ablokhin

This week as we take our trek on the Value Finder, we find ourselves in an unfamiliar place; a world with over a billion market cap.

Now, this particular world may seem scary, it may seem like something that a retail investor should shy away from, even run from when trying to build a small account, but fear not my friends, because the company is still plenty small enough for future growth.

Let me introduce you to it with a couple of metrics:

-

Forward P/E ~ 6.5

-

Dividend Yield > 8%

-

Price to Book ~ 1.5

-

Short Ratio > 15%

What high yielder is this?

Welcome to Franchise Group, Inc. (NASDAQ:FRG)

Company Description

FRG is a pretty easy company to understand. It basically is in the name, but to dive a bit further, here is what they do: They purchase franchised and franchisable businesses that they think are for sale at an advantageous price to make future profits. After purchase, they tweak the company to make more money.

It’s seriously that simple.

Think of Berkshire Hathaway for franchisable businesses.

As Nicolas Cage on SNL would say though, “That’s high praise”, so let’s check out what the whole company looks like.

Tenor

Moat

Well, we can run into our first potential problem here as there isn’t necessarily a true moat in FRG. Anyone can buy up other companies and try to turn a profit by using their resources, so the actual operations don’t present much of a moat. But after doing my research, I can say that the company does have a particular advantage, with its quality group of management that knows how to acquire the right fitting businesses and then increase efficiency.

