAAP operating margin is pretty disastrous, at -37%. For every $1 in revenue that the company generated, it lost $0.37, before interest expenses and taxes.

Over the last year, Snowflake’s GAAP loss actually widened — the company lost $155 million in 2021’s October quarter, and $200 million in 2022’s October quarter, Snowflake’s most recent quarter for which an earnings report has been released. Growing the business is great, but when said business growth results in expanding losses, that’s not creating value for shareholders. It is also not what one would expect in terms of operating leverage — ideally, profits should improve meaningfully when revenue expands.

Looking at Snowflake’s share count, we see that the number of shares has risen from 303 million one year ago to 320 million as of the end of the most recent quarter. That makes for a 6% share count increase. When shareholders get an earnings yield of 0.3% (and that is generous, as we are using the non-GAAP number here), while the share count climbs by 6% per year, it’s hard to argue that this will be accretive for shareholders in the long run.

Of course, Snowflake could improve its margins over time, if it improves expense controls and when revenues keep rising. But even if profits rise dramatically, it’s hard to see how the earnings yield will rise above the annual dilution rate anytime soon. Analysts are currently predicting that Snowflake will earn $0.51 per share in the upcoming year — and that’s a non-GAAP number, thus SBC is already backed out. Even that does only translate into an earnings yield of 0.36%, as the earnings multiple for the upcoming year is 278 based on those estimates. If Snowflake continues to increase its share count at a mid-single digit rate, that’s not at all justified by the meager earnings yield, I believe.

In fact, Snowflake’s 6% share count increase over the last year pencils out to $2.4 billion in additional market capitalization at current prices. At the same time, Snowflake has only generated revenue of ~$2 billion over the same time frame. Issuing shares worth more than $2 billion to employees that generate less than $2 billion in revenue, while also paying additional employee compensation via cash payments, does not seem like a good deal for shareholders — although it seems like a good deal for employees and SNOW’s management team.

Don’t Be Greedy

While Snowflake is a company that generates compelling business growth, its relative growth rate keeps declining, and that trend will likely remain in place. SNOW will still generate above-average revenue growth for years, but investors shouldn’t expect that past growth rates will be maintained.

At the same time, there are major question marks when it comes to profitability — even when we back out share issuance, profitability is weak, and that is generous as share issuance results in direct costs for shareholders due to the dilution it causes.

While Snowflake has seen its shares pull back by more than 50% over the last year, it is far from a bargain today — it trades at 280x next year’s non-GAAP earnings still. I thus believe that shareholders shouldn’t get greedy here — the fact that shares are a way better value compared to one year ago does not mean that SNOW is a good value today. In an environment where risk-free treasuries offer yields in the 4% range, a 0.4% earnings yield from SNOW is not convincing.

Be the first to comment