Kameleon007

The Trade Desk, Inc. (NASDAQ:TTD) is slated to release its FQ4’22 and FY22 earnings report on February 15.

Despite its growth premium, TTD has significantly outperformed the S&P 500 (SPX) (SPY) over the past month, as risk-on behavior returned in earnest.

As such, it also lifted the buying sentiments over TTD, which has consolidated constructively since forming its May 2022 lows.

With the sharp recovery from its November lows, investors still waiting on the sidelines could wonder whether it’s time to make a move, even though the Fed could shock the market at the upcoming FOMC meeting.

Why?

Consider TTD’s steep valuation premium as it last traded at a NTM EBITDA multiple of 36.7x, way above its peers’ median of 7.7x (according to S&P Cap IQ data). Moreover, its NTM normalized P/E of 50.8x likely requires the company to continue growing rapidly, moving ahead, with little allowance for execution mishaps.

However, it’s critical to note that while CEO Jeff Green & team have consistently executed well in a highly challenging 2022 relative to the ad market, The Trade Desk is not immune to macroeconomic headwinds. There are several things that the company can control, but the fallout from the Fed’s interest rate decisions is certainly not one of them.

However, Wall Street analysts still expect the company to thrive in FY23. Accordingly, TTD is projected to report revenue growth of 24.5% in FQ4, in line with the company’s guidance. In addition, its adjusted EBITDA is estimated to increase by 20%, below FQ3’s 32.6% growth.

However, analysts expect The Trade Desk to shrug off the ad industry downturn by posting revenue growth of 16.1% for FQ1’23. Will that be “low enough” for TTD to cross? We urge investors to pay close attention to management’s commentary, which could set the tone for its performance, given its recent recovery.

As the leading independent demand-side platform, The Trade Desk is in an enviable position in the fast-growing Connected TV (CTV) vertical. Even though eMarketer took down its digital ad spending forecasts for social network ad spending, it estimates that CTV ad spending will continue to perform well.

Accordingly, the spending on advertising through CTV in the US is predicted to increase by 27.2% in 2023, reaching nearly $27B. With CTV ads accounting for about 7% of total media ad expenditure, there is significant potential for further growth.

Coupled with Walmart’s (WMT) robust performance in its retail media ads, we believe The Trade Desk’s commerce vertical could see a further boost. Keen investors should recall that Walmart partners with TTD leveraging its tech stack on its retail media ad business.

Walmart has seen solid performance on its ad formats, which “increased by 31% YoY in Q4.” In addition, it has been instrumental in lifting its ad revenue by 40% in 2022. Therefore it suggests that the ad downturn impacted Google (GOOGL) (GOOG) and Meta (META) more significantly, given their market leadership and Apple’s (AAPL) App Tracking Transparency (ATT) challenges.

Hence, The Trade Desk’s prospects in 2023 should look constructive, with CTV likely continuing to make headway against Linear TV as a secular growth driver.

But, we believe the critical question concerning investors has always been about TTD’s valuation and whether the support by buyers is convincing at the current levels?

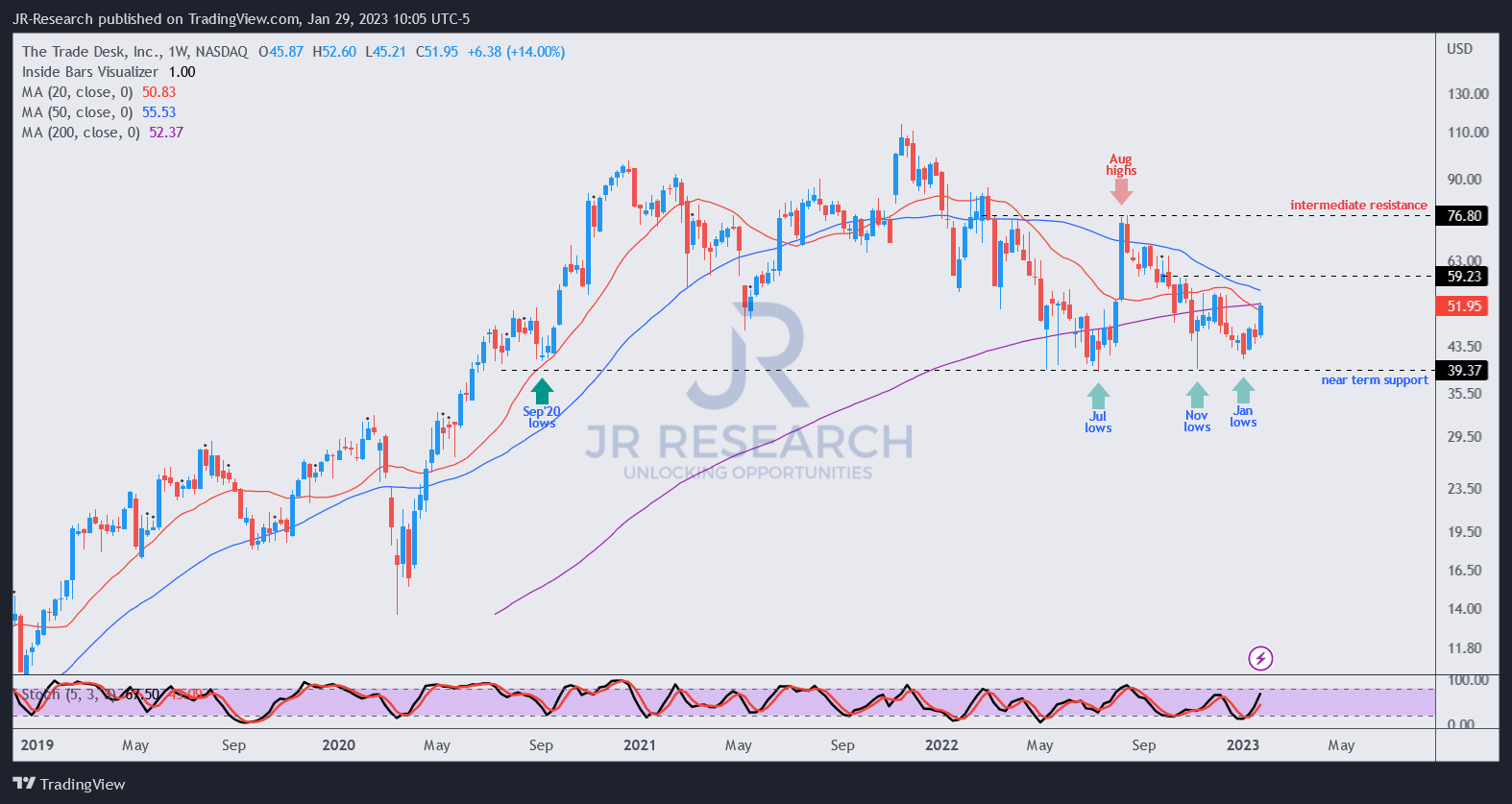

TTD price chart (weekly) (TradingView)

As seen above, TTD’s buyers have shown conviction in defending the stock against further downside at the $40 level.

That level is consistent with significant dip buying price action seen in September 2020, May 2022, July 2022, November 2022, and January 2023.

Hence, investors who demand a higher margin of safety could consider buying the next potential pullback toward those levels.

However, TTD remains deeply entrenched in a medium-term downtrend from which it needs to emerge for a sustainable recovery in 2023.

We also believe its recent optimism may have been reflected in the recovery from its January lows. Hence, the focus will likely turn to management’s outlook for FY23 and whether TTD can continue its expected outperformance against the ad industry.

A weaker-than-anticipated guidance could proffer patient investors the potential dip-buying opportunity.

Rating: Hold (Revise from Buy).

Be the first to comment