Dilok Klaisataporn/iStock via Getty Images

By Scott Welch

“I just dropped in to see what condition my condition was in”

(By Kenny Rogers & The First Edition, 1967)

When reviewing the current state of the global economy and investment markets, we recommend focusing on market signals and weeding out market noise. We believe the five primary economic and market signals that provide perspective on where we go from here are GDP growth, earnings, interest rates, inflation and Central Bank policy.

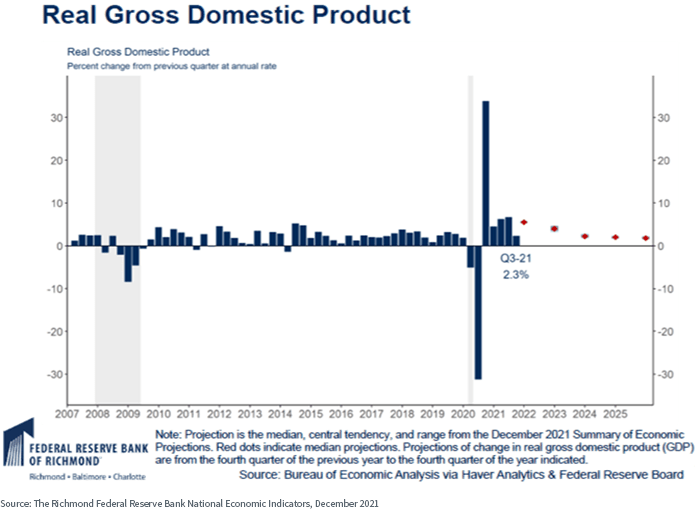

GDP Growth

While decelerating from the pace of 2021, U.S. economic growth is expected to remain reasonably strong in 2022, especially if (as we expect) COVID-19 moves increasingly into the rearview mirror. Consensus estimates for GDP growth in 2022 are ~4%.

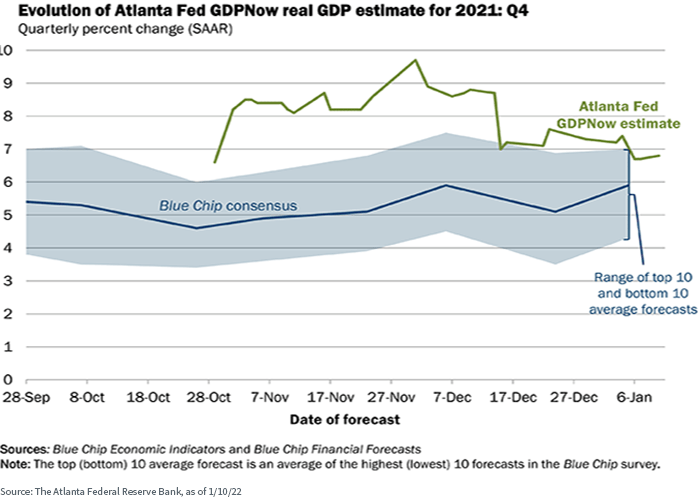

The Atlanta Fed “GDPNow” estimate pegs Q4 2021 GDP growth at a sizzling 6.8%. We see this as the potential start to another “economic reopening” cycle in the first half of 2022.

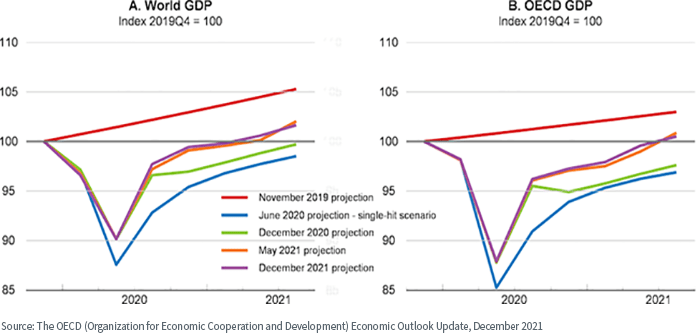

Global growth (focus on the purple line in the below charts) is expected to be generally positive as well. 2021 global growth came in at ~5.6%, and the estimate for 2022 is ~4.5%-5.0%.

