Paul Morigi

Introduction

This is my second article covering Occidental Petroleum Corp. (NYSE:OXY) and for the first time, I decided to look at the company beyond comparing it to some other peers.

At some point, I got interested in the question of why Warren Buffet chose OXY among others, somewhere even more efficient and cheaper companies. In my article today, I will try to look at the company through his eyes – as much as possible. And most importantly, I will try to understand whether it makes sense for retail investors to pay attention to OXY at its current price levels. Let’s dive in.

What’s So Special In OXY?

Founded in 1920 and headquartered in Houston, Occidental Petroleum is an international oil and gas exploration and production company with operations in the United States, the Middle East, and Latin America. Actually, the company is the largest independent oil producer in Oman and the second-largest oil producer offshore in Qatar.

By market capitalization, Occidental is one of the largest U.S. oil and gas companies.

Seeking Alpha

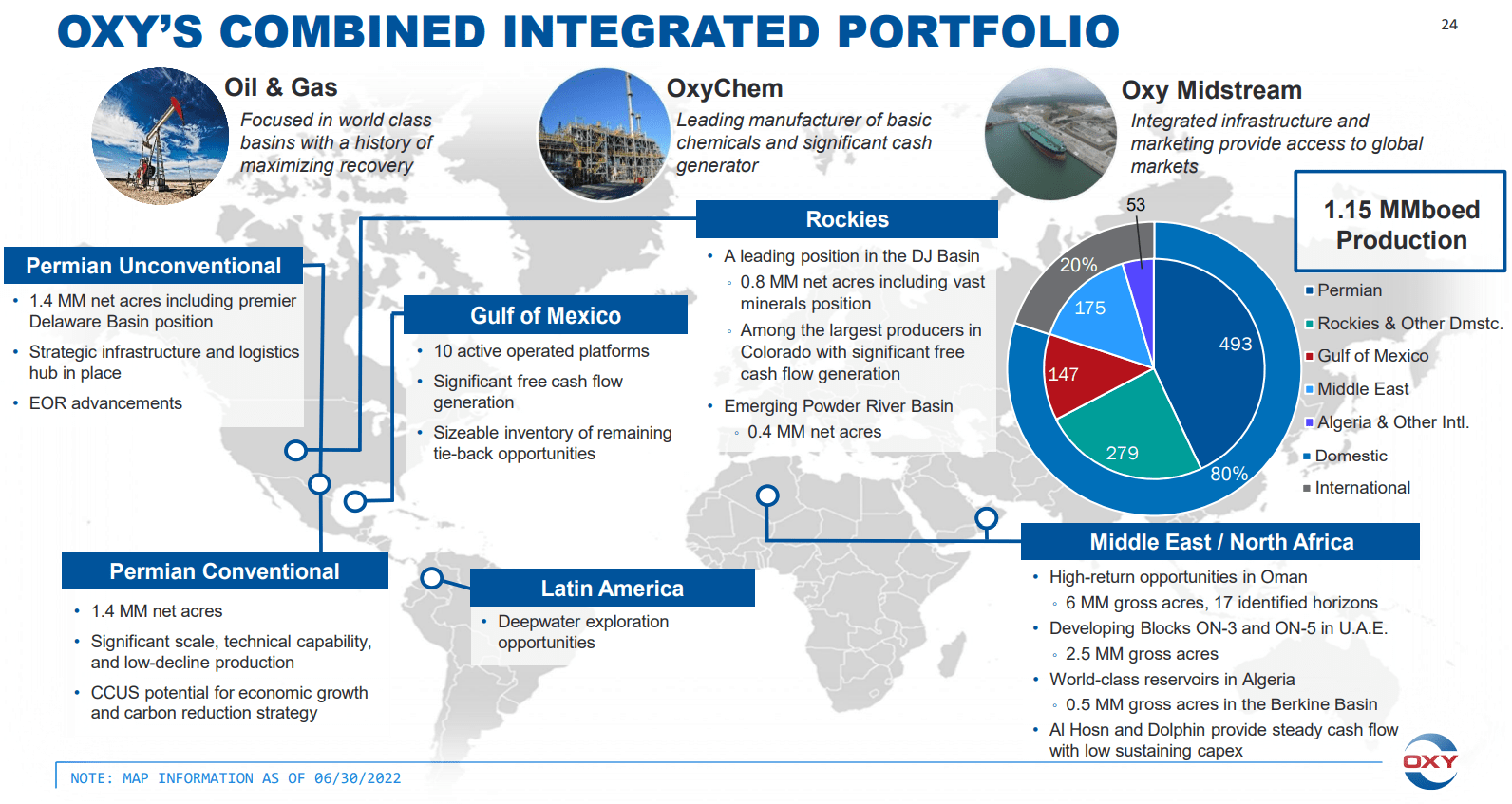

The company’s wholly-owned subsidiary, OxyChem, produces and markets color alkali products and vinyls. Occidental’s Midstream and Marketing segment (including the Low Carbon Ventures) gathers, processes, and markets hydrocarbons and other commodities.