FRG Presentation

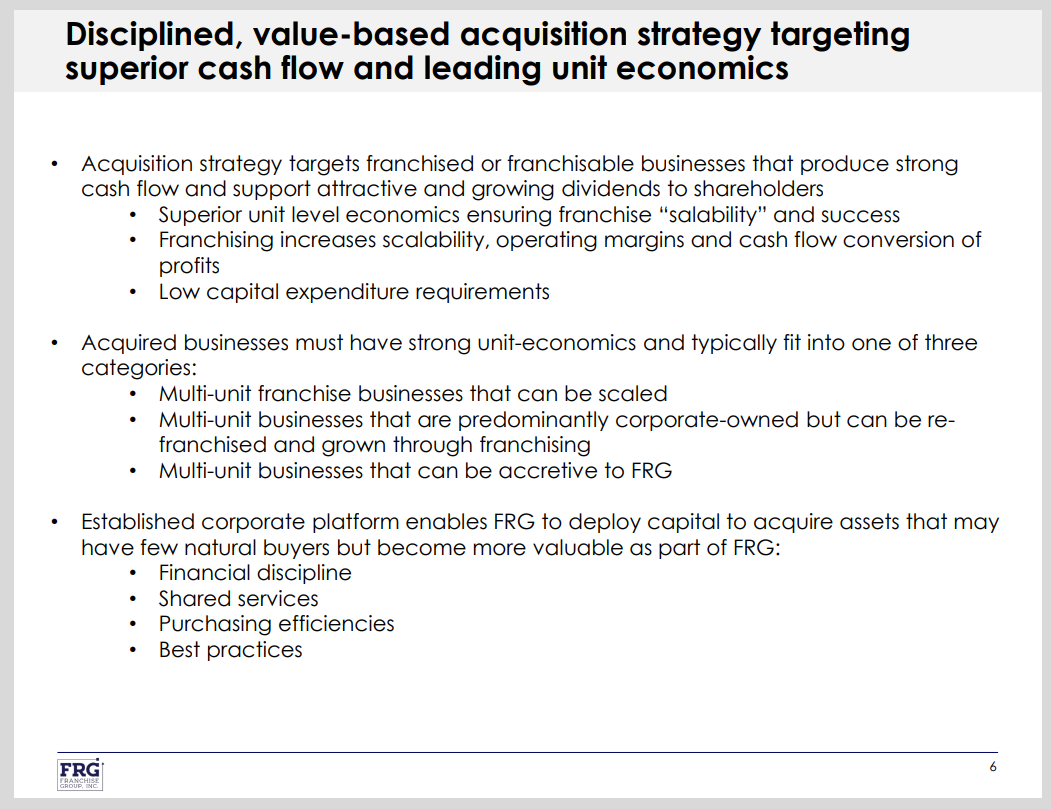

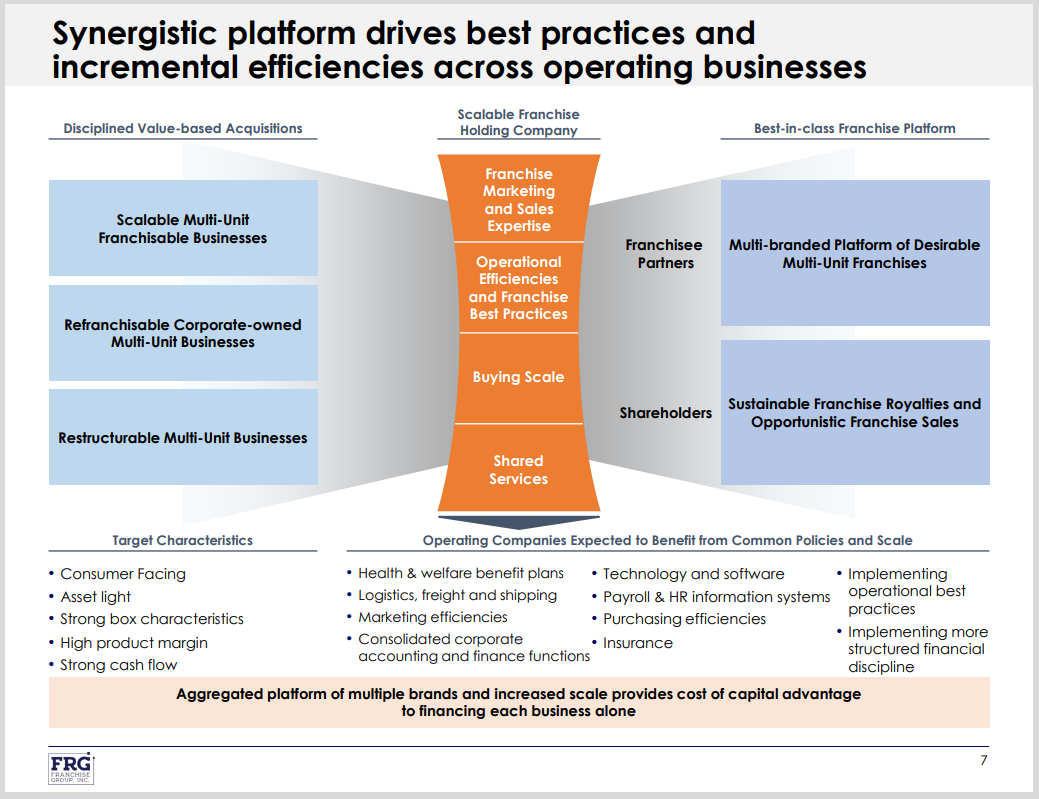

Led by Brian Kahn, the company has developed a strategy to target and acquire businesses that allow for profitable franchising and can be made more efficient through synergies already existing inside FRG.

