ssucsy

“If all the economists were laid end to end, they’d never reach a conclusion.” – George Bernard Shaw

Labor Day, the ‘unofficial’ end to summer has come and gone. Analysts, Traders, and Investors have returned from the last of their well-earned summer vacations. Meanwhile, the equity market has done some traveling of its own. Amazingly, the S&P 500 is only 3.5% below its Memorial Day level, but there’s so much more to the story. At the start of the summer, the Index rapidly fell into BEAR market territory with the S&P 500 declining ~24% from its January record high. Then, despite depressed sentiment, it notched an impressive 17% rally—lifting optimism that the S&P 500 would notch its seventh consecutive positive summertime return. But weakness set in as all of the major indices were soundly rejected at key technical resistance levels. Ignoring the “charts” can be costly.

This volatility has provided a lot of fodder for both BULL and BEAR arguments. The BEARS believe the market’s gains were nothing more than a bear market rally, failing at obvious 200-day moving average resistance, and that a much lower low will occur. Conversely, the BULLS believe that the lows are in and that the current pullback is normal. The bottoming process has begun.

Investors have learned valuable insights about the economy and financial markets that will help construct a view for the remainder of the year. Heading into the last quarter of 2022, we can safely say we’ve never experienced anything like the current backdrop before. For one, this Quantitative Tightening cycle won’t be like the others. The unwinding of the balance sheet is set to ramp up this month with the Fed increasing its reduction pace from $47.5 billion to $95 billion per month. Given that it is coinciding with the most aggressive tightening cycle in 20 years and that tightening is occurring globally (e.g., Canada, Europe, UK), Treasury market liquidity will likely be challenged, and bond market volatility will likely be elevated in the months ahead.

Another thing we’ve learned, since Covid, it seems everybody has been wrong more often than they’ve been right. Remember the analysts telling everyone that Russia would take Ukraine in 5 days and then March further into the Eurozone? WRONG. As of today, it is the Russian army that is in retreat and giving back some of the territories they originally claimed.

In terms of bad analysis, the rate at which economic data has been coming in weaker than expected recently hit its highest level over a trailing two-month period than all but one other period in the last 22 years. That one period was at the depths of the Financial Crisis. Yet there remain those that cling to the notion that the economy is doing just fine.

Earnings Beat Estimates

Market analysts were way off the mark this past earnings season. They forecasted a disastrous earnings season, but the actual results weren’t nearly as bad, and the S&P 500 had its best earnings season performance in more than 10 years. Positive corporate EPS will support stock prices, but there is growing concern estimates are way too high given the state of the economic data. Plus, the lag effect of tightening on the economy will also cause a moderation in earnings for a while. Analysts may now find themselves wrong again by being too optimistic.

Fed Watchers Were Caught Off Guard

The bulk of economists seemed surprised that Powell and the Fed have taken on a more hawkish tone in recent weeks. I’m not sure how they arrived at that incorrect conclusion. The initial talk of a FED pivot coming soon has also been WRONG. The FED entered the scene for ONE purpose, to fight inflation, and they made it clear at Jackson Hole that is what they are going to do. Analysts pointed to a slowdown in the economy and with that, some inflation pressure easing, so they “assumed” the Fed would soon “pivot”. WRONG.

Much of the cooling at the headline inflation level was driven by gasoline prices retreating from their $5.02/gallon peak to under $4/gallon. However, there is plenty of “other” energy cost inputs that are embedded in this economy. So after being way too dovish for way too long, they have moved to the other extreme with what has been one of the most aggressive rate hike cycles in such a short period and there are more increases to come.

The combination of a weak economy and the FED being forced into the scene to fight inflation is what I warned about last year. We saw the signs that were pointing to a contraction, but the analysis bought into the “rhetoric” and kept forecasting growth in the first half of this year. WRONG again. Instead, it was back-to-back negative GDP prints. Therefore, the weakness we have seen in the economy is very real and can remain that way. In the interim equity markets have now had to price that in.

Economists got caught wearing rose-colored glasses.

Fear not, the rhetoric continues. There is plenty of pundit commentaries that the U.S. isn’t in a recession and analysts are opining that despite little success in the past, this Fed can still engineer a soft-landing. I sure hope they can pull it off but I have a crash helmet at the ready. It is amazing (but not so unusual) for the majority to be WRONG with their assessment of the markets. BUT this two-year period has been one for the history books.

Oh, and let’s not forget “transitory inflation”. A premise that I also bought into early on before realizing the majority were offering a biased political opinion. The same holds for the “Hopium” trade which suggested Inflation was about to drop like a rock. That assessment has already been proven wrong and those that wish to stay on that path and listen to biased rhetoric are going to be run over.

I didn’t see the situation as rosy as some because of economic policy and it’s why the call for a change to the “New Era” strategy in February where buy the dip was replaced with sell the rally. That change also called for concentrating on “what was working”. I don’t have a crystal ball, but what I have learned to do is “listen” to what the market is saying. We are now in a BEAR market that is in the process of “playing out”. Perhaps attempting to carve out a bottom. Perhaps ready to drop into another leg lower.

There is no change in my outlook. What occurs next with stock prices will be dependent on what the investment community expects the economy to look like as we enter 2023. The “look” of the economy will depend on how inflation shakes out and just how far the Fed has to go to cool it off. Ironically, present economic policies will continue to dampen growth and in effect, will do the Fed’s job. If I’m correct on that then the Fed won’t have to go over the edge to kill inflation. However, either way, the economy suffers.

The Bottom Line; Investors should be prepared for a long and uncertain road ahead. We’ve discussed that the probability of a “V” recovery in the markets was extremely low, and as I stated last week that possibility is now slim to none. Markets are agreeing and confirming that with indices stumbling after every rally attempt.

The road ahead to the next BULL market will seem easy at times (if the right strategy is employed) and at other moments very difficult for all to navigate. That will require an Open mind and a flexible strategy.

The Week On Wall Street

The three-week losing streak was broken in the prior week and all looked fine as the S&P opened this week on a strong note that brought the winning streak to four days totaling ~6%.

Enter a headline regarding inflation, and as we have seen in the past the situation turns quickly. In a BULL market, the surprises come on the upside. In a BEAR market, the surprises are ugly. Tuesday’s surprise was indeed ugly. The NASDAQ fell 5%, and it was the seventh drop of 4%+ already this year. The DJIA suffered the 7th worst loss and the S&P its 5th worst point loss in history.

The rally was snuffed out in one session. From there it was back and forth trading with the indices moving between gains and losses until Friday. A “gap down” opening set the tone for the day in which all of the indices could not recover from.

The Weekly losses accelerated on Friday;

S&P -4.7%

NASDAQ – 3.9%

DJIA – 4.1%

Dow Transports -8%

Russell 2000 – 4.2%

Stray tuned it could get very interesting.

The Economy

GDP in the first half was negative and we heard every excuse as to why that occurred. On top of that, the cheerleaders were saying that the economy would rebound significantly in Q3 and Q4. I warned back in 2021 that I didn’t see any robust growth on the horizon as we entered the year.

The Atlanta Fed GDPNow estimate for 3QGDP is now at 0.50%. On August 11th forecasts for the 3rd quarter were at 2.5%. Once again I warned that these estimates were way too high. I won’t jump to a conclusion but if this trend continues there is a decent probability that we will see the 3rd quarter in a row with a negative print. I’ve said it repeatedly, there are no growth initiatives in place and the anti-business backdrop is still with us. I’m not here to root against the economy (far from it) but there is no reason to buy into the absurd “out of touch with reality” cheerleading fanatics. The data doesn’t lie.

Inflation

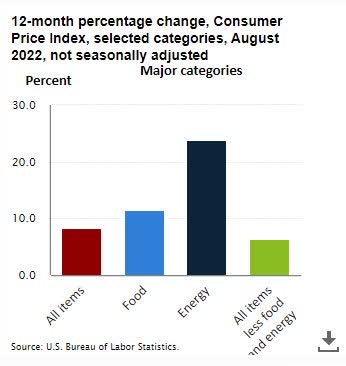

Economists expected a 0.1% Month over Month decline in CPI; Cleveland Fed inflation nowcasting data suggested a 0.06% advance. The actual numbers were stronger than expected with the headline rising 0.1% while the core reading of 0.6% was double expectations.

The overall 12-month pace slowed marginally to 8.3% y/y from 8.5% y/y and was 6.3% y/y versus 5.9% y/y for the ex-food and energy metric. The latter is the highest since March which also equaled the hottest clip in 40 years.

Markets were positioned for a weaker print, so the strong number completely reversed the positive tone in early morning futures and when trading opened sent stocks sharply lower. I’ve said it for a while inflation isn’t going away anytime soon, but I do have to admit this print did surprise me. It’s not just about getting inflation from 8% to say 5%, it’s how long it stays at elevated levels.

The 75 basis point increase that was penciled in is now cast in stone, and while I won’t speculate on what comes after that, the Fed’s 2% inflation target is a long way from where we are today and that keeps them in the picture for a LONG time.

After official numbers like these, it’s impossible to say that inflation isn’t a problem anymore, yet I’m sure there will be some “spinning” with more rhetoric that is based on “hopium”. I’m in the “show me” camp. Among other issues, Energy costs are still high.

Inflation – CPI (www.bls.gov/)

The folks listening to the rhetoric and drinking the KOOL Aid being served need to start paying attention to what is going on around them. Inflation is embedded and cemented in place with spending. Moreover, energy prices are still high and they appear in EVERY category that is measured.

The second look at inflation (Producer prices) didn’t shed any light on the concerning picture that was presented in the CPI report yesterday. PPI dipped -0.1% in August with the core rate bouncing 0.4% following the -0.4% headline decline in July. All-time highs were hit in March at 1.7% for the headline and 1.3% on the core. The respective 12-month rates were 8.7% y/y and 7.3% y/y, decelerating from July’s 9.8% y/y and 7.6% clips.

NFIB Small business data published this week showed sentiment rose 1.9 points in August to 91.8, marking the eighth consecutive month below the 48-year average of 98 but reversing some of the declines in the first half of the year. Twenty-nine percent of owners reported that inflation was their single most important problem in operating their business, a decrease of eight points from July’s highest reading since the fourth quarter of 1979.

The labor market continues to cool from its recent peak. Across a range of six different indicators, small businesses are expecting or experiencing slower hiring, less wage growth, and less labor scarcity. NFIB Chief Economist Bill Dunkelberg;

The small business economy is still recovering from the pandemic while inflation continues to be a serious problem for owners across the nation. Owners are managing the rising costs of utilities, fuel, labor, supplies, materials, rent, and inventory to protect their earnings. The worker shortage is impacting small business productivity as owners raise compensation to attract better workers.”

Small business makes up approximately two-thirds of GDP. At the moment they aren’t sending a positive message. Is anyone listening?

Manufacturing

A weakening economy is also being reflected by weak Manufacturing data.

Industrial production dipped -0.2 in August, weaker than expected, after rising 0.5% in July. Capacity utilization fell to 80.0% from 80.2% previously.

September Empire State manufacturing index improved 29.8 points to -1.5, much stronger than expected, and recovered about half of the 42.4 point plunge to a 2-year low of -31.3 in August. However, it remains in contraction.

Philly Fed index tumbled -16.1 points to -9.9 in September, much weaker than expected, after climbing 18.5 points to 6.2 in August. Most of the components weakened.

The lone positive in both manufacturing reports were the Prices Paid component.

Consumer

Retail sales rose 0.3% in August and fell by 0.3% excluding autos. There was a real mix of data and revisions to complicate the outlook. Sales excluding autos, gas and building materials edged up 0.2% from 0.2% in July.

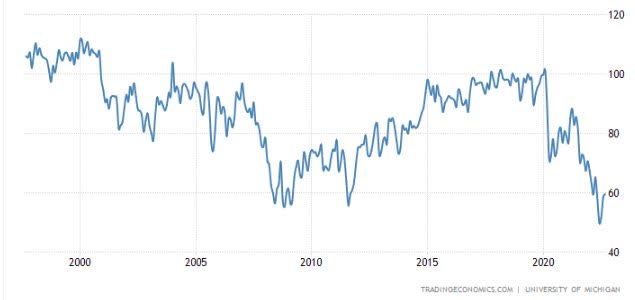

Consumer sentiment rose another 1 point to 59.2 in the preliminary September report after rebounding 6.7 points to 58.2 in August. This is the best since April. Both of the components posted gains. The current conditions index edged up to 58.9 from 58.6 previously, and is also up from its historic low of 53.8 for June. The expectations gauge rose to 59.9 from 58.0.

Despite the improvement this month these results are levels last seen during the Financial crisis.

Michigan Sentiment (www.tradingeconomics.com/united-states/consumer-confidence)

The Global Scene

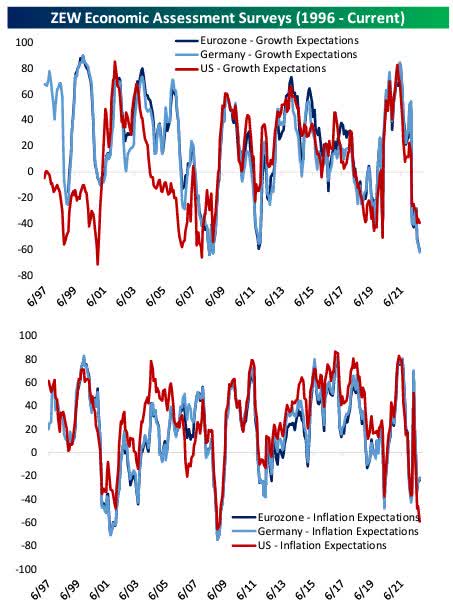

Each month, ZEW publishes surveys of financial market watchers which give a nice insight into sentiment on the world economy. While these surveys aren’t helpful for forecasting on a forward basis, they do give a good idea of consensus. In the current context, that consensus is extreme, to say the least.

ZEW survey (www.bespokepremium.com)

As shown above, the growth outlook is as weak as any point in series history for Europe, while US growth expectations are also very soft. Similarly, inflation forecasts are very weak. This is a firm counterpoint to central bank concerns that inflation is getting entrenched as financial market participants expect very high current inflation to fall on both sides of the Atlantic going forward. They received a dose of reality with this week’s CPI report. If that is truly their mindset the market has not priced in the reality of high inflation hanging around well into next year. This realization could set off a complete repricing of the equity markets going forward.

China

Chinese Industrial Output continues to trend higher rising 4.2% after the July gain of 3.8%. Retail sales edged up 5.4%, better than analysts’ expectations for a 3.5% rise and 2.7% growth in July.

Food For Thought

Small business reports are telling the same sorry month after month. It’s very difficult to find workers. The JOLTS report confirms that with about 10 million job openings available. We’ve also seen the Labor participation rate continues to remain depressed. Using data from the government’s census bureau, The Wall Street Journal uncovered surprising details that point to the root cause of why it’s so difficult to get people to work. We all have heard the income inequality argument and for sure there is a large wealth gap between the top and bottom but that isn’t the issue at hand. People in the middle work much harder, but don’t earn much more, than those at the bottom.

The WSJ;

The problem in the US today is income EQUALITY, not INEQUALITY.”

That sure sounds quite a bit different from what we have been listening to. The middle class is working, and working hard to improve their lot in life. However, when we add up the numbers they don’t earn much more than those at the bottom levels.

Census Bureau statistics indicate that, among working-age households, the bottom 20% earned only $6,941 on average, and only 36% were employed. But after transfer payments (Welfare, Rent, Transportation subsidies, etc.) and taxes, those households had an average income of $48,806. The average working-age household in the second quintile earned $31,811 and 85% of them were employed. But after transfers and taxes, they had an income of $50,492, a mere 3.5% more than the bottom quintile.

However, these figures don’t tell the whole story. In the bottom quintile, there are on average only 1.9 people living in a household. The second and middle quintiles have 2.4 and 2.6 people respectively. After adjusting income for the number of people living in the household, the bottom-quintile household received $33,653 per capita. The second and middle quintile households had on average $29,497 and $32,574 per capita, respectively. The blockbuster finding is that on a per capita basis the average bottom quintile household received 14% more income than the average second-quintile household and 3.3% more than the average middle-income household.

Admittedly this didn’t happen overnight, but it has undoubtedly been exacerbated since 2021. In October 2021 food stamp recipients received a historic 25% increase in their benefits. In addition, benefits were authorized to an additional 25 million. This is just one example of the increase in benefits that have been doled out.

Most assuredly some are in need (disabled, etc.) but one would have to wear blinders and earplugs to not be aware of what is going on. At the end of 2021 41.5million people received food stamp benefits, up 17% from 2020. The pandemic is over, there are 10 million job openings and those numbers should be declining not rising. There are scores of people on programs that find it much easier to stay home and live the same as a blue-collar worker putting in a solid 40-hour workweek.

As mentioned earlier this didn’t occur overnight. The U.S has embarked on its brand of socialism and is growing exponentially with today’s “entitled” mindset. The government reports the percentage of working-age people in the bottom quintile who worked plummeted from 68% to 36% in the last 50 years. At some point, the number of workers that are paying the freight in the form of taxes to support all of these programs will eventually buckle.

With entitlement payments giving recipients about as much for not working as they could earn working, only a mandatory work requirement as a condition for receiving means-tested benefits will bring them back into the labor market. Given the current mindset in place today, that wouldn’t seem to be a change that we will see anytime soon. This dilemma is a ball and chain on growth and a primary reason why employers, especially in the services sector, can’t find employees willing to work.

Sentiment

The S&P 500 may have fallen around 1.5% over the past week, but individual investors have reportedly become increasingly bullish. 26.1% of responses to the weekly AAII sentiment survey were reported as bullish this week, up from a recent low of 18.1% last week.

While bulls rose back above a quarter of responses, bears fell back below 50%. Bearish sentiment dropped to 46% which was only the lowest level since the week of August 24th.

The Daily chart of the S&P 500 (SPY)

Since the S&P and other indices were rebuffed at their respective resistance zones, it’s been downhill. That trend continued this week.

S&P 500 (www.FreeStockCharts.com)

The early September lows did not hold and that opens the door for a possible retest of the June lows.

Investment Backdrop

We are now past the Labor Day holiday here in the U.S. and have therefore entered the homestretch for the rest of the year. There shouldn’t be anything special about this time of the year, but, for many reasons, the activity often picks up and markets get more volatile in the final months (for better or worse). Many of the most memorable events in market history either took place in this latter part of the year or saw their existing moves accelerate after Labor Day. September and October, in particular, are noted for being difficult. That is, of course, not always the case, though it does usually pay to be more cautious during this period than in the typically slower summer months.

We’ve seen the S&P falter at resistance, then temporarily hold at an important support zone that was necessary to preserve any bullish case. With an economy that is weakening and inflation remaining stubborn at 8%, this continues to be a headline-driven market. After a 6% rally in the S&P in four days, any pause would be normal, but on these days a pause is a one-day 4% drop in the indices. What makes the situation more difficult is the “internal” market conditions leading up to last Tuesday’s action. Coming into that day, 83% of NYSE operating companies were already back above the 10-day moving average (after getting down around 3% just a few days ago). In the last four trading days, market breadth reverse higher with four straight days of net positive readings over +250 and two positive ‘all or nothing days’ (days where S&P 500 net daily breadth reading comes above +400 or below -400). Long story short. It was a broad rally.

So while the signal looked “green” a headline turns the situation to “red”. This doesn’t amount to a “liquidate and raise cash period” (not yet) but it also isn’t a “buy this dip” moment either. The latter advice holds unless you are into the few bullish trends that remain, or have a LONG time horizon.

The trend is your friend and that is where an investor’s money needs to be invested. The “BULL” trends that exist should be obvious by now, and there is nothing wrong with being involved in the downside as well. After all, that is the PRIMARY trend.

Thank you for reading this analysis. If you enjoyed this article so far, this next section provides a quick taste of what members of my marketplace service receive in DAILY updates. If you find these weekly articles useful, you may want to join a community of SAVVY Investors that have discovered “how the market works”.

The 2022 Playbook is now “Lean and Mean”

Opportunities are condensed in Energy, Commodities, Utilities, and Healthcare. Along with that I’ve defined Bearish to Bullish reversals. The message to clients and members of my service has not changed. Stay with what is working.

Each week I revisit the “canary message” which served as a warning for the economy. The focus was on the Financials, Transports, Semiconductors, and Small Caps. I used them as a “tell” for what direction the economy was headed to help forge a near-term strategy. Unfortunately, all of the canaries are very, very sick.

Sectors

A picture is worth a thousand words. Members of my service receive a more detailed sector analysis each week with charts that present a great picture that assists in assembling our strategy. Energy (XLE), Utilities (XLU), Healthcare (XLV), the Commodity (BCI), and Insurance (IAK) sub-sectors remain in Bullish trends. Every other sector is mired in a BEAR market.

Energy

Although crude oil hit a 7 month low recently, energy stocks remained resilient, and many that I own or track are holding up very well. The short intermediate and long-term trends are all Bullish and some of that strength is attributed to strong balance sheets, cash flow, and above-average dividend payouts.

Natural Gas

The Nat Gas ETF (UNG) experienced a volatile week and finished below short term support. I maintain an overweight position in the sector that has many tailwinds to keep it in a BULL trend.

Gold

I’ve mentioned a number of times that I didn’t see any Bullish setup worth tracking in this precious metal. That view is being confirmed as Gold broke below support to a 2 year low this week.

It remains a “No-touch” for me.

Financials

The Financials (XLF) rallied strongly this week, but are still well away from turning the BEAR trend into a BULLISH one. Renewed strength in this group would go a long way in helping the general market recover.

Healthcare

With the general market weakness, the sector (XLV) is struggling, but continues to trade in a sideways pattern. I believe there are opportunities here that will hold up much better than the average stock in a weak economy. These gems also pay above-average dividends.

Sub-Sector BIOTECH

The Biotech ETF (XBI) continues its “BEAR to BULL” reversal pattern and early in the week appeared ready to challenge the August highs. It’s been a give-and-take week for the group that is now clinging to support.

Technology

When the interest rate moves higher (10-year Treasury now at 3.4%) The algorithms sell Technology. Therefore with the trend in rates moving up, the trend in technology is down. I expect this to be a headwind for the group for quite some time. With stocks like Microsoft (MSFT), Alphabet (GOOG), Nvidia (NVDA), etc. all in BEAR trends only those with a Long Term view should be playing in this space.

Sub-Sector Semiconductors

The semiconductors (SOXX) appear to be attempting to find a bottom, as the ETF is struggling now to hold above the early September lows. If support holds a sideways pattern could emerge, but this week support didn’t hold, and it could be a sign that the June lows will be revisited. Another sector where an investor is either “short” or sitting on the sidelines. The BEAR trend here is firmly entrenched.

ARK Innovation ETF (ARKK)

This reversal pattern started to look questionable last week, battle lines were drawn and the BEARS took control of the short term chart this week. Now we will see if the series of higher lows established since June will remain intact.

Cryptocurrency

As equities solidly rebounded this week, Bitcoin has likewise turned higher. The world’s largest crypto has rallied recently until the selling event on Tuesday. Cryptos are correlated with risk-on these days and they too were crushed, The positive pattern that I was watching in Grayscale Ethereum ETF (OTCQX:ETHE) and the Bitcoin ETF (OTC:GBTC), evaporated quickly.

Final Thoughts

Last week’s article was entitled “The Bears Still Hold The Key”. My reason was simple. Despite the “bounce”, my belief was nothing had changed. The “show me” market was going to have to prove itself before the BULLS can claim any victories. The Policy error warnings have been part of the message here since 2021. Spending increases inflation, additional reckless spending and unnecessary entitlements add concrete to the situation. High energy costs attributable to poor (or no) Energy policy add the water that cements inflation in place. More importantly, the technical situation was perfectly aligned with that backdrop.

Welcome to the New Era of High Inflation and High-interest rates. A new market strategy was identified to take advantage of these issues in February of this year and I spoke about the potential for recession. The pied pipers that have led investors and consumers with the talk of “all is well” with the economy are just now starting to think the US has a chance of falling into a recession. They are at least 6 months behind Savvy Investors.

Here is a news flash. If we do not start to see a “change” in the mindset of policymakers then my view of a LONG and DEEP recession now comes to the forefront. Unlike many other pundits, I won’t jump to that or any other conclusion until the stock market tips its hand. Perhaps the indices settle into a large trading range with plenty of starts and stops that will continue to be very confusing. In my view that would be the “BEST case” scenario.

At the end of the day, it will eventually come down to what the market envisions future corporate earnings are going to be. Of course, that depends on what “action” or lack of action is taken on the fundamental side. Rome is burning and the fiddlers are in denial about the economic data at hand. Instead of fixing the issues they are celebrating what they believe is a solid economy. Ladies and Gentlemen, that combination is nitroglycerin.

I continue to remain open-minded with a flexible approach that will align with the ever-changing direction of this market. That gives me the best chance for success in a very challenging economic backdrop.

Postscript

Please allow me to take a moment and remind all of the readers of an important issue. I provide investment advice to clients and members of my marketplace service. Each week I strive to provide an investment backdrop that helps investors make their own decisions. In these types of forums, readers bring a host of situations and variables to the table when visiting these articles. Therefore it is impossible to pinpoint what may be right for each situation.

In different circumstances, I can determine each client’s personal situation/requirements and discuss issues with them when needed. That is impossible with readers of these articles. Therefore I will attempt to help form an opinion without crossing the line into specific advice. Please keep that in mind when forming your investment strategy.

THANKS to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!

Be the first to comment