OXY’s Q2 IR presentation

Occidental is a leading oil producer in the U.S., and a key player in the Permian Basin, with a significant presence in Texas and New Mexico. As we know, the Permian Basin is the driving force behind growth in U.S. oil production, having a bigger share of wells yet to be developed (63%), compared to rival basins and accounting for 60% of the total growth in the country. Over the past decade, production in the Basin has skyrocketed, increasing from 890,000 to 4.3 million barrels per day, more than double the growth rate of total U.S. crude production.

Bloomberg [author’s notes]![Bloomberg [author's notes]](https://static.seekingalpha.com/uploads/2023/2/6/49513514-16757441517038982_origin.png)

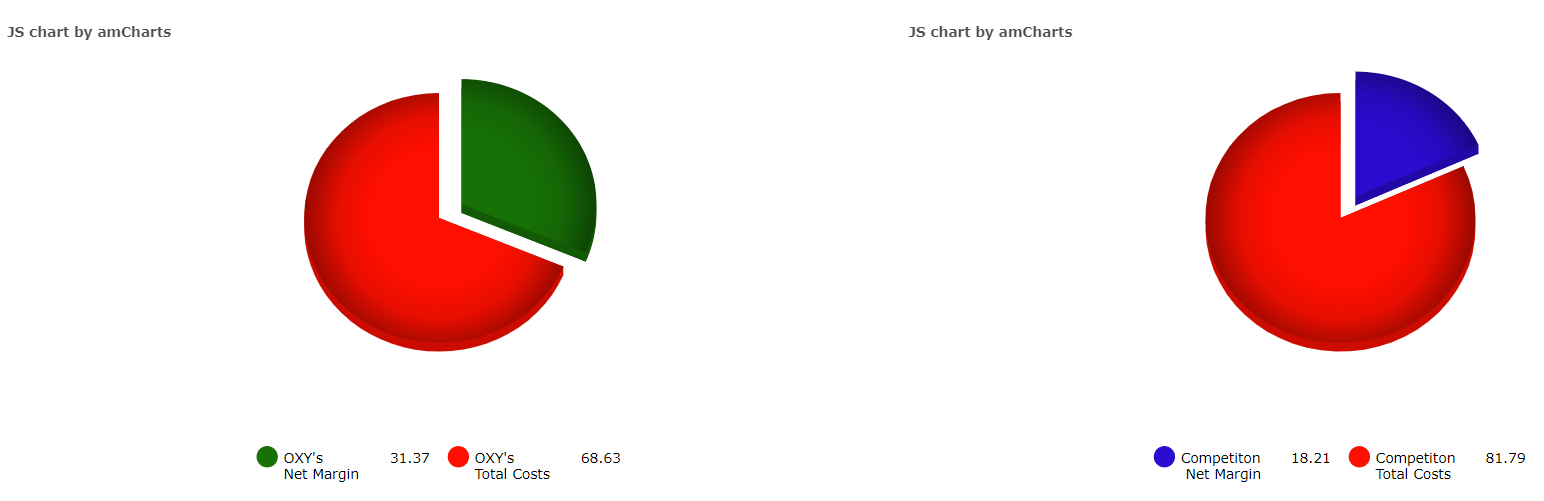

With Permian oil production appearing to reach its peak, this means oil prices will likely rise, giving a significant advantage to low-cost producers like Occidental. This allows – and likely will allow the company in the future – to keep its profit margins well above the market, as evidenced by CSIMarket.com’s study [based on Q3 2022 numbers]:

CSIMarket.com

As fellow contributor Nathaniel Petruska wrote in his recent article on OXY, the company’s competitive advantage depends on cost-effectively maintaining production by developing both conventional and unconventional fields and utilizing primary and enhanced oil recovery (EOR) methods in regions where Occidental has an advantage. And as we remember, the Permian – one of the treats of the U.S. – is such a place.

I think Permian has the proximity to our CO2 infrastructure, has the ability to both the sequestration and net 0 oil to enhanced oil recovery process. And so depending on where the customer’s preferences are for sequestration or net 0 oil, we have the ability to do both.

