LilliDay

The Disinflation Rally Needs to Correct

We are getting ahead of ourselves and need to take profits, accumulate cash to reinvest at lower levels. I think we are in for a 7-10% correction and likely to test the Dec 28th S&P 500 Index (SP500) low of 3,783.

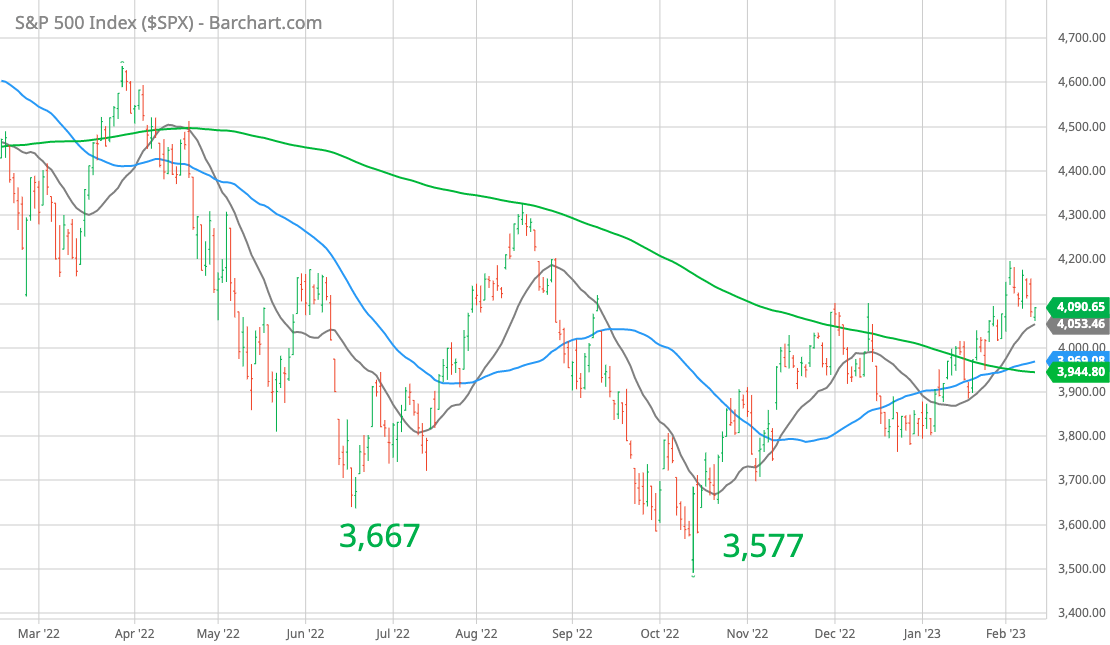

Since the S&P 500 started what I call the “disinflation” rally following a Goldilocks Dec 2022 jobs report, we had added on 10.5% from 3,783 in a month alone, and almost 17% from the Oct 12th bear market bottom of 3,577.

The Disinflation Rally (Seeking Alpha)

S&P 500 – 1Year (Barcharts)

The disinflation rally was a feel good rally, detailed in my article of Jan 23,2023, driven by two narratives – disinflation and recession fears, the key features of which were:

- A benign Dec 2022, jobs report with moderate job growth of 223,000 and lower wage growth of only 4.6%.

- Lower inflation expectations from the Fed Consumer Survey of only 4% compared to Dec 2022’s 4.4%

- Somewhat benign CPI and PPI Readings with drops of 0.1% and 0.5% from the previous month.

Additionally, recessionary signals some of which I’ve noted below, convinced the markets that the Fed would pay heed, put a cap on interest rates and not over tighten as previously thought.

- High reserves provisioning of $6.2Bn from the four large banks.

- A drop of 0.7% MoM in Industrial Production.

- 1.1% MoM, drop in retail sales in December.

- An 18% drop in existing home sales.

As a consequence, in January, the 10 year Treasury dropped from 3.745% on Jan 2nd, to a low of 3.373 on Jan 18, to 3.398 on Feb 2nd. From there it has bounced back to 3.738 erasing almost all its January gains. Clearly, the bond markets don’t feel so good about the Fed’s actions any more.