FRG Presentation

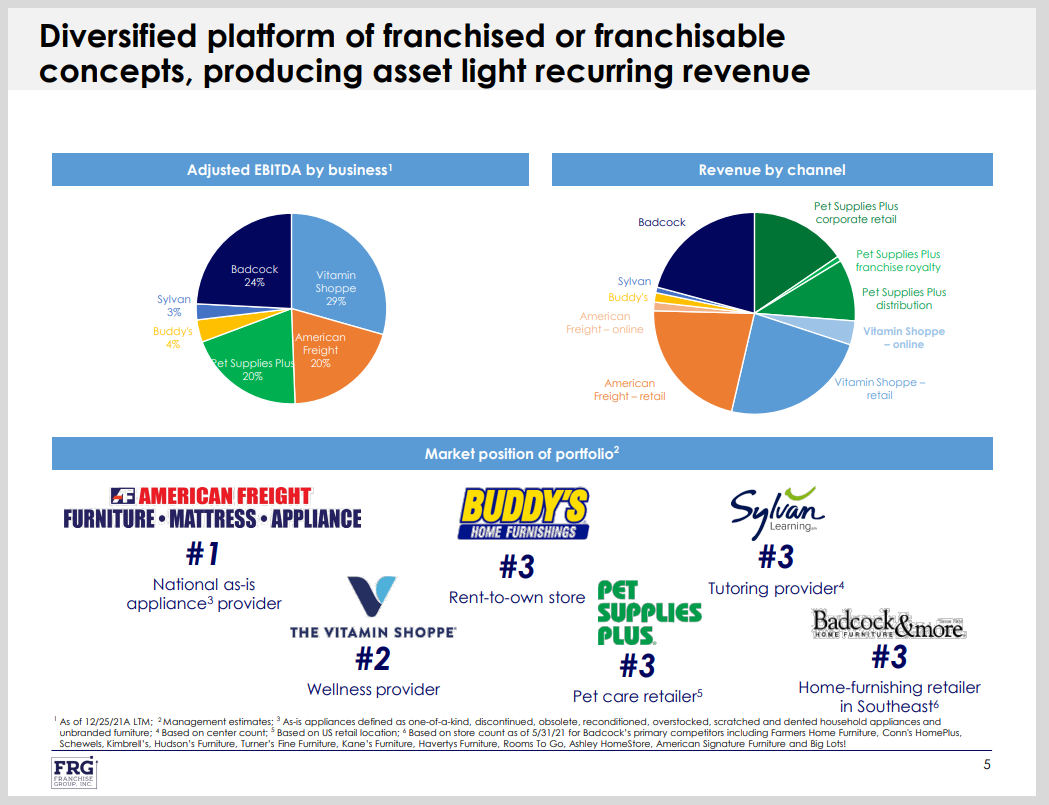

They own companies like Pet Supplies Plus, American Freight, Vitamin Shoppe, Badcock Home, and many others like these. Most know these brands and are familiar with how they work, and each actually may have its little moat inside their respective industry.

It’s a very interesting company and one that I have enjoyed reading about.

Pros

Insider Incentive. If you have read the past Weekly Value Finders, then you know that I hate when companies hand out free shares to executives so that they can sell them for a sweet little bonus. But if you want to find a company whose executives have an interest in shareholder returns, then look for one with high insider ownership. This is where FRG comes in. Currently, the CEO, Brian Kahn, owns around 20% of the shares, which is a massive plus for me.