Translation: A potentially volatile but generally positive environment for “risk-on” assets. There are several “known unknowns” to these economic forecasts, specifically:

- The ultimate outcome of the proposed “Build Back Better” plan (or, as is more likely, specific pieces of it)

- The continued evolution of the coronavirus pandemic and corresponding national, state and local responses

- Rising geopolitical tensions between the U.S., China, Russia, Europe and Iran.

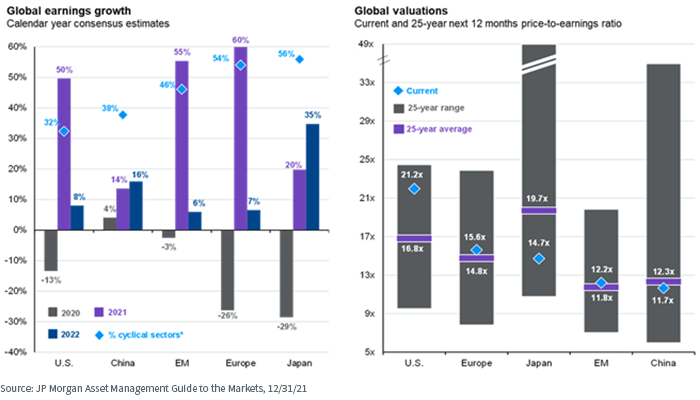

Earnings

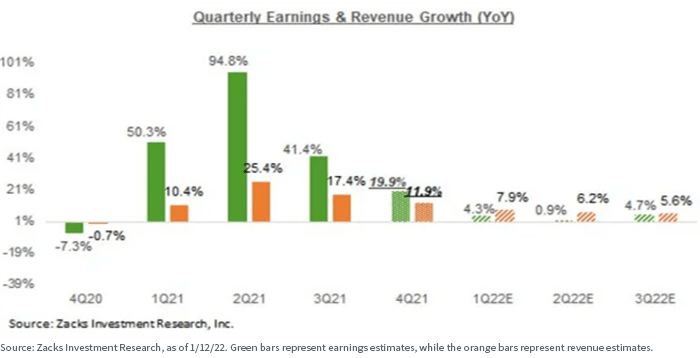

The U.S. Q4 2021 earnings season is just underway, and the outlook is for lower but still positive revenue and earnings growth.

Non-U.S. earnings are expected to be reasonably strong as well in 2022. Valuations outside the U.S. continue to look relatively attractive versus the U.S., especially in Japan.

Translation: A continued positive environment for global risk assets. We believe there will be a valuations “tug-of-war” between positive earnings and rising interest rates over the course of the year. We also believe “quality” (i.e., companies with strong balance sheets, earnings and cash flows) may become increasingly important as we sail into the potentially volatile seas of 2022.