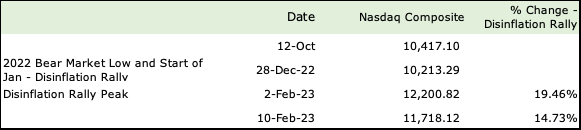

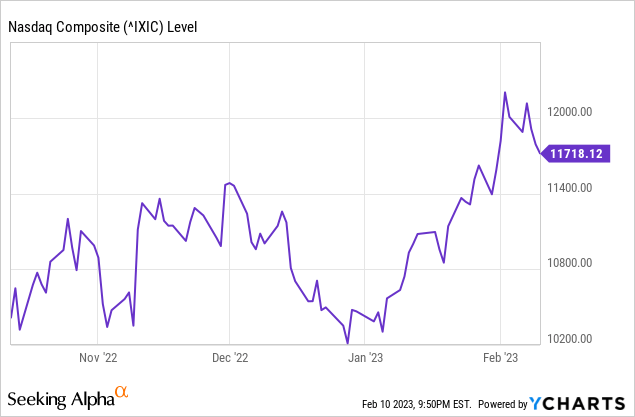

Outperforming the S&P 500, the NASDAQ Composite Index (COMP.IND) shot up a massive 19.5% in a month!. The Nasdaq Composite is much more sensitive to interest rates, given the tech and growth stocks that comprises it.

Nasdaq Composite Jan 2023 Rally (Seeking Alpha)

What has changed – why should we be looking for a correction?

Higher Payrolls – The January 2023, Non Farms Payroll report on Feb 3rd, was a scorcher with 517,000 jobs added, far higher than consensus estimate of 187,000. Wages were higher 0.3% MoM and 4.4% YoY, also 0.1% above expectations. Nothing in it even remotely pointed towards a recession or disinflation. Unlike the December report, Goldilocks wasn’t even in the same country, forget about the room.

Prior to the Feb 3rd jobs report, on Feb 1st, the Feds increased the Fed Funds rate by 25 basis points to 4.5% – 4.75% – in line with expectations. In spite of the 11% rise in the S&P 500 and the 17% rise in the Nasdaq Composite in January, Powell in his prepared remarks did not try to talk down the market, something he had quite forcefully done after the December 2022, Fed meeting.

Higher payrolls lead to higher interest rates – The bond markets thought otherwise and following the excellent job numbers, bond yields began to rise signaling that the battle against inflation is far from over. 10 Year treasuries jumped from January’s lows of 3.398% to 3.738% in the span of a week, erasing all of January’s gains.

Fed Terminal rate expectations, which had stayed steadily below 5% from Oct 2022 to January 2023 has now crept back up over 5%, a difference of over 25 basis points. According to a Bloomberg Feb 8th article

Overnight index swaps are still priced for easing later this year. At the moment, they show the Fed’s benchmark peaking around 5.17%

After the Feb 1st Fed meeting, expectations had dropped to a possible 25 basis point hike in March and no chances of a hike in May. Clearly, that is not the case today with expectations of an almost certain 25 basis point hike in March, a likely 25 basis point hike in May, and to top it all, the same Bloomberg article also cites an $18Mn wager on the terminal rate reaching 6% by September.

I would certainly factor these before investing in the market.

Higher interest rates with weak earnings beget lower multiples

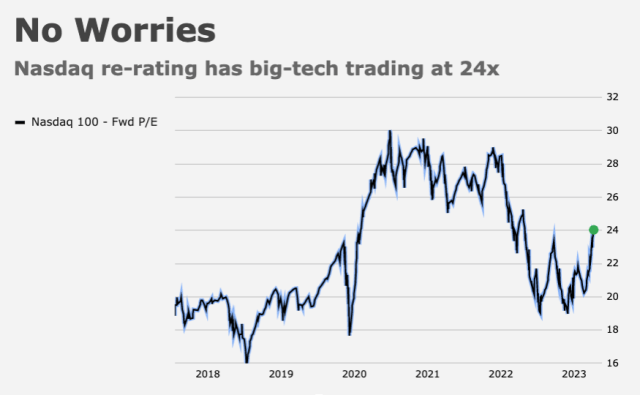

Probably, the biggest sign of complacency and over optimism is the re-rating of the Nasdaq 100 (NDX:IND). Leaving aside the crazy multiples during Covid, when tech seemed unconquerable; today at a forward P/E of 24, we are still way ahead of 2018-2020 P/E’s of 16-20. Taken at a mid-point of a P/E of 18, we are ahead by a whopping 33%!

The Nasdaq 100 (The Heisenberg Report)

One could understand the market’s enthusiasm if earnings were rising, but sadly, we seem to have forgotten that they’re waning in a big way. Here are the mega 5 Dec 2022 earnings and Mar 2023 guidance as an example:

Tech Earnings (Seeking Alpha)

There was only one positive increase in earnings for Q4-2022 from the big 5, Microsoft, (MSFT) a soft 2% increase and an even softer 1% guidance for the March, quarter after a 3 month revision downward of 5%! Apple (AAPL), Alphabet (GOOG), Amazon (AMZN) and Meta (META) all decreased earnings and guided lower, even after previously lowered guidance!. The numbers leave you numb and in my opinion, the markets giving the mega caps a thumbs up is a big mistake. I believe we will definitely see these mega caps drop.

Also, somewhere we have gotten into this mindset that a P/E of 24 is OK, just because it is a much lower multiple than the peak of 30! That multiple was a serious anomaly based on the pandemic and unless we get out of that mindset, we’re very likely to keep repeating the same mistake. I was speaking to a very large portfolio manager two days ago; he’s quite cautious and conservative and sitting on about 20% cash, but even he wistfully said that “The Nasdaq Comp was down 34% from its 16,057 peak and that’s a lot”; Thankfully, he quickly reminded himself that compared to 2012-2020 valuations, yes, historically the NASDAQ 100 was still stretched and that too in a much higher inflation and interest rate regime.

One of last year’s best performing analysts, Mike Wilson of Morgan Stanley reiterated his bearish call on the markets as early as January 23rd.

In bear markets like last year’s, when just about everyone lost money, investors lose confidence,” Morgan Stanley’s Mike Wilson said, in his latest note, exhorting market participants to “ignore the noise” and trust the process.

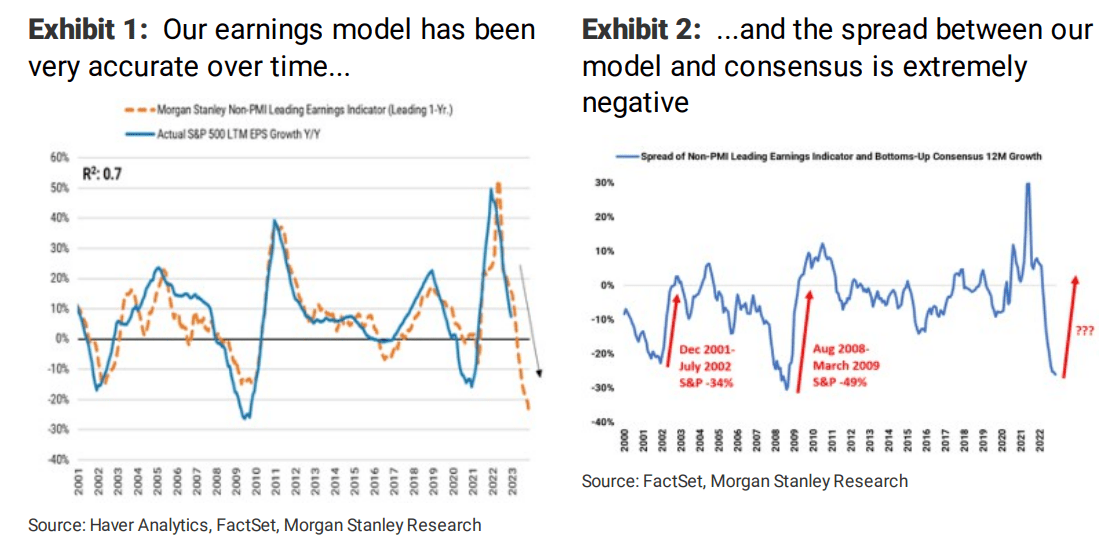

I couldn’t agree more – weak economic indicators presage earnings drops and even as we celebrate a likely lower interest rate regime in 2023 with a rousing rally, we are ignoring a very precarious corporate earnings season. In my article in January, I had listed several economic indicators that pointed towards a weak year ahead. The team at Morgan Stanley shows how closely correlated PMI indicators are to earnings.

S&P 500 and PMI’s (Heisenberg Report, Haver Analytics, FactSet, Morgan Stanley Research)

An Unsustainable Rally

Several other indicators also convince me that the rally has run out of steam.

A large part of the run up was short covering and low positioning – A lower S&P VIX Index (VIX), which led to about $140Bn of CTA buying had propelled the markets in January according to Nomura. In January, the VIX dropped from the low 20’s to 18, but in the long run a level around 18 can be a sign of complacency and a good contrarian indicator.

The VIX led rally has run its course and is highly unlikely to continue — chances of a further melt up are slim to none.. Marko Kolanovic, chief strategist at JP Morgan, also wrote that fund managers were not fully invested – many had new allocations come in January and in the frenzy had to keep buying. Positioning, since then has moved up substantially. Given the strength of the jobs report, Marko believes that Goldilocks is drenched and the focus should shift to weak earnings.

The meme stock rally and the massive build up in options trading are signs of weakness. From the linked Barron’s article:

These short-term options have succeeded meme stocks as the Street’s gambling vehicle of choice, adds Peter Tchir, the derivatives maven who heads macro strategy at Academy Securities. About 90% of his recent conversations are about 0DTE, he relates in an email. And Thursday saw record call-option volume, with the vast majority of expirations on Feb. 2 and Feb. 3. The SPDR S&P 500 exchange-traded fund (NYSEARCA:SPY) usually leads the most-active list; Tesla (TSLA) does the same among single stocks.

It’s been a while since I heard the word YOLO (You Only Live Once) and when YOLO trading is making its way back into the market narrative, it’s time to look for the exits. Low quality and speculative traders dominating the market chasing momentum never ends well.

Should we buy and hold through the correction?

From 1935, the S&P 500 has fallen more than 20% in a calendar year on only 5 occasions.

1937, 1974, 2002, 2008 and 2022. (In 2022, the index closed at 3,839.50 or 19.44% lower but was lower than 20% at its bottom). I’ve excluded the great depression years of 1930-1931.

On all four occasions the S&P 500 has rebounded positively the next year. Given that, there is an 80% chance that the S&P 500 will close above its 3,839.50 (Dec 30th, 2022 closing). Thus begs the question from a buy and hold investor – Since 3,839.50 is just 6% lower than the current index of 4,096, why worry about a correction and subsequent rebound? If that were the case, why would we risk shorting the market or trading in a market that is expected to rebound in less than a year. Is it worth the risk?

I, myself have a 2023 year end target of 4,150 based on two assumptions:

a) S&P 500’s earnings will drop only 5% to $210 in 2023 and rebound to $237 in 2024, b) 10 year treasuries will hold between 3.25 and 3.50% during second half of 2023, so I’m not a bear for sure. However, I strongly believe that we will see a correction to at least 3,783, (8% lower) from where we started the disinflation rally and the S&P 500 is also likely to test its Oct 12th bottom of 3,577 (13% lower), based on the following reasons.

- Q1 earnings are likely to go further south and Q2 guidance would be poor – From the very light punishment doled out to the mega 5 market leaders, I had cited above, the markets are pricing in poor earnings incorrectly. In Meta’s case, its stock price went up 20% on a 30% weaker earnings guidance because of a vague promise of cost cutting and a $40Bn buyback! Looks like Reality Labs is reality in name only…

- The January rally was based entirely on some disinflation, a dovish Fed, short covering, the return of meme stocks and excessive options trading on momentum. Disinflation and a dovish Fed, in my opinion is still too early to call – their work is still not done. Lower oil prices was one of the primary reasons for the drop in inflation and with Russia curbing production today and China reopening, it is too premature to tag lower oil prices for 2023. We could see some inflation creeping up again this summer. Short covering is not sustainable, meme stock buying and excessive options trading usually end badly and take the markets down with them.

Given the tenuous state of the markets, I will keep taking profits and setting aside cash to buy back at lower levels. There are other alternatives and cash doesn’t lose money. A decent money market account offers you close to 4% and a CD tops 5% — if the investment is not priced right there is no need to rush in. Cash is not trash when Lyft Inc (LYFT) drops 36% in one day.

I won’t touch my core buy and hold investment holdings in my retirement accounts of course; but, there is no point in chasing momentum or what I believe are incorrect multiples. 2022 was an extremely difficult year and not taking enough profits in late 2021 and early 2022 when the returns far exceeded targets, turned to be very costly.

Trading Strategy

Besides my retirement accounts, which are pure Buy and Hold investments, I also keep a trading account to buy on dips and take profits of the same, when the markets get over heated or valuations get out of whack. As long as we remain in a bear market with uncertainty about inflation, recession and interest rates, trading will be a focus area in 2023.

I have trimmed a few positions including my largest holding, the red hot Nvidia (NVDA), which greatly appreciated from Microsoft AI foray, because of the need to use the best quality GPU’s to power their applications.

NVIDIA – Core holding, bought between $147-$160 in my trading account, trimmed 40% around $220, will buy back between $180 and $200. Q4-2023 results should be interesting as will be the guidance.

Unity Software (U) – Bought $24-$26, sold 60% around $34-$38, will buy back around $30. It has a lot going for it, but 2023 is a tough year for ad-tech.

AMD (AMD) – Added in the mid 60’s in my trading account, trimmed 60% around $80. Plan to hold the rest.

Taiwan Semiconductor Manufacturing (TSM) – Core Holding. Added between $75-80 in my trading account, sold 30%, will hold the rest.

Teradyne (TER) – Core Holding, constant buying on dips, last bought in the mid 90’s recommended since $79 and will buy more below $100.

Microsoft – Core Holding – will add below $240 – the AI hype has gotten ahead of itself.

Alphabet – Core Holding – can add between $80 and $85. I think the markets have overreacted on the AI and search engine issues, but I think the advertising market is still weak.

SPDR S&P 500 Trust ETF (SPY) Added around 384-388, hold for now, buy below 370.

Be the first to comment