AaronAmat/iStock via Getty Images

We ended a four-day losing streak yesterday with modestly positive returns for all the major market averages. There may still be a glimmer of hope for a Santa Claus rally after all, but I think it is dependent on the last major economic data report we receive this Friday before the stretch between the last five trading days of this year and the first two of next year begins. According to Dow Jones Market Data, that stretch has seen an average gain for the S&P 500 of 1.4% since 1950 and produced positive returns 79% of the time. That is what has come to be known as the Santa Claus rally.

Finviz

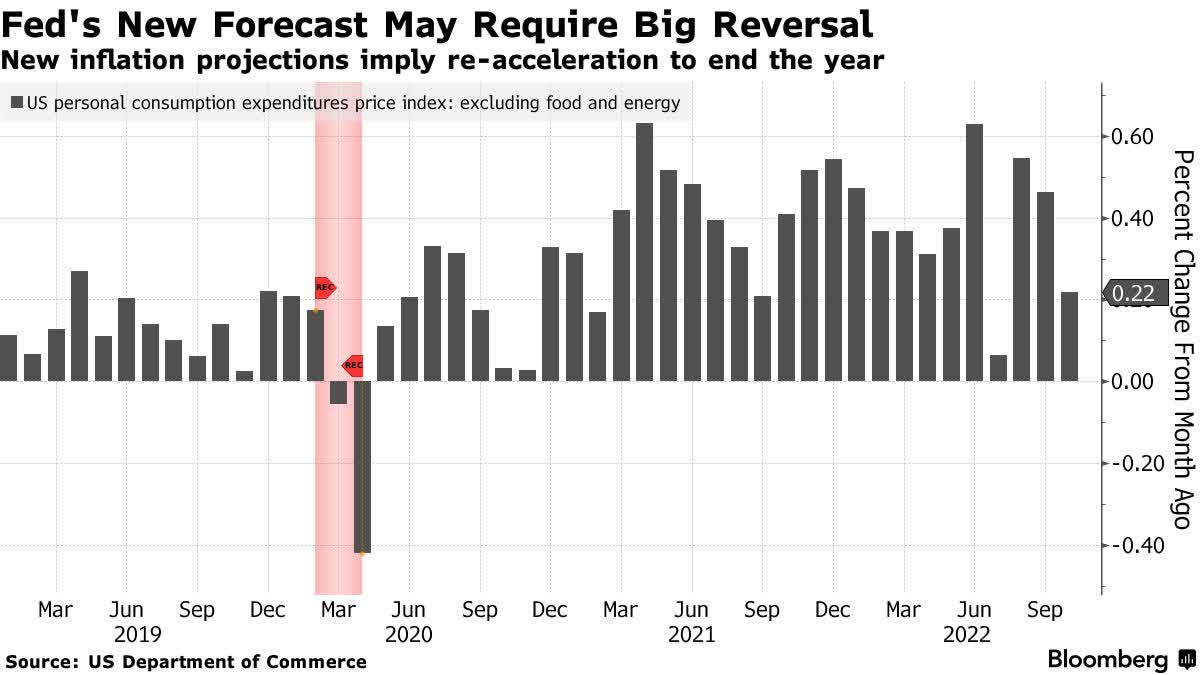

The number I am talking about is Friday’s release of the core Personal Consumption Expenditures price index (PCE), which is the Fed’s preferred measure of inflation. The PCE for November should be closely correlated with the Consumer Price Index for the same month, which was already released and surprised to the downside. The 0.2% increase for CPI likely means core PCE prices rose 0.1% for the same month. That should result in an annualized rate of 4.5%. We will have to wait until late January for the December numbers, but it is very unlikely that we will see a sharp upward reversal in either the CPI or PCE at year end.

Bloomberg

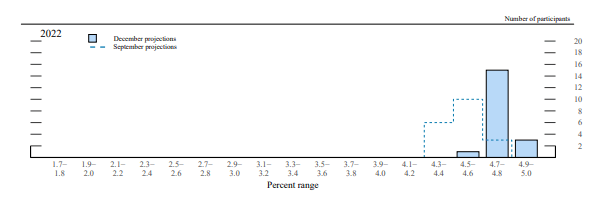

Yet that is what it will take to realize the Fed’s year-end inflation forecast. When the Fed released the update for its Summary of Economic Projections after last week’s meeting, it increased its estimate for the core PCE from 4.5% to 4.8%, as seen in the chart below. If the core PCE comes in at 0.1% in November after realizing an increase of 0.2% in October, it will take a jump of 0.7% in December to hit 4.8% for the year. I don’t see that happening.

Federal Reserve

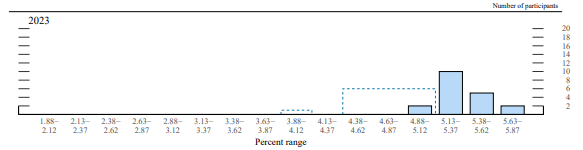

During Chairman Powell’s press conference that followed the meeting, he indicated that it was this higher starting point for 2023 that led to the upward revision in the terminal rate for Fed funds from 4.6% to 5.1%. It was that upward revision that sparked the 7% decline in the S&P 500 that we have seen over the past week. Why did the Fed not account for the lower-than-expected CPI print for November that arrived the day before its meeting concluded in its revision? I can only speculate that members were either too lazy to adjust their estimates or did not want to spark a rally going into year end that would further loosen financial conditions. My suspicion is the latter.

Federal Reserve

Still, if Friday’s PCE number is lower than expected, as was the CPI, then it should result in a much lower annualized number than 4.8%. We would have confirmation of that in January with the December number, which will come before the Fed’s next meeting on February 1. If the Fed’s increase in its 2022 core PCE forecast from 4.5% to 4.8% was the impetus for raising its peak Fed funds rate estimate for 2023, then a much lower starting point should lower it. Of course, markets will anticipate this well before the Fed’s next meeting, and it should be reflected in bond yields and risk asset prices well after a possible Santa Claus rally.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Be the first to comment