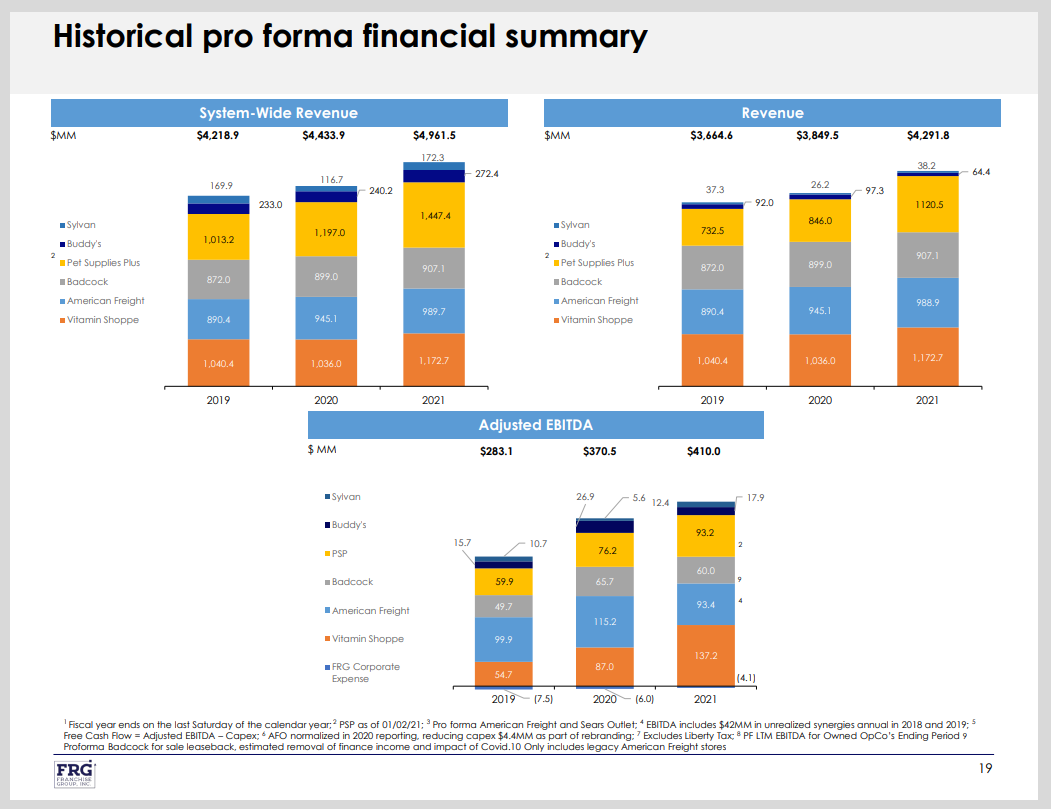

Dividend Structure. As previously noted, the current yield of FRG is just above 8%. That seems scary high though, right? Wrong. In 2016, the company was paying a 64-cent dividend per share. Currently, they pay almost the same per quarter. This has come as they have committed to paying a dividend of around 25% EBITDA. Last year, they paid ~$90 million in dividends on ~$410 million in EBITDA. During the Q2 earnings call, Brian Kahn said the following:

The Franchise Group second quarter financial performance was within our expectations but for the full year 2022, we’re lowering our financial outlook for revenue to approximately $4.3 billion from $4.45 billion; adjusted EBITDA to approximately $390 million from $450 million; and non-GAAP earnings per share to approximately $4.00 a share from $5.00 a share. Inflationary pressures leading to lower profitability in our home furnishings businesses while profit growth in pet, health and wellness and education services are providing the diversification in scale that allowed FRG to declare another quarterly dividend at a $2.50 per share annual rate.

FRG Presentation

Massive Buyback Program. Want a way to increase shareholder returns when there isn’t a company to buy? Buy your own company back! Along the same lines as the dividend structure, there are two factors in revenue per share. If you can’t increase the one, then decrease the other! During the latest call, Mr. Kahn announced that the board has approved a 500 million dollar buyback program for the upcoming years. For those out there, counting that is almost 40% of outstanding shares! The company has increased its share count over the past few years as acquisitions have been the focus, but now it seems to be ready to remedy the situation.

Okay, it’s getting way too rosy out here. Let’s go to the cons.

Cons

Recession. What has two thumbs and thinks investing in franchisable retail businesses during a significant recession is a bad idea? Me. Let’s take a poll of the room here. If you are strapped for cash, would you head out to buy: supplements, furniture, tutoring, or any non-necessary pet supplies? The answer is a resounding, I’m not sure. All of the companies that are owned by FRG represent a discount when compared to their competitors, so the pain could be less than expected but retail is retail, and when extra money isn’t in abundance, they get hurt. This is a major near-term risk for the company, no matter how you shake it.

FRG Presentation

Acquisition-Based Growth. This is another major downfall of FRG. While they have opened up new franchise stores within their brands, the real growth comes from purchasing companies. While there is a backlog of franchise stores to open, if they can’t find a company to purchase for a fair price, then what happens? This could end up being a major issue if a bad move is made. Earlier this year, they made a massive over-share price bid for Kohl’s (KSS) and were turned down. Was that a bad move avoided or an opportunity lost? We may never know.