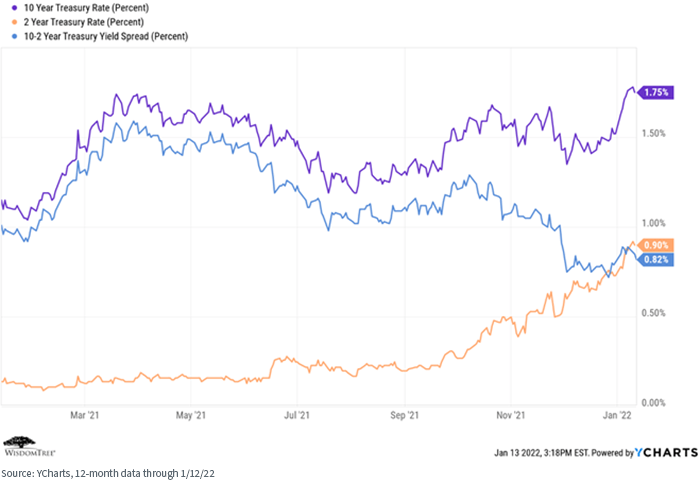

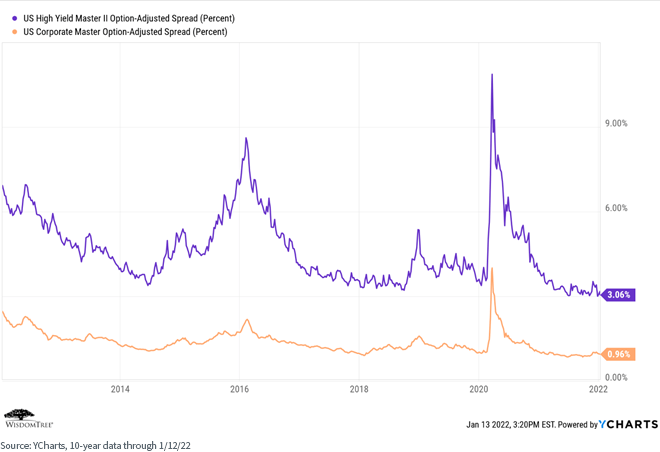

Interest Rates and Spreads

While rates have risen across the yield curve (a trend we expect to continue), the real action has been in the short end of the curve (orange line), as the market reacts to higher inflation and a more hawkish Fed.

Credit spreads remain tight (suggesting investor comfort with potential default rates) but are not out of line with historical levels. Quality security selection, however, remains critical.

Translation: We maintain our positioning of being under-weight in duration and over-weight in credit relative to the Bloomberg Barclays US Aggregate Bond Index, with a focus on quality security selection, especially in high yield. Corporate balance sheets are solid, so coupons should be relatively safe. We see potential pockets of opportunity in interest rate-hedged bonds (esp. high yield), floating rate Treasuries and alternative credit. But now is not the time to be taking excessive risk in your fixed income portfolio.

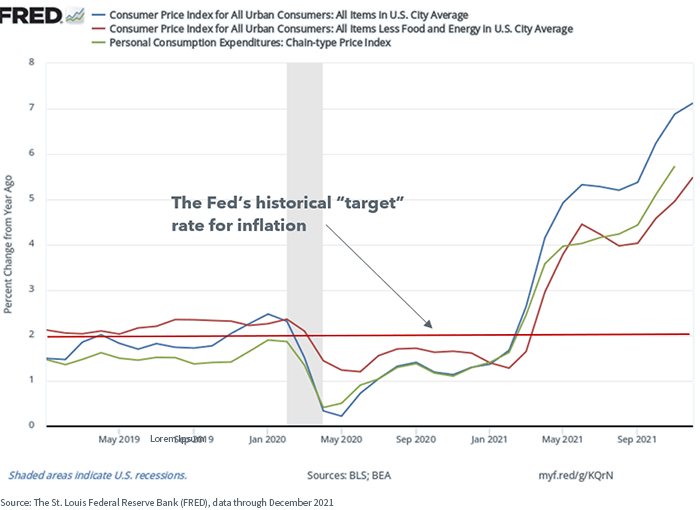

Inflation

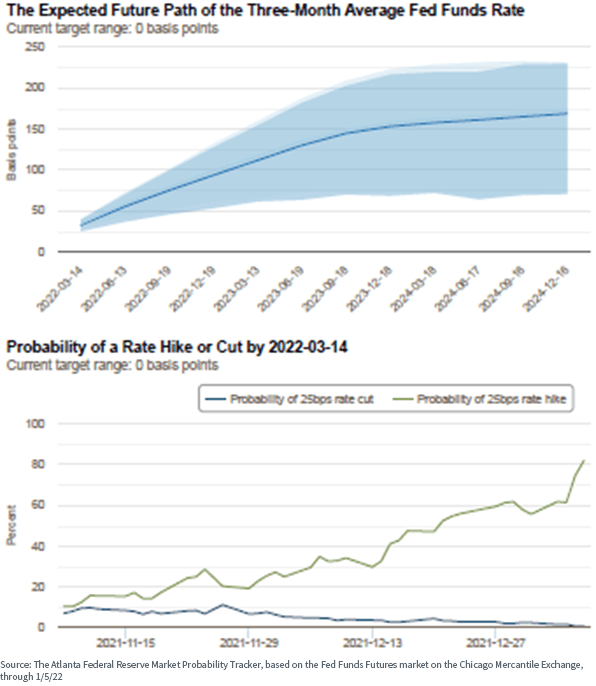

Inflation is the economic issue of the year-the Fed seemingly has turned more “hawkish” but perhaps waited too long. All eyes will be on Fed behavior and actions as we move through 2022. Three rate hikes are currently priced into the market-we think we might see four.