Source: OXY’s Q3 2022 Earnings Call

It is important to look at the integrated structure of the company as a whole – not only at the O&G segment. Here, Occidental Petroleum has a distinctive feature as well – its OxyChem’s market position is 1st or 2nd in the U.S. for the principal basic chemicals products it manufactures and markets, including chlorine, caustic soda, and caustic potash, according to EPCA.eu. On a global basis, OxyChem is the second-largest merchant marketer in the world of chlorine and the largest marketer of its co‑product, caustic soda.

OxyChem is planning to invest $1.1 billion in upgrading its Battleground plant [in Deer Park] from 2023 to 2026. I think this modernization may bring in more free cash flow thanks to improved margins and a boost in product volume once the commercialization begins by the 2nd quarter of 2026 – the company will extend the bull cycle of this segment due to this investment. It’s predicted that the project will add an extra $250-350 million to its incremental EBITDA while generating a strong return and improving its market standing.

In addition, thanks to the large federal spending towards reducing carbon emissions [the Inflation Reduction Act], Occidental plans to build 100 DAC facilities [Direct air capture technologies] that extract CO2 directly from the atmosphere] by 2035, up from 70 before, Reuters reports. The company noted that the total addressable market for CO2 removal is 10-15 billion tons per year to achieve net zero by 2050 and that DAC could potentially serve 5 billion tons per year of that market. OXY aims to reduce its net emissions by some 270 million tons over a decade through its DAC plants.

The above-mentioned long-term and quite expensive investments that OXY makes allow it to extend its business cycle while generating high margins due to its market position and a fairly attractive region of presence. Is not this exactly what Warren Buffett is always looking for in his investments, which he would prefer to hold “forever“?

On February 6th, the company communicated to investors that maximizing shareholder returns is their top priority. With the current uncertain global oil market, OXY can be patient and wait for stability before increasing production, instead choosing to use the available free cash flow for share buybacks, which reduces the number of shares available for purchase, leading to a higher return for shareholders.

It was free cash flow that at one point was dubbed “Warren Buffett’s metric” because of its importance in assessing the quality of a company’s operations. Given the size of Berkshire, I suspect that the world’s greatest investor was forced to look at that very metric among the largest and most liquid names. And there, OXY was simply unbeatable in terms of FCF generation capacity:

Goldman Sachs [2 February 2023] plus author’s notes![Goldman Sachs [2 February 2023]](https://static.seekingalpha.com/uploads/2023/2/7/49513514-16757507747033572_origin.png)

As you can observe, none of the comparable integrated oil and gas companies with a similar market capitalization have an FCF yield that matches OXY. This aligns with what is commonly seen among mid-cap or even small-cap companies, which tend to have lower liquidity and higher risk due to their smaller size.

As Goldman Sachs analysts write in their latest note [taken from ZeroHedge’s proprietary sources], for the past few months OXY stock significantly underperformed large-cap and super majors as investors have been concerned about the company’s capital spending plans for 2023, and expectations of downward revisions to its earnings forecast. However, OXY successfully reduced its debt in 2022 and plans to allocate its FCF in 2023 primarily to share repurchases and preferred equity redemption. The company is estimated to spend around $8.5-$9.0 billion in free cash flow, with roughly $3.8 billion going towards buybacks, ~$600 million towards dividends, and $3.4 billion towards preferred equity redemption, GS analysts say.

At a recent energy conference, management stated that its capital spending for 2023 would be around $5.7 billion, compared to $4.3 billion in 2022. This increase is primarily driven by the CAPEX on DAC plants, the expansion of the Battleground plant, increased spending in the Gulf of Mexico/Permian Basin for enhanced oil recovery, and the addition of a 3rd rig in the Rockies. But as I mentioned above, these costs are mandatory to extend the business cycle and protect the company from major legal/operational risks going forward.

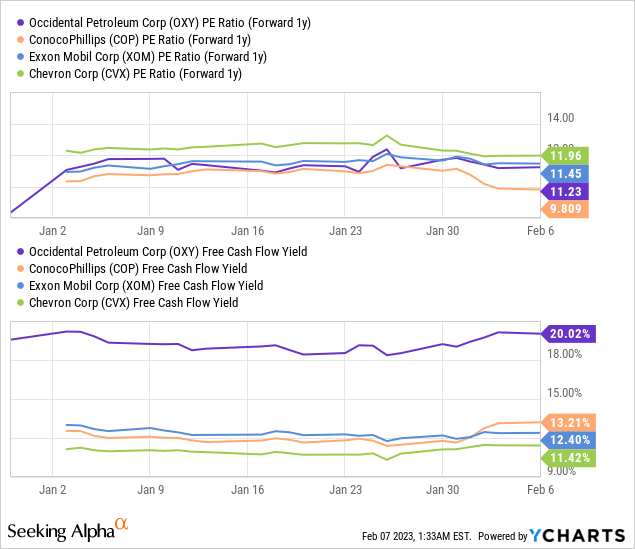

Despite OXY’s recent underperformance relative to peers, the stock currently trades at a 20% FCF yield, compared to 11-13% for peers like Chevron (CVX), Exxon Mobil (XOM), and ConocoPhillips (COP) – and with a 1-year forward price-to-earnings ratio that is only ~1% above the average for this particular sample:

Although Goldman rates the company as Neutral, the analysts see its risk-reward profile improving, and expected OXY to deliver total returns of ~32% to reach a 12-month price target of $81 per share. From what I see in terms of valuation and yields, I have no arguments against this finding.

Buffett’s $60 protection

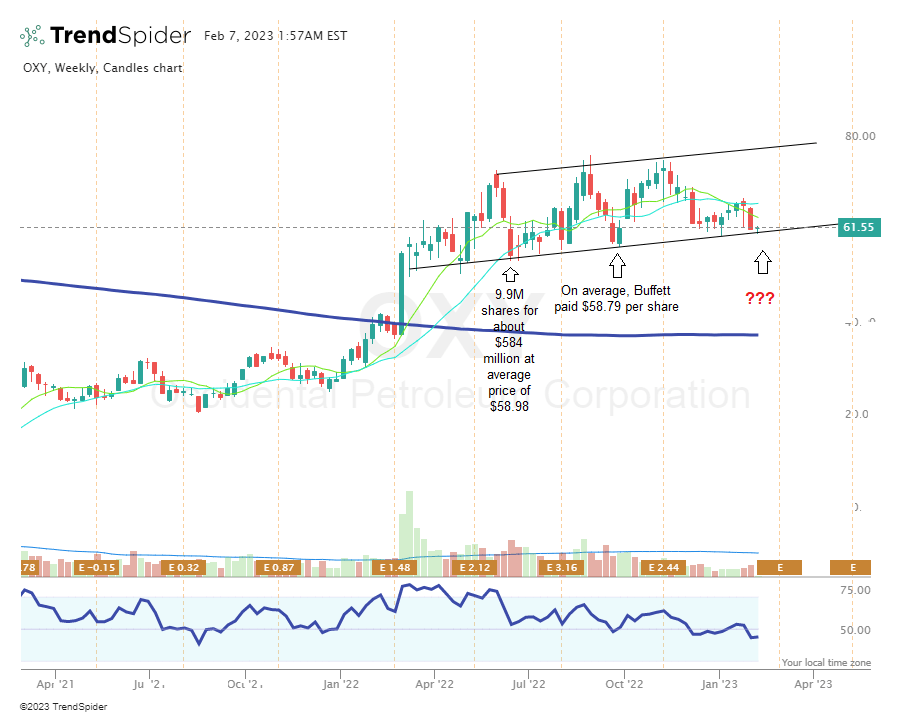

I am not a professional market technician, but I think I can understand from a chart why certain trading activities take place. Since the Q4 2021 earnings announcement by OXY in February 2022, the stock has formed a flag-like base after rising more than 45% in just one week. Since then, the stock has been in a sideways but rising trend, forming higher lows ($51.53, $54.3, $57.43, and $59.7) near the $50-60 mark, which can probably be called “Buffett’s protection level” since the price has not been able to break through this channel due to Mr. Buffett’s massive buying:

TrendSpider, author’s notes based on Seeking Alpha data

As you can see, OXY is now testing the support again near the “Buffett’s protection level”. Considering that the Federal Energy Regulatory Commission gave Berkshire Hathaway (BRK.B) permission on August 19 to buy up to 50% of the available OXY shares, I think it will continue to buy drawdowns below $60 per share, giving us – retail investors – some sort of margin of safety. Against the backdrop of the 20% FCF yield, the current situation almost guarantees a better risk/reward ratio in OXY stock compared to most other peers in the market.

Your Takeaway

In summary, I suggest that the real reason Warren Buffett bought the stock is the combination of Occidental’s distinguishing characteristics:

- the opportunity for good operational growth due to the size and geography of its operations;

- a shareholder-friendly and long-term approach to capital allocation – the ability to extend the business cycle;

- relative cheapness in terms of FCF generation capacity.

Of course, there are many risks that could prevent the realization of my thesis. For example, a global recession lasting longer than many expect could significantly affect oil demand and, consequently, Brent/WTI prices. OXY may suffer greatly against this backdrop. However, even if fear rules the market, I do not think Buffett will sell – he would rather increase his 21.5% stake.

So I concur with the conclusions of analysts at Goldman Sachs, who attest to a ~32% earnings potential for OXY. I recommend considering the stock for buying at current support levels.

Thanks for reading!

Be the first to comment