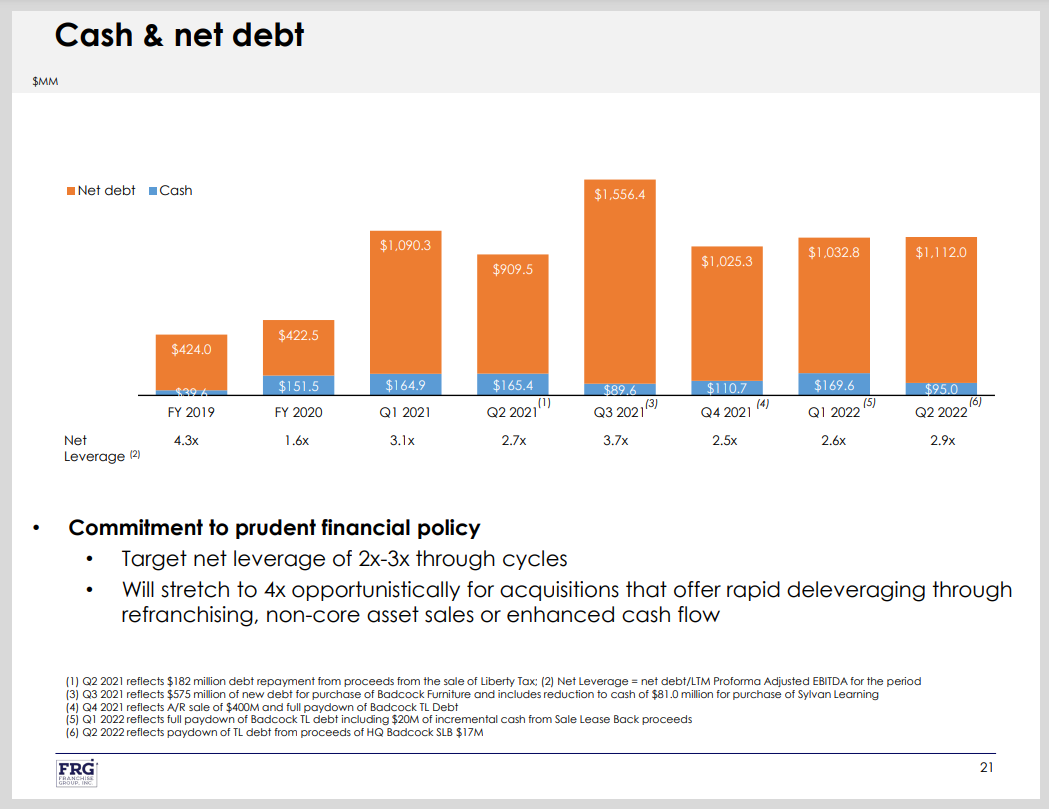

Debt Control. Now to this point, FRG has done a great job at managing debt and cash balances so this should be a pro, but it could become an issue very quickly. In their recent earnings presentation, they noted that would be willing to stretch leverage past 4x if the right acquisition presents itself. That acquisition was seemingly Kohl’s but it didn’t work out. While moves have worked well in the past, it doesn’t mean they will continue to work in the future. History gives me optimism, but a 4x leverage ratio possibility gives me a slight pause when looking at a dividend income stock.

FRG Presentation

Conclusion

Franchise Group, Inc. is a business that is based on the same value investing principles that many of us grew up on. Find a company that is for sale under its value, buy it, then make some tweaks to turn it more profitable.

When it comes to business, it’s a tale as old as time.

That being said though, the current price of the stock places it firmly in the “Watchlist” category for me. While I could pick up a seemingly safe dividend that would pay me well above the norm and let it reinvest while I sleep, I also see some serious risks to the revenue in the near term.

I will most likely set my sights on the $23-25 dollar range for FRG, something that was seen recently, and see if it gets there. If the environment changes and guidance is reaffirmed, or another acquisition is made, then I can re-evaluate and go from there. Until then, though, I am glad that I stumbled upon this company and hope you all are too.

As always, thanks for reading, and happy investing!

Be the first to comment