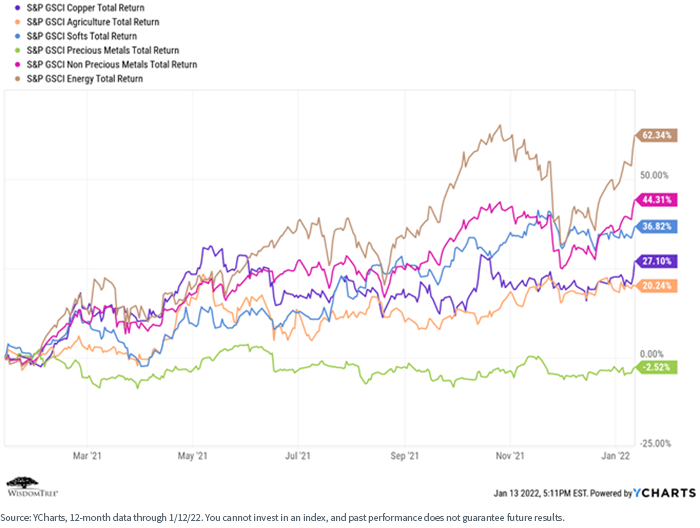

Global commodities are rising on expectations for an “economic reopening” regime in the first half of 2022. Even precious metals, after a generally poor 2021, have rallied recently as inflation fears grow.

Translation: Inflation is the story for at least the first half of 2022. The Fed is turning increasingly hawkish but must walk a “tightrope” between curbing inflation and throttling economic growth-it will not be easy. Stocks historically have provided a reasonable hedge to moderate inflation, and we also maintain our position in broad-basket commodities within several of our Model Portfolios.

Central Bank Policy

After perhaps waiting too long, the Fed has turned increasingly hawkish. The market is pricing in at least three rate hikes in 2022, and we believe there may be four. In addition, the Fed has signaled it may move as soon as March with its initial rate hike. Market volatility has risen as a result. The Fed Funds Futures market is now pricing in a 1.00% Fed Funds Rate by the end of 2022-we think it may end up even higher than that.

Translation: All eyes are on the Fed. Economic growth and corporate earnings are expected to be generally positive for risk assets, but the “counterbalance” is the direction and level of interest rates and the actions of the Fed as we move through the year.

Summary

When focusing on what we believe are the primary market signals, the “condition our condition is in” is something of a mixed bag. Economic growth and earnings are expected to be positive, COVID-19 and its variants should move to the rear-view mirror, and gridlock in Washington, DC, is usually positive for equity markets.

We do believe that “fundamentals” will matter again, and that we may enjoy another “economic reopening” market regime in the first half of 2022, which may favor value, small-cap, quality and dividend-focused stocks.

But inflation, interest rates, Fed behavior and legislative uncertainty all weigh on market sentiment. So, while we are cautiously optimistic in our outlook for 2022, we think we may be in for increased volatility. We continue to recommend focusing on a longer-term time horizon and the construction of “all-weather” portfolios, diversified at both the asset class and risk factor levels.

Scott Welch, CIMA, Chief Investment Officer – Model Portfolios

Scott Welch is the CIO of Model Portfolios at WisdomTree Asset Management, a provider of factor-based ETFs and differentiated model portfolio solutions. In this capacity, he oversees the creation and ongoing management of the WisdomTree model portfolio solution set. He is also a member of the WisdomTree Asset Allocation and Investment Committees. Prior to joining WisdomTree, Scott was the Chief Investment Officer of Dynasty Financial Partners, a provider of outsourced investment research, portfolio management, technology, and practice management solutions to RIAs and advisory teams making the move to independence. He remains an outside member of the Dynasty Investment Committee. He sits on the Board of Directors of IWI, the Advisory Board of the ABA Wealth Management & Trust Conference, and the Editorial Advisory Boards of the Journal of Wealth Management and the IWI Investments & Wealth Monitor. Scott earned a Bachelor of Science in Mathematics from the University of California at Irvine and an MBA with a concentration in Finance from the University of Massachusetts at Amherst.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment