dan_prat

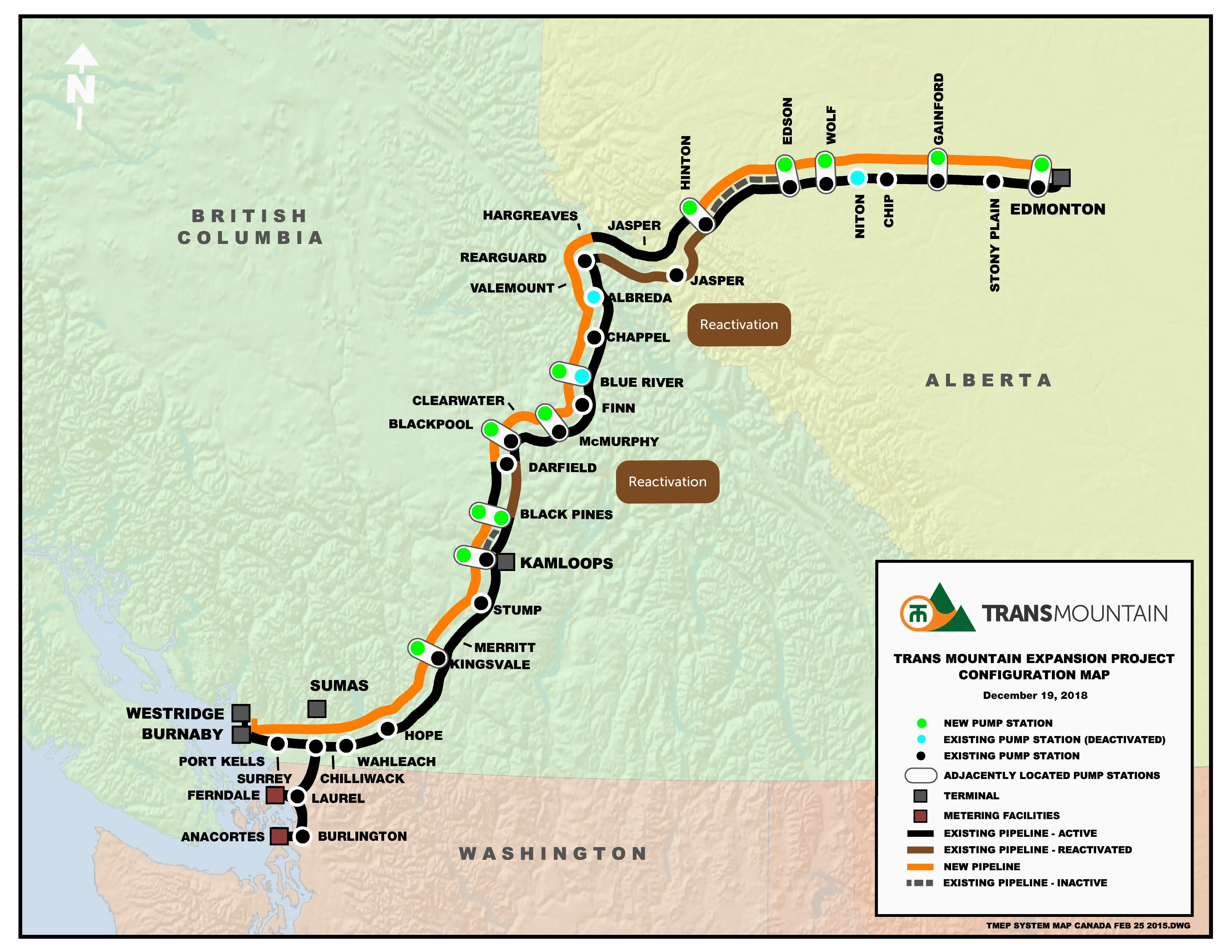

According to the current schedule, mechanical completion of the Trans Mountain pipeline expansion project is expected to be completed in Q3 of this year. The expansion will take the pipeline’s capacity from 300,000 bpd to 890,000 bpd, adding more than a half-a-million bpd of pipeline exit capacity from the center of Canadian oil sands production near Edmonton, Alberta to the Canadian West Coast port of Burnaby, British Columbia (see map below). From there, oil sands exporters will have access to refineries on the West Coast of the U.S. as well as in Asia, particularly China. No doubt, the in-service of this pipeline expansion project will be celebrated near and far in Alberta as big oil sands producers, like Cenovus (NYSE:CVE), will be able to increase production while enjoying a very likely and significant contraction in the long-standing – and sometime very wide – discount between WCS and WTI.

Trans Mountain Pipeline

Investment Thesis

As most energy investors know, for many years the Canadian oil sands producers have suffered from a lack of adequate pipeline exit capacity. While Canadians have typically blamed the U.S. for not being able to build projects like the Keystone-XL pipeline, the fact is that the Canadian energy sector simply has not taken matters into its own hands and built a pipeline – or pipelines – to its West Coast in order to directly reach export markets. As a result, too much productive capacity fighting over too little pipeline capacity has led to persistent and sometimes drastically deep discounts of Western Canadian Select (“WCS”) as compared to West Texas Intermediate (“WTI”), which does have relatively easy access to export markets.

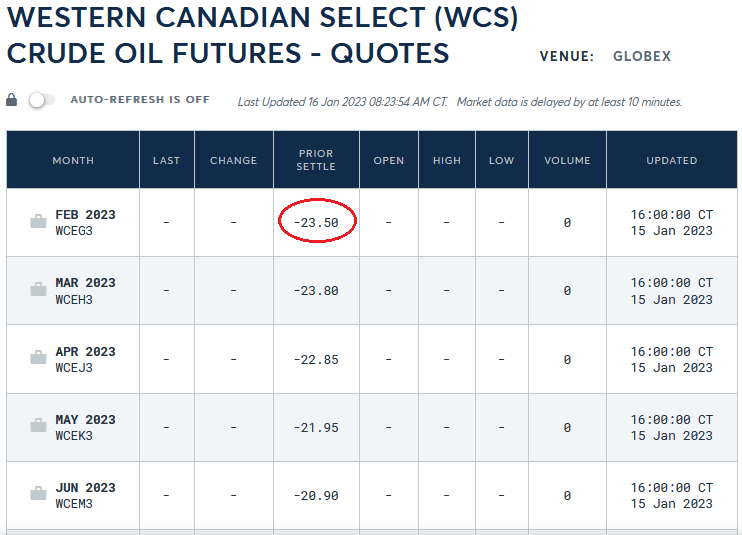

The current WCS discount to WTI for the February futures contracts is a whopping $23.50/bbl:

CME Group

Interestingly enough, the discount stays over $20/bbl even out to February of next year, long after the expected startup of the Trans Mountain Expansion (“TMPE”) pipeline project. I can’t explain that, so if any of you have an opinion, please leave it in the comment section. Even RBN Energy’s Top-10 Energy Prognostications for 2023 (see: Year of the Rabbit) predicts:

… the price spread between Canadian crudes such as Western Canadian Select and West Texas Intermediate will narrow as U.S. refiners bid up the price to hold on to some of the Canadian barrels

Cenovus

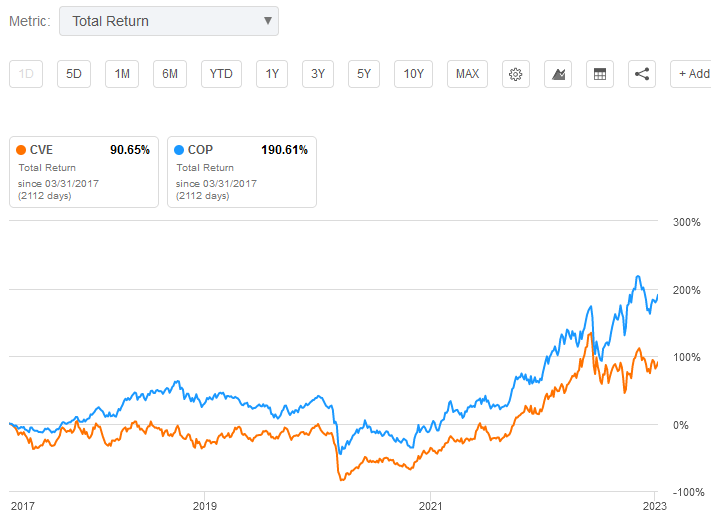

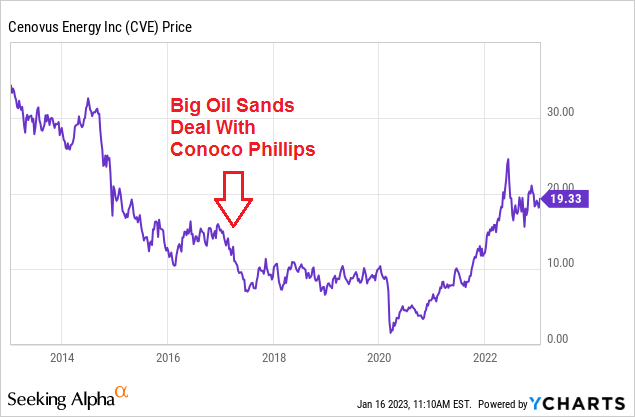

As most of you know, Cenovus bought the vast majority of ConocoPhillips (COP) oil sands assets and production back in March of 2017. That took CVE into the big leagues as a major competitor to top oil sands producers Suncor (SU). While the oil sands bulls thought the deal was great for Cenovus, I was clear in my articles that the deal was much more beneficial for COP (see The Big COP/CVE Oil Sands Deal – Six Months Later). That was indeed the case, with COP stock delivering total returns ~100% higher than CVE since the deal was closed:

Seeking Alpha

Today, Cenovus is one of the largest oil sands producers and as such has been a beneficiary of Putin’s horrific war-on-Ukraine, the breaking of the global energy supply chain, and the subsequent increase in oil & gas prices.

Indeed, in its Q3 earnings announcement, Cenovus reported it generated earnings of $0.81/share and $2.1 billion in free-cash-flow. Net production was 777,900 boe/d – up from 761,500 boe/d in the previous quarter. Aggregate production from Christina Lake and Foster Creek, CVE’s largest tar sands projects, was a combined 435,200 bpd. Total estimated oil sands production for full-year 2022 is 612,000 bpd and equates to roughly 75% of CVE’s total production. (CVE’s Q4 report is due out on February 16th).

The Dividend

For years Cenovus struggled under the debt-load as a result of the big oil sands deal with ConocoPhillips. But the company has made significant progress on that front: long-term debt was reduced to $8.8 billion as of the end of Q3, down from $11.2 billion at the end of Q2. Net debt of ~$5.3 billion is down $4.3 billion since the start of the year. This bodes well for shareholders going forward because significantly less interest payment requirements means more cash leftover for dividends.

Indeed, Cenovus – after cutting the quarterly dividend from C$0.2662 in 2015, to C$0.05 in 2016 – and eventually down to C$0.0175 in 2021, raised the quarterly dividend to C$0.1050/share this year. In addition, to this “base” dividend, the company instituted a variable dividend policy in Q4, with an initial declaration of C$0.1140/share. This is good news for Cenovus shareholders, and I expect that when the TMPE project goes in-service, the company will be able to declare significantly higher variable dividends it will be a primary beneficiary of increased production combined with significantly higher realized prices for WCS as the discount to WTI narrows (at least for a while).

Cenovus is also buying back stock. In Q3, CVE purchased ~29 million shares for $659 million. That equates to an estimated C$22.72/share (the stock is currently trading at C$25.70). Since the share buyback program began in November of 2021, Cenovus has bought-back ~118 million common shares.

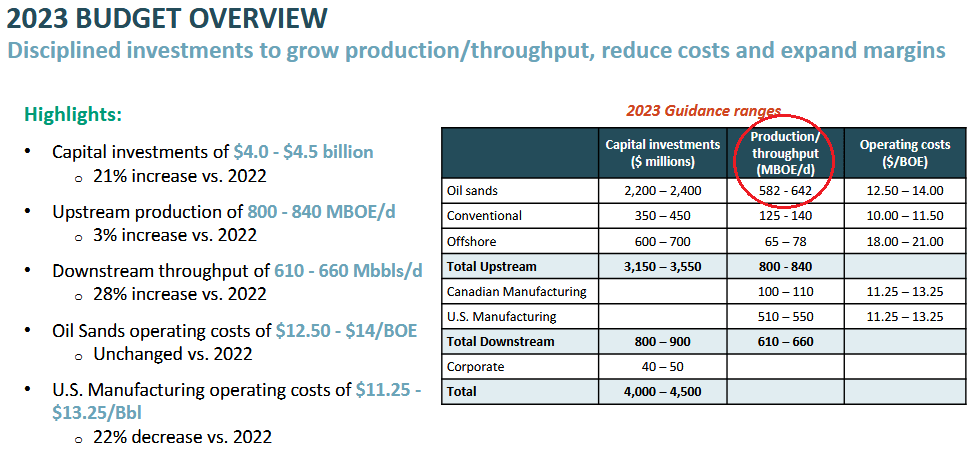

The FY23 budget is shown below in a slide from the Q3 presentation:

Cenovus

Note the rather wide-range of expected oil sands production (582,000-642,000 bpd) – the mid-point of which (612,000 bpd), which just happens to be exactly what the company projects full-year 2022 oil sands production to average. Upside is likely dependent on the company’s ever variable large-scale maintenance projects (one expense COP shareholders are very happy to no longer endure) as well as the exact timing of the Trans Mountain Pipeline fill.

In 2021, total Canadian oil sands average daily production was a record 3.5 million bpd. That being the case, the 590,000 bpd of incremental exit capacity from the TMPE project will require a 16.9% increase in overall oil sands production to keep it, and existing pipelines, full. I would expect the share of incremental capacity additions for each participating company would be roughly in line with each producers’ current share of overall production.

In addition to Cenovus, other oil sands producers who have made significant 15-20 year commitments to fill ~80% of TMPE expansion capacity include big oil sands players like Suncor (SU), Canadian Natural Resources (CNQ), and Imperial Oil (IMO). 80% of contracted expansion capacity equates to 472,000 bpd. Considering CVE’s estimated 612,000 bpd of FY22 production equates to ~17.5% of Canada’s FY21 total oil sands production, CVE could raise production by an estimated 82,600 bpd if pipeline expansion capacity is doled out on an equitable basis. That would equate to a 13.5% increase in CVE’s overall oil sand production as compared to the midpoint of FY23 guidance. Combined with expectations for higher WCS margin, this should prove to be a windfall for CVE shareholders in terms of increased dividend income.

Other Considerations

As I have said for years on Seeking Alpha, the best way to have played oil sands production in the past has been through the refiners. After all, they have been able to recoup much of the lost margin due to their consumption of heavily discounted WCS feedstock. That is especially the case for a refiner like Phillips 66 (PSX), who has a significantly higher distillate yield as compared to its peers.

Indeed, PSX is expected earn a whopping $19.81/share this year – much of that due to very high diesel margin. Obviously, if I (and RBN Energy) is right about the WCS discount significantly narrowing as the TMPE project is filled and oil sands producers take time to ramp up production, that would negatively impact Phillips 66. However, note that PSX’s two primary WCS feedstock refineries – Wood River and Borger – are part of the 50/50 WRB joint-venture between Cenovus and Phillips 66. Also, note that Wood River produces 85,000 bpd of gasoline and 70,000 bpd of distillates. This is a great example of PSX’s higher distillate yield as compared to the typical 3:2:1 crack, in which 3 bbls of oil generates 2 bbls of gasoline and 1 bbl of distillates. That is, instead of the typical 2:1 ratio of gasoline/distillates, Wood River is only ~1.2x. This is great for PSX considering diesel margin has been, still is, and is expected to continue to be so much higher than gasoline. Regardless, it can’t hurt PSX to have this tie-up with Cenovus for WCS feedstock. After all, why would CVE significantly raise the price of WCS to PSX only to lose the margin back when it comes to distributions from its refining JV with PSX?

Summary & Conclusions

The 590,000 bpd Trans Mountain Pipeline expansion project will be a Godsend to long suffering oil sands producers when it goes in-service. Mechanical completion is scheduled for Q3, which means line-fill could come as early as Q4. Certainly by Q1 2024 this pipeline should be full. While oil sands producers ramp-up to meet this huge slug of new incremental export capacity (~17% of total 2021 oil sands production), the WCS discount to WTI is likely to significantly narrow. That is great news for oil sands producers – and Cenovus is likely to be a primary beneficiary (as will Suncor and CNQ). While it is likely a bit too early to invest heavily on this thesis, investors should keep an eye out for TMPE project updates over the Summer because these stocks will likely start moving higher before the announced completion of the expansion project.

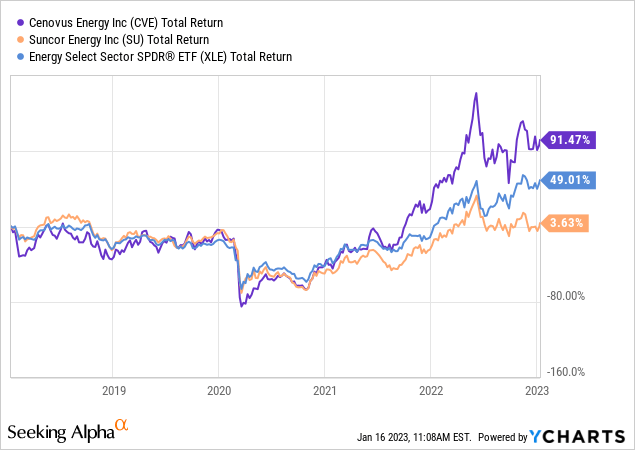

I’ll end with a comparison of the 5-year total returns of Cenovus and Suncor versus the SPDR Energy ETF (XLE) and note that Cenovus has been an out-performing energy stock over that timeframe:

Of course, part of that out-performance was because Cenovus had been so badly beaten down after it was clear the company paid too much for ConocoPhillips oil sands assets (indeed, the CEO was let go soon after):

YCharts

Obviously, that is not an inspiring 10-year chart. And while it has taken 5-years plus, with the TMPE project opening up oil sands export capacity, Cenovus may finally be in a position to deliver strong shareholder returns. That is, until the oil sands producers ramp-up to fill the new pipeline, which, as we saw from the Enbridge (ENB) Line-3 expansion project in late 2021, didn’t take very long. Note Line-3 was an additional ~380,000 bpd of capacity, and it didn’t take long at all before WCS futures went back to a deep discount to WTI. That is because we live in an Era of Energy Abundance, and that includes the oil sands produces – which, like the Lower-48 shale producers – have 10s of billions of proven oil sands reserves that are easily recoverable, by a number of big companies, and brought to market.

Be the